|

市場調查報告書

商品編碼

2073025

北美動物飼料中有機微量元素:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)North America Animal Feed Organic Trace Minerals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

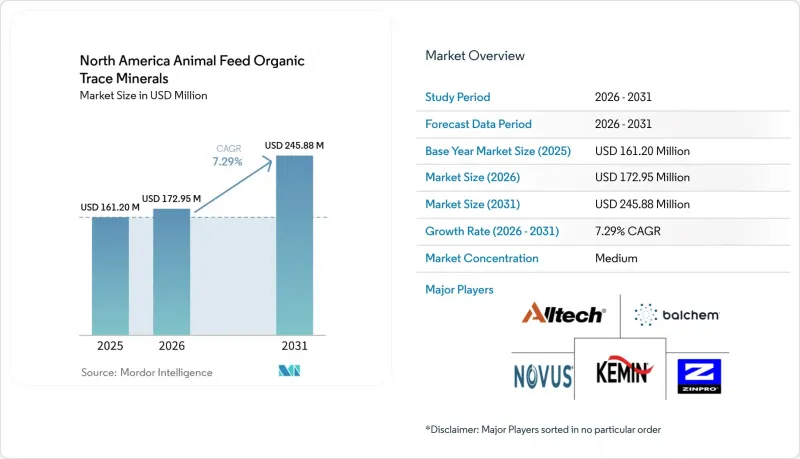

根據 Mordor Intelligence 預測,北美動物飼料有機微量元素市場規模將從 2025 年的 1.612 億美元和 2026 年的 1.7295 億美元成長到 2031 年的 2.4588 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 7.29%。

本報告按微量元素(鋅、鐵、銅、錳、硒及其他)、動物類型(牛、乳牛、牛、豬、水產養殖及其他)、螯合類型(胺基酸螯合物、蛋白質鹽及其他)和地區(美國、加拿大、墨西哥、北美及其他)進行細分。市場預測以美元計價。

北美動物飼料中有機微量元素的洞察與趨勢

對優質動物性蛋白質和飼料效率的需求不斷成長

北美動物飼料中有機微量元素市場正受益於消費者對符合有機和潔淨標示標準的食品日益成長的偏好。這種需求推動了經認證的有機畜牧業的擴張,使得礦物質補充在所有飼料方案中仍然至關重要。根據美國法規7(205.236和205.237),作為有機產品出售的牲畜必須持續進行有機管理,並飼餵符合有機處理規定的飼料。這支撐了對經批准的礦物質添加劑的穩定需求。牲畜的實際反應也支持了這種購買需求。堪薩斯大學牛實驗室2024年4月的報告顯示,與飼餵無機硫酸鹽的牛群相比,飼餵有機鋅、銅、錳和鈷複合物的壓力肉牛發病率更低,日增重更高。隨著越來越多的生產者認知到有機礦物質既是符合法規要求的手段,也是提高生產力的投入,北美飼料中有機微量元素市場正從高階小眾農業管道擴展到更廣泛的領域。

從無機鹽過渡到高生物利用度的有機礦物質

北美動物飼料中有機微量元素的市場也不斷擴大。許多傳統養殖戶在未獲得全面認證的情況下,就開始調整部分礦物質添加方案。隨著營養團隊致力於在不改變整個飼料配方系統的前提下提高飼料轉換率並減少微量元素的損失,部分替代策略變得越來越普遍。這種方法至關重要,因為它將擴大全部區域規模大規模的傳統畜牧養殖戶的需求,尤其是在家禽和乳牛系統中,因為這些系統可以更詳細地追蹤動物對不同形態礦物質的反應。這種轉變在那些已經根據明確的品質和標籤標準管理飼料的地區最為明顯,例如美國各州的有機飼料項目。隨著時間的推移,這種分階段推廣的模式將使北美動物飼料中有機微量元素的市場基礎超越認證有機畜牧業,更加廣泛。

與無機替代品相比的價格差異

高價仍是限制北美飼料微量元素飼料市場快速滲透傳統畜牧系統的最大阻礙因素之一。有機螯合和蛋白質結合的微量元素比無機硫酸鹽和氧化物價格高得多,因此,當飼料價格上漲或牲畜價格下跌時,企業越來越難以消化這部分差價。這種壓力在生豬和肉雞養殖業尤為突出,因為這些養殖場的單頭利潤率較低,而且每次配方調整都會對複合飼料成本進行嚴格審查。大規模一體化生產商可以透過規模經濟和調整配方帶來的利潤成長來緩解這種價格差異,但小規模牛和多品種飼料戶則更容易受到額外成本的影響。因此,儘管市場需求結構強勁,但北美有機微量元素飼料市場容易受到經濟週期的影響而停滯不前。

細分市場分析

到2025年,鋅將佔據北美動物飼料有機微量元素市場49.3%的佔有率,成為最大的微量元素細分市場。其主導地位源自於鋅在乳牛、肉牛、家禽和生豬養殖業的廣泛應用,這些產業的蹄部健康、羽毛品質、免疫功能和繁殖能力都依賴穩定的鋅含量。此外,與其他許多微量元素相比,生產者對鋅的了解更為深入,因此他們更傾向於重複購買預混合料和直接補充形式的鋅。有機鋅的重要性也體現在減少微量元素排泄的壓力上,因為其高生物利用度允許在不影響生產性能的前提下添加少量有機鋅。

在北美動物飼料有機微量元素市場,硒的需求預計到2031年將以7.7%的複合年成長率成長,使其成為成長最快的微量元素類別。這一成長與水產養殖和其他集約化養殖系統密切相關,在這些系統中,高密度生產條件下,抗氧化防禦和抗逆性變得尤為重要。 2025年2月發表在《海洋科學前沿》(Frontiers in Marine Science)上的一項研究表明,在集約化水產養殖條件下,添加維生素C和E的有機硒能夠改善幼年鰱魚的生長、氧化酵素活性和血液指標。銅、鐵和錳仍然主要滿足特定物種和生長階段的需求,而鉻仍然屬於小規模的專業類別。從整個北美有機飼料礦物質產業來看,鋅是支撐最大銷售量的主力產品,而硒則是成長最為顯著的領域。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對優質動物性蛋白質的需求不斷成長,以及提高飼料轉換率的必要性。

- 從無機鹽過渡到高生物利用度的有機礦物質

- 遵守飼料安全和礦物質排泄相關法規的壓力越來越大。

- 在大規模綜合畜牧養殖系統中引入精準營養

- DDGS 的硫拮抗作用增加了對更穩定礦物形態的需求。

- 旨在緩解熱應激的鉻、鋅和硒項目的需求

- 市場限制因素

- 高階定價與非有機替代方案的比較

- 有機認證和標籤的複雜性

- 合規預混合料中有關受限蛋白質來源和有機載體的規定

- 有機礦物化學中性能變異性的粗略定義

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 微量元素類型

- 鋅

- 鐵

- 銅

- 錳

- 碳粉匣

- 鉻

- 其他

- 依動物類型

- 家禽

- 乳牛

- 肉牛

- 豬

- 水產養殖

- 馬

- 寵物

- 其他

- 螯合型

- 胺基酸螯合物

- 蛋白質攝取

- 多醣複合物

- 羥基化微量元素

- 丙酸酯

- 酵母來源的錯合

- 其他

- 按地區

- 美國

- 加拿大

- 墨西哥

- 其他北美國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介。

- Zinpro Corporation

- Novus International, Inc.

- Alltech, Inc.

- Kemin Industries, Inc.

- Balchem Corporation

- Archer-Daniels-Midland Company

- Cargill, Incorporated

- Phibro Animal Health Corporation

- Nutreco NV

- Purina Animal Nutrition LLC

- BioZyme, Incorporated

- Adisseo USA Inc.

- DSM-Firmenich AG

- Biochem Zusatzstoffe Handels-und Produktionsgesellschaft mbH

- EW Nutrition USA LLC

第7章 市場機會與未來展望

According to Mordor Intelligence, the north america animal feed organic trace minerals market size is projected to expand from USD 161.20 million in 2025 and USD 172.95 million in 2026 to USD 245.88 million by 2031, registering a compound annual growth rate (CAGR) of 7.29% between 2026 and 2031.

This report is Segmented by Trace Element (Zinc, Iron, Copper, Manganese, Selenium, and Others), by Animal Type (Poultry, Dairy Cattle, Beef Cattle, Swine, Aquaculture, and More), by Chelation Type (Amino-Acid Chelates, Proteinates, and More), and by Geography (United States, Canada, Mexico, and Rest of North America). The Market Forecasts are Provided in Terms of Value (USD).

Insights and Trends of North America Animal Feed Organic Trace Minerals

Higher Demand for Premium Animal Protein and Feed Efficiency

The North America animal feed organic trace minerals market is benefiting from stronger consumer preference for food produced under organic and clean-label systems. That demand supports more certified organic livestock production, which, in turn, keeps mineral supplementation essential across feed programs. Under 7 Code of Federal Regulations 205.236 and 205.237, livestock sold as organic must remain under continuous organic management and must receive feed that meets organic handling rules, which supports steady replacement demand for approved mineral inputs. The buying case is also supported by measured animal responses, as Kansas State University Beef Cattle Institute reported in April 2024 that stressed beef heifers fed organic zinc, copper, manganese, and cobalt complexes showed lower morbidity and higher daily gain than those fed inorganic sulfates. As more producers see organic minerals as both a compliance tool and a performance input, the North America animal feed organic trace minerals market gains support beyond niche premium farming channels.

Shift From Inorganic Salts to Higher-Bioavailability Organic Minerals

The North America animal feed organic trace minerals market is also advancing, as many conventional producers are not waiting for full certification before changing parts of their mineral programs. Partial replacement strategies are becoming more common, as nutrition teams seek better feed conversion and lower trace mineral losses without changing the full ration system. This approach matters because it expands demand into the much larger conventional livestock base across the region, especially in poultry and dairy systems, where response to mineral form can be tracked more closely. The shift is strongest where producers already manage feed under clear quality and labeling standards, including organic feed programs overseen at the state level in the United States. Over time, this staged adoption pattern gives the North America animal feed organic trace minerals market a wider base than certified organic livestock alone.

Premium Pricing Versus Inorganic Alternatives

Premium pricing remains one of the clearest limits on how fast the North America animal feed organic trace minerals market can penetrate conventional livestock systems. Organic chelated and proteinated minerals carry a much higher cost than inorganic sulfates and oxides, and that gap becomes harder to absorb when feed grains are expensive, or animal selling prices soften. The pressure is strongest in swine and broiler operations, where per-head margins are thin, and ration costs are closely reviewed at every reformulation cycle. Large integrated producers can spread the premium across scale efficiencies and response gains, but smaller cattle and mixed-animal operators face greater direct exposure to the added cost. This keeps demand structurally positive while still making the North America animal feed organic trace minerals market vulnerable to cyclical pauses.

Other drivers and restraints analyzed in the detailed report include:

- Tighter Feed-safety and Mineral-Excretion Compliance Pressure

- Precision Nutrition Adoption in Large Integrated Livestock Systems

- Organic Certification and Labeling Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Zinc held 49.3% of the North America animal feed organic trace minerals market share in 2025, which made it the largest trace element segment. Its leadership stems from its widespread use across dairy, beef, poultry, and swine, where hoof integrity, feather quality, immune function, and reproductive performance all depend on reliable zinc status. Producers also understand zinc better than many other trace elements, so repeat purchase behavior is stronger in both premix and direct supplementation formats. In addition, pressure to reduce trace mineral excretion keeps organic zinc relevant, as higher bioavailability can support lower inclusion rates without weakening performance.

The North America animal feed organic trace minerals market for selenium-linked demand is forecast to expand at a 7.7% CAGR through 2031, making selenium the fastest-growing trace element segment. Growth is closely tied to aquaculture and other intensive systems, where antioxidant defense and stress resilience matter more under high-density production conditions. Research published in Frontiers in Marine Science in February 2025 showed that organic selenium with vitamins C and E improved growth, antioxidant enzyme activity, and blood parameters in juvenile silver carp under intensive aquaculture conditions. Copper, iron, and manganese continue to serve narrower species and stage specific needs, while chromium remains a smaller specialty category. Across the North America organic feed minerals industry, that leaves zinc as the broadest volume anchor and selenium as the clearest expansion pocket.

Complete Report Scope:

- By Trace Element Type

- Zinc

- Iron

- Copper

- Manganese

- Selenium

- Chromium

- Others

- By Animal Type

- Poultry

- Dairy Cattle

- Beef Cattle

- Swine

- Aquaculture

- Equine

- Pets

- Others

- By Chelation Type

- Amino-Acid Chelates

- Proteinates

- Polysaccharide Complexes

- Hydroxy-Trace Minerals

- Propionates

- Yeast-Based Complexes

- Others

- By Geography

- United States

- Canada

- Mexico

- Rest of North America

List of Companies Covered in this Report:

- Zinpro Corporation

- Novus International, Inc.

- Alltech, Inc.

- Kemin Industries, Inc.

- Balchem Corporation

- Archer-Daniels-Midland Company

- Cargill, Incorporated

- Phibro Animal Health Corporation

- Nutreco N.V.

- Purina Animal Nutrition LLC

- BioZyme, Incorporated

- Adisseo USA Inc.

- DSM-Firmenich AG

- Biochem Zusatzstoffe Handels- und Produktionsgesellschaft mbH

- EW Nutrition USA LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Higher demand for premium animal protein and feed efficiency

- 4.2.2 Shift from inorganic salts to higher-bioavailability organic minerals

- 4.2.3 Tighter feed-safety and mineral-excretion compliance pressure

- 4.2.4 Precision nutrition adoption in large integrated livestock systems

- 4.2.5 DDGS sulfur antagonism raising need for more stable mineral forms

- 4.2.6 Heat-stress mitigation demand for chromium, zinc, and selenium programs

- 4.3 Market Restraints

- 4.3.1 Premium pricing versus inorganic alternatives

- 4.3.2 Organic certification and labeling complexity

- 4.3.3 Restricted protein sources and organic-carrier rules for compliant premixes

- 4.3.4 Performance variability across loosely defined organic mineral chemistries

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Trace Element Type

- 5.1.1 Zinc

- 5.1.2 Iron

- 5.1.3 Copper

- 5.1.4 Manganese

- 5.1.5 Selenium

- 5.1.6 Chromium

- 5.1.7 Others

- 5.2 By Animal Type

- 5.2.1 Poultry

- 5.2.2 Dairy Cattle

- 5.2.3 Beef Cattle

- 5.2.4 Swine

- 5.2.5 Aquaculture

- 5.2.6 Equine

- 5.2.7 Pets

- 5.2.8 Others

- 5.3 By Chelation Type

- 5.3.1 Amino-Acid Chelates

- 5.3.2 Proteinates

- 5.3.3 Polysaccharide Complexes

- 5.3.4 Hydroxy-Trace Minerals

- 5.3.5 Propionates

- 5.3.6 Yeast-Based Complexes

- 5.3.7 Others

- 5.4 By Geography

- 5.4.1 United States

- 5.4.2 Canada

- 5.4.3 Mexico

- 5.4.4 Rest of North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Zinpro Corporation

- 6.4.2 Novus International, Inc.

- 6.4.3 Alltech, Inc.

- 6.4.4 Kemin Industries, Inc.

- 6.4.5 Balchem Corporation

- 6.4.6 Archer-Daniels-Midland Company

- 6.4.7 Cargill, Incorporated

- 6.4.8 Phibro Animal Health Corporation

- 6.4.9 Nutreco N.V.

- 6.4.10 Purina Animal Nutrition LLC

- 6.4.11 BioZyme, Incorporated

- 6.4.12 Adisseo USA Inc.

- 6.4.13 DSM-Firmenich AG

- 6.4.14 Biochem Zusatzstoffe Handels- und Produktionsgesellschaft mbH

- 6.4.15 EW Nutrition USA LLC

7 Market Opportunities and Future Outlook

美國動物飼料用有機微量元素:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)南美洲動物飼料中的有機微量元素:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲動物飼料用有機微量元素:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

美國動物飼料用有機微量元素:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)南美洲動物飼料中的有機微量元素:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲動物飼料用有機微量元素:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 飼料中微量元素的市場機會、成長要素、產業趨勢和預測(2025-2035 年)。

飼料中微量元素的市場機會、成長要素、產業趨勢和預測(2025-2035 年)。 飼料飼料有機微量元素市場報告:按微量元素類型、動物類型和地區分類(2026-2034 年)

飼料飼料有機微量元素市場報告:按微量元素類型、動物類型和地區分類(2026-2034 年) 2026-2034年全球動物飼料中有機微量元素市場規模、佔有率、趨勢和成長分析報告動物飼料用有機微量元素市場機會、成長要素、產業趨勢分析及預測(2026年至2035年)

2026-2034年全球動物飼料中有機微量元素市場規模、佔有率、趨勢和成長分析報告動物飼料用有機微量元素市場機會、成長要素、產業趨勢分析及預測(2026年至2035年) 動物飼料用有機微量元素市場規模、佔有率和成長分析(按產品、來源、形態、應用、動物類型和地區分類)-產業預測,2026-2033年

動物飼料用有機微量元素市場規模、佔有率和成長分析(按產品、來源、形態、應用、動物類型和地區分類)-產業預測,2026-2033年