|

市場調查報告書

商品編碼

2072704

人力資源轉型服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)HR Transformation Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

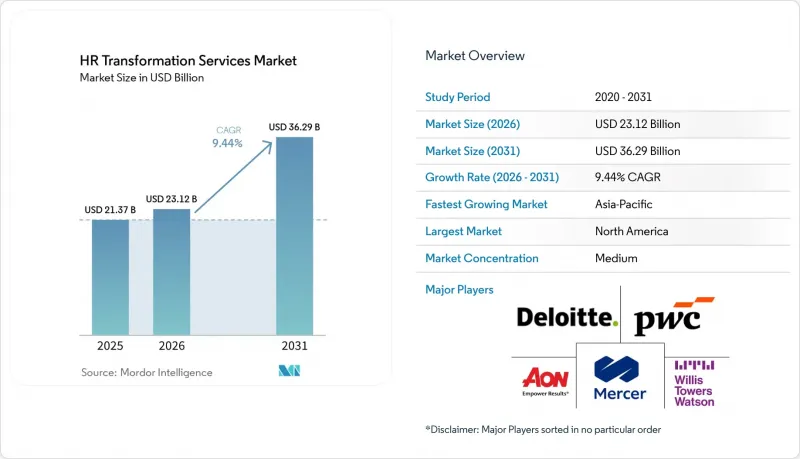

根據 Mordor Intelligence 預測,人力資源轉型服務市場預計將從 2025 年的 213.7 億美元成長到 2026 年的 231.2 億美元,到 2031 年達到 362.9 億美元,2026 年至 2031 年的複合年成長率為 9.4%。

本報告按服務類型(如人力資源營運模式和組織設計)、公司規模(大型企業、中小企業)、最終用戶行業(如銀行、金融服務和保險、醫療保健和生命科學)以及地區(北美、南美、歐洲、亞太地區以及中東和非洲)進行細分,市場預測以貨幣(美元)表示。

全球人力資源轉型服務市場趨勢與洞察

企業對重新設計端對端人力資源管理模式的需求日益成長

端到端的重新設計已成為人力資源轉型服務市場支出計畫中的重中之重。這是因為企業逐漸意識到,僅僅依靠新工具無法改變最終結果。許多組織仍然沿用基於控制、核准和行政完整性的人力資源架構,而非基於速度、分析和人工智慧驅動的決策。這種情況促使客戶轉向涵蓋流程所有權、服務交付層、工作流程自動化、決策權和經理自助服務等單一範圍的綜合方案,而非單一專案。近期趨勢表明,人工智慧功能正在整合到整個人力資源體系中,隨著價值取決於組織內部工作流程的建構和管治方式,重新設計工作變得愈發迫切。 2026 年,隨著專用人工智慧代理被引入人力資源工作流程,類似的趨勢再次出現。這進一步凸顯了企業在實現大規模可靠自動化之前,重新檢視核准邏輯、升級規則和角色定義的必要性。因此,人力資源轉型服務市場對整體架構重新設計的需求日益成長,而非僅專注於單一技術更新。

擴大基於雲端的人力資源轉型藍圖的採用

隨著眾多企業將基於雲端的人力資本管理 (HCM) 系統定位為薪資核算、人才管理、入職、工作安排和勞動力規劃的基礎,雲端技術的普及持續推動著人力資源轉型服務市場的發展。由於最初的雲端技術應用往往依賴與傳統人力資源流程相仿的標準配置,如今越來越多的客戶正在重新與服務供應商合作,以完成最佳化、整合和管治任務。一家領先的雲端 HCM 平台服務於 13,000 家客戶的超過 1.4 億用戶,並在 2026 年上半年完成了 825 個新的運作。這表明大規模的部署基礎仍然需要持續的重新設計和實施服務。近期發布的平台版本也大大擴展了服務交付範圍,遠遠超出了最初的平台部署,增強了整個套件的 AI 整合、工作流程統一和技能管治。向自主企業能力的廣泛轉變意味著薪資核算、招聘、入職和勞動力規劃等人力資源工作流程現在與嵌入式助理更加緊密地整合,儘管這些助手仍然需要配置和修改方面的支援。這種「雲端採用→最佳化」的循環正在為成熟地區和高成長地區的人力資源轉型服務市場創造永續的需求管道。

傳統人力資源組織面臨沉重的變革管理負擔

人力資源轉型服務市場持續面臨來自傳統人力資源團隊的阻力。這是因為許多專案同時改變了角色、核准途徑、服務邊界和責任模式。因此,即使經營團隊認同數位化工具和人工智慧驅動的工作流程的必要性,轉型依然困難重重。一項2026年的數位化調查顯示,時間限制和實施複雜性仍然是企業面臨的主要障礙,這與延緩人力資源重塑計畫的營運負擔密切相關。對跨國公司而言,這個問題往往更為嚴峻,因為政策集中化、薪資核算體系統一和員工資料管治必須在不同司法管轄區內協調實施。一項2026年的專案利用多個基於雲端的人力資本管理(HCM)模組,對歐洲和美國的人力資源環境進行現代化改造,充分展現了營運和實施負擔的普遍性。因此,即使策略需求已經明確,人力資源轉型服務市場也可能面臨更長的銷售週期和更長的交付時間。

細分市場分析

到2025年,人力資源流程轉型和重組將佔人力資源轉型服務市場28.37%的佔有率,這凸顯出工作流程重塑仍然是企業採購決策的核心。這個主導地位反映了明確的支出優先順序:許多客戶希望在更深入地投資自動化和進階分析之前,先最佳化流程邏輯、服務層級和交接環節。在人力資源轉型服務市場中,工作流程重塑仍然佔據最大的預算佔有率,因為那些已經實施基於雲端的人力資本管理(HCM)而非傳統工作流程的企業往往收益有限。人力資源技術轉型服務也發揮著重要作用,因為許多公司正在對先前的遷移專案進行後續跟進,轉向平台整合、改進整合和最佳化配置。

預計到2031年,勞動力分析和人力資源數據轉型將以11.62%的複合年成長率成長,成為人力資源轉型服務市場中成長最快的服務類別。該領域的成長是循序漸進的,因為客戶需要先整合資料來源,然後改進管治,接著建立可操作的規劃模型,最後將這些洞察整合到管理工作流程中。近期趨勢推動了這一發展模式,即更加緊密地將勞動力規劃與業務和財務需求相結合,從而增加了對能夠彌合技術、數據和營運設計差距的服務提供者的需求。人力資源共享服務和外包轉型服務仍在繼續提供,通常是針對那些在初步重組計劃後透過共享服務中心實現服務交付標準化的大型企業。目前,人力資源營運模式和組織設計在支出中所佔比例仍然小規模,但隨著企業負責人在擴展人工智慧驅動的人力資源工作流程之前需要更完善的藍圖,它們的重要性日益凸顯。因此,人力資源轉型服務產業正在從僅依賴一次性平台實施轉向將底層重組與以數據為中心的現代化相結合的方向。

區域分析

預計到2025年,北美將佔據人力資源轉型服務市場38.29%的佔有率,成為最大的區域貢獻者。該地區受益於大型企業買家的高度集中、成熟的諮詢和IT服務基礎設施,以及企業人力資源職能部門整體雲端HCM的廣泛採用。美國仍然是需求的核心,因為大型企業正在將人工智慧計畫與人力資源工作流程、資料模型和管治的可操作性重新設計相結合。加拿大透過與跨國公司計畫的區域合作擴大了需求,而隨著近岸服務和政策協調在北美商業區域日益普遍,墨西哥的重要性也不斷提升。這些因素推動北美人力資源轉型服務市場保持活力,從最初的重新設計專案到後續的最佳化工作,市場始終蓬勃發展。

在歐洲,由於合規義務持續高企以及跨國公司流程標準化的迫切需求,對人力資源轉型服務的需求仍然穩定。該地區還面臨傳統人力資源架構和複雜實施環境帶來的沉重負擔;德國工商會(DIHK)2026年的一項調查顯示,時間限制和實施複雜性仍然是企業數位化轉型的主要障礙。這些挑戰推動了對能夠整合重組、管治和變革管理(而不僅僅是技術實施)的服務提供者的需求。雖然南美洲的規模仍然較小,但隨著企業數位轉型和當地勞動合規要求的增加,巴西和其他跨國公司所在地的業務正在逐步成長。

預計到2031年,亞太地區將以14.26%的複合年成長率成長,成為人力資源轉型服務市場成長最快的地區。印度是主要驅動力,其勞動力正規化、數位化公共基礎設施建設以及全球能力中心的擴張,都催生了對共享服務重塑、薪資核算標準化和分析支援的需求。世界大型企業聯合會在2026年報告中指出,亞太地區的執行長們正在重新評估成長、風險和營運模式,將人力資源轉型從單純的營運挑戰提升為更廣泛的業務挑戰。在日本、中國、韓國和東協市場,隨著企業實現勞動力模式現代化並加強跨國合作,多年期交易管道正不斷拓展。中東地區在沙烏地阿拉伯和阿拉伯聯合大公國等國家勞動力發展計畫的推動下持續成長,而非洲市場仍處於早期發展階段,其成長動力主要來自勞動力正規化以及南非和奈及利亞等市場科技產業的蓬勃發展。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 企業對重新設計端對端人力資源管理模式的需求日益成長

- 擴大基於雲端的人力資源轉型藍圖的採用

- 在分散的員工隊伍中,需要統一全球人力資源政策。

- 提高員工體驗和勞動力彈性的壓力日益增大

- 擴展數據驅動的勞動規劃與人力資源分析

- 加速落實多邊勞工和隱私法規的合規要求

- 市場限制因素

- 傳統人力資源組織變革管理的負擔

- 量化轉型項目短期投資報酬率的難度。

- 人力資源流程重組和轉型諮詢技能方面的人才短缺

- 分散的舊式人力資源系統和資料遷移的複雜性

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按服務類型

- 人力資源管理模型與組織設計

- 人力資源流程的轉型與重組

- 人力資源技術轉型服務

- 人力資源共享服務與外包轉型

- 變革勞動力分析與人力資源數據

- 按公司規模

- 大公司

- 小型企業

- 按最終用戶行業分類

- BFSI

- 醫療保健和生命科學

- 資訊科技/通訊

- 零售與電子商務

- 工業製造

- 政府/公共部門

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 荷蘭

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Aon plc

- Automatic Data Processing, Inc.

- Buck Global, LLC

- Capgemini SE

- Deloitte Touche Tohmatsu Limited

- International Business Machines Corporation

- KPMG International Limited

- Mercer LLC

- SD Worx

- NGA Human Resources

- NTT DATA Group Corporation

- Strada

- Oracle Corporation

- PricewaterhouseCoopers International Limited

- Genpact

- SAP SE

- Tata Consultancy Services Limited

- Wipro Limited

- Willis Towers Watson Public Limited Company

- Zalaris ASA

- HCL Technologies Limited

- Alight, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the HR transformation services market size is expected to increase from USD 21.37 billion in 2025 to USD 23.12 billion in 2026 and reach USD 36.29 billion by 2031, growing at a CAGR of 9.44% over 2026-2031.

This report is Segmented by Service Type (HR Operating Model and Organizational Design, and More), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (BFSI, Healthcare and Life Sciences, and More), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa), The Market Forecasts are Provided in Terms of Value (USD).

Global HR Transformation Services Market Trends and Insights

Growing Enterprise Demand for End-To-End HR Operating Model Redesign

End-to-end redesign has moved to the front of spending plans in the HR transformation services market because enterprises now see that new tools alone do not change outcomes. Many organizations still maintain HR structures built for control, approvals, and administrative consistency rather than for speed, analytics, and AI-supported decision-making. That is pushing clients toward programs that cover process ownership, service delivery layers, workflow automation, decision rights, and manager self-service within a single scope rather than in isolated projects. Recent product developments show that AI capabilities are being embedded across the HR stack, making redesign work more urgent because value depends on how workflows are configured and governed within the organization. A similar direction emerged in 2026 with the introduction of specialized AI agents into HR workflows, which further raises the need for enterprises to rethink approval logic, escalation rules, and role definitions before automation can work reliably at scale. As a result, the HR transformation services market is seeing stronger demand for full architecture redesign than for isolated technology refresh work.

Rising Adoption of Cloud-Based HR Transformation Roadmaps

Cloud adoption continues to support the HR transformation services market, as many organizations now treat cloud HCM as the foundation for payroll, talent, onboarding, scheduling, and workforce planning. The first wave of deployments often relied on standard configurations that mirrored older HR processes, so a growing number of clients are returning to providers for optimization, integration, and governance work. More than 140 million users across 13,000 customers were served by a major cloud HCM platform, with 825 new go-lives completed in the first half of 2026, indicating a large installed base that still requires ongoing redesign and adoption services. Recent platform releases also strengthened suite-wide AI integration, unified workflows, and skills governance, extending the service tail well beyond initial platform deployment. A broader move toward autonomous enterprise capabilities further connected HR workflows such as payroll, recruiting, onboarding, and workforce planning with embedded assistants that still require configuration and change support. This cloud-then-optimize cycle is creating a durable pipeline for the HR transformation services market in both mature and high-growth regions.

High Change-Management Burden Across Legacy HR Organizations

The HR transformation services market still faces resistance from legacy HR teams because many programs change roles, approval paths, service boundaries, and accountability models simultaneously. That makes transformation difficult even when leadership agrees with the need for digital tools and AI-enabled workflows. A 2026 digitalization survey found that time constraints and implementation complexity remained major barriers for enterprises, which aligns closely with the execution burden that slows HR redesign programs. The issue is often greater in multinational organizations because policy harmonization, payroll alignment, and employee data governance must move in step across jurisdictions. A 2026 engagement that modernized an HR landscape across Europe and the United States using multiple cloud HCM modules illustrates how broad the operating and adoption burden can become. Because of this, the HR transformation services market can see long sales cycles and extended delivery timelines even when the strategic need is already clear.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Data-Driven Workforce Planning And HR Analytics

- Increased Pressure to Improve Employee Experience and Workforce Agility

- Difficulty Quantifying Near-Term ROI from Transformation Programs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

HR Process Transformation and Reengineering accounted for 28.37% of the HR transformation services market in 2025, underscoring that workflow redesign remains central to enterprise buying decisions. This leadership reflects a clear spending sequence, as many clients want to fix process logic, service layers, and handoffs before investing more deeply in automation and advanced analytics. Organizations that move cloud HCM onto older workflows often see only limited gains, so redesign work continues to attract the largest budgets inside the HR transformation services market. HR Technology Transformation Services also plays a major role, as many enterprises are now consolidating platforms, improving integrations, and refining configurations following earlier migration programs.

Workforce Analytics and HR Data Transformation is projected to expand at an 11.62% CAGR through 2031, making it the fastest-growing service category in the HR transformation services market. Growth here is building in phases because clients first need to unify data sources, then improve governance, then create usable planning models, and then embed those insights into manager workflows. Recent product developments support this pattern by linking workforce planning more closely with business and financial needs, which increases the need for providers that can bridge technology, data, and operating design. HR Shared Services and Outsourcing Transformation continues to serve large organizations that are standardizing delivery through shared services centers, often after an initial redesign program. HR Operating Model and Organizational Design remains smaller by current spend, but it is gaining weight as enterprise buyers look for a stronger blueprint before they scale AI-enabled HR workflows. The HR transformation services industry is therefore shifting toward a mix of foundational redesign and data-centered modernization rather than relying solely on one-time platform implementation.

Complete Report Scope:

- By Service Type

- HR Operating Model and Organizational Design

- HR Process Transformation and Reengineering

- HR Technology Transformation Services

- HR Shared Services and Outsourcing Transformation

- Workforce Analytics and HR Data Transformation

- By Enterprise Size

- Large Enterprises

- Small And Medium Enterprises

- By End-user Industry

- BFSI

- Healthcare and Life Sciences

- Information Technology and Telecom

- Retail and E-commerce

- Industrial Manufacturing

- Government and Public Sector

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Netherlands

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America held 38.29% of the HR transformation services market share in 2025, making it the largest regional contributor. The region benefits from a high concentration of large enterprise buyers, mature consulting and IT services capacity, and wide adoption of cloud HCM across corporate HR functions. The United States remains the core demand engine because large employers are trying to align AI ambitions with practical redesign of HR workflows, data models, and governance. Canada adds volume through regional alignment with multinational programs, while Mexico is gaining relevance as nearshore delivery and policy coordination across North American operating zones become more common. These factors keep the HR transformation services market active in North America across both initial redesign mandates and follow-on optimization work.

Europe continues to generate steady demand for HR transformation services as compliance obligations and process standardization needs remain high across multinational employers. The region also carries a significant burden from older HR structures and complex implementation environments, and Germany's 2026 DIHK survey showed that time constraints and implementation complexity were still major barriers to business digitalization. That friction supports demand for providers that can combine redesign, governance, and change management rather than technology deployment alone. South America is still smaller in scale, but Brazil and other multinational operating hubs are starting to generate incremental work tied to enterprise digitalization and local labor compliance requirements.

Asia-Pacific is projected to expand at a 14.26% CAGR through 2031, making it the fastest-growing region in the HR transformation services market. India is a major driver because workforce formalization, digital public infrastructure, and growth in global capability centers are creating demand for shared services redesign, payroll standardization, and analytics support. The Conference Board reported in 2026 that CEOs across Asia-Pacific were reassessing growth, risk, and operating models, which elevated HR transformation from an operational issue to a broader business agenda. Japan, China, South Korea, and ASEAN markets are also building multi-year pipelines as companies modernize workforce models and seek better cross-border coordination. The Middle East is growing through national workforce development programs in Saudi Arabia and the UAE, while Africa remains an earlier-stage opportunity, led by formalization and technology-sector growth in markets such as South Africa and Nigeria.

- Aon plc

- Automatic Data Processing, Inc.

- Buck Global, LLC

- Capgemini SE

- Deloitte Touche Tohmatsu Limited

- International Business Machines Corporation

- KPMG International Limited

- Mercer LLC

- SD Worx

- NGA Human Resources

- NTT DATA Group Corporation

- Strada

- Oracle Corporation

- PricewaterhouseCoopers International Limited

- Genpact

- SAP SE

- Tata Consultancy Services Limited

- Wipro Limited

- Willis Towers Watson Public Limited Company

- Zalaris ASA

- HCL Technologies Limited

- Alight, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Enterprise Demand For End-To-End HR Operating Model Redesign

- 4.2.2 Rising Adoption Of Cloud-Based HR Transformation Roadmaps

- 4.2.3 Need To Standardize Global HR Policies Across Distributed Workforces

- 4.2.4 Increased Pressure To Improve Employee Experience And Workforce Agility

- 4.2.5 Expansion Of Data-Driven Workforce Planning And HR Analytics

- 4.2.6 Accelerating Compliance Needs For Multi-Country Labor And Privacy Regulations

- 4.3 Market Restraints

- 4.3.1 High Change-Management Burden Across Legacy HR Organizations

- 4.3.2 Difficulty Quantifying Near-Term ROI From Transformation Programs

- 4.3.3 Talent Shortage In HR Process Redesign And Change Advisory Skills

- 4.3.4 Fragmented Legacy HR Systems And Data Migration Complexity

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat Of New Entrants

- 4.8.2 Bargaining Power Of Suppliers

- 4.8.3 Bargaining Power Of Buyers

- 4.8.4 Threat Of Substitutes

- 4.8.5 Intensity of Comptetive Rivalary

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 HR Operating Model and Organizational Design

- 5.1.2 HR Process Transformation and Reengineering

- 5.1.3 HR Technology Transformation Services

- 5.1.4 HR Shared Services and Outsourcing Transformation

- 5.1.5 Workforce Analytics and HR Data Transformation

- 5.2 By Enterprise Size

- 5.2.1 Large Enterprises

- 5.2.2 Small And Medium Enterprises

- 5.3 By End-user Industry

- 5.3.1 BFSI

- 5.3.2 Healthcare and Life Sciences

- 5.3.3 Information Technology and Telecom

- 5.3.4 Retail and E-commerce

- 5.3.5 Industrial Manufacturing

- 5.3.6 Government and Public Sector

- 5.3.7 Other End-user Industries

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Netherlands

- 5.4.3.8 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 Australia and New Zealand

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Nigeria

- 5.4.6.3 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Aon plc

- 6.4.2 Automatic Data Processing, Inc.

- 6.4.3 Buck Global, LLC

- 6.4.4 Capgemini SE

- 6.4.5 Deloitte Touche Tohmatsu Limited

- 6.4.6 International Business Machines Corporation

- 6.4.7 KPMG International Limited

- 6.4.8 Mercer LLC

- 6.4.9 SD Worx

- 6.4.10 NGA Human Resources

- 6.4.11 NTT DATA Group Corporation

- 6.4.12 Strada

- 6.4.13 Oracle Corporation

- 6.4.14 PricewaterhouseCoopers International Limited

- 6.4.15 Genpact

- 6.4.16 SAP SE

- 6.4.17 Tata Consultancy Services Limited

- 6.4.18 Wipro Limited

- 6.4.19 Willis Towers Watson Public Limited Company

- 6.4.20 Zalaris ASA

- 6.4.21 HCL Technologies Limited

- 6.4.22 Alight, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

人力資源專業服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

人力資源專業服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 人力專業服務市場規模、佔有率和成長分析:按服務類型、部署模式、組織規模、最終用戶產業和地區分類-2026-2033年產業預測

人力專業服務市場規模、佔有率和成長分析:按服務類型、部署模式、組織規模、最終用戶產業和地區分類-2026-2033年產業預測 人力資源(HR)技術市場規模、佔有率和成長分析:按類型、部署模式、組織規模、最終用戶、產業和地區分類-2026-2033年產業預測

人力資源(HR)技術市場規模、佔有率和成長分析:按類型、部署模式、組織規模、最終用戶、產業和地區分類-2026-2033年產業預測 人力資源(HR)技術市場規模、佔有率、趨勢和預測:按應用、類型、最終用戶行業、企業規模和地區分類,2026-2034年

人力資源(HR)技術市場規模、佔有率、趨勢和預測:按應用、類型、最終用戶行業、企業規模和地區分類,2026-2034年 2026年全球人力資源專業服務市場報告2026年全球人力資源人工智慧市場報告2026年全球人力資源諮詢服務市場報告2026年全球人力資源轉型諮詢市場報告

2026年全球人力資源專業服務市場報告2026年全球人力資源人工智慧市場報告2026年全球人力資源諮詢服務市場報告2026年全球人力資源轉型諮詢市場報告 企業高生產力應用平台即服務市場 - 全球產業規模、佔有率、趨勢、機會、預測:按組件、部署、產業、地區和競爭對手分類,2021-2031 年人力資源諮詢:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

企業高生產力應用平台即服務市場 - 全球產業規模、佔有率、趨勢、機會、預測:按組件、部署、產業、地區和競爭對手分類,2021-2031 年人力資源諮詢:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)