|

市場調查報告書

商品編碼

2072612

印度卡車市場:市場佔有率分析、產業趨勢與統計及成長預測(2025-2030 年)India Truck - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

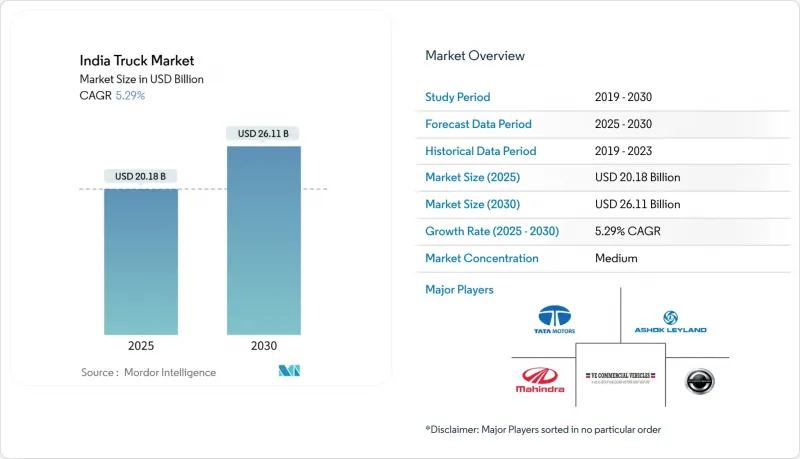

根據 Mordor Intelligence 預測,印度卡車市場規模預計將在 2025 年達到 201.8 億美元,到 2030 年達到 261.1 億美元,複合年成長率為 5.29%。

本報告按車輛類型(小型、中型及其他)、負載容量(3.5-7.5噸、7.5-16噸及其他)、燃料類型(柴油、汽油及其他)、應用領域(物流、建築及其他)、所有權類型(車隊運營商和個體車主)以及車身類型(平板車、廂式貨車及其他)進行分類類型。市場預測以貨幣價值(美元)和銷售(輛)兩種形式呈現。

印度卡車市場趨勢與洞察

政府推動基礎建設發展(Bharatmala、Gati Shakti)

2024會計年度,印度國家公路管理局(NHAI)投入大量資金2.07兆印度盧比(約247.9億美元)用於公路建設,創下歷史新高。這筆資本支出較上一會計年度成長20%,是歷史最高水準。在2025-2026財政年度聯邦預算中,政府向公路運輸和公路部累計2.87333兆印度盧比(約330.7億美元),較2025會計年度撥款略微增加2.41%。到2025年,將建成19,201公里的經濟走廊,自動卸貨卡車和牽引車的運轉率已開始提高。新的軸荷標準適用於更大的車隊,並指南原始設備製造商(OEM)的底盤設計。印度卡車市場正在積極回應,推出更重的規格,以最佳化水泥、鋼鐵和煤炭等散裝貨物的運輸。即使僅以德里-孟買路線為例,貨物密度也在增加,從而支持持續的運作週期,改善卡車的總擁有成本。

電子商務主導的物流繁榮

受小包裹遞送量激增的推動,印度物流業正經歷快速轉型,這也持續刺激印度卡車運輸市場的需求。領先的電子商務企業正在擴展其配送網路和基礎設施,以滿足消費者對更快服務日益成長的期望。隨著物流業務深入中小城市,貨運路線正被重新規劃為新的消費中心,這增加了對更靈活、更適合城市環境的小型車輛的需求。遠端資訊處理技術的進步正在提高路線效率和車輛生產力,使卡車運輸生態系統能夠更快地響應並最佳化不斷變化的市場動態。

對符合BS-VI排放標準的卡車進行資本投資

自2025年10月起,強制執行BS-VI排放標準並引入空調駕駛室將使每輛車增加2萬至3萬印度盧比(約合250至375美元)的成本,使2026會計年度行業總資本支出達到600億印度盧比(約合7.5億美元)。目前仍佔車隊70%的小規模企業難以應對每月還款額(EMI)的增加,這導致車輛更換速度放緩,並抑制了印度卡車市場的短期需求。

細分市場分析

輕型卡車在2024年佔印度卡車總出貨量的48.33%,是印度卡車市場的支柱,預計到2030年將維持6.94%的複合年成長率。由於都市區道路法規和電商配送時限的限制,能夠在人口密集的城市地區行駛的緊湊型軸距車輛更受歡迎。 OEM融資方案和電動車動力系統的低維護成本進一步推動了此類卡車的需求。中型卡車主要負責區域間的快速運輸,而重型牽引車則在水泥、鋼鐵和煤炭運輸路線上佔據主導地位。輕型卡車的電氣化,以及繞過公共電網限制的專用充電樁,使得200公里都市區路線的投資能夠快速收回。

像Magenta Mobility的3噸級電動卡車這樣的第二代車型,現在每天可以完成三個往返行程,資產利用率加倍,成本曲線也隨之改變。同時,由於三線貿易叢集對噸英里數的需求不斷成長,內燃機卡車仍有市場需求,這個細分市場仍然是印度卡車市場的重要成長引擎。

2024年,3.5至7.5噸級卡車的銷售量佔比將達39.18%。這反映了印度零售網路的碎片化特點,在這種模式下,負載容量的柔軟性比單純的貨物能力更為重要。隨著全通路零售商推動微型倉庫快速補貨,預計該級別卡車的複合年成長率將達到7.14%,超過所有其他負載容量等級。嚴格的市政軸距法規和較低的橋樑淨空高度進一步提升了小噸位卡車的效用。

隨著高速公路建設的不斷推進,樞紐間貨運線路可能會逐步轉向總噸位16噸以上的車輛,但由於送貨上門的需求,7.5噸以下車輛的需求預計仍將保持強勁。從戰略角度來看,汽車製造商正透過採用模組化車身套件來擴大印度卡車市場,以提高平台經濟性並實現產品種類多樣化,而無需經歷新的車型認證流程。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 政府推動基礎建設發展(Bharatmala、Gati Shakti)

- 電子商務主導的物流繁榮

- 車輛報廢政策帶來的更換需求

- 基於總擁有成本效益向 CNG/LNG 過渡

- 二、三線城市低溫運輸的擴展

- 互聯軌道遠端資訊處理系統的實施

- 市場限制因素

- 增加對符合BS-VI排放標準的卡車的資本投資

- 柴油價格波動

- 駕駛人和勞動力老化

- 大型車輛的充電網路不足。

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 按車輛類型

- 小型

- 中號

- 大的

- 按負載容量

- 3.5至7.5噸

- 7.5至16噸

- 16-30噸

- 超過30噸

- 按燃料類型

- 柴油引擎

- 汽油

- 電的

- 其他

- 透過使用

- 後勤

- 建造

- 農業

- 礦業

- 公用事業

- 其他

- 依所有權類型

- 車隊營運商

- 個人所有者

- 按車輛類型

- 平板

- 廂型車

- 冷藏

- 油船

- 翻斗車

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Tata Motors Limited

- Ashok Leyland

- Mahindra & Mahindra Limited

- VE Commercial Vehicles Ltd.(Eicher)

- BharatBenz(Daimler India Commercial Vehicles)

- Volvo Trucks India

- Scania Commercial Vehicles India Pvt. Ltd.

- Force Motors Limited

- Isuzu Motors India Private Limited

- Hino Motors India

- Olectra Greentech

- BYD India

- Omega Seiki Mobility

- Tresa Motors

第7章 市場機會與未來展望

According to Mordor Intelligence, the indian truck market size stood at USD 20.18 billion in 2025 and is forecast to reach USD 26.11 billion by 2030, reflecting a 5.29% CAGR.

This report is Segmented by Vehicle Type (Light Duty, Medium Duty, and More), Tonnage Capacity (3. 5-7. 5 Tons, 7. 5-16 Tons, and More), Fuel Type (Diesel, Petrol, and More), Application (Logistics, Construction, and More), Ownership (Fleet Operators and Individual Owners), Body Type (Flatbed, Box Truck, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

India Truck Market Trends and Insights

Government Infrastructure Push (Bharatmala, Gati Shakti)

In FY24, the National Highways Authority of India (NHAI) set a new benchmark by investing a staggering Rs. 2,07,000 crore (USD 24.79 billion) in national highway construction. This capital outlay marked a record high, surging 20% from the previous fiscal year. For the Union Budget 2025-26, the government earmarked Rs. 2,87,333.3 crore (USD 33.07 billion) for the Ministry of Road Transport and Highways, a modest 2.41% increase from FY25's allocations. Completing 19,201 km of economic corridors by 2025 already lifts tipper and tractor-trailer utilization. New axle-load norms align with higher-capacity fleets, guiding OEM chassis design. The Indian truck market responds with heavier configurations optimized for bulk cement, steel, and coal haulage. Rising freight density on the Delhi-Mumbai route alone supports continuous-duty cycles that improve truck total cost of ownership.

E-commerce-Led Logistics Boom

India's logistics sector is experiencing a rapid transformation, driven by a sharp rise in parcel deliveries, fueling continuous demand for trucking services in the India truck market. Leading e-commerce companies are expanding their delivery networks and infrastructure to meet growing consumer expectations for faster service. As logistics operations extend deeper into smaller cities, freight routes are reoriented toward new consumption hubs, increasing the need for agile, light-duty vehicles suited for urban environments. Technological advancements in telematics enhance route efficiency and vehicle productivity, making the trucking ecosystem more responsive and optimized for evolving market dynamics.

High BS-VI Truck Capex

Mandatory BS-VI upgrades and AC cabs add INR 20,000-30,000 (USD 250-375) per unit from October 2025, elevating industry capex to INR 60 billion (USD 750 million) in FY26 . Small operators, still 70% of ownership, struggle with higher EMIs, delaying fleet refresh, and dampening near-term demand within the India truck market.

Other drivers and restraints analyzed in the detailed report include:

- Scrappage Policy-Driven Replacement Demand

- Shift to CNG/LNG on TCO Benefits

- Volatile Diesel Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Light-duty trucks held 48.33% of 2024 shipments, underpinning the India truck market while posting a 6.94% CAGR through 2030. Urban road restrictions and e-commerce time windows favor compact wheelbases that weave through dense streets. OEM financing schemes and low-maintenance EV drivetrains further tilt demand toward this class. Medium-duty units cater to regional express lines, whereas heavy tractors dominate cement, steel, and coal corridors. Light-duty electrification unlocks rapid payback on 200-km urban routes, supported by depot chargers that bypass public-grid constraints.

Second-generation models such as Magenta Mobility's 3-ton EV now complete three turns daily, doubling asset productivity and reshaping cost curves. Meanwhile, rising ton-mile demand from Tier-3 trade clusters preserves internal-combustion variants, keeping the segment an indispensable growth engine within the India truck market.

Trucks in the 3.5-7.5 ton band captured 39.18% of 2024 volume, reflecting India's granular retail networks that call for payload agility rather than brute capacity. Their 7.14% CAGR stands above all other tonnage classes as omnichannel retailers push fast replenishment to micro-warehouses. Tight municipal axle mandates and low-bridge clearances reinforce small-tonnage utility.

Continued highway upgrades could gradually swing freight toward 16-ton gross vehicle weights for hub-to-hub lanes, yet doorstep delivery promises keep sub-7.5-ton demand vibrant. Strategically, OEMs overlay modular body kits to stretch platform economics, augmenting the India truck market size through SKU diversity without new homologation cycles.

Complete Report Scope:

- By Vehicle Type

- Light Duty

- Medium Duty

- Heavy Duty

- By Tonnage Capacity

- 3.5-7.5 Tons

- 7.5-16 Tons

- 16-30 Tons

- Above 30 Tons

- By Fuel Type

- Diesel

- Petrol

- Electric

- Other Fuel Type

- By Application

- Logistics

- Construction

- Agriculture

- Mining

- Utility

- Others

- By Ownership

- Fleet Operators

- Individual Owners

- By Body Type

- Flatbed

- Box Truck

- Refrigerated

- Tanker

- Tipper

List of Companies Covered in this Report:

- Tata Motors Limited

- Ashok Leyland

- Mahindra & Mahindra Limited

- VE Commercial Vehicles Ltd. (Eicher)

- BharatBenz (Daimler India Commercial Vehicles)

- Volvo Trucks India

- Scania Commercial Vehicles India Pvt. Ltd.

- Force Motors Limited

- Isuzu Motors India Private Limited

- Hino Motors India

- Olectra Greentech

- BYD India

- Omega Seiki Mobility

- Tresa Motors

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government Infrastructure Push (Bharatmala, Gati Shakti)

- 4.2.2 E-commerce-Led Logistics Boom

- 4.2.3 Scrappage Policy-Driven Replacement Demand

- 4.2.4 Shift to CNG/LNG on TCO Benefits

- 4.2.5 Cold-Chain Expansion in Tier-2/3 Cities

- 4.2.6 Connected-Truck Telematics Adoption

- 4.3 Market Restraints

- 4.3.1 High BS-VI Truck Capex

- 4.3.2 Volatile Diesel Prices

- 4.3.3 Driver Shortage and Aging Workforce

- 4.3.4 Sparse Heavy-Duty Charging Network

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value and Volume)

- 5.1 By Vehicle Type

- 5.1.1 Light Duty

- 5.1.2 Medium Duty

- 5.1.3 Heavy Duty

- 5.2 By Tonnage Capacity

- 5.2.1 3.5-7.5 Tons

- 5.2.2 7.5-16 Tons

- 5.2.3 16-30 Tons

- 5.2.4 Above 30 Tons

- 5.3 By Fuel Type

- 5.3.1 Diesel

- 5.3.2 Petrol

- 5.3.3 Electric

- 5.3.4 Other Fuel Type

- 5.4 By Application

- 5.4.1 Logistics

- 5.4.2 Construction

- 5.4.3 Agriculture

- 5.4.4 Mining

- 5.4.5 Utility

- 5.4.6 Others

- 5.5 By Ownership

- 5.5.1 Fleet Operators

- 5.5.2 Individual Owners

- 5.6 By Body Type

- 5.6.1 Flatbed

- 5.6.2 Box Truck

- 5.6.3 Refrigerated

- 5.6.4 Tanker

- 5.6.5 Tipper

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Tata Motors Limited

- 6.4.2 Ashok Leyland

- 6.4.3 Mahindra & Mahindra Limited

- 6.4.4 VE Commercial Vehicles Ltd. (Eicher)

- 6.4.5 BharatBenz (Daimler India Commercial Vehicles)

- 6.4.6 Volvo Trucks India

- 6.4.7 Scania Commercial Vehicles India Pvt. Ltd.

- 6.4.8 Force Motors Limited

- 6.4.9 Isuzu Motors India Private Limited

- 6.4.10 Hino Motors India

- 6.4.11 Olectra Greentech

- 6.4.12 BYD India

- 6.4.13 Omega Seiki Mobility

- 6.4.14 Tresa Motors

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

二手車市場分析與預測(至2035年):類型、產品類型、服務、技術、零件、應用、流程、最終用戶、形式

二手車市場分析與預測(至2035年):類型、產品類型、服務、技術、零件、應用、流程、最終用戶、形式 全球汽車電動尾門市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球汽車電動尾門市場規模、佔有率、趨勢和成長分析報告(2026-2034) 卡車市場商機、成長要素、產業趨勢分析及2026-2035年預測。

卡車市場商機、成長要素、產業趨勢分析及2026-2035年預測。 2026年全球拖車市場報告2026年全球混合動力卡車市場報告輕型卡車市場規模、市場佔有率和成長率、全球行業分析、按類型、應用和地區分類的細分以及未來預測(2026-2034 年)。

2026年全球拖車市場報告2026年全球混合動力卡車市場報告輕型卡車市場規模、市場佔有率和成長率、全球行業分析、按類型、應用和地區分類的細分以及未來預測(2026-2034 年)。 食品油輪市場:依罐體材質、容量範圍及終端用戶產業分類-2026-2032年全球預測

食品油輪市場:依罐體材質、容量範圍及終端用戶產業分類-2026-2032年全球預測 美國罐車運輸:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

美國罐車運輸:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年) 日本卡車市場規模、佔有率、趨勢和預測:按車輛類型、負載容量、燃料類型、應用和地區分類,2026-2034年

日本卡車市場規模、佔有率、趨勢和預測:按車輛類型、負載容量、燃料類型、應用和地區分類,2026-2034年 卡車市場-全球產業規模、佔有率、趨勢、機會、預測:按等級、燃料類型、最終用戶產業、地區和競爭格局分類,2021-2031年

卡車市場-全球產業規模、佔有率、趨勢、機會、預測:按等級、燃料類型、最終用戶產業、地區和競爭格局分類,2021-2031年