|

市場調查報告書

商品編碼

1851776

服務提供平台:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)Service Delivery Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

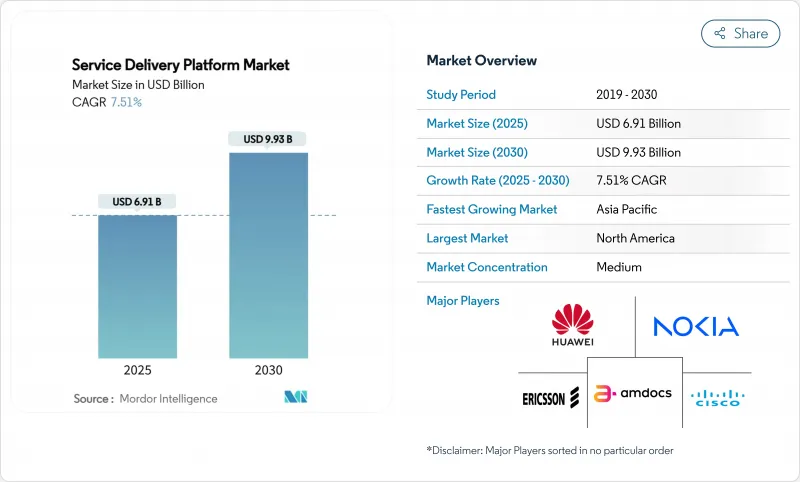

預計到 2025 年,服務提供平台市場規模將達到 69.1 億美元,到 2030 年將達到 93.3 億美元,在此期間的複合年成長率為 7.51%。

獨立部署的5G網路、雲端原生轉型策略以及對傳統OSS/BSS堆疊的迫切替換,共同推動資本流向平台現代化。通訊業者正投資於微服務架構,以縮短發布週期、實現網路切片,並實現低延遲企業用例的商業化。工業園區私有5G的普及以及消費者對高度個人化提案日益成長的需求,進一步提升了軟體定義的敏捷性。隨著超大規模雲端供應商、傳統網路供應商和利基軟體專家齊聚同一市場,競爭日益激烈,迫使各方尋求整合、夥伴關係和開放API策略。

全球服務傳遞平臺市場趨勢與洞察

5G部署推動彈性的服務編配

為了建構一體化的 5G 網路,營運商必須採用編配層,以毫秒速度分配網路資源,並透過開放 API 公開各項功能。愛立信估計,光是網路切片就能釋放 2,000 億美元的新價值,這也解釋了為什麼新加坡電信 (SingTel) 於 2024 年將面向消費者的網路切片商業化,以建構其高階 5G+ 服務。隨著營運商將工作負載遷移到雲端原生核心網,2025 年第一季全球行動核心網支出年增 32%。基於服務的架構天生適合微服務,平台供應商正在整合策略引擎,以實現延遲、頻寬和安全保障的貨幣化。因此,服務傳遞平臺市場正在滿足對基於意圖的編配的需求,這種編排方式將 5G 無線資源與企業服務等級協定 (SLA) 連結起來。隨著醫療、物流和媒體等產業運作更多網路切片,商機將會增加,平台擴充性將成為競爭優勢。

通訊業者向雲端原生轉型

超大規模聯盟正在重塑通訊業者的IT發展藍圖。沃達豐與微軟達成了一項為期10年、價值15億美元的協議,覆蓋歐洲和非洲的3億用戶,該協議正在將工作負載遷移到Azure雲端平台,並引入DevOps實踐,將發布週期從數月縮短至數週。德國電信(Telefónica Germany)在不中斷服務的情況下,將4,500萬用戶遷移到雲端原生5G核心網,證明了容器化網路功能的成熟度。持續整合和自動化測試現在支援快速啟用新功能,而動態資源擴充則有助於控制成本。供應商正在透過SaaS交付模式和計量收費許可來回應,從而擴大可觸及的服務傳遞平臺市場。從長遠來看,雲端優先策略有望使通訊業者減少對專有硬體的依賴,並以更大的敏捷性推出跨產業的提案。

現代化改造傳統OSS/BSS系統需要高額資本支出。

替換大型主機時代的技術堆疊所需的前期投資,阻礙了許多中型和新興市場通訊業者全面推進數位化。斯里蘭卡Airtel的轉型使營運IT成本降低了80%,但也需要持續的資本注入和專家諮詢支援。規模較小的通訊業者通常依賴疊加方案,這種方案保留了核心系統孤島,限制了短期平台收入。雲端訂閱模式可以緩解資產負債表壓力,但整合複雜性仍會對專業服務預算產生重大影響。因此,短期內採用率可能會趨於平緩,預計將使整體服務傳遞平臺市場的複合年成長率下降1.2個百分點。

細分市場分析

服務傳遞平臺市場的軟體收入正以11.7%的複合年成長率成長,成長超過整體市場成長速度,這主要得益於營運商從專有設備轉向以API為中心的編配套件。到2024年,服務收入仍將佔總收入的60.3%,反映出市場對整合、遷移和託管營運的持續需求。供應商正投入大量研發資源(光是華為一家公司在2024年的研發投入就將達到248億美元),以縮短服務創新週期,包括人工智慧、分析和低程式碼工具等領域。

平台軟體抽象化了網路複雜性,並支援可組合的微服務,從而加快了合作夥伴的入駐速度。像 Nexign 框架這樣的計劃已將整合時間從三個月縮短至四周,使 MegaFon 能夠快速部署超過 170 項服務。專業服務對於傳統系統切換階段和 DevOps 實施至關重要。總而言之,軟體的成長可能會穩定提升服務交付平台的市場佔有率,最終超越模組化、基於授權的產品。

2024年,雲端部署將佔全球營收的63.1%,年複合成長率達14.2%,通訊業者降低資本投入風險並追求彈性擴展。 T-Mobile遷移到AWS以降低硬體開銷並提高運作,正是預付優先趨勢的體現。

在金融服務和公共部門,混合架構正在興起,因為這些領域的資料駐留法規要求必須部署本地控制平面。供應商套件現在支援自動化 CI/CD 管線和零接觸網路功能升級,進一步推動了雲端技術的普及。因此,預計到 2030 年,由雲端採用驅動的服務提供平台市場規模將超過 50 億美元。

區域分析

2024年,北美將佔全球營收的31.6%,這主要得益於積極的5G部署計畫、頻譜政策以及深厚的雲端技術專長。諸如Verizon以200億美元收購Frontier以及Charter以345億美元收購Cox等大型併購案,將擴大光纖網路覆蓋範圍,並促進端對端平台整合。 T-Mobile與KKR合資收購MetroNet,將加速其固定無線提案。監管機構對供應鏈安全和海底電纜監管的關注,催生了合規諮詢需求,並正在重塑該地區的供應商服務組合。

亞太地區預計將以14.1%的複合年成長率實現最快成長,通訊業者正將重心轉向非網路連線收入,該收入在2024年上半年已佔總收入的19.9%。中國移動和中國聯通正利用其在雲端運算、視訊和工業數位服務領域的規模優勢。星和的「雲端無限」(Cloud Infinity)計畫利用AWS、Google雲端和諾基亞的多重雲端編配,為企業工作負載提供低於10毫秒的延遲,展現了其架構創新。各國數位經濟政策為私有5G和智慧製造的部署提供了獎勵,進一步增強了該地區的成長動能。

歐洲是一個成熟且監管完善的環境,歐盟人工智慧法律和資料主權指令對架構選擇產生影響。沃達豐與Azure的夥伴關係體現了其對跨多個國家市場雲端原生轉型的長期資本投入。英國的《電信安全法》要求一級營運商實施258項網路安全控制措施,加速了平台升級。南美和中東及非洲地區的基準較低,但行動網路普及率的提高和政府數位化計畫表明,未來對敏捷服務交付框架的需求將十分強勁。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 市場定義與研究假設

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 5G部署推動彈性的服務編配

- 通訊業者向雲端原生轉型

- 數位業務支援系統及對高度個人化服務的需求

- 物聯網的普及需要可擴展的服務管理

- 採用微服務和容器化

- 網路切片與私有 5G 貨幣化

- 市場限制

- 現代化改造傳統OSS/BSS系統需要高額資本支出。

- 網路安全和資料隱私問題

- 雲端SDP生態系統中的供應商鎖定問題

- DevOps/雲端原生人才短缺

- 價值鏈分析

- 關鍵法規結構評估

- 關鍵相關人員影響評估

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 宏觀經濟因素的影響

第5章 市場規模與成長預測

- 按類型

- 軟體

- 服務

- 透過部署模式

- 本地部署

- 雲

- 透過使用

- 通訊業者

- BFSI

- 媒體與娛樂

- 衛生保健

- 零售與電子商務

- 政府和公共部門

- 其他

- 依網路類型

- 無線的

- 有線

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Huawei Technologies Co., Ltd.

- HCL Technologies Limited

- Fujitsu Limited

- Accenture plc

- Telenity, Inc.

- Nokia Corporation

- Ericsson AB

- Cisco Systems, Inc.

- Amdocs Limited

- Oracle Corporation

- ZTE Corporation

- Hewlett Packard Enterprise Company

- Tata Consultancy Services Limited

- NEC Corporation

- IBM Corporation

- CSG Systems International, Inc.

- Comarch SA

- Tech Mahindra Limited

- Openet(Amdocs)

- Qvantel Oy

第7章 市場機會與未來趨勢

- 閒置頻段與未滿足需求評估

The service delivery platform market size stood at USD 6.91 billion in 2025 and is forecast to advance to USD 9.33 billion by 2030, reflecting a 7.51% CAGR over the period.

5G standalone deployments, cloud-native transformation strategies and the urgent replacement of legacy OSS/BSS stacks combine to pull capital toward platform modernization. Operators are investing in microservices architectures that shorten release cycles, enable network slicing, and monetize low-latency enterprise use cases. Software-defined agility is further amplified by private-5G adoption in industrial campuses and by rising demand for hyper-personalized consumer propositions. Competitive intensity is rising as hyperscale cloud providers, traditional network vendors and niche software specialists converge on the same opportunity set, forcing consolidation, partnerships and open-API strategies.

Global Service Delivery Platform Market Trends and Insights

5G Roll-outs Driving Flexible Service Orchestration

Standalone 5G build-outs obligate operators to adopt orchestration layers that allocate network resources in milliseconds and expose capabilities through open APIs. Ericsson estimates network slicing alone can unlock USD 200 billion in new value, underscoring why Singtel commercialised consumer slicing in 2024 to create premium 5G+ tiers . Global mobile core spending jumped 32% year-over-year in Q1 2025 as carriers moved workloads onto cloud-native cores. Service-based architecture inherently suits microservices, and platform vendors are embedding policy engines that monetise latency, bandwidth and security guarantees. The service delivery platform market therefore captures demand for intent-based orchestration that links 5G radio resources to enterprise SLAs. As more slices go live in healthcare, logistics and media, revenue opportunities will multiply and platform scalability will become a competitive determinant.

Cloud-native Transformation Among Telecom Operators

Hyperscale alliances are recasting telco IT roadmaps. Vodafone's decade-long USD 1.5 billion pact with Microsoft targets 300 million subscribers across Europe and Africa, shifting workloads to Azure and embedding DevOps practices that shrink release cycles from months to weeks. Telefonica Germany migrated 45 million users to a cloud-native 5G core without service disruption, evidencing maturity of containerised network functions. Continuous integration and automated testing now underpin rapid feature activation, while dynamic resource scaling improves cost discipline. Vendors are responding with SaaS delivery models and pay-as-you-grow licensing, expanding the addressable service delivery platform market. Over the long term, cloud-first strategies will make telcos less dependent on proprietary hardware and more agile in launching cross-vertical propositions.

High CAPEX to Modernise Legacy OSS/BSS

The upfront investment to replace mainframe-era stacks deters many mid-tier and emerging-market operators from full-scale digitalisation. Airtel Sri Lanka's transformation trimmed operating IT spend by 80% but required phased capital injections and specialist consulting support . Smaller carriers often resort to overlay approaches that leave core silos intact, tempering immediate platform revenues. While cloud subscription models soften balance-sheet pressure, integration complexity still commands sizeable professional services budgets. As a result, near-term adoption curves can flatten, moderating the overall service delivery platform market CAGR by an estimated -1.2 percentage points.

Other drivers and restraints analyzed in the detailed report include:

- Demand for Digital BSS and Hyper-personalised Services

- IoT Proliferation Requiring Scalable Service Management

- Cyber-security and Data-privacy Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software revenue in the service delivery platform market is climbing at an 11.7% CAGR, eclipsing the headline growth rate as operators migrate from proprietary appliances to API-centric orchestration suites. Services still generated 60.3% of 2024 turnover, reflecting ongoing demand for integration, migration, and managed operations. Vendors allocate substantial R&D-Huawei alone spent USD 24.8 billion in 2024-toward AI, analytics, and low-code tooling that compress service innovation timelines.

Platform software enables composable microservices that abstract network complexity and promote partner onboarding. Projects such as Nexign's framework cut integration windows from three months to barely four weeks, allowing MegaFon to roll out 170-plus offers swiftly . Professional services remain indispensable during legacy cut-over phases and DevOps enablement. Taken together, software gains will steadily lift the service delivery platform market share of modular, license-based products.

Cloud implementations contributed 63.1% of global revenue in 2024 and are increasing at a 14.2% CAGR as carriers de-risk capital commitments and pursue elastic scaling. The cloud-first trajectory is evidenced by T-Mobile migrating its prepaid BSS onto AWS to cut hardware overhead and improve uptime.

Hybrid blueprints are emerging in financial services and public-sector contexts where data residency rules mandate on-premise control planes. Vendor toolkits now automate CI/CD pipelines and provide zero-touch network function upgrades, further tilting preference toward cloud. Consequently, the service delivery platform market size attributed to cloud deployments is expected to eclipse USD 5 billion before 2030.

The Service Delivery Platform Market Report is Segmented by Type (Software, Services), Deployment Mode (On-Premise, Cloud), Application (Telecom Operators, BFSI, Media and Entertainment, Healthcare, Retail and E-Commerce, Government and Public Sector, Others), Network Type (Wireless, Wireline), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 31.6% of revenue in 2024, buoyed by aggressive 5G roll-out timetables, supportive spectrum policy and deep cloud expertise. Large-scale mergers such as Verizon's USD 20 billion Frontier acquisition and Charter's USD 34.5 billion Cox purchase expand fibre footprints and stimulate end-to-end platform consolidation. T-Mobile's joint venture with KKR to gain Metronet accelerates integrated fixed-wireless propositions. Regulatory focus on supply-chain security and submarine cable oversight creates parallel compliance consulting demand, shaping vendor service portfolios in the region.

Asia-Pacific is forecast to generate a 14.1% CAGR, the fastest worldwide, as operators pivot toward beyond-connectivity revenue that already formed 19.9% of H1-2024 takings. China Mobile and China Unicom channel scale advantages into cloud, video and industrial digital services. StarHub's Cloud Infinity programme leverages multi-cloud orchestration with AWS, Google Cloud and Nokia to deliver sub-10 millisecond latency for enterprise workloads, illustrating architectural innovation. National digital-economy policies funnel incentives toward private 5G and smart-manufacturing roll-outs, reinforcing regional momentum.

Europe represents a mature, regulation-heavy environment where the EU's AI Act and data-sovereignty mandates influence architectural choices. Vodafone's Azure partnership exemplifies long-term capital commitment to cloud-native transformation across several national markets. The UK Telecoms Security Act compels tier-1 operators to implement 258 cybersecurity controls, prompting accelerated platform upgrades. Although South America and the Middle East and Africa start from lower baselines, rising mobile penetration and government digitalisation agendas signal vibrant future demand for agile service delivery frameworks.

- Huawei Technologies Co., Ltd.

- HCL Technologies Limited

- Fujitsu Limited

- Accenture plc

- Telenity, Inc.

- Nokia Corporation

- Ericsson AB

- Cisco Systems, Inc.

- Amdocs Limited

- Oracle Corporation

- ZTE Corporation

- Hewlett Packard Enterprise Company

- Tata Consultancy Services Limited

- NEC Corporation

- IBM Corporation

- CSG Systems International, Inc.

- Comarch SA

- Tech Mahindra Limited

- Openet (Amdocs)

- Qvantel Oy

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Market Definition and Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 5G roll-outs driving flexible service orchestration

- 4.2.2 Cloud-native transformation among telecom operators

- 4.2.3 Demand for digital BSS and hyper-personalised services

- 4.2.4 IoT proliferation requiring scalable service management

- 4.2.5 Micro-services and containerisation adoption

- 4.2.6 Network slicing and private-5G monetisation

- 4.3 Market Restraints

- 4.3.1 High CAPEX to modernise legacy OSS/BSS

- 4.3.2 Cyber-security and data-privacy concerns

- 4.3.3 Vendor lock-in in cloud-SDP ecosystems

- 4.3.4 Shortage of DevOps / cloud-native talent

- 4.4 Value Chain Analysis

- 4.5 Evaluation of Critical Regulatory Framework

- 4.6 Impact Assessment of Key Stakeholders

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Impact of Macro-economic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 On-Premise

- 5.2.2 Cloud

- 5.3 By Application

- 5.3.1 Telecom Operators

- 5.3.2 BFSI

- 5.3.3 Media and Entertainment

- 5.3.4 Healthcare

- 5.3.5 Retail and E-commerce

- 5.3.6 Government and Public Sector

- 5.3.7 Others

- 5.4 By Network Type

- 5.4.1 Wireless

- 5.4.2 Wireline

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Huawei Technologies Co., Ltd.

- 6.4.2 HCL Technologies Limited

- 6.4.3 Fujitsu Limited

- 6.4.4 Accenture plc

- 6.4.5 Telenity, Inc.

- 6.4.6 Nokia Corporation

- 6.4.7 Ericsson AB

- 6.4.8 Cisco Systems, Inc.

- 6.4.9 Amdocs Limited

- 6.4.10 Oracle Corporation

- 6.4.11 ZTE Corporation

- 6.4.12 Hewlett Packard Enterprise Company

- 6.4.13 Tata Consultancy Services Limited

- 6.4.14 NEC Corporation

- 6.4.15 IBM Corporation

- 6.4.16 CSG Systems International, Inc.

- 6.4.17 Comarch SA

- 6.4.18 Tech Mahindra Limited

- 6.4.19 Openet (Amdocs)

- 6.4.20 Qvantel Oy

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-space and Unmet-need Assessment

全球末端配送自動化市場預測(至2034年):按組件、技術、配送方式、應用、最終用戶和地區分類的分析

全球末端配送自動化市場預測(至2034年):按組件、技術、配送方式、應用、最終用戶和地區分類的分析 人力資源服務配送平臺:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)北美人力資源服務配送平臺:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

人力資源服務配送平臺:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)北美人力資源服務配送平臺:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年) 2026年全球服務交付自動化市場報告

2026年全球服務交付自動化市場報告 服務提供自動化市場:按組件、產業、部署類型和組織規模分類 - 2026-2032 年全球預測

服務提供自動化市場:按組件、產業、部署類型和組織規模分類 - 2026-2032 年全球預測 全球服務提供自動化市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球服務提供自動化市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 服務提供自動化市場規模、佔有率和成長分析(按組件、類型、使用者類型、垂直產業和地區分類)-2026-2033年產業預測服務提供自動化市場預測至 2032 年:按類型、產品、組件、部署模式、應用、最終用戶和地區分類的全球分析服務提供自動化:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)

服務提供自動化市場規模、佔有率和成長分析(按組件、類型、使用者類型、垂直產業和地區分類)-2026-2033年產業預測服務提供自動化市場預測至 2032 年:按類型、產品、組件、部署模式、應用、最終用戶和地區分類的全球分析服務提供自動化:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)