|

市場調查報告書

商品編碼

2072682

北美人力資源服務配送平臺:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)North America HR Service Delivery Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

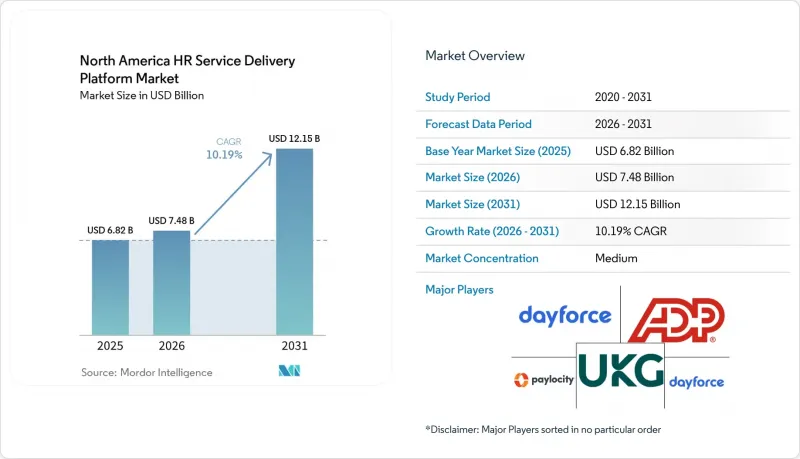

根據 Mordor Intelligence 預測,北美人力資源服務配送平臺市場規模將從 2025 年的 68.2 億美元和 2026 年的 74.8 億美元成長到 2031 年的 121.5 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 10.19%。

本報告按元件(軟體和服務)、部署模式(雲端、本地部署、混合部署)、企業規模(大型企業、中小企業)、最終用戶產業(銀行、金融服務和保險、醫療保健和生命科學、資訊科技和電信、其他)以及地區進行細分。市場預測以美元計價。

北美人力資源服務配送平臺市場的趨勢與洞察。

從傳統人力資源系統遷移到雲端

在北美人力資源服務配送平臺市場,雲端遷移仍是短期內最主要的促進因素。企業正尋求以整合系統取代分散的人力資源工具,以便在單一環境中支援服務交付、薪資核算和分析。 SAP 於 2025 年推出了 SuccessFactors 企業服務管理平台,將人力資源案例處理與智慧自助服務相結合,這反映了該公司向整合雲端服務層而非孤立模組轉型的趨勢。 Workday 於 2026 年將 Sana 擴展到其整個人力資源和財務工作流程,顯示領先的平台越來越注重執行自動化操作,而不僅僅是記錄任務。微軟也推出了員工自助服務代理,透過單一介面連接 SharePoint、Workday 和 ServiceNow 中的知識和工作流程資源,幫助企業從分散的傳統系統遷移。由於許多公司不會一次取代所有核心系統,因此這種遷移催生了對連接器、薪資核算整合和工作流程編配的需求。因此,雲端遷移正在推動軟體需求成長,同時也為整個北美人力資源服務配送平臺市場的部署和管理服務供應商擴大了商機。

對整合式員工自助服務和案例管理的需求日益成長。

在北美人力資源服務配送平臺市場,隨著雇主尋求在不增加服務台人員的情況下快速解決問題,對整合式員工自助服務和案例管理的需求日益成長。 IBM 表示,其 AskHR 平台目前可自動處理 80 多項人力資源任務,每年處理超過 210 萬次員工互動。這表明,人工智慧主導的自助服務可以大規模應用於企業級運營,而不僅僅是作為試點功能。 SAP 於 2025 年發布了 SuccessFactors 企業服務管理平台,隨後透過 Joule 助理擴展了其服務解決能力。這進一步強化了向集中式案例接收、路由和員工支援的單一平台的轉變。微軟的員工自助服務代理也表明,雇主正在尋求透過將人力資源知識和營運支援整合到單一互動式介面中來消除系統切換。隨著這些工具的改進,案例分流不再只是削減成本的措施,而是成為服務品質的一部分,因為它使人力資源團隊能夠將更多時間投入到敏感問題和複雜的人才挑戰中。此外,文件記錄、稽核追蹤和員工存取控制等因素也促使組織使用專為人力資源案例設計的工具,而不是通用的工單管理系統。

資料隱私和跨境員工資料管理

資料隱私和跨境員工資料管理正在減緩採購流程。這是因為在北美人力資源服務配送平臺市場,雇主必須仔細審查薪資單、個案數據和薪資記錄在不同司法管轄區之間的流動情況。修訂後的加州《消費者隱私法案》(CCPA) 將於2026年1月1日生效,該法案要求某些雇主在處理涉及重大隱私風險(例如使用自動化決策)的人力資源資料之前,必須進行正式的隱私風險評估。對於跨國公司而言,歐盟和北美系統之間員工資料的傳輸也需要系統化的合規框架,這需要在簽訂合約前進行法律審查和供應商審計。這通常有利於能夠提供更統一的GDPR、CCPA和PIPEDA合規框架的大規模平台。小規模、專注於特定領域的工具在功能上仍然具有競爭力,但由於採購團隊優先考慮隱私認證和資料處理管理,因此它們的銷售週期往往更長。因此,需求並未減少,但卻導致部署延遲,並增加了買賣雙方的合規負擔。

細分市場分析

到2025年,軟體將佔據71.82%的市場佔有率,成為北美人力資源服務配送平臺市場中最大的組成部分。核心人力資源、薪資福利和員工服務管理模組(處理量最大的流程)將繼續成為中大型企業採購支出的基礎。隨著企業以整合到日常工作流程中的功能取代單獨的儀錶板和單一功能工具,他們在人力分析、人才管理和人力資源管理方面的軟體支出也在增加。 2025年和2026年的產品發布清晰地展現了這一趨勢,企業服務管理和自主HCM功能將大部分服務解決和決策支援轉移到軟體層本身。由於企業傾向於選擇能夠減少系統切換並提高資料完整性的綜合套件,軟體仍然是收入的重要支柱。

預計到2031年,服務業將以12.47%的複合年成長率成長,成為北美人力資源服務配送平臺市場成長最快的細分領域。 2026年4月,一項新的託管解決方案發布,該方案配備專門團隊代表客戶管理薪資核算和人力資源運營,這反映出市場對持續管理支援的需求日益成長,而非一次性實施。 2026年2月,其他供應商也開始向尋求實施支援的中小型企業普遍提供捆綁式人力資源服務,將科技與實際的人力資源支援結合。由於人工智慧管治、薪資核算管理、資料管理和運作調優都需要持續支持,即使軟體引進週期變得更加高效,業務收益預計仍將保持強勁成長。

預計到2025年,基於雲端的部署將佔北美人力資源服務配送平臺市場的65.30%,證實了SaaS將成為主導交付模式。雲端模式之所以依然具有吸引力,是因為它支援更快的功能更新、更便捷的員工存取以及在大規模的員工群體中更輕鬆地部署人工智慧驅動的工作流程。它也符合當前的採購趨勢,即需要整合平台來連接跨部門的核心人力資源、自助服務和分析功能。對於某些組織,例如政府機構、國防機構和金融業,本地部署環境仍然很重要,因為這些機構在資料處理方面受到更嚴格的監管。儘管如此,北美人力資源服務產業仍在繼續向雲端主導的營運模式轉型,因為大多數新的自動化功能都是首先在雲端建置的。

混合部署預計到2031年將以11.93%的複合年成長率成長,成為成長最快的部署方式。大規模企業通常會保留傳統的本地ERP和薪資核算系統,同時將員工自助服務、分析和服務管理遷移到雲端。這一趨勢使得混合架構成為深思熟慮的設計選擇,而非舊有系統和完全SaaS之間的臨時過渡方案。新興的邊緣到雲端模式進一步擴展了這個邏輯,使企業能夠透過雲端介面與員工進行AI互動,同時在嚴格控制的環境中處理敏感記錄。這解釋了為什麼在北美人力資源服務配送平臺市場,混合部署的採用率隨著雲端的成長而增加,而不是隨著轉型進程的推進而消失。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 從傳統人力資源系統遷移到雲端

- 對整合式員工自助服務和案例管理的需求日益成長。

- 對即時勞動力分析和工作流程自動化的需求

- 透過混合式和分散式工作模式,拓展與數位人才的連結。

- 歐盟的《工資透明度指令》強制要求對工作和工資資料進行標準化。

- 基於技能的人才規劃與內部人才流動

- 市場限制因素

- 資料隱私和員工資料的跨境管理

- 與現有ERP系統和薪資核算系統整合的複雜性。

- 歐盟人工智慧法律及演算法在就業決策中的課責

- 資料主權和區域託管要求

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 軟體

- 核心人員

- 員工服務管理與幫助台

- 薪資/報酬

- 勞動力管理

- 人才管理

- 人力資源分析與報告編制

- 學習與技能發展

- 服務

- 軟體

- 按部署模式

- 基於雲端的

- 現場

- 混合

- 按最終用戶公司規模分類

- 大公司

- 小型企業

- 按最終用戶行業分類

- BFSI

- 醫療保健和生命科學

- 資訊科技/通訊

- 零售與電子商務

- 工業製造

- 政府/公共部門

- 其他終端用戶產業

- 按地區

- 美國

- 加拿大

- 墨西哥

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介。

- Workday, Inc.

- Automatic Data Processing, Inc.

- Ultimate Kronos Group, Inc.

- Dayforce, Inc.

- Paycom Software, Inc.

- Paylocity Holding Corporation

- Paychex, Inc.

- Paycor HCM, Inc.

- Bamboo HR LLC

- Hi Bob Limited

- Gusto Inc.

- Darwinbox Digital Solutions Private Limited

- Rippling People Center Inc.

- Deel Inc.

- Papaya Global Ltd.

- Remote Technology, Inc.

- isolved Inc.

- ServiceNow, Inc.

- Namely, Inc.

- Workable Technology Limited

第7章 市場機會與未來展望

According to Mordor Intelligence, the north america HR service delivery platform market size is projected to expand from USD 6.82 billion in 2025 and USD 7.48 billion in 2026 to USD 12.15 billion by 2031, registering a CAGR of 10.19% between 2026 and 2031.

This report is Segmented by Component (Software and Services), Deployment Model (Cloud-Based, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (BFSI, Healthcare and Life Sciences, Information Technology and Telecom, and More ), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America HR Service Delivery Platform Market Trends and Insights

Cloud Migration from Legacy Human Resources Stacks

Cloud migration remains the clearest near-term driver of the North America HR service delivery platform market, as enterprises seek to replace disconnected HR tools with unified systems that support service delivery, payroll, and analytics in a single environment. SAP introduced SuccessFactors Enterprise Service Management in 2025 to connect HR case handling with intelligent self-service, reflecting the vendor's broader move toward integrated cloud service layers rather than isolated modules. Workday expanded Sana in 2026 across HR and finance workflows, demonstrating that major platforms are now being designed for action-taking automation rather than only system-of-record tasks. Microsoft also deployed its Employee Self-Service Agent to connect knowledge and workflow sources across SharePoint, Workday, and ServiceNow through a single interface, supporting the shift away from fragmented legacy stacks. This migration is creating follow-on demand for connectors, payroll integrations, and workflow orchestration, as most enterprises are not replacing every core system at once. The result is that cloud migration is lifting software demand while also extending revenue opportunities for implementation and managed service providers across the North America HR service delivery platform market.

Rising Demand for Unified Employee Self-Service And Case Management

Demand for unified employee self-service and case management is rising because employers want faster issue resolution without adding service desk headcount across the North America HR service delivery platform market. IBM stated that its AskHR platform now automates more than 80 HR tasks and handles more than 2.1 million employee conversations each year, which shows that AI-led self-service can operate at enterprise scale rather than as a pilot feature. SAP launched SuccessFactors Enterprise Service Management in 2025 and later extended service resolution capabilities through Joule assistants, reinforcing the move toward a single platform for case intake, routing, and employee support. Microsoft's Employee Self-Service Agent also showed how employers are trying to remove system switching by bringing HR knowledge and transaction support into a single conversational interface. As these tools improve, case deflection is moving beyond a cost measure and becoming part of service quality because HR teams can spend more time on sensitive or complex workforce issues. Documentation, audit trails, and employee access controls are also driving organizations toward purpose-built HR case tools rather than generic ticketing systems.

Data Privacy And Cross-Border Employee Data Controls

Data privacy and cross-border employee data controls are slowing procurement because employers must review how payroll, case data, and compensation records move across jurisdictions in the North America HR service delivery platform market. California's amended CCPA regulations, effective January 1, 2026, required certain employers to conduct formal privacy risk assessments before processing HR data tied to significant privacy risk, including automated decision-making uses. For multinational employers, employee data transfers between the EU and North American systems also require structured compliance mechanisms, which adds legal review and vendor audit work before contracts are signed. This tends to favor larger platforms that can present a more unified compliance posture across GDPR, CCPA, and PIPEDA requirements. Smaller or niche tools can still compete on features, but they face a longer sales cycle when procurement teams prioritize privacy certifications and data-handling controls. The result is not lower demand, but slower deployment and a higher compliance burden for buyers and vendors alike.

Other drivers and restraints analyzed in the detailed report include:

- Need for Real-Time Workforce Analytics and Workflow Automation

- Hybrid and Distributed Work Models Expanding Digital Human Resources Touchpoints

- Integration Complexity With Legacy Enterprise Resource Planning And Payroll Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software held a 71.82% share of the market in 2025, making it the largest component of the North America HR service delivery platform market. Core HR, payroll, and compensation, and employee service management modules remain the base of buyer spending because they handle the highest-volume processes across large and mid-sized organizations. Buyers are also directing more software spend toward people analytics, talent management, and workforce management as they replace separate dashboards and point tools with functions embedded inside daily workflows. Product releases in 2025 and 2026 clearly showed this direction, with enterprise service management and autonomous HCM capabilities moving more service resolution and decision support into the software layer itself. This keeps software as the revenue anchor because enterprises prefer broad suites that reduce switching across systems and tighten data consistency.

Services are projected to grow at a 12.47% CAGR through 2031, making it the fastest-moving component segment in the North America HR service delivery platform market. In April 2026, new managed solutions were launched with dedicated teams that administer payroll and HR operations on behalf of clients, which reflects rising demand for managed support rather than one-time implementation work. Other providers also made bundled HR services generally available in February 2026, combining technology with hands-on HR support for smaller employers seeking execution support. AI governance, payroll administration, data stewardship, and post-go-live tuning all require ongoing support, which means services revenue should remain strong even when software deployment cycles become more efficient.

Cloud-based deployment accounted for 65.30% of the North America HR service delivery platform market share in 2025, which confirmed SaaS as the leading delivery model. The cloud model continues to appeal because it supports faster feature updates, better employee access, and easier rollout of AI-enabled workflows across large workforces. It also aligns with current buying preferences for unified platforms that connect core HR, self-service, and analytics across departments. On-premises environments remain relevant for a smaller group of organizations in government, defense, and tightly regulated financial settings where data-handling restrictions are stricter. Even so, the North America HR service delivery industry continues to move toward cloud-led operating models because most new automation capabilities are being built there first.

Hybrid deployment is projected to expand at a 11.93% CAGR through 2031, making it the fastest-growing deployment approach. Large employers often retain older on-premises ERP or payroll systems while moving employee self-service, analytics, and service management to the cloud. That pattern is turning hybrid architecture into a deliberate design choice rather than a temporary midpoint between legacy and full SaaS. The emerging edge-to-cloud model extends this logic further, enabling employers to run employee-facing AI interactions through cloud interfaces while routing sensitive records through more controlled environments. This helps explain why hybrid adoption is rising alongside cloud growth in the North America HR service delivery platform market instead of disappearing as migration advances.

Complete Report Scope:

- By Component

- Software

- Core Human Resources

- Employee Service Management and Helpdesk

- Payroll and Compensation

- Workforce Management

- Talent Management

- People Analytics and Reporting

- Learning and Development

- Services

- Software

- By Deployment Model

- Cloud-Based

- On-Premises

- Hybrid

- By End User Enterprise Size

- Large Enterprises

- Small and Medium-Sized Enterprises

- By End-user Industry

- BFSI

- Healthcare and Life Sciences

- Information Technology and Telecom

- Retail and E-commerce

- Industrial Manufacturing

- Government and Public Sector

- Other End-user Industries

- By Geography

- United States

- Canada

- Mexico

List of Companies Covered in this Report:

- Workday, Inc.

- Automatic Data Processing, Inc.

- Ultimate Kronos Group, Inc.

- Dayforce, Inc.

- Paycom Software, Inc.

- Paylocity Holding Corporation

- Paychex, Inc.

- Paycor HCM, Inc.

- Bamboo HR LLC

- Hi Bob Limited

- Gusto Inc.

- Darwinbox Digital Solutions Private Limited

- Rippling People Center Inc.

- Deel Inc.

- Papaya Global Ltd.

- Remote Technology, Inc.

- isolved Inc.

- ServiceNow, Inc.

- Namely, Inc.

- Workable Technology Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud Migration From Legacy Human Resources Stacks

- 4.2.2 Rising Demand For Unified Employee Self-Service and Case Management

- 4.2.3 Need For Real-Time Workforce Analytics and Workflow Automation

- 4.2.4 Hybrid and Distributed Work Models Expanding Digital Human Resources Touchpoints

- 4.2.5 European Union Pay Transparency Directive Forcing Harmonized Job and Pay Data

- 4.2.6 Skills-Based Workforce Planning and Internal Talent Mobility

- 4.3 Market Restraints

- 4.3.1 Data Privacy and Cross-Border Employee Data Controls

- 4.3.2 Integration Complexity With Legacy Enterprise Resource Planning and Payroll Systems

- 4.3.3 European Union Artificial Intelligence Act and Algorithmic Accountability For Employment Decisions

- 4.3.4 Data Sovereignty and Regional Hosting Requirements

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Comptetive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.1.1 Core Human Resources

- 5.1.1.2 Employee Service Management and Helpdesk

- 5.1.1.3 Payroll and Compensation

- 5.1.1.4 Workforce Management

- 5.1.1.5 Talent Management

- 5.1.1.6 People Analytics and Reporting

- 5.1.1.7 Learning and Development

- 5.1.2 Services

- 5.1.1 Software

- 5.2 By Deployment Model

- 5.2.1 Cloud-Based

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By End User Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-Sized Enterprises

- 5.4 By End-user Industry

- 5.4.1 BFSI

- 5.4.2 Healthcare and Life Sciences

- 5.4.3 Information Technology and Telecom

- 5.4.4 Retail and E-commerce

- 5.4.5 Industrial Manufacturing

- 5.4.6 Government and Public Sector

- 5.4.7 Other End-user Industries

- 5.5 By Geography

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 Workday, Inc.

- 6.4.2 Automatic Data Processing, Inc.

- 6.4.3 Ultimate Kronos Group, Inc.

- 6.4.4 Dayforce, Inc.

- 6.4.5 Paycom Software, Inc.

- 6.4.6 Paylocity Holding Corporation

- 6.4.7 Paychex, Inc.

- 6.4.8 Paycor HCM, Inc.

- 6.4.9 Bamboo HR LLC

- 6.4.10 Hi Bob Limited

- 6.4.11 Gusto Inc.

- 6.4.12 Darwinbox Digital Solutions Private Limited

- 6.4.13 Rippling People Center Inc.

- 6.4.14 Deel Inc.

- 6.4.15 Papaya Global Ltd.

- 6.4.16 Remote Technology, Inc.

- 6.4.17 isolved Inc.

- 6.4.18 ServiceNow, Inc.

- 6.4.19 Namely, Inc.

- 6.4.20 Workable Technology Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

全球末端配送自動化市場預測(至2034年):按組件、技術、配送方式、應用、最終用戶和地區分類的分析

全球末端配送自動化市場預測(至2034年):按組件、技術、配送方式、應用、最終用戶和地區分類的分析 人力資源服務配送平臺:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

人力資源服務配送平臺:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026年全球服務交付自動化市場報告

2026年全球服務交付自動化市場報告 服務提供自動化市場:按組件、產業、部署類型和組織規模分類 - 2026-2032 年全球預測

服務提供自動化市場:按組件、產業、部署類型和組織規模分類 - 2026-2032 年全球預測 全球服務提供自動化市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球服務提供自動化市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 服務提供自動化市場規模、佔有率和成長分析(按組件、類型、使用者類型、垂直產業和地區分類)-2026-2033年產業預測服務提供自動化市場預測至 2032 年:按類型、產品、組件、部署模式、應用、最終用戶和地區分類的全球分析服務提供平台:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)服務提供自動化:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)

服務提供自動化市場規模、佔有率和成長分析(按組件、類型、使用者類型、垂直產業和地區分類)-2026-2033年產業預測服務提供自動化市場預測至 2032 年:按類型、產品、組件、部署模式、應用、最終用戶和地區分類的全球分析服務提供平台:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)服務提供自動化:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)