|

市場調查報告書

商品編碼

2072678

人力資源服務配送平臺:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)HR Service Delivery Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

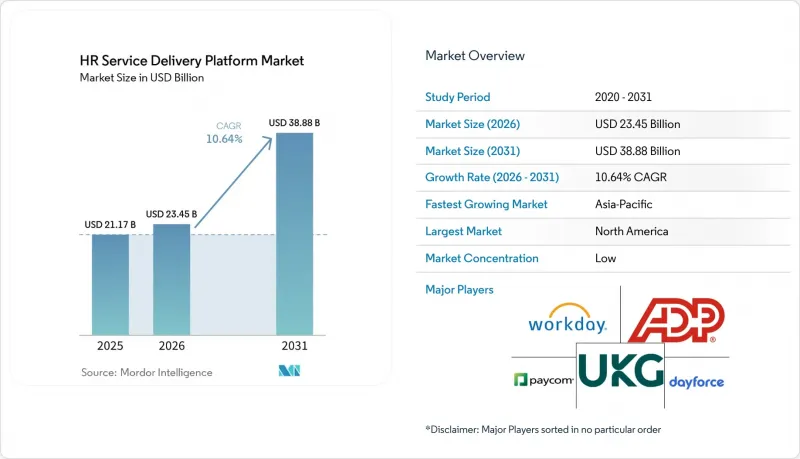

根據 Mordor Intelligence 預測,人力資源服務配送平臺市場預計將從 2025 年的 212.7 億美元成長到 2026 年的 234.5 億美元,到 2031 年達到 388.8 億美元,2026 年至 2031 年的複合年成長率為 10.64%預計。

本報告按組件(軟體和服務)、部署模式(雲端、本地部署、混合部署)、企業規模(大型企業和中小企業)、最終用戶行業(銀行、金融服務和保險、醫療保健和生命科學、資訊技術和電信、零售和電子商務等)以及地區進行細分。市場預測以美元計價。

全球人力資源服務配送平臺市場趨勢與洞察

從傳統人力資源系統遷移到雲端

在人力資源服務傳遞平臺市場,雲端遷移不再只是成本問題,而是關乎業務永續營運的核心。 Strada 於 2025 年 7 月發布的一份報告指出,約 40% 的公司仍在運行過時的本地部署人力資源和企業資源規劃 (ERP) 系統,預算限制和整合複雜性影響了 42% 的轉型計劃。這些發現意義重大,因為延遲遷移的代價如今更加沉重。特別是,隨著 SAP ECC 將於 2025 年 12 月停止支持,Microsoft Dynamics GP 也將於 2029 年停止支持,繼續使用傳統系統環境的組織將面臨更高的安全性和功能風險。美國聯邦政府透過人事管理辦公室 (OPM) 和管理與預算辦公室 (OMB) 宣布的「聯邦人力資源 2.0」計畫進一步強化了這一趨勢。該計畫將於 2026 財政年度啟動,旨在將 100 多個傳統人力資源系統整合到單一的商業平台中。此外,ISG預測,到2027年底,83%的公司將採用SaaS或混合雲端作為其人力資源技術的核心,這意味著人力資源服務配送平臺市場的過渡期正在迅速縮短。因此,能夠縮短實施時間並證明不僅能降低許可成本還能帶來營運效益的供應商,將在整個人力資源服務配送平臺市場中佔據更有利的地位。

對整合式員工自助服務和案例管理的需求日益成長。

人力資源服務配送平臺市場的發展也受到人們對分散的人力資源服務台模式和緩慢的員工支援工作流程的不滿所驅動。麥肯錫2025年的報告指出,歐洲只有19%的核心人力資源流程由生成式人工智慧驅動,另有32%仍處於試點階段,這意味著能夠大規模自動化路由、搜尋和問題解決的平台仍有龐大的市場空間。在服務型組織的設計中也存在類似的需求,其中專門的人力資源共享服務中心並未被充分利用。這意味著許多公司尚未充分認知到將服務交付集中到通用平台上所帶來的效率提升。 UKG在醫療保健行業展示了這種模式的價值。他們的「快速招募」功能實現了高達90%的重複性招募任務的自動化,將招募時間縮短了10天,並將面臨嚴重人才短缺的客戶公司的應徵者到錄用者的轉換率提高了兩倍。因此,人力資源服務配送平臺市場對能夠將員工自助服務、案例管理、知識存取和工作流程自動化整合到單一營運層的平台的需求日益成長。

資料隱私和跨境員工資料管理

關於隱私和跨境資料傳輸的法規仍然是人力資源服務配送平臺市場面臨的最大障礙之一。挑戰不僅限於法律審查,跨國公司還必須將標準合約條款、資料傳輸影響評估和子處理者管治直接整合到其平台營運中。 2026年4月,歐洲資料保護委員會 (EDPB) 批准了“Europrivacy”,將其作為GDPR第42條和第46條下首個基於認證的國際資料傳輸機制,建立了一條新的合規途徑,供應商必須在遵循傳統傳輸框架的同時應對這一挑戰。對採購的影響已經顯現,醫療保健、金融服務和公共部門的採購方越來越傾向於選擇擁有歐盟基礎設施和更強大的本地託管及管理系統的供應商。在德國、法國和比荷盧經濟聯盟等市場,GDPR第28條下的實質審查也促使企業評估那些能夠證明其在整個本地託管和資料處理鏈中具有清晰課責的供應商,這進一步限制了全球標準化平台在人力資源服務交付市場的柔軟性。

細分市場分析

到2025年,軟體將佔人力資源服務配送平臺市場71.21%的佔有率,這意味著經常性授權收入仍然是該領域的核心收入來源。在服務配送平臺產業,買家越來越傾向於選擇整合了核心人力資源、員工服務管理、薪資核算、勞動力管理、人才管理工具、分析和學習功能的套件,而不是一系列獨立的產品。這一趨勢支持一種模式,即持續的AI發布、合規性更新和模組擴充能夠增強長期更新和交叉銷售活動。因此,即使客戶仍在討論應該在單一供應商下實現多少整合,軟體仍然在人力資源服務配送平臺市場佔據主導地位。

サービス部門は、2031年までCAGR12.43%で成長すると予測されており、基盤規模は小さいもの、最も成長の速い構成要素となる見込みです。プラットフォームの範囲が広がり、日常業務に深く組み込まれるにつれて、導入、マネージドサービス、コンプライアンス,アドバイザリーへの需要が高まる傾向にあるため、このことがソフトウェア部門の優位性を損なうことはありません。ベンダーによるサポート、クライアントサクセスプログラム、マネージドサービスは、中小企業(SMB)のHCM導入企業にとって価値実現の中心となりつつあり、これはこの方向性と一致しています。HR服務配送平臺市場において、ソフトウェアの市場規模は依然として大きいもの、運用モデルが複雑化するにつれて、顧客は展開、統合、ポリシーの整合化に関する支援を必要とするため、サービス層の重要性は高まっています。

2025年,基於雲端的人力資源服務傳遞平臺市場佔有率將達到64.90%。這反映了基礎設施成本的降低、功能交付速度的加快以及跨分散式員工隊伍更便捷的政策更新。這一趨勢與人力資源服務傳遞平臺市場向託管環境的廣泛轉變相一致,後者支援分析、自助服務和持續配置變更,且無需本地部署開銷。 Workday於2025年11月發布了“Workday EU Sovereign Cloud”,進一步強化了這一方向。該雲端平台可在歐盟境內提供完整的資料居住,並支援在歐盟境內的營運。這表明,供應商正在雲端模式下解決監管問題,而不是與之保持距離。聯邦政府人事管理辦公室(OPM)和聯邦政府管理與預算辦公室(OMB)也表達了類似的轉變,宣布計劃在2028會計年度之前,根據「聯邦人力資源2.0」計劃,將100多個聯邦傳統系統遷移到商業平台。

ハイブリッド展開は2031年までCAGR11.87%で拡大すると予測されており、一部の雇用主がコンプライアンスや管理のために依然として混合アーキテクチャを必要としていることを示しています。金融サービス、医療、政府機関の購買負責人は、セルフサービスや分析のためにクラウドの俊敏性を求める一方で、特定の給与や人事データについてはローカルで管理された環境に保持したいと考えることがよくあります。この傾向は、HR服務配送平臺市場におけるハイブリッド展開の成長が、クラウドへの躊躇を示すものではなく、データ居住規則や内部のリスクポリシーへの対応であることを意味しています。したがって、HR服務配送平臺業界では引き続き「クラウドファースト」の設計が主流となる一方、法的および運用上の条件により、より細分化された導入選択肢が求められる分野では、ハイブリッドアーキテクチャが拡大していくでしょう。

區域分析

到2025年,北美將佔據人力資源服務配送平臺市場41.71%的佔有率,成為全球最大的區域收入來源。這項需求主要來自美國,美國企業對SaaS的採用率持續高於平均水平,大型企業也持續推動其勞動力管理系統的現代化改造。聯邦政府的「HR 2.0」計畫正是這一趨勢最明確的公開訊號。人事管理辦公室(OPM)和管理與預算辦公室(OMB)共同發起了一項計劃,旨在將100多個政府機構的人力資源系統整合到一個商業化的HCM平台中,預計這項為期10年的合約價值將超過10億美元。在加拿大,由於13個省和地區都面臨合規方面的挑戰,具備自動法規更新和薪資核算等增強功能的平台更具優勢,從而催生了新的市場需求。墨西哥製造業的成長以及對跨境人才管理的需求,尤其是在小時工比例較高的環境中,也為人力資源服務配送平臺市場提供了支援。

欧州は、HR服務配送平臺市場において依然として規制が最も厳しい地域の一つであり、その複雑さも強力な商業性的促進要因となりつつあります。指令(EU)2023/970により、加盟国は2026年6月7日までに「賃金透明性指令」を国内法に組み込むことが義務付けられ、これにより雇用主は職務構造の統一や、報告のためのHRデータと給与データの統合を迫られています。従業員数が250人以上の雇用主は、2026年のデータに基づき、2027年から年次男女賃金格差報告を開始することになり、これによりプラットフォーム導入に向けたシステム準備期間が短縮されました。ドイツ、英國、フランス、オランダは依然として同地域で最大の収益市場ですが、現地でのホスティングやGDPRへの対応が、ベンダー選定においてますます重要な要素となっています。また、ロシアでは、連邦法第242-FZ号によりデータローカリゼーションが中核的な要件として義務付けられているため、世界のクラウド導入モデルの適用範囲が制限されており、同国では依然として制約の多い状況が続いています。

アジア太平洋地域は、2031年までCAGR15.21%で成長すると予測されており、HR服務配送平臺市場において最も成長が著しい地域となる見込みです。この地域の成長は、多国籍企業の事業拡大、中堅企業におけるデジタル化の加速、および一部の使用事例において世界のスイートよりも各国固有の規制への対応に長けた現地ベンダーの台頭によるものです。中国では、Kingdee AI HRやYonyouといったプラットフォームが、現地の労働、税務、社会保険の要件を中心に構築されており、この傾向を如実に示しています。また、インドも、Darwinboxが2025年3月に1億4,000万米ドルを調達し、より広範な国際的な事業拡大の一環として本社をシンガポールに移転したことを受け、重要性を増しています。日本においても、2026年4月にSmartHRの登録企業数が8万社を突破し、労務管理雲端供應商として7年連続で首位を維持したことが、もう一つの明確な徵兆となりました。これは、アジア太平洋地域の人事服務配送平臺市場が、世界の既存企業だけで定義されているわけではないことを示しています。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 從傳統人力資源系統遷移到雲端

- 對整合式員工自助服務和案例管理的需求日益成長。

- 對即時勞動力分析和工作流程自動化的需求

- 透過混合式和分散式工作模式,拓展與數位人才的連結。

- 歐盟的《工資透明度指令》強制要求對工作和工資資料進行標準化。

- 基於技能的人才規劃與內部人才流動

- 市場限制因素

- 資料隱私和員工資料的跨境管理

- 與現有ERP系統和薪資核算系統整合的複雜性。

- 歐盟人工智慧法律及演算法在就業決策中的課責

- 資料主權和區域託管要求

- 宏觀經濟因素對市場的影響

- 產業與價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 軟體

- 核心人員

- 員工服務管理與幫助台

- 薪資/報酬

- 勞動力管理

- 人才管理

- 人力資源分析與報告編制

- 學習與技能發展

- 服務

- 軟體

- 按部署模式

- 基於雲端的

- 現場

- 混合

- 按最終用戶公司規模分類

- 大公司

- 小型企業

- 按最終用戶行業分類

- BFSI

- 醫療保健和生命科學

- 資訊科技/通訊

- 零售與電子商務

- 工業製造

- 政府/公共部門

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 荷蘭

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介。

- Workday, Inc.

- Automatic Data Processing, Inc.

- Ultimate Kronos Group, Inc.

- Dayforce, Inc.

- Paycom Software, Inc.

- Paylocity Holding Corporation

- Paychex, Inc.

- Paycor HCM, Inc.

- Bamboo HR LLC

- Hi Bob Limited

- Personio SE and Co. KG

- Darwinbox Digital Solutions Private Limited

- Rippling People Center Inc.

- Deel Inc.

- Papaya Global Ltd.

- Remote Technology, Inc.

- Zalaris ASA

- Zellis UK Limited

- isolved, Inc.

- ServiceNow, Inc

第7章 市場機會與未來展望

According to Mordor Intelligence, the HR service delivery platform market size is expected to increase from USD 21.27 billion in 2025 to USD 23.45 billion in 2026 and reach USD 38.88 billion by 2031, growing at a CAGR of 10.64% over 2026-2031.

This report is Segmented by Component (Software, and Services), Deployment Model (Cloud-Based, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (BFSI, Healthcare and Life Sciences, Information Technology and Telecom, Retail and E-Commerce, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global HR Service Delivery Platform Market Trends and Insights

Cloud Migration from Legacy Human Resources Stacks

Cloud migration in the HR service delivery platform market has moved beyond a cost discussion and now sits at the center of operating resilience. Strada reported in July 2025 that nearly 40% of businesses still ran aging on-premise HR and ERP systems, and that budget limits and integration complexity each affected 42% of transformation plans. That finding matters because delayed migration now carries a larger penalty, especially after SAP ECC reached end-of-life in December 2025 and Microsoft Dynamics GP moved toward support expiry in 2029, which raises security and capability risk for organizations that stay on older stacks. The U.S. federal government reinforced this direction when OPM and OMB announced Federal HR 2.0, a program that begins in fiscal 2026 and aims to consolidate more than 100 legacy HR systems onto a single commercial platform. ISG also projected that 83% of companies will have SaaS or hybrid cloud at the core of their HR technology by the end of 2027, suggesting that the migration window in the HR service delivery platform market is narrowing quickly. Vendors that can shorten deployment time and show operational gains, not just license savings, are therefore in a stronger position across the HR service delivery platform market.

Rising Demand for Unified Employee Self-Service And Case Management

The HR service delivery platform market is also being pushed by frustration with fragmented HR helpdesk models and slow employee support workflows. McKinsey reported in 2025 that only 19% of core HR processes in Europe had been enhanced with generative AI, while another 32% remained in pilot stages, leaving a large room for platforms that can automate routing, search, and resolution at scale. The same demand is evident in service organization design, where specialized HR shared-services centers remain underused, meaning many companies have not yet captured the efficiency gains from centralizing service delivery on a common platform. UKG showed the value of this model in healthcare, where its Rapid Hire capability automated up to 90% of repetitive hiring tasks, reduced time-to-hire by 10 days, and tripled apply-to-hire conversion rates for customers operating under acute staffing pressure. As a result, the HR service delivery platform market is seeing stronger demand for platforms that combine employee self-service, case management, knowledge access, and workflow automation into a single operating layer.

Data Privacy And Cross-Border Employee Data Controls

Privacy and cross-border transfer rules remain one of the clearest brakes on the HR service delivery platform market. The challenge is no longer limited to legal review because multinational employers now need standard contractual clauses, transfer impact assessments, and sub-processor governance embedded directly into platform operations. The EDPB approved Europrivacy in April 2026 as the first certification-based mechanism for international data transfers under Articles 42 and 46 of the GDPR, creating a new compliance path that vendors must support alongside older transfer frameworks. Procurement effects are already visible because buyers in healthcare, financial services, and the public sector increasingly favor vendors with EU-based infrastructure and stronger local residency controls. In markets such as Germany, France, and the Benelux, due diligence under GDPR Article 28 is also pushing evaluations toward vendors that can demonstrate local hosting and clearer accountability across data-handling chains, narrowing the flexibility of globally standardized platforms in the HR service delivery market.

Other drivers and restraints analyzed in the detailed report include:

- Need For Real-Time Workforce Analytics And Workflow Automation

- Hybrid And Distributed Work Models Expanding Digital Human Resources Touchpoints

- Integration Complexity with Legacy Enterprise Resource Planning and Payroll Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 71.21% of the HR service delivery platform market in 2025, which shows that recurring licenses remain the core commercial engine for the category. In the HR service delivery platform industry, buyers increasingly want core HR, employee service management, payroll, workforce management, talent tools, analytics, and learning, all connected within one suite rather than stitched together as separate products. That preference supports a model where continuous AI releases, compliance updates, and module expansion reinforce renewal and cross-sell activity over time. The result is that software continues to dominate the HR service delivery platform market, even as customers debate how far they should consolidate under a single vendor.

Services are projected to grow at a 12.43% CAGR through 2031, making it the faster-growing component, even though it starts from a smaller base. This does not weaken the software case because implementation, managed services, and compliance advisory demand tend to rise as platforms become broader and more embedded in daily operations. Vendor support, client success programs, and managed services are becoming central to value realization for SMB HCM buyers, which aligns with this direction. The HR service delivery platform market size for software remains larger, but the services layer is becoming more durable because customers need help with rollout, integration, and policy alignment as the operating model grows more complex.

Cloud-based deployment accounted for 64.90% of the HR service delivery platform market in 2025, reflecting lower infrastructure costs, faster feature delivery, and easier policy updates across distributed workforces. That position aligns with the wider shift in the HR service delivery platform market toward hosted environments that support analytics, self-service, and continuous configuration change without on-premises overhead. Workday reinforced this direction in November 2025 when it launched Workday EU Sovereign Cloud with full EU data residency and EU-based operations, showing that vendors are addressing regulatory concerns inside the cloud model rather than stepping away from it. OPM and OMB also signaled the same transition when Federal HR 2.0 set out to move more than 100 legacy federal systems onto a commercial platform by fiscal 2028.

Hybrid deployment is forecast to grow at a 11.87% CAGR through 2031, indicating that some employers still need a mixed architecture for compliance and control. Financial services, healthcare, and government buyers often want cloud agility for self-service and analytics while keeping selected payroll or personnel data in locally controlled environments. That pattern means hybrid growth in the HR service delivery platform market is not a sign of cloud hesitation, but a response to residency rules and internal risk policy. The HR service delivery platform industry, therefore, continues to favor cloud-first design, while hybrid architecture expands where legal and operating conditions require more segmented deployment choices.

Complete Report Scope:

- By Component

- Software

- Core Human Resources

- Employee Service Management and Helpdesk

- Payroll and Compensation

- Workforce Management

- Talent Management

- People Analytics and Reporting

- Learning and Development

- Services

- Software

- By Deployment Model

- Cloud-Based

- On-Premises

- Hybrid

- By End User Enterprise Size

- Large Enterprises

- Small and Medium-Sized Enterprises

- By End-user Industry

- BFSI

- Healthcare and Life Sciences

- Information Technology and Telecom

- Retail and E-commerce

- Industrial Manufacturing

- Government and Public Sector

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Netherlands

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America held 41.71% of the HR service delivery platform market share in 2025, which made it the leading regional revenue base. The United States accounted for most of that demand because enterprise SaaS adoption remained above global averages and large employers continued to modernize workforce systems at scale. Federal HR 2.0 became the clearest public signal of this trend when OPM and OMB set out to consolidate more than 100 agency HR systems onto a single commercial HCM platform, with a 10-year contract expected to exceed USD 1 billion. Canada introduces a new source of demand, as 13 provinces and territories create a multi-jurisdictional compliance burden that favors platforms with automated legislative updates and stronger payroll alignment. Mexico also supports the HR service delivery platform market through manufacturing growth and cross-border workforce administration needs, especially in high-volume hourly labor settings.

Europe remains one of the most regulation-heavy parts of the HR service delivery platform market, and that complexity is also becoming a strong commercial driver. Directive (EU) 2023/970 required member states to transpose the Pay Transparency Directive by June 7, 2026, which pushed employers to harmonize job structures and combine HR and payroll data for reporting. Employers with 250 or more workers will begin annual gender pay gap reporting in 2027 based on 2026 data, which tightened the system-readiness window for platform deployment. Germany, the United Kingdom, France, and the Netherlands remain the largest revenue markets in the region, while local hosting and GDPR readiness increasingly shape vendor selection. Russia also maintains a more restricted profile because Federal Law No. 242-FZ mandates data localization as a core requirement, limiting the scope for global cloud deployment models.

Asia-Pacific is projected to grow at a 15.21% CAGR through 2031, making it the fastest-growing geography in the HR service delivery platform market. Growth in this region comes from multinational expansion, faster digitization among mid-sized employers, and the rise of local vendors that handle country-specific rules better than global suites in some use cases. China illustrates that pattern through platforms such as Kingdee AI HR and Yonyou, which are built around local labor, tax, and social insurance requirements. India has also become more important after Darwinbox raised USD 140 million in March 2025 and shifted its headquarters to Singapore as part of a broader international scale-up. Japan added another clear signal in April 2026 when SmartHR passed 80,000 registered companies and secured its seventh consecutive year as the leading labor-management cloud vendor, which shows that the HR service delivery platform market in Asia-Pacific is not defined by global incumbents alone.

- Workday, Inc.

- Automatic Data Processing, Inc.

- Ultimate Kronos Group, Inc.

- Dayforce, Inc.

- Paycom Software, Inc.

- Paylocity Holding Corporation

- Paychex, Inc.

- Paycor HCM, Inc.

- Bamboo HR LLC

- Hi Bob Limited

- Personio SE and Co. KG

- Darwinbox Digital Solutions Private Limited

- Rippling People Center Inc.

- Deel Inc.

- Papaya Global Ltd.

- Remote Technology, Inc.

- Zalaris ASA

- Zellis UK Limited

- isolved, Inc.

- ServiceNow, Inc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud Migration From Legacy Human Resources Stacks

- 4.2.2 Rising Demand For Unified Employee Self-Service and Case Management

- 4.2.3 Need For Real-Time Workforce Analytics and Workflow Automation

- 4.2.4 Hybrid and Distributed Work Models Expanding Digital Human Resources Touchpoints

- 4.2.5 European Union Pay Transparency Directive Forcing Harmonized Job and Pay Data

- 4.2.6 Skills-Based Workforce Planning and Internal Talent Mobility

- 4.3 Market Restraints

- 4.3.1 Data Privacy and Cross-Border Employee Data Controls

- 4.3.2 Integration Complexity With Legacy Enterprise Resource Planning and Payroll Systems

- 4.3.3 European Union Artificial Intelligence Act and Algorithmic Accountability For Employment Decisions

- 4.3.4 Data Sovereignty and Regional Hosting Requirements

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry-Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Comptetive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.1.1 Core Human Resources

- 5.1.1.2 Employee Service Management and Helpdesk

- 5.1.1.3 Payroll and Compensation

- 5.1.1.4 Workforce Management

- 5.1.1.5 Talent Management

- 5.1.1.6 People Analytics and Reporting

- 5.1.1.7 Learning and Development

- 5.1.2 Services

- 5.1.1 Software

- 5.2 By Deployment Model

- 5.2.1 Cloud-Based

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By End User Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-Sized Enterprises

- 5.4 By End-user Industry

- 5.4.1 BFSI

- 5.4.2 Healthcare and Life Sciences

- 5.4.3 Information Technology and Telecom

- 5.4.4 Retail and E-commerce

- 5.4.5 Industrial Manufacturing

- 5.4.6 Government and Public Sector

- 5.4.7 Other End-user Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Netherlands

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 Workday, Inc.

- 6.4.2 Automatic Data Processing, Inc.

- 6.4.3 Ultimate Kronos Group, Inc.

- 6.4.4 Dayforce, Inc.

- 6.4.5 Paycom Software, Inc.

- 6.4.6 Paylocity Holding Corporation

- 6.4.7 Paychex, Inc.

- 6.4.8 Paycor HCM, Inc.

- 6.4.9 Bamboo HR LLC

- 6.4.10 Hi Bob Limited

- 6.4.11 Personio SE and Co. KG

- 6.4.12 Darwinbox Digital Solutions Private Limited

- 6.4.13 Rippling People Center Inc.

- 6.4.14 Deel Inc.

- 6.4.15 Papaya Global Ltd.

- 6.4.16 Remote Technology, Inc.

- 6.4.17 Zalaris ASA

- 6.4.18 Zellis UK Limited

- 6.4.19 isolved, Inc.

- 6.4.20 ServiceNow, Inc

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

全球末端配送自動化市場預測(至2034年):按組件、技術、配送方式、應用、最終用戶和地區分類的分析

全球末端配送自動化市場預測(至2034年):按組件、技術、配送方式、應用、最終用戶和地區分類的分析 北美人力資源服務配送平臺:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

北美人力資源服務配送平臺:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年) 2026年全球服務交付自動化市場報告

2026年全球服務交付自動化市場報告 服務提供自動化市場:按組件、產業、部署類型和組織規模分類 - 2026-2032 年全球預測

服務提供自動化市場:按組件、產業、部署類型和組織規模分類 - 2026-2032 年全球預測 全球服務提供自動化市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球服務提供自動化市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 服務提供自動化市場規模、佔有率和成長分析(按組件、類型、使用者類型、垂直產業和地區分類)-2026-2033年產業預測服務提供自動化市場預測至 2032 年:按類型、產品、組件、部署模式、應用、最終用戶和地區分類的全球分析服務提供平台:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)服務提供自動化:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)

服務提供自動化市場規模、佔有率和成長分析(按組件、類型、使用者類型、垂直產業和地區分類)-2026-2033年產業預測服務提供自動化市場預測至 2032 年:按類型、產品、組件、部署模式、應用、最終用戶和地區分類的全球分析服務提供平台:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)服務提供自動化:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)