|

市場調查報告書

商品編碼

2061708

德國潤滑油市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Germany Lubricants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

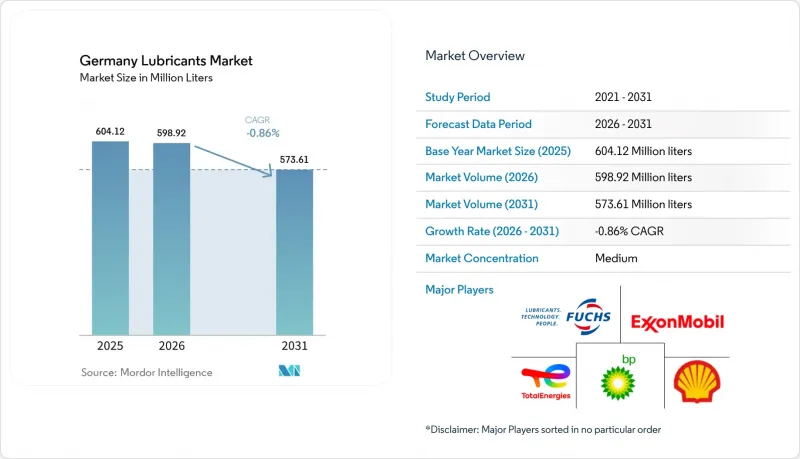

根據 Mordor Intelligence 預測,德國潤滑油市場將從 2025 年的 6.0412 億公升萎縮至 2026 年的 5.9892 億公升,然後從 2026 年到 2031 年以 -0.86% 的複合年成長率成長,到 2031 年達到 5.731 億升。

本報告按產品類型(汽車引擎油、工業引擎油、變速箱油、齒輪油、煞車油、液壓油、潤滑脂、加工油)、終端用戶產業(汽車、船舶、航太、重型機械、工業)和基礎油類型(礦物油、合成油、半合成油、生物基油)進行分類。市場預測以體積(公升)為單位。

德國潤滑油市場趨勢與洞察

製造業採購經理人指數的復甦提振了金屬加工產業對液壓油的需求。

2025年12月,德國機械和汽車工廠的產量在經歷大幅下滑後趨於穩定。隨後,每次批量進貨量(PMI)的增加都帶動了對金屬切削製程的需求。整合物聯網感測器的預測性維護乳液成功延長了油箱壽命,從而減少了浪費。巴登-符騰堡州的供應商已開始將冷卻液補充與CNC工具機運轉率掛鉤,顯著減少了停機時間。同時,從甲醛釋放劑轉向酯類半合成油,有助於在不影響表面光潔度的前提下,符合ISO 6743-7標準。隨著生產的穩定,這些製程改進將產生協同效應,即使在德國潤滑油市場萎縮的情況下,也能帶來適度的銷售量成長。

電動車專用電子流體和溫度控管油

德國汽車工業協會 (VDA) 預測,到 2026 年,電池式電動車(BEV) 的註冊量將顯著成長,而 2024 年的成長則較為緩慢。每輛純電動車都需要一種導熱係數超過 0.15 W/m*K 的介電冷卻液,以及一種用於電氣絕緣和減少摩擦的特殊電橋油。工廠的加註供應合約有助於提高動力傳動系統的效率。專為電動車電池設計的合成酯類冷卻液可確保在寬廣的溫度範圍內保持黏度穩定性。隨著汽車產業向電氣化轉型,這些專用液體正成為德國潤滑油市場成長最快的細分領域。

歐洲煉油廠的關閉導致基礎油供應緊張。

英國石油公司(BP)宣布計劃關閉位於蓋爾森基興的原油加工廠。同時,殼牌公司已將位於韋瑟林的工廠改造為能夠生產III類基礎油的基地。近年來,德國基礎油銷售量大幅下滑,迫使調配商從ARA(美國基礎油協會)的樞紐採購高品質基礎油。此外,缺乏長期採購協議的中小型調配商正面臨利潤率下滑的壓力,這種情況可能會加速產業整合。

細分市場分析

預計到2025年,汽車引擎機油將成為市場主導,佔29.72%。然而,0W-16和0W-20等超低黏度機油的出現徹底改變了市場格局,減少了加註量,並顯著延長了換油週期。金屬加工油是唯一呈現正向趨勢的領域,在採購經理人指數(PMI)回升的推動下,預計到2031年將以0.06%的複合年成長率穩定成長。合成渦輪機油和變壓器油則受益於離岸風力發電專案和電網升級帶來的需求成長。同時,煞車油升級至DOT 5.1標準,以更好地應對再生煞車產生的高溫。因此,德國機油市場的萎縮速度超過了整體市場的下滑速度。

到2025年,工業用油、變速箱油和齒輪油將佔據相當大的市場佔有率,這主要得益於商用車隊偏好的長換油週期。液壓油和潤滑脂曾佔據相當大的市場佔有率,但面臨電液執行器替代品的競爭。在基礎礦物油產品市場佔有率下滑的情況下,採用基於物聯網的狀態監測技術的特種混合油在德國潤滑油市場開闢了一片新天地。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 製造業採購經理人指數的復甦提振了金屬加工液的需求。

- 電動車專用電子流體和溫度控管油

- 離岸風電和綠氫能對渦輪機液的需求

- 歐盟電池法規促進電解領域的專業知識發展。

- 透過CSRD廣泛使用再精煉基礎油

- 市場限制因素

- 歐洲煉油廠的關閉導致基礎油供應短缺。

- 即將推出的 PFAS 法規對高溫潤滑脂構成威脅。

- 取消電動車補貼正在扭曲特種流體的成分。

- 價值鏈分析

- 法律規範

- 終端用戶趨勢

- 汽車產業

- 製造業

- 發電業

- 波特五力模型

第5章 市場規模與成長預測

- 依產品類型

- 汽車引擎油

- 工業機油

- 變速箱油

- 齒輪油

- 煞車油

- 油壓

- 潤滑脂

- 加工油(包括橡膠加工油和白油)

- 金屬加工潤滑劑

- 渦輪機油

- 變壓器油

- 其他產品類型

- 按最終用戶行業分類

- 車

- 搭乘用車

- 商用車輛

- 摩托車

- 海上

- 航太

- 重型機械

- 建造

- 礦業

- 農業

- 產業

- 發電

- 冶金與金屬加工

- 紡織品

- 石油和天然氣

- 其他終端用戶產業

- 車

- 依基材類型

- 礦物油性潤滑劑

- 合成潤滑油

- 半合成潤滑油

- 生物性潤滑劑

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- ADDINOL

- BP plc

- Carl Bechem GmbH

- Exxon Mobil Corporation

- FUCHS

- Kluber Lubrication

- LIQUI MOLY GmbH

- Quaker Chemical Corporation

- ROWE Mineralolwerk GmbH

- SCT Lubricants

- Shell plc

- TotalEnergies

- Valvoline

- Zeller+Gmelin

第7章 市場機會與未來展望

第8章:執行長面臨的關鍵策略挑戰

According to Mordor Intelligence, the germany lubricants market size is expected to decline from 604.12 million liters in 2025 to 598.92 million liters in 2026 and is forecast to reach 573.61 million liters by 2031 at -0.86% CAGR over 2026-2031.

This report is Segmented by Product Type (Automotive Engine Oil, Industrial Engine Oil, Transmission Fluids, Gear Oil, Brake Fluids, Hydraulic Fluids, Greases, Process Oil, and More), End-User Industry (Automotive, Marine, Aerospace, Heavy Equipment, and Industrial), Base Stock Type (Mineral Oil-Based, Synthetic, Semi-Synthetic, and Bio-Based). Market Forecasts are Provided in Volume (Liters).

Germany Lubricants Market Trends and Insights

Manufacturing-PMI Rebound Lifting Metalworking Fluids

In December 2025, Germany's machinery and motor-vehicle plants experienced a significant dip in output before stabilizing. Every uptick in the PMI subsequently bolstered the demand for metal-cutting. Predictive-maintenance emulsions, now integrated with IoT sensors, have successfully extended sump life, leading to a reduction in disposal volumes. Suppliers in Baden-Wurttemberg have already begun synchronizing coolant replenishment with CNC utilization, achieving a notable reduction in downtime. Meanwhile, a shift from formaldehyde releasers to ester-based semi-synthetics has allowed for easy compliance with ISO 6743-7, ensuring surface finish quality isn't compromised. As production stabilizes, these process enhancements are expected to compound, driving modest volume growth even in a contracting German lubricants market.

EV-Specific E-Fluids and Thermal-Management Oils

By 2026, the Verband der Automobilindustrie forecasts significant growth in battery electric vehicle (BEV) registrations compared to the subdued figures of 2024. Each BEV necessitates dielectric coolants with thermal conductivity greater than 0.15 W/m*K, alongside e-axle oils specifically formulated for electrical insulation and reduced friction. Contracts for factory-fill supplies enhance drivetrain efficiency. Synthetic-ester coolants designed for electric vehicle batteries ensure viscosity stability across a wide temperature range. As automotive fleets transition to electric, these specialized fluids are emerging as the most rapidly expanding segment in Germany's lubricants market.

European Refinery Closures Tightening Base-Oil Supply

BP has announced plans to close down its crude capacity at Gelsenkirchen. Meanwhile, Shell repurposed its Wesseling facility into a site capable of producing Group III base oil. In recent years, Germany experienced a significant decline in base-oil sales, which compelled blenders to source premium stocks from the ARA hub. Additionally, smaller formulators, lacking long-term offtake contracts, have been grappling with margin compression, a situation that could hasten industry consolidation.

Other drivers and restraints analyzed in the detailed report include:

- Offshore-Wind and Green-Hydrogen Turbine-Fluid Demand

- EU Batteries Regulation Fostering Electrolyte Know-How

- Upcoming PFAS Ban Threatening High-Temp Greases

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Automotive engine oil dominated at 29.72% in 2025. However, ultra-low-viscosity formulations such as 0W-16 and 0W-20 revolutionized the market, allowing for fill volume reductions and extending service intervals significantly. Metalworking fluids show the only positive trend, inching forward at 0.06% CAGR through 2031 as PMI rebounds. Synthetic turbine and transformer oils rode the wave of demand from offshore wind projects and grid upgrades. Meanwhile, brake fluids evolved, with upgrades to DOT 5.1 to better handle the intense heat from regenerative braking. Consequently, the market for engine oils in Germany contracted at a pace outstripping the broader market decline.

In 2025, industrial oil, transmission fluid, and gear oil collectively commanded a significant portion of the market volume, bolstered by long drain intervals favored by commercial fleets. Hydraulic fluids and greases, accounting for a notable share, faced competition from electro-hydraulic actuation substitutes. In a market where basic mineral products waned, specialty blends that leveraged IoT condition monitoring carved out a niche in the German lubricants landscape.

List of Companies Covered in this Report:

- ADDINOL

- BP p.l.c.

- Carl Bechem GmbH

- Exxon Mobil Corporation

- FUCHS

- Kluber Lubrication

- LIQUI MOLY GmbH

- Quaker Chemical Corporation

- ROWE Mineralolwerk GmbH

- SCT Lubricants

- Shell plc

- TotalEnergies

- Valvoline

- Zeller+Gmelin

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Manufacturing-PMI rebound lifting metal-working fluids

- 4.2.2 EV-specific e-fluids and thermal-management oils

- 4.2.3 Offshore-wind and green-hydrogen turbine-fluid demand

- 4.2.4 EU Batteries Regulation fostering electrolyte know-how

- 4.2.5 CSRD-driven uptake of re-refined base oils

- 4.3 Market Restraints

- 4.3.1 European refinery closures tightening base-oil supply

- 4.3.2 Upcoming PFAS ban threatening high-temp greases

- 4.3.3 EV-subsidy withdrawal distorting specialty-fluid mix

- 4.4 Value Chain Analysis

- 4.5 Regulatory Framework

- 4.6 End-User Trends

- 4.6.1 Automotive Industry

- 4.6.2 Manufacturing Industry

- 4.6.3 Power Generation Industry

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Automotive Engine Oil

- 5.1.2 Industrial Engine Oil

- 5.1.3 Transmission Fluids

- 5.1.4 Gear Oil

- 5.1.5 Brake Fluids

- 5.1.6 Hydraulic Fluids

- 5.1.7 Greases

- 5.1.8 Process Oil (Including Rubber Process Oil and White Oil)

- 5.1.9 Metalworking Fluids

- 5.1.10 Turbine Oil

- 5.1.11 Transformer Oil

- 5.1.12 Other Product Types

- 5.2 By End-user Industry

- 5.2.1 Automotive

- 5.2.1.1 Passenger Vehicles

- 5.2.1.2 Commercial Vehicles

- 5.2.1.3 Two-Wheelers

- 5.2.2 Marine

- 5.2.3 Aerospace

- 5.2.4 Heavy Equipment

- 5.2.4.1 Construction

- 5.2.4.2 Mining

- 5.2.4.3 Agriculture

- 5.2.5 Industrial

- 5.2.5.1 Power Generation

- 5.2.5.2 Metallurgy and Metalworking

- 5.2.5.3 Textiles

- 5.2.5.4 Oil and Gas

- 5.2.5.5 Other End-Use Industries

- 5.2.1 Automotive

- 5.3 By Base Stock Type

- 5.3.1 Mineral Oil-Based Lubricants

- 5.3.2 Synthetic Lubricants

- 5.3.3 Semi-Synthetic Lubricants

- 5.3.4 Bio-Based Lubricants

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 ADDINOL

- 6.4.2 BP p.l.c.

- 6.4.3 Carl Bechem GmbH

- 6.4.4 Exxon Mobil Corporation

- 6.4.5 FUCHS

- 6.4.6 Kluber Lubrication

- 6.4.7 LIQUI MOLY GmbH

- 6.4.8 Quaker Chemical Corporation

- 6.4.9 ROWE Mineralolwerk GmbH

- 6.4.10 SCT Lubricants

- 6.4.11 Shell plc

- 6.4.12 TotalEnergies

- 6.4.13 Valvoline

- 6.4.14 Zeller+Gmelin

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

8 Key Strategic Questions for CEOs

潤滑油和潤滑脂市場預測至2034年-按產品類型、基礎油、增稠劑類型、應用、最終用戶、分銷管道和地區分類的全球分析

潤滑油和潤滑脂市場預測至2034年-按產品類型、基礎油、增稠劑類型、應用、最終用戶、分銷管道和地區分類的全球分析 特種潤滑油市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、最終用戶、地區和競爭格局分類,2021-2031年

特種潤滑油市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、最終用戶、地區和競爭格局分類,2021-2031年 鑽井潤滑劑市場規模、佔有率和成長分析:按產品類型、應用、功能和地區分類-2026-2033年產業預測

鑽井潤滑劑市場規模、佔有率和成長分析:按產品類型、應用、功能和地區分類-2026-2033年產業預測 海上潤滑油市場規模、佔有率和趨勢分析報告:按應用、最終用途、地區和細分市場分類(2026-2033 年)機器人潤滑劑市場預測至2034年—按產品類型、潤滑劑類型、應用、最終用戶和地區分類的全球分析

海上潤滑油市場規模、佔有率和趨勢分析報告:按應用、最終用途、地區和細分市場分類(2026-2033 年)機器人潤滑劑市場預測至2034年—按產品類型、潤滑劑類型、應用、最終用戶和地區分類的全球分析 歐洲潤滑油:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

歐洲潤滑油:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 拉絲潤滑劑市場:2026-2032年全球市場預測(依產品類型、添加劑類型、線材類型、應用、終端用戶產業和銷售管道分類)

拉絲潤滑劑市場:2026-2032年全球市場預測(依產品類型、添加劑類型、線材類型、應用、終端用戶產業和銷售管道分類) 潤滑油市場:依產品類型、基礎油、終端用戶產業及地區分類(2026-2034 年)獨立潤滑油製造商市場報告:按類型、應用和地區分類(2026-2034 年)外科潤滑劑市場:按類型、應用、最終用戶和分銷管道分類-2026-2032年全球市場預測

潤滑油市場:依產品類型、基礎油、終端用戶產業及地區分類(2026-2034 年)獨立潤滑油製造商市場報告:按類型、應用和地區分類(2026-2034 年)外科潤滑劑市場:按類型、應用、最終用戶和分銷管道分類-2026-2032年全球市場預測