|

市場調查報告書

商品編碼

2061709

歐洲潤滑油:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Europe Lubricants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

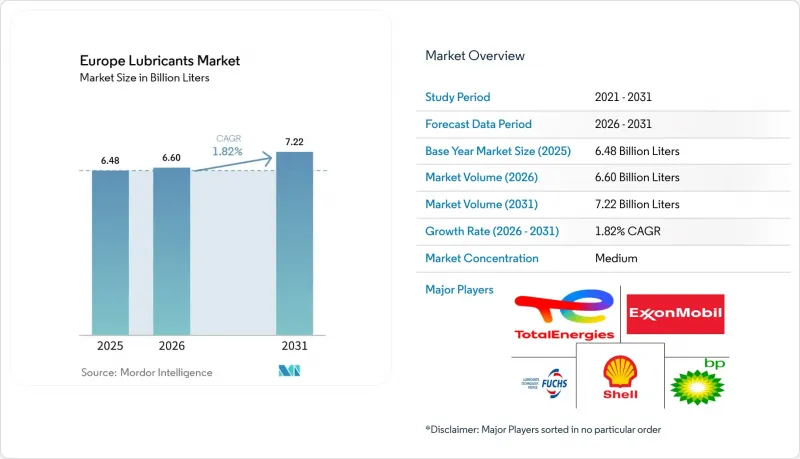

根據 Mordor Intelligence 預測,歐洲潤滑油市場將從 2025 年的 64.8 億公升成長到 2026 年的 66 億公升,到 2031 年將達到 72.2 億公升,2026 年至 2031 年的複合年成長率為 1.82%。

本報告按產品類型(汽車引擎油、工業引擎油、齒輪油等)、基料類型(礦物油、合成油、半合成油、生物基油)、終端用戶產業(汽車、船舶、航太等)和地區(法國、德國、義大利、俄羅斯、西班牙、英國及其他歐洲國家)進行細分。市場預測以公升為單位。

歐洲潤滑油市場趨勢與洞察

中歐和東歐的工業復甦和快速自動化

2025年,中東歐(CEE)製造業產出呈現強勁成長態勢,其中波蘭工業生產指數顯著提升(4.2%),捷克零組件產業(為德國原始設備製造商供應零件)成長8%。這一成長主要得益於對用於電池外殼和電機疊片精密加工的金屬加工液的需求。匈牙利在2024年至2025年間獲得了18億歐元(19.5億美元)的電池工廠投資。每座超級工廠都需要用於自動化生產線的熱力流體和液壓流體。羅馬尼亞鋼鐵廠和波蘭鑄造廠向工業4.0的升級改造,增加了對用於渦輪機和壓縮機的潤滑油的需求,這些潤滑油支持感測器驅動的維護。買家對液壓系統的ISO 12925-1清潔度標準的要求日益提高,使得潤滑油品質成為採購決策的關鍵因素。這些趨勢正在推動工業流體市場的銷售和利潤率成長。

疫情後汽車擁有量的恢復

到2025年,歐洲的汽車保有量將達到2.52億輛,平均車齡車齡12.5年,位居世界第一。儘管新車註冊量正向混合動力汽車和電池式電動車傾斜,但舊款引擎仍消耗大量機油,支撐著售後市場的需求。柴油車仍佔汽車總量的40%,因此,歐盟6d柴油車需要同時使用高SAPS和低SAPS配方的機油。到2025年,電池式電動車僅佔汽車總量的1.8%,因此它們對引擎油需求的即時影響有限。混合動力汽車越來越依賴低黏度等級的機油,例如0W-16和0W-20,以提高燃油效率。在商用車領域,合成機油的使用將換油週期延長至10萬公里,這在銷售和利潤率之間造成了權衡,使高階潤滑油供應商受益。

原油和添加劑價格的波動給利潤率帶來了壓力。

2025年布蘭特原油均價為每桶82美元,2026年初維持在每桶84美元左右。基礎油價格與原油價格密切相關,由於零售價格未能跟上成本上漲的步伐,調配商的利潤率面臨壓力。 2024年至2025年,由於供應商數量有限,二硫化鉬和ZDDP濃縮物的供應受限,導致添加劑包成本上漲12%。義大利和西班牙的中小型調配商報告稱,2025年第四季部分SKU的毛利率為負。此外,強勢美元推高了以歐元計價的進口成本,進一步擠壓了面向北非和中東市場的出口商的利潤空間。

細分市場分析

截至2025年,汽車機油佔總銷售量的39.12%,而潤滑脂預計將以2.07%的複合年成長率(CAGR)持續成長至2031年。鋰基潤滑脂在該領域佔據主導地位,約佔整個品類的60%,廣泛應用於電動車的輪轂軸承和風力發電機的葉片變槳機構。由於其卓越的防銹性能,磺酸磺酸鹽基潤滑脂在船舶和非公路應用領域越來越受歡迎。在波蘭、捷克和匈牙利,金屬加工液的需求正在成長,這主要得益於電池零件加工需要低發泡乳液以延長刀具壽命。與此同時,變速箱油的需求正在放緩。這是因為混合動力汽車的雙離合器系統比傳統自動變速箱需要更少的油。另一方面,由於車輛老化,煞車油的消耗量保持穩定。

此外,潤滑脂因其能夠承受離岸風力發電機和高速電動車軸承中的極端溫度,而具有很高的利潤率。在中東歐地區,液壓油在建築和採礦業的應用日益廣泛,林業和海上設備必須使用標有HEES標籤的酯類混合物。渦輪機油正逐步轉向III類和IV類合成油,從而實現五年更換週期,並減少高峰發電廠和風電場的停機時間。變壓器油的升級正在支持德國和法國電網的現代化,其中酯類油提高了都市區變電站的防火安全性。輪胎製造和製藥業對加工油的需求正轉向符合REACH法規中多環芳烴(PAH)含量閾值的加工分餾芳烴萃取物。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 中歐和東歐的工業復甦和快速自動化

- 疫情後汽車擁有量的恢復

- 離岸風力發電的擴張需要齒輪油和油壓油。

- 循環經濟架構下的精煉基礎油法規

- 人工智慧驅動的預測性維護正在提升對維護液的需求。

- 市場限制因素

- 原油價格和添加劑價格的波動給利潤率帶來了壓力。

- 歐盟關於阻燃液中 PFAS 和磷酸酯的法規

- 風力發電機齒輪箱中使用的終身填充潤滑油正在抑製售後市場的發展。

- 價值鏈分析

- 法律規範

- 終端用戶趨勢

- 汽車產業

- 製造業

- 發電業

- 波特五力模型

第5章 市場規模與成長預測

- 依產品類型

- 汽車引擎油

- 工業機油

- 變速箱油

- 齒輪油

- 煞車油

- 油壓

- 潤滑脂

- 加工油(包括橡膠加工油和白油)

- 金屬加工潤滑劑

- 渦輪機油

- 變壓器油

- 其他產品類型

- 依基材類型

- 礦物油性潤滑劑

- 合成潤滑油

- 半合成潤滑油

- 生物性潤滑劑

- 按最終用戶行業分類

- 車

- 搭乘用車

- 商用車輛

- 摩托車

- 海上

- 航太

- 重型機械

- 建造

- 礦業

- 農業

- 產業

- 發電

- 冶金與金屬加工

- 紡織品

- 石油和天然氣

- 其他終端用戶產業

- 車

- 按地區

- 法國

- 德國

- 義大利

- 俄羅斯

- 西班牙

- 英國

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- BP plc

- Chevron Corporation

- Eni SpA

- Exxon Mobil Corporation

- FUCHS

- Gazpromneft

- Idemitsu Kosan Co. Ltd

- Kluber Lubrication

- Liqui Moly GmbH

- Lukoil

- MOL Hungary

- Repsol

- Rosneft

- Shell plc

- TotalEnergies

第7章 市場機會與未來展望

第8章:執行長面臨的關鍵策略挑戰

According to Mordor Intelligence, the europe lubricants market size is expected to grow from 6.48 Billion Liters in 2025 to 6.60 Billion Liters in 2026 and is forecast to reach 7.22 Billion Liters by 2031 at 1.82% CAGR over 2026-2031.

This report is Segmented by Product Type (Automotive Engine Oil, Industrial Engine Oil, Gear Oil, and More), Base Stock Type (Mineral Oil-Based, Synthetic, Semi-Synthetic, and Bio-Based), End-User Industry (Automotive, Marine, Aerospace, and More), and Geography (France, Germany, Italy, Russia, Spain, United Kingdom, and Rest of Europe). The Market Forecasts are Provided in Terms of Volume (Liters).

Europe Lubricants Market Trends and Insights

Industrial Rebound And Automation Surge In CEE

Manufacturing output in Central and Eastern Europe saw robust growth in 2025, highlighted by a 4.2% rise in Poland's industrial production index and an 8% expansion in the Czech component sector supplying German OEMs. This growth has driven demand for metalworking fluids used in precision machining of battery housings and motor laminations. Hungary secured EUR 1.8 billion (USD 1.95 billion) in battery-plant investments during 2024-2025, with each gigafactory requiring heat-transfer and hydraulic oils for automated production lines. Industry 4.0 upgrades in Romanian mills and Polish foundries have increased the need for turbine and compressor lubricants, which support sensor-driven maintenance. Buyers are increasingly demanding ISO 12925-1 cleanliness standards for hydraulic systems, embedding lubricant quality into procurement decisions. These developments collectively boost both volume and margins in the industrial fluids market.

Post-Pandemic Vehicle-Parc Recovery

Europe's car fleet reached 252 million units in 2025, maintaining its status as the oldest globally, with an average age of 12.5 years. Older engines continue to consume more oil, supporting aftermarket sales despite a shift in new registrations toward hybrids and battery-electric vehicles. Diesel vehicles still make up 40% of the fleet, necessitating the coexistence of high-SAPS and low-SAPS formulations for Euro 6d diesels. Battery-electric vehicles accounted for only 1.8% of the fleet in 2025, limiting their immediate impact on engine oil demand. Hybrid vehicles increasingly rely on low-viscosity grades like 0W-16 and 0W-20, which enhance fuel efficiency. Commercial fleets are extending oil drain intervals to 100,000 kilometers by using synthetic formulations, creating a volume-for-margin trade-off that benefits premium lubricant suppliers.

Volatile Crude-Oil And Additive Prices Squeeze Margins

Brent crude oil averaged USD 82 per barrel in 2025 and remained near USD 84 in early 2026. Base-oil prices closely tracked crude trends, compressing blender margins when retail prices lagged behind cost increases. Additive package costs rose by 12% during 2024-2025 due to supply constraints for molybdenum disulfide and ZDDP concentrates, which are produced by a limited number of suppliers. Smaller blenders in Italy and Spain reported negative gross margins on certain SKUs in Q4 2025. Additionally, the strength of the US dollar inflated euro-denominated import costs, further pressuring margins for exporters targeting North Africa and the Middle-East.

Other drivers and restraints analyzed in the detailed report include:

- Offshore-Wind Build-Out Needs Gear And Hydraulic Lubes

- Circular-Economy Mandates For Re-Refined Base Oils

- EU PFAS And Phosphate-Ester Restrictions In Fire-Resistant Fluids

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The automotive engine oil accounted for a 39.12% volume share in 2025, while greases are expected to grow at the fastest 2.07% CAGR through 2031. Lithium-complex greases dominate the segment, representing approximately 60% of the category, and are widely used in electric vehicle wheel bearings and wind turbine blade-pitch mechanisms. Calcium-sulfonate greases are gaining popularity in marine and off-highway applications due to their enhanced rust protection. Metalworking fluids are witnessing increased demand in Poland, the Czech Republic, and Hungary, driven by battery-component machining that requires low-foaming emulsions to extend tool life. Meanwhile, transmission fluid demand is moderating as hybrid dual-clutch systems require smaller oil volumes compared to traditional automatics, while brake fluid consumption remains stable, supported by an ageing vehicle fleet.

Greases also offer high margins due to their ability to withstand extreme temperatures in offshore turbines and high-speed EV bearings. Hydraulic fluid usage is expanding in Central and Eastern Europe (CEE) construction and mining sectors, with HEES-labeled ester blends mandated for forestry and offshore equipment. Turbine oils are transitioning to Group III and Group IV synthetics, enabling five-year drain intervals and reducing downtime in peaker plants and wind farms. Transformer oil upgrades are supporting grid modernization in Germany and France, where ester-based fluids enhance fire safety for urban substations. Process oil demand in tire manufacturing and pharmaceuticals is shifting toward treated distillate aromatic extracts that comply with REACH thresholds for PAH content.

List of Companies Covered in this Report:

- BP p.l.c.

- Chevron Corporation

- Eni SpA

- Exxon Mobil Corporation

- FUCHS

- Gazpromneft

- Idemitsu Kosan Co. Ltd

- Kluber Lubrication

- Liqui Moly GmbH

- Lukoil

- MOL Hungary

- Repsol

- Rosneft

- Shell plc

- TotalEnergies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Industrial rebound and automation surge in CEE

- 4.2.2 Post-pandemic vehicle-parc recovery

- 4.2.3 Offshore-wind build-out needs gear and hydraulic lubes

- 4.2.4 Circular-economy mandates for re-refined base oils

- 4.2.5 AI-enabled predictive-maintenance boosting service fluids

- 4.3 Market Restraints

- 4.3.1 Volatile crude-oil and additive prices squeeze margins

- 4.3.2 EU PFAS and phosphate-ester restrictions in fire-resistant fluids

- 4.3.3 Lifetime-fill lubricants in wind-turbine gearboxes curb aftermarket

- 4.4 Value Chain Analysis

- 4.5 Regulatory Framework

- 4.6 End-user Trends

- 4.6.1 Automotive Industry

- 4.6.2 Manufacturing Industry

- 4.6.3 Power Generation Industry

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Automotive Engine Oil

- 5.1.2 Industrial Engine Oil

- 5.1.3 Transmission Fluids

- 5.1.4 Gear Oil

- 5.1.5 Brake Fluids

- 5.1.6 Hydraulic Fluids

- 5.1.7 Greases

- 5.1.8 Process Oil (Including Rubber Process Oil and White Oil)

- 5.1.9 Metalworking Fluids

- 5.1.10 Turbine Oil

- 5.1.11 Transformer Oil

- 5.1.12 Other Product Types

- 5.2 By Base Stock Type

- 5.2.1 Mineral Oil-Based Lubricants

- 5.2.2 Synthetic Lubricants

- 5.2.3 Semi-Synthetic Lubricants

- 5.2.4 Bio-Based Lubricants

- 5.3 By End-user Industry

- 5.3.1 Automotive

- 5.3.1.1 Passenger Vehicles

- 5.3.1.2 Commercial Vehicles

- 5.3.1.3 Two-Wheelers

- 5.3.2 Marine

- 5.3.3 Aerospace

- 5.3.4 Heavy Equipment

- 5.3.4.1 Construction

- 5.3.4.2 Mining

- 5.3.4.3 Agriculture

- 5.3.5 Industrial

- 5.3.5.1 Power Generation

- 5.3.5.2 Metallurgy and Metalworking

- 5.3.5.3 Textiles

- 5.3.5.4 Oil and Gas

- 5.3.6 Other End-user Industries

- 5.3.1 Automotive

- 5.4 By Geography

- 5.4.1 France

- 5.4.2 Germany

- 5.4.3 Italy

- 5.4.4 Russia

- 5.4.5 Spain

- 5.4.6 United Kingdom

- 5.4.7 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 BP p.l.c.

- 6.4.2 Chevron Corporation

- 6.4.3 Eni SpA

- 6.4.4 Exxon Mobil Corporation

- 6.4.5 FUCHS

- 6.4.6 Gazpromneft

- 6.4.7 Idemitsu Kosan Co. Ltd

- 6.4.8 Kluber Lubrication

- 6.4.9 Liqui Moly GmbH

- 6.4.10 Lukoil

- 6.4.11 MOL Hungary

- 6.4.12 Repsol

- 6.4.13 Rosneft

- 6.4.14 Shell plc

- 6.4.15 TotalEnergies

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

8 Key Strategic Questions for CEOs

潤滑油和潤滑脂市場預測至2034年-按產品類型、基礎油、增稠劑類型、應用、最終用戶、分銷管道和地區分類的全球分析

潤滑油和潤滑脂市場預測至2034年-按產品類型、基礎油、增稠劑類型、應用、最終用戶、分銷管道和地區分類的全球分析 特種潤滑油市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、最終用戶、地區和競爭格局分類,2021-2031年

特種潤滑油市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、最終用戶、地區和競爭格局分類,2021-2031年 鑽井潤滑劑市場規模、佔有率和成長分析:按產品類型、應用、功能和地區分類-2026-2033年產業預測

鑽井潤滑劑市場規模、佔有率和成長分析:按產品類型、應用、功能和地區分類-2026-2033年產業預測 海上潤滑油市場規模、佔有率和趨勢分析報告:按應用、最終用途、地區和細分市場分類(2026-2033 年)機器人潤滑劑市場預測至2034年—按產品類型、潤滑劑類型、應用、最終用戶和地區分類的全球分析

海上潤滑油市場規模、佔有率和趨勢分析報告:按應用、最終用途、地區和細分市場分類(2026-2033 年)機器人潤滑劑市場預測至2034年—按產品類型、潤滑劑類型、應用、最終用戶和地區分類的全球分析 德國潤滑油市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

德國潤滑油市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 拉絲潤滑劑市場:2026-2032年全球市場預測(依產品類型、添加劑類型、線材類型、應用、終端用戶產業和銷售管道分類)

拉絲潤滑劑市場:2026-2032年全球市場預測(依產品類型、添加劑類型、線材類型、應用、終端用戶產業和銷售管道分類) 潤滑油市場:依產品類型、基礎油、終端用戶產業及地區分類(2026-2034 年)獨立潤滑油製造商市場報告:按類型、應用和地區分類(2026-2034 年)外科潤滑劑市場:按類型、應用、最終用戶和分銷管道分類-2026-2032年全球市場預測

潤滑油市場:依產品類型、基礎油、終端用戶產業及地區分類(2026-2034 年)獨立潤滑油製造商市場報告:按類型、應用和地區分類(2026-2034 年)外科潤滑劑市場:按類型、應用、最終用戶和分銷管道分類-2026-2032年全球市場預測