|

市場調查報告書

商品編碼

2066756

藝術品物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Fine Art Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

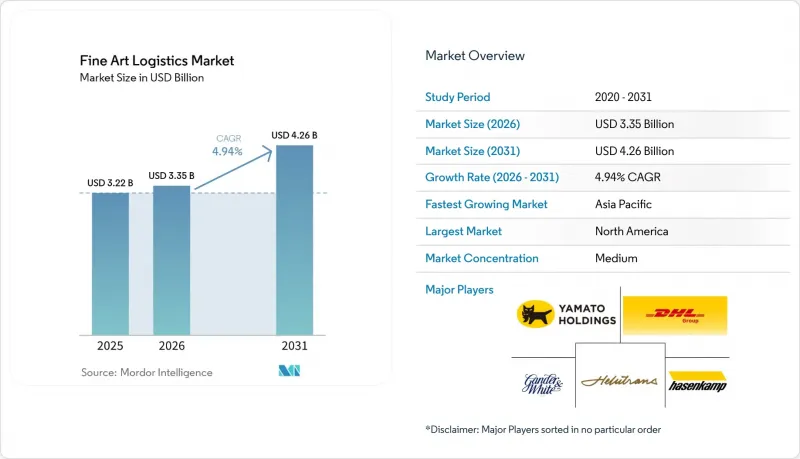

根據 Mordor Intelligence 預測,藝術品物流市場預計將從 2025 年的 32.2 億美元成長到 2026 年的 33.5 億美元,到 2031 年達到 42.6 億美元,2026 年至 2031 年的複合年成長率為 4.94%。

混合式(實體場館+線上)競標正在縮短運輸時間,同時,隨著新加坡、香港、日內瓦和杜拜等地的免稅港增加洲際轉運點數量,物流結構也正在轉變。本報告按物流功能(運輸(陸運、空運、海運、鐵路)、倉儲配送、附加價值服務)、最終用戶(藝術品、經銷商和畫廊、競標行、博物館、藝術博覽會、私人收藏家及其他)和地區(北美、南美、亞太、歐洲、中東和非洲)進行分類。市場預測以美元計價。

全球藝術品物流市場的趨勢與洞察

混合式(實體場所+線上)競標形式的普及導致了即時出貨量的激增。

目前,競標行正在全球將現場預展與線上競標同步進行。藝術品必須在直播開始前抵達預展地點,通過數位指紋驗證,並在數天內運送給買家。這使得傳統的為期三週的競標週期縮短至不到十天。遠端3D掃描技術使競標能夠查看高解析度的複製影像,但實體藝術品仍需運輸,以滿足售前狀況報告標準。不斷擴大的競標群體導致跨境售後運輸量增加,推動藝術品物流市場的運輸能力轉向高多模態模式。與護照、簽證和海關申報相關的合規要求增加了行政工作量,但專家們正在將這些流程整合到承包競標物流方案中。

提高保險承保限額將導致相關人員轉向專業公司。

在發生多起重大損失事件後,保險公司現在要求更高的「全程」保險限額,促使相關人員選擇與勞合社預先篩選過的物流公司簽訂合約。更嚴格的實質審查要求在提貨前進行製裁篩檢和洗錢防制報告。頂級供應商提供全面的保險保障,加快保單簽發速度,從而形成分級供應結構,小規模承運商負責低價值的本地運輸。日益繁重的行政工作量有利於那些提供全天候理賠熱線和數位化審計追蹤的公司。

噴射機燃料和船用燃料油價格的波動會造成成本的不確定性。

能源價格波動導致額外費用超出年度物流預算,並擠壓了提前數月鎖定價格的合約利潤空間。大型供應商透過期貨交易和轉嫁條款來對沖燃料風險,進一步拉大了與小型競爭對手之間的差距。這種價格波動正在加速行業整合,越來越多的公司尋求收購,以獲得應對成本飆升所需的財務實力。

細分市場分析

至2025年,運輸業將佔藝術品物流市場的60.39%。空運憑藉其嚴格的安全保障和快速的運輸速度,將主導高價值物品的運輸;而採用生物燃料的海運航線將承運對成本敏感的展會貨物。在低排放區,電動車將擴大用於最後一公里運輸,鐵路走廊將以低碳的方式連接歐洲各大城市。倉儲和配送將發揮溫控轉運樞紐的作用,支援多地點運輸路線。附加價值服務的成長速度預計將超過藝術品物流市場的整體規模,這反映出客戶對包含合規性、保險和認證支援等一站式服務的需求。物聯網感測器、區塊鏈帳本和客製化風險諮詢正在將曾經的一次性運輸業務轉變為多年期管理合約。

預計在預測期內,附加價值服務將以5.45%的複合年成長率實現最快成長。技術投資正在重塑定價結構。智慧箱租賃、線上預訂平台以及與競標目錄的API整合正在減少手動處理步驟。能夠提供即時儲存歷史資料的公司可以設定更高的價格,而那些依賴傳統運輸車輛和紙本清單的公司則被迫在微薄的利潤率下競爭。這種差距加劇了藝術品物流市場的「兩極化」:數位化供應商不斷擴大其EBITDA和收購倍數,而數位化程度較低的承運商則面臨收入停滯不前的困境。

區域分析

以紐約和洛杉磯競標市場為中心的北美地區預計在2025年將佔全球銷售額的42.14%。藏家高度集中,確保了全年不間斷的運輸需求,而清晰的海關程序和保稅倉儲則有效減少了監管摩擦。美國博物館堅持嚴格的文物保護標準,從而推高了對配備物聯網技術的運輸箱和GPS追蹤車輛的高階需求。

歐洲仍然是藝術品貿易的歷史樞紐,但英國脫歐後的各項程序減緩了英國與歐盟之間的運輸速度,導致部分貿易轉移到盧森堡和日內瓦的自由港。歐洲鐵路網路為歐盟內部的低碳運輸路線提供了可能,而倫敦眾多保險公司的存在也確保了藝術品物流市場所需的承保人供應。歐盟自2027年起強制要求揭露碳排放的法規預計將加速生質燃料和電動車的普及。

亞太地區是成長最快的地區,預計到2031年將以5.55%的複合年成長率成長。香港和新加坡的自由港為倉儲提供了稅收優惠環境,而中國主要城市(一線城市)的超級富豪階級人口正在激增。首爾、東京和雪梨等地的政府文化投資正在推動博物館的擴建,從而帶動西方藝術瑰寶的進口量增加,以及亞洲現代主義作品國際巡迴展覽的增加。擁有會說中文的配送人員以及具備西方文物保護和修復資格的供應商正在擴大其市場佔有率。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 混合式(現場+線上)競標模式正在擴大即時出貨量。

- 隨著保險覆蓋範圍門檻的提高,相關人員正轉向專業服務提供者。

- 歐洲和海灣合作理事會國家免稅藝術品自由港的擴張將刺激洲際貿易。

- 具備物聯網功能的溫控貨櫃正在推動智慧物流供應商的需求。

- 對生物燃料遠洋航線的需求正在推動永續海上運輸的發展。

- 公寓所有權平台需要輪換儲存和微型倉配模式。

- 市場限制因素

- 噴射機燃料和船用燃料油價格的波動造成了成本的不確定性。

- 地緣政治制裁增加了出口許可和合規的複雜性。

- 博物館級永續包裝材料的短缺正在減緩綠色轉型進程。

- 對非法古董更嚴格的檢查延長了獲得來源證明所需的時間。

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 關於票價需要注意的幾點

第5章 市場規模與成長預測

- 透過物流功能

- 運輸

- 道路運輸

- 航空

- 海路和內河航道

- 鐵路

- 倉儲/物流

- 附加價值服務(貼標籤、套件組裝、諮詢)

- 運輸

- 最終用戶

- 藝術品經銷商和畫廊

- 競標行

- 博物館

- 藝術博覽會

- 私人收藏家

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 秘魯

- 智利

- 阿根廷

- 其他南美國家

- 亞太地區

- 印度

- 中國

- 日本

- 澳洲

- 韓國

- 東南亞(新加坡、馬來西亞、泰國、印尼、越南、菲律賓)

- 其他亞太國家

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 比荷盧經濟聯盟(比利時、荷蘭、盧森堡)

- 北歐國家(丹麥、芬蘭、冰島、挪威、瑞典)

- 其他歐洲國家

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Yamato Transport Co., Ltd.

- Gander & White

- Sinotrans

- Helu-Trans

- Hasenkamp

- DSV A/S

- Masterpiece International

- US Art

- DHL Group

- Andre Chenue

- LP Art

- Crozier Fine Arts

- Cadogan Tate

- Crown Fine Art

- Momart

- Dietl International

- Convelio

- Cargolux(CV Precious)

- Lotus Fine Arts Logistics

- Baltrans*

第7章 市場機會與未來展望

According to Mordor Intelligence, the fine art logistics market is expected to increase from USD 3.22 billion in 2025 to USD 3.35 billion in 2026 and reach USD 4.26 billion by 2031, growing at a CAGR of 4.94% over 2026-2031.

Structural change is underway as hybrid live-plus-digital auctions tighten shipment windows, while duty-free freeports in Singapore, Hong Kong, Geneva, and Dubai multiply inter-continental transfer points. This report is Segmented by Logistics Function (Transportation (Road, Air, Sea, and Rail), Warehousing & Distribution, and Value-Added Services), by End Users (Art, Dealers and Galleries, Auction Houses, Museums, Art Fairs, Private Collectors, and Others), and by Geography (North America, South America, Asia Pacific, Europe, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Fine Art Logistics Market Trends and Insights

Hybrid Live-Plus-Digital Auction Formats Intensify Just-In-Time Shipment Volumes

Auction houses now synchronize in-person previews with global online bidding. Artworks must reach preview venues ahead of streaming schedules, pass digital fingerprint checks, and depart for buyers within days, compressing the traditional three-week auction cycle into less than 10 days. Remote 3-D scanning lets bidders view high-resolution twins, yet the physical object still travels to meet pre-sale condition reporting standards. Broader bidder reach increases post-sale cross-border shipments, shifting fine art logistics market capacity toward agile, multi-modal routing. Compliance layers tied to passports, visas, and customs declarations add paperwork that specialist providers embed into turnkey auction logistics packages.

Higher Insurance Coverage Thresholds Push Stakeholders Toward Specialist Providers

Underwriters now insist on larger "nail-to-nail" limits after several high-profile loss events, driving stakeholders toward logistics firms with pre-vetted Lloyd's agreements. Enhanced due-diligence requires sanctions screening and anti-money-laundering reporting before pick-up. Premium providers offer bundled coverage that accelerates policy issuance, creating a tiered supply landscape where smaller carriers handle lower-value regional moves. The added paperwork favors firms that maintain 24-hour specialist claims desks and digital audit trails.

Volatile Jet-Fuel and Bunker Prices Inject Cost Unpredictability

Energy-price swings translate into surcharges that outpace annual logistics budgets, squeezing margins when contracts lock prices months ahead. Larger providers hedge fuel exposure through futures and pass-through clauses, widening the gap with smaller rivals. The volatility accelerates consolidation as acquisition candidates seek the balance-sheet muscle required to weather cost spikes.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Duty-Free Art Freeports in Europe and GCC Amplifies Inter-Continental Flows

- IoT-Enabled Climate-Monitoring Crates Create Pull for Smart-Logistics Vendors

- Geopolitical Sanctions Heighten Export-License and Compliance Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation captured 60.39% of fine art logistics market share in 2025. Air freight dominates high-value transfers thanks to stringent security and rapid transit times, while bio-marine-fuel sea lanes absorb cost-sensitive exhibition shipments. Road fleets, increasingly electric inside low-emission zones, handle final-mile moves, and rail corridors link European capitals on lower carbon footprints. Warehousing and distribution provide climate-controlled bridges that support multi-stop itineraries. Value-added services are projected to grow faster than the overall fine art logistics market size, reflecting client appetite for bundled regulatory, insurance, and authentication support. IoT sensors, blockchain ledgers, and bespoke risk consulting convert once-transactional shipping jobs into multi-year stewardship contracts.

Value-added services are expected to grow the fastest with 5.45% CAGR over the forecast period. Technology investment is reshaping price structures. Smart-box leasing, online booking portals, and API connectivity with auction catalogues compress manual touchpoints. Firms that can demonstrate real-time chain-of-custody data command premiums, while those limited to legacy vans and paper manifests compete on thin margins. The divergence reinforces a two-speed Fine art logistics market, where digitally enabled providers expand EBITDA and acquisition multiples, and undigitized carriers face revenue stagnation.

Geography Analysis

North America generated 42.14% of 2025 revenue, anchored by New York and Los Angeles auction ecosystems. Dense collector bases support year-round moves, while well-defined customs procedures and bonded warehouses lower regulatory friction. United States museums maintain strict conservation standards, driving premium demand for IoT-equipped crates and GPS-tracked vehicles.

Europe remains the historic crossroads of fine art trade, yet post-Brexit paperwork has lengthened UK-EU transfers, nudging some volume toward Luxembourg and Geneva freeports. Continental rail networks enable lower-carbon intra-EU routes, and strong insurer presence in London retains underwriting talent essential to the Fine art logistics market. EU regulations mandating carbon disclosure from 2027 will likely accelerate adoption of bio-fuel and electric fleets.

Asia-Pacific is the fastest-growing region, expanding at a 5.55% CAGR to 2031. Hong Kong and Singapore freeports underpin tax-efficient storage, while China's Tier-1 cities host a surging ultra-high-net-worth population. Government cultural investments in Seoul, Tokyo, and Sydney spur museum expansion, driving import flows of Western masterpieces and outbound touring shows of Asian modernists. Providers that combine Mandarin-speaking couriers with Western conservation credentials gain share.

- Yamato Transport Co., Ltd.

- Gander & White

- Sinotrans

- Helu-Trans

- Hasenkamp

- DSV A/S

- Masterpiece International

- U.S. Art

- DHL Group

- Andre Chenue

- LP Art

- Crozier Fine Arts

- Cadogan Tate

- Crown Fine Art

- Momart

- Dietl International

- Convelio

- Cargolux (CV Precious)

- Lotus Fine Arts Logistics

- Baltrans*

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Hybrid Live-Plus-Digital Auction Formats Intensify Just-in-Time Shipment Volumes

- 4.2.2 Higher Insurance Coverage Thresholds Push Stakeholders Toward Specialist Providers

- 4.2.3 Expansion of Duty-Free Art Freeports in Europe and GCC Amplifies Inter-Continental Flows

- 4.2.4 IoT-Enabled Climate-Monitoring Crates Create Pull for Smart-Logistics Vendors

- 4.2.5 Demand for Bio-Marine-Fuel Shipping Lanes Spurs Sustainable Ocean Transport

- 4.2.6 Fractional-Ownership Platforms Require Rotating Custody and Micro-Fulfilment Models

- 4.3 Market Restraints

- 4.3.1 Volatile Jet-Fuel and Bunker Prices Inject Cost Unpredictability

- 4.3.2 Geopolitical Sanctions Heighten Export-License and Compliance Complexity

- 4.3.3 Shortage of Museum-Grade Sustainable Packing Substrates Slows Green Transition

- 4.3.4 Stricter Anti-Illicit-Antiquities Checks Prolong Provenance Documentation Cycles

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Spotlight on Transport Rates

5 Market Size and Growth Forecasts (Value)

- 5.1 By Logistics Function

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Air

- 5.1.1.3 Sea and Inland Waterways

- 5.1.1.4 Rail

- 5.1.2 Warehousing and Distribution

- 5.1.3 Value-added Services (Labelling, Kitting, Consulting)

- 5.1.1 Transportation

- 5.2 By End Users

- 5.2.1 Art Dealers and Galleries

- 5.2.2 Auction Houses

- 5.2.3 Museums

- 5.2.4 Art Fairs

- 5.2.5 Private Collectors

- 5.2.6 Others

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 South America

- 5.3.2.1 Brazil

- 5.3.2.2 Peru

- 5.3.2.3 Chile

- 5.3.2.4 Argentina

- 5.3.2.5 Rest of South America

- 5.3.3 Asia Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.3.3.7 Rest of Asia-Pacific

- 5.3.4 Europe

- 5.3.4.1 United Kingdom

- 5.3.4.2 Germany

- 5.3.4.3 France

- 5.3.4.4 Spain

- 5.3.4.5 Italy

- 5.3.4.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.3.4.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.3.4.8 Rest of Europe

- 5.3.5 Middle East And Africa

- 5.3.5.1 United Arab of Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 South Africa

- 5.3.5.4 Nigeria

- 5.3.5.5 Rest of Middle East And Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Yamato Transport Co., Ltd.

- 6.4.2 Gander & White

- 6.4.3 Sinotrans

- 6.4.4 Helu-Trans

- 6.4.5 Hasenkamp

- 6.4.6 DSV A/S

- 6.4.7 Masterpiece International

- 6.4.8 U.S. Art

- 6.4.9 DHL Group

- 6.4.10 Andre Chenue

- 6.4.11 LP Art

- 6.4.12 Crozier Fine Arts

- 6.4.13 Cadogan Tate

- 6.4.14 Crown Fine Art

- 6.4.15 Momart

- 6.4.16 Dietl International

- 6.4.17 Convelio

- 6.4.18 Cargolux (CV Precious)

- 6.4.19 Lotus Fine Arts Logistics

- 6.4.20 Baltrans*

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Sustainability and Carbon-Neutral Logistics

- 7.3 Digital Tracking and Provenance Solutions

北美藝術品物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

北美藝術品物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 美術和雕塑市場規模、佔有率和成長分析:按主題、時代/風格、價格範圍、最終用戶、分銷管道和地區分類-2026-2033年產業預測

美術和雕塑市場規模、佔有率和成長分析:按主題、時代/風格、價格範圍、最終用戶、分銷管道和地區分類-2026-2033年產業預測 2026-2030年全球藝術品經銷市場

2026-2030年全球藝術品經銷市場 藝術品物流市場:依服務類型、運輸方式、技術及最終用戶分類-2026-2032年全球市場預測

藝術品物流市場:依服務類型、運輸方式、技術及最終用戶分類-2026-2032年全球市場預測 藝術基金市場:按基金類型、用途和地區分類藝術品物流:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)

藝術基金市場:按基金類型、用途和地區分類藝術品物流:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030) 美術品·雕刻的全球市場:產業分析,規模,佔有率,成長,趨勢,預測(2024年~2031年)

美術品·雕刻的全球市場:產業分析,規模,佔有率,成長,趨勢,預測(2024年~2031年) 藝術品物流的世界市場

藝術品物流的世界市場