|

市場調查報告書

商品編碼

2072546

人力資源專業服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)HR Professional Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

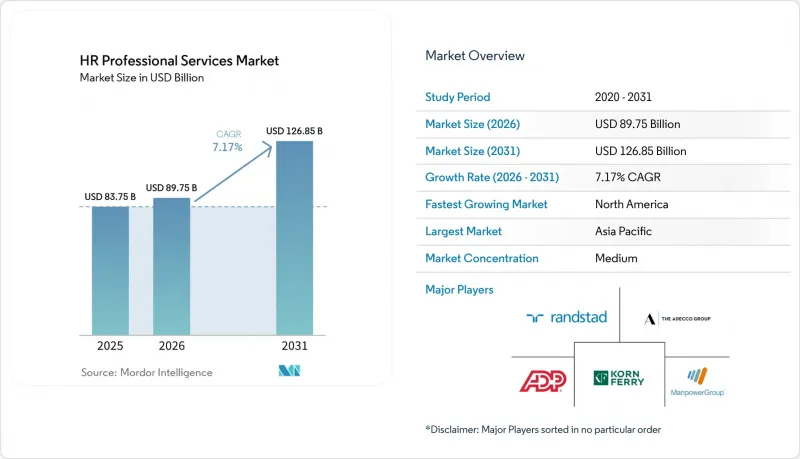

據 Mordor Intelligence 稱,2025 年人力資源專業服務市場價值為 837.5 億美元,預計到 2031 年將達到 1268.5 億美元,而 2026 年為 897.5 億美元,預測期(2026-2031 年)的複合年成長率為 7.17%。

本報告按提供者類型(顧問公司、SaaS(軟體即服務)公司)、功能類型(招聘和人才獲取、福利和計費管理、勞動力規劃和分析、其他)、最終用戶行業(銀行、金融服務和保險、醫療保健、其他)以及地區(北美、其他)進行細分。市場預測以美元計價。

全球人力資源專業服務市場趨勢與洞察

利用生成式人工智慧實現招募自動化

生成式人工智慧正在重塑人才招募的經濟模式,它能夠自動化履歷分析、初步篩選和能力預測評分,從而將平均招募週期縮短三分之一。早期採用者正在將自身的大規模語言模型提示整合到應徵者追蹤系統中,這造成了對平台的強烈依賴,有利於那些擁有整合智慧財產權(IP)的服務供應商。將人工智慧驅動的人才招募與人工面試輔導相結合的供應商報告稱,第一年留存率顯著提高,這一指標現已納入基於績效的收費系統。北美監管機構已發布關於演算法偏差的臨時指南,要求服務提供者在其服務中加入透明的模型審計追蹤。因此,基於SaaS的招募引擎享有溢價,因為內建的管治功能降低了客戶的合規風險。與競爭對手的差異化正在轉向特定領域的訓練數據,醫療保健、銀行和公共部門的案例研究主導了早期採用。隨著這些引擎的成熟,中型買家擴大避免傳統的招聘流程外包(RPO)競標,轉而加速與平台簽訂直接契約,從而擴大了人力資源專業服務市場的潛在客戶群。

數據驅動的薪資核算錯誤預測工具

整合到全球薪資核算服務工作流程中的機器學習模型,如今能夠在付款前檢測出重複記錄和稅碼應用錯誤等異常情況,從而大幅降低了糾正成本,此前平均每個錯誤需要花費 291 美元。預測準確率隨著交易量的增加而提高,這使得小規模供應商處於劣勢,也促使大規模薪資核算聚合商更加關注產業整合。財務長將避免錯誤視為合規保障,因此與批量處理合約相比,他們願意支付 20-25% 的服務費。整合的 API 允許將審計日誌直接髮送到企業資源規劃 (ERP) 系統,無需人工核對即可滿足 SOX 404 的證據要件。供應商正在將薪資分析儀表板打包,將營運數據轉化為策略性的人事費用資訊。各國稅制改革的日益複雜化,促使客戶延長合約期限,並在整個監管週期內鎖定供應商。這些趨勢正在增強人力資源專業服務市場長期獲利能力的穩定且持續的收入來源。

關於資料隱私和資料居住的規定

全球日益嚴格的隱私法規,例如GDPR和中國的《個人資訊保護法》,要求服務提供者按司法管轄區分類其基礎設施,導致營運成本增加15-20%,規模經濟效益下降。持續的監管變化迫使服務提供者反覆進行系統重新設計,審計週期如今已成為客戶合約中的標準條款。跨境資料傳輸的限制要求在國內進行加密金鑰管理,提高了對技術架構師技能水準的要求。為了應對勒索軟體風險,服務提供者承擔了額外的網路保險費用,自2024年以來,該費用已上漲8-12%。因此,客戶正在嚴格審查供應商的安全認證,並將ISO 27001條款納入主服務合約。未能證明端到端合規性可能導致競標被排除在公司的RFP(徵求提案)最終候選名單之外,從而限制其收入來源。這些壓力共同抑制了人力資源專業服務市場短期利潤率的成長。

細分市場分析

預計到2031年,軟體即服務 (SaaS) 供應商的複合年成長率將達到14.67%,在所有提供者類別中成長最快,這主要得益於自助式工作流程獲得了經營團隊的支持。隨著中型買家越來越傾向於訂閱式經營模式而非多年諮詢契約,這些平台上的人力資源專業服務市場正在不斷擴張。 SaaS 供應商正在整合分析儀表板,以便清晰了解招募流程的速度、合規性警報和缺勤趨勢,從而縮短決策週期並降低變更管理預算。諮詢和顧問公司仍將在2025年佔據37.52%的收入佔有率,這主要得益於與併購、監管合規和雲端採用後最佳化相關的複雜轉型項目。一種混合服務模式正在興起,諮詢顧問白牌銷售,並將諮詢收入與許可轉售收入相結合,以期保護其客戶支出佔有率。 Oracle收購 HiredScore 和 Workday 的人工智慧藍圖凸顯了「平台優先」的競爭,即在企業內部整合人才匹配演算法,這給純粹的顧問公司的利潤率帶來了壓力。

現有顧問公司正透過提供基於結果的服務等級協議 (SLA) 來應對挑戰,這些協議保證為監管審計做好準備並提高員工留任率,從而將專業知識貨幣化,使其不再僅依賴計費工時。許多公司現在經營創投工作室,孵化小眾的人力資源技術資產,以確保在談判中獲得智慧財產權優勢。同時,領先的 SaaS 公司正在建立認證部署生態系統,以減少部署摩擦並超越內部服務結構進行擴展。這種相互依存正在模糊類別界限,並導致交叉銷售協議激增。因此,客戶採購團隊正在仔細審查總體擁有成本 (TCO),比較將諮詢服務和 SaaS 費用捆綁在一起的方案與單獨的平台訂閱方案。隨著生態系的成熟,平台管治標準逐漸建立,互通性和開放 API 正成為供應商選擇的關鍵標準。

區域分析

北美地區擁有高度成熟的企業外包模式和強大的HR技術供應商生態系統,為相關服務業提供支持,預計到2025年將保持39.45%的市場佔有率,繼續保持領先地位。該地區聯邦、省和州級監管的多樣性持續支撐著對區域性合規諮詢的需求。在加拿大,省級勞動法正在推動平台擴張,帶來高於平均的成長。同時,在墨西哥,近岸外包熱潮正在推動高價雙語人力資源政策協調專案的發展。美國供應商正在南部邊境沿線擴展雙語服務中心,以滿足新興加工出口區(maquiladoras)對薪資核算服務的需求。創業投資地湧入人力資源科技新創企業,進一步加速了創新週期,使服務合作夥伴能夠將其專有工具整合到託管服務協議中。

亞太地區是成長最快的地區,預計複合年成長率將達到10.07%,這主要得益於經濟擴張和數位政府措施強制推行電子工資申報和即時勞動力數據報告。印度的服務交付模式正在從成本驅動的外包模式轉向高價值人力資源分析服務的出口模式轉變,吸引了需要整合全球和本地交付模式的跨國公司總部專案。中國嚴格的資料本地化法律促進了合資企業的形成,外國供應商可以利用國內雲端基礎設施來滿足居住要求。東南亞人才短缺的市場依賴外部供應商來滿足合規性和擴大薪資核算規模的需求,推高了合約續約率。在澳洲和韓國,基於績效的合約正在穩步發展,當供應商能夠提供清晰的人才保留和多元化關鍵績效指標(KPI)時,溢價是合理的。越南和印尼等新興經濟體正在超越傳統的本地部署系統,採用「行動優先」的人力資源應用程式,這些應用程式與本地電子錢包生態系統整合,以實現靈活的薪水支付。

在歐洲,由於GDPR合規成本使供應商的營運支出增加了15-20%,且宏觀經濟的不確定性限制了企業的IT預算,因此複合年成長率(CAGR)的預測相對保守。儘管如此,在與勞工委員會談判和共同決策法方面擁有專業知識的供應商正在德國和法國獲得長期合約。在英國,脫歐後與歐盟勞動法的差異催生了針對跨區域企業的諮詢服務這一利基市場需求。比荷盧經濟聯盟和北歐國家的客戶對基於結果的合約表現出最高的興趣,這反映出他們對分析技術的成熟應用以及對可衡量結果的重視。由於高失業率和預算限制,南歐發展滯後,但歐盟復甦基金資助的公共部門現代化計畫正在湧現。營運泛歐資料網格架構的供應商正透過隱私工程實現差異化,從而減輕跨多個司法管轄區的客戶的合規負擔。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 利用基因人工智慧實現招募流程自動化

- 數據驅動的薪資核算錯誤預測工具

- 對超本地化合規專業知識的需求

- 將人力資源分析整合到 ERP 系統中

- 傳統人力資源管理系統的雲端遷移

- 績效型人力資源服務合約的興起

- 市場限制因素

- 資料隱私和居住法規

- 多個國家都面臨薪資核算專員短缺的問題

- 新興市場勞動法的碎片化

- 人力資源外包公司網路保險保費上漲

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 按服務提供者類型

- 顧問公司

- SaaS(軟體即服務)公司

- 依功能類型

- 招募和人才獲取

- 福利/理賠管理

- 人員規劃與分析

- 薪資和薪資管理

- 其他功能

- 按最終用戶行業分類

- BFSI

- 衛生保健

- 資訊科技/通訊

- 製造業

- 零售

- 政府

- 其他行業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 秘魯

- 智利

- 阿根廷

- 其他南美國家

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 比荷盧經濟聯盟(比利時、荷蘭、盧森堡)

- 北歐國家(丹麥、芬蘭、冰島、挪威、瑞典)

- 其他歐洲國家

- 亞太地區

- 印度

- 中國

- 日本

- 澳洲

- 韓國

- 東南亞(新加坡、馬來西亞、泰國、印尼、越南、菲律賓)

- 其他亞太國家

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- ADP

- Randstad NV

- Adecco Group

- ManpowerGroup

- Korn Ferry

- IBM

- Accenture

- Paychex

- Ceridian

- Workday

- SAP

- Oracle

- Mercer

- Deloitte

- Willis Towers Watson

- Infosys

- Tata Consultancy Services

- Neeyamo

- SD Worx

- Alight Solutions

第7章 市場機會與未來展望

According to Mordor Intelligence, the HR professional services market size was valued at USD 83.75 billion in 2025 and estimated to grow from USD 89.75 billion in 2026 to reach USD 126.85 billion by 2031, at a CAGR of 7.17% during the forecast period (2026-2031).

This report is Segmented by Provider Type (Consulting Companies, Software-As-A-Service Companies), Function Type (Recruitment and Talent Acquisition, Benefits and Claims Management, Workforce Planning and Analytics, and Other), End-User Industry (BFSI, Healthcare, and Other), and Geography (North America, and Other). The Market Forecasts are Provided in Terms of Value (USD).

Global HR Professional Services Market Trends and Insights

Gen-AI Powered Recruitment Automation

Generative AI is redefining talent acquisition economics by automating resume parsing, initial screenings, and predictive fit scoring, which collectively shrink average hiring cycles by one-third. Early adopters are layering proprietary large-language-model prompts onto applicant-tracking systems, creating sticky platform dependencies that favor service providers owning integrated IP. Vendors pairing AI sourcing with human interview coaching report notable improvements in first-year retention, a metric now embedded in outcome-based fee schedules. Regulatory bodies in North America have issued preliminary algorithmic bias guidelines, pushing providers to build transparent model-audit trails into their offerings. SaaS-first recruitment engines consequently enjoy a pricing premium because built-in governance reduces client compliance risk. Competitive differentiation is shifting toward domain-specific training data; healthcare, banking, and public sector examples dominate early proof points. As these engines mature, mid-market buyers increasingly bypass traditional RPO bids, accelerating direct platform subscriptions that widen the HR professional services market addressable pool.

Data-Driven Payroll Error-Prediction Tools

Machine-learning models embedded in global payroll service workflows now flag anomalies such as duplicate records or irregular tax code application before funds disburse, slashing remediation costs that historically averaged USD 291 per error. The predictive accuracy rises with transaction volume, which places small providers at a disadvantage and fuels consolidation interest from larger payroll aggregators. CFOs perceive error-avoidance capabilities as compliance insurance, legitimizing 20-25% service fee uplifts compared with batch-processing contracts. Integration APIs feed audit logs directly to enterprise resource planning systems, satisfying SOX 404 evidence requirements without manual reconciliations. Vendors are bundling payroll analytics dashboards, turning operational data into strategic workforce cost intelligence. The complexity of country-specific tax reforms encourages clients to extend contract durations, locking in providers for full regulatory cycles. These dynamics reinforce sticky recurring revenue streams that underpin long-run margins within the HR professional services market.

Data-Privacy & Residency Regulations

Tightening global privacy laws such as GDPR and China's PIPL obligate providers to segment infrastructure by jurisdiction, adding 15-20% to operating costs and diluting scale benefits. Ongoing regulatory churn forces recurrent system redesigns, with audit cycles now standard practice across client contracts. Cross-border data-transfer restrictions compel in-country encryption key management, elevating technical-architect skill requisites. Providers absorb incremental cyber-insurance premiums, which have climbed 8-12% since 2024 in response to ransomware risk . Clients consequently scrutinize vendor security certifications, embedding ISO 27001 clauses into master service agreements. Failure to demonstrate end-to-end compliance can disqualify bidders from enterprise RFP shortlists, limiting revenue pipelines. Cumulatively, these pressures temper near-term margin expansion within the HR professional services market.

Other drivers and restraints analyzed in the detailed report include:

- Hyper-Local Compliance Expertise Demand

- Integration of HR Analytics into ERP Stacks

- Shortage of Multi-Country Payroll Talent

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software-as-a-Service suppliers are on track to post a 14.67% CAGR to 2031, reflecting the fastest expansion among provider categories as self-service workflows gain board-level sponsorship. The HR professional services market size for these platforms is widening because mid-market buyers increasingly favor subscription economics over multi-year consulting retainers. SaaS vendors embed analytic dashboards that visualize hiring funnel velocity, compliance alerts, and absenteeism trends, traits that compress decision cycles and shrink change-management budgets. Consulting & Advisory firms still held 37.52% revenue share in 2025 through complex transformation mandates tied to mergers, regulatory remediation, and post-cloud optimization. Hybrid service models are emerging in which consultants white-label partner SaaS modules, blending advisory revenue with license resale in an effort to defend wallet share. Oracle's acquisition of HiredScore and Workday's AI roadmap underscore a platform-first race to internalize talent-matching algorithms, putting margin pressure on pure-play consultancies.

Consulting incumbents counter by packaging outcome-based SLAs that guarantee regulatory audit readiness or retention uplift, thereby monetizing domain expertise beyond billable hours. Many firms now operate venture studios that spin out niche HR tech assets to secure intellectual-property leverage in negotiations. In parallel, SaaS leaders cultivate certified implementation ecosystems to reduce onboarding friction and unlock scale beyond internal service benches. This reciprocal interdependence blurs categorical boundaries, with cross-selling agreements proliferating. Client procurement teams thus weigh total-cost-of-ownership scenarios comparing bundled advisory plus SaaS fees to stand-alone platform subscriptions. As ecosystems mature, platform governance standards emerge, making interoperability and open APIs critical vendor-selection criteria.

Complete Report Scope:

- By Provider Type

- Consulting Companies

- Software-as-a-Service Companies

- By Function Type

- Recruitment And Talent Acquisition

- Benefits And Claims Management

- Workforce Planning and Analytics

- Payroll And Compensation Management

- Other Functions

- By Function Type

- BFSI

- Healthcare

- IT and Telecom

- Manufacturing

- Retail

- Government

- Other Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- Rest of Europe

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South-East Asia (SG, MY, TH, ID, VN, PH)

- Rest of Asia-Pacific

- Middle East & Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East & Africa

- North America

Geography Analysis

North America preserved its lead with 39.45% revenue share in 2025 owing to high enterprise outsourcing maturity and a robust ecosystem of HR technology vendors that feed adjacent service streams. The region's regulatory heterogeneity across federal, state, and provincial jurisdictions sustains demand for localized compliance advisory. Canada posts above-average growth as provincial employment codes drive incremental platform configurations, while Mexico's near-shoring boom triggers bilingual HR policy harmonization projects that command premium rates. U.S. providers have expanded bilingual service hubs along the southern border to capture emerging maquiladora payroll volumes. A steady flow of venture capital into HR tech start-ups further fuels innovation cycles, enabling service partners to bundle proprietary tools into managed-service agreements.

Asia-Pacific represents the fastest-growing geography with a projected 10.07% CAGR, propelled by economic expansion and digital-government initiatives that mandate electronic payroll filing and real-time labor data reporting. India's service-delivery heritage is evolving from cost-centric outsourcing to value-added HR analytics exports, drawing multinational headquarters projects that require integrated global-in-country delivery models. China's stringent data-localization laws encourage joint-venture structures wherein foreign providers leverage domestic cloud infrastructure to meet residency requirements. Southeast Asia's talent-scarce markets rely on external providers for compliance and payroll scale, fostering high contract-renewal rates. Australia and South Korea show steady uptake of outcome-based contracts, validating premium pricing when vendors present clear retention or diversity KPIs. Emerging economies such as Vietnam and Indonesia are leapfrogging legacy on-premises systems, adopting mobile-first HR applications that integrate with regional e-wallet ecosystems for flexible pay disbursement.

Europe records a relatively restrained CAGR outlook as GDPR compliance costs add 15-20% to provider operating expenses and macroeconomic uncertainty tempers corporate IT budgets. Nevertheless, specialized vendors fluent in works-council negotiations and co-determination statutes secure long-term engagements in Germany and France. The United Kingdom's post-Brexit divergence from EU labor codes creates niche advisory demand for companies straddling both territories. BENELUX and Nordic clients display the highest appetite for performance-linked contracts, reflecting mature analytics adoption and cultural emphasis on measurable outcomes. Southern Europe lags due to higher unemployment and budget constraints, yet public-sector modernization projects financed by EU recovery funds are emerging. Providers operating pan-European data mesh architectures differentiate on privacy engineering, reducing compliance overhead for multi-jurisdiction clients.

- ADP

- Randstad NV

- Adecco Group

- ManpowerGroup

- Korn Ferry

- IBM

- Accenture

- Paychex

- Ceridian

- Workday

- SAP

- Oracle

- Mercer

- Deloitte

- Willis Towers Watson

- Infosys

- Tata Consultancy Services

- Neeyamo

- SD Worx

- Alight Solutions

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Gen-AI powered recruitment automation

- 4.2.2 Data-driven payroll error-prediction tools

- 4.2.3 Hyper-local compliance expertise demand

- 4.2.4 Integration of HR analytics into ERP stacks

- 4.2.5 Cloud migration of legacy HR suites

- 4.2.6 Rise of outcome-based HR service contracts

- 4.3 Market Restraints

- 4.3.1 Data-privacy & residency regulations

- 4.3.2 Shortage of multi-country payroll talent

- 4.3.3 Fragmented labour laws in emerging markets

- 4.3.4 Rising cyber-insurance premiums for HRO firms

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Provider Type

- 5.1.1 Consulting Companies

- 5.1.2 Software-as-a-Service Companies

- 5.2 By Function Type

- 5.2.1 Recruitment And Talent Acquisition

- 5.2.2 Benefits And Claims Management

- 5.2.3 Workforce Planning and Analytics

- 5.2.4 Payroll And Compensation Management

- 5.2.5 Other Functions

- 5.3 By Function Type

- 5.3.1 BFSI

- 5.3.2 Healthcare

- 5.3.3 IT and Telecom

- 5.3.4 Manufacturing

- 5.3.5 Retail

- 5.3.6 Government

- 5.3.7 Other Industries

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Peru

- 5.4.2.3 Chile

- 5.4.2.4 Argentina

- 5.4.2.5 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Spain

- 5.4.3.5 Italy

- 5.4.3.6 BENELUX (Belgium, Netherlands, Luxembourg)

- 5.4.3.7 NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- 5.4.3.8 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 India

- 5.4.4.2 China

- 5.4.4.3 Japan

- 5.4.4.4 Australia

- 5.4.4.5 South Korea

- 5.4.4.6 South-East Asia (SG, MY, TH, ID, VN, PH)

- 5.4.4.7 Rest of Asia-Pacific

- 5.4.5 Middle East & Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Nigeria

- 5.4.5.5 Rest of Middle East & Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 ADP

- 6.4.2 Randstad NV

- 6.4.3 Adecco Group

- 6.4.4 ManpowerGroup

- 6.4.5 Korn Ferry

- 6.4.6 IBM

- 6.4.7 Accenture

- 6.4.8 Paychex

- 6.4.9 Ceridian

- 6.4.10 Workday

- 6.4.11 SAP

- 6.4.12 Oracle

- 6.4.13 Mercer

- 6.4.14 Deloitte

- 6.4.15 Willis Towers Watson

- 6.4.16 Infosys

- 6.4.17 Tata Consultancy Services

- 6.4.18 Neeyamo

- 6.4.19 SD Worx

- 6.4.20 Alight Solutions

7 Market Opportunities & Future Outlook

- 7.1 Embedded payroll-fintech services

- 7.2 AI-driven employee wellness analytics

人力專業服務市場規模、佔有率和成長分析:按服務類型、部署模式、組織規模、最終用戶產業和地區分類-2026-2033年產業預測

人力專業服務市場規模、佔有率和成長分析:按服務類型、部署模式、組織規模、最終用戶產業和地區分類-2026-2033年產業預測 人力資源轉型服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

人力資源轉型服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 人力資源(HR)技術市場規模、佔有率和成長分析:按類型、部署模式、組織規模、最終用戶、產業和地區分類-2026-2033年產業預測

人力資源(HR)技術市場規模、佔有率和成長分析:按類型、部署模式、組織規模、最終用戶、產業和地區分類-2026-2033年產業預測 人力資源(HR)技術市場規模、佔有率、趨勢和預測:按應用、類型、最終用戶行業、企業規模和地區分類,2026-2034年

人力資源(HR)技術市場規模、佔有率、趨勢和預測:按應用、類型、最終用戶行業、企業規模和地區分類,2026-2034年 2026年全球人力資源專業服務市場報告2026年全球人力資源人工智慧市場報告2026年全球人力資源諮詢服務市場報告2026年全球人力資源轉型諮詢市場報告

2026年全球人力資源專業服務市場報告2026年全球人力資源人工智慧市場報告2026年全球人力資源諮詢服務市場報告2026年全球人力資源轉型諮詢市場報告 企業高生產力應用平台即服務市場 - 全球產業規模、佔有率、趨勢、機會、預測:按組件、部署、產業、地區和競爭對手分類,2021-2031 年人力資源諮詢:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

企業高生產力應用平台即服務市場 - 全球產業規模、佔有率、趨勢、機會、預測:按組件、部署、產業、地區和競爭對手分類,2021-2031 年人力資源諮詢:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)