|

市場調查報告書

商品編碼

2066618

西班牙快遞、速遞、包裹市場:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Spain Courier, Express, And Parcel (CEP) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

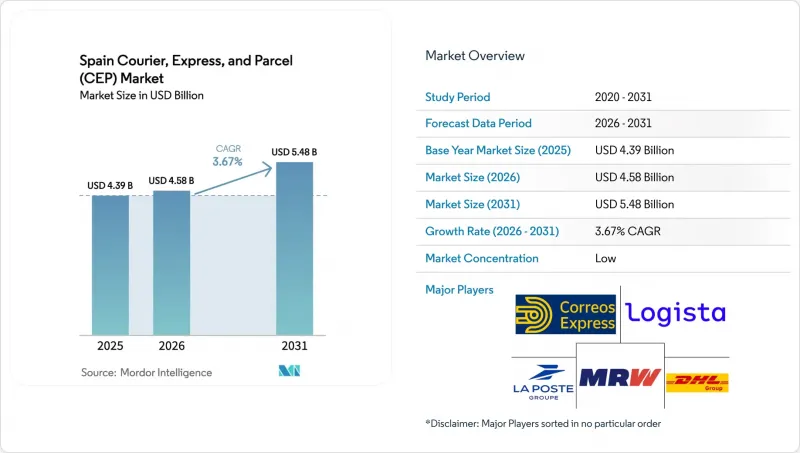

據 Mordor Intelligence 稱,西班牙快遞、速遞、包裹 (CEP) 市場在 2025 年的價值為 43.9 億美元,預計到 2031 年將從 2026 年的 45.8 億美元成長至 54.8 億美元,在預測期(2026-2031 年)成長至 54.8 億美元,在預測期為 3.67%。

西班牙電子商務滲透率高達兩位數,退貨率也高達22%,加上對低溫運輸服務的需求不斷成長,小包裹量持續攀升。本報告按目的地(國內、國際)、配送速度(快遞、普通快遞)、模式(B2B等)、貨物重量(重型、輕型、中重型)、運輸方式(空運、陸運、其他)以及終端用戶行業(電子商務、金融服務等)進行細分。市場預測以美元計價。

西班牙快遞、速遞、包裹市場的趨勢與見解。

西班牙高達 22% 的電子商務退貨率正在推動逆向物流的激增。

西班牙近22%的退貨率使其成為歐洲最具挑戰性的電商環境之一,迫使企業重組其樞紐輻射式網路以適應雙向物流,並在配送中心內增設檢驗和再處理生產線。服裝和鞋類佔退貨的大部分,由於尺寸不確定性以及消費者購買多個尺寸的情況,退貨率通常超過30%。 C2C(消費者對消費者)市場為雙向物流增添了新的環節,使所有C2C貨運的處理地點數量增加了一倍。投資於專用逆向物流能力和庫存視覺化平台的企業正在將傳統的成本中心轉變為差異化優勢。隨著越來越多的品牌採用召回計劃,預計未來五年西班牙快遞、包裹和快遞(CEP)市場的逆向物流量成長將超過正向物流的成長。

人工智慧驅動的動態路線規劃和負載容量最佳化可降低每公里成本。

透過分析交通狀況、天氣資訊和歷史配送模式的機器學習演算法,幹線運輸和最後一公里配送成本降低了12%至18%。即時配送重新排序功能使巴塞隆納擁塞路段的每小時停靠次數增加了20%以上,使承運商能夠在平台主導的貨運壓力下保持盈利。像亞馬遜阿斯圖裡亞斯物流中心這樣資本密集的機器人配送中心,透過將人工智慧分類與自動導引運輸車(AGV)相結合,維持了高峰時段的運力。由於難以投資資料科學人才,中型供應商擴大採用白牌SaaS最佳化工具或與科技公司合作,這進一步拉大了西班牙快遞、速遞和包裹(CEP)市場競爭對手之間的能力差距。

紙板、燃料和冷媒價格的飆升導致單位成本上漲超過 8%。

紙漿短缺導致瓦楞紙板價格飆升15-20%,柴油價格在每公升1.20歐元至1.60歐元之間波動,加上氟化氣體逐步減量導致冷媒成本上漲,到2025年,這些因素將對整體利潤率構成壓力。儘管承運商對沖了燃油成本並簽訂了包裝材料的固定價格契約,但控制超過80%訂單的大型平台卻抵制價格調整。由於小型供應商難以消化價格上漲的影響,西班牙快遞、速遞和包裹(CEP)市場出現了防禦性併購以及更加重視人工智慧驅動的效率提升措施。

細分市場分析

到2025年,製造業將佔西班牙快遞、速遞、包裹(CEP)市場佔有率的32.41%,主要得益於加泰隆尼亞和納瓦拉地區汽車和機械生產的穩定成長。儘管西班牙與製造業相關的快遞、速遞、包裹市場依然強勁,但其增速較為溫和,處於個位數中段水平,與工業生產週期相符。

受時尚、電子產品和家居用品行業線上滲透率不斷提高的推動,包括C2C轉售在內的電子商務小包裹預計將以4.00%的複合年成長率成長至2031年。製造商擴大採用B2B電子商務平台採購零件,從而實現可預測的小批量出貨。同時,時尚零售商正利用逆向物流中心應對超過30%的退貨率。金融服務業支援高利潤的文件宅配,而更嚴格的GDP法規促使醫療用品托運人使用高階快遞服務。終端用戶的多元化正在緩解特定產業的波動性,這使得能夠在西班牙CEP(快遞、速遞、包裹)市場經營跨產業網路的營運商更具優勢。

2025年,西班牙國內小包裹佔西班牙快遞、速遞、包裹(CEP)市場規模的63.92%,但隨著都市區市場服務飽和,其成長速度正在放緩。國際物流預計到2031年將維持3.80%的複合年成長率,這主要得益於歐盟增值稅(VAT)和IOSS法規的協調統一,簡化了150歐元以下貨物的海關手續。

跨境成長主要集中在西班牙、法國和德國之間的運輸路線上,氫燃料卡車試點計畫和鐵路-鐵路聯運服務為此提供了支持,每年可減少11,500次卡車運輸。西班牙出口商也利用文化親和性和時區優勢,透過UPS的Estafeta網路拓展對拉丁美洲的出口。隨著國際貿易結構的多元化,承運商被迫加強清關能力,並投資建造覆蓋整個西班牙快遞、快遞和包裹市場的多幣種、多語言客戶入口網站。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 人口統計數據

- 按經濟活動分類的GDP構成

- 按經濟活動分類的GDP成長率

- 通貨膨脹

- 經濟表現及概覽

- 電子商務產業的趨勢

- 製造業的發展趨勢

- 運輸和倉儲部門的GDP

- 出口趨勢

- 進口趨勢

- 燃油價格

- 物流績效

- 基礎設施

- 法律規範

- 價值鍊和通路分析

- 市場促進因素

- 西班牙高達 22% 的電子商務退貨率正在推動逆向物流的激增。

- 人工智慧驅動的動態路線規劃和最佳化的負載容量降低了每公里成本。

- 跨境食品雜貨和食材自煮包的蓬勃發展,推動了對溫控小包裹的需求。

- 歐盟資助的氫燃料卡車示範計畫降低了長途運輸的排放成本和通行費。

- 歐盟對藥品GDP監管的收緊導致低溫運輸快遞處理的貨物量增加。

- C2C 轉售平台(Wallapop、Vinted)的快速成長以及小包裹流量的增加。

- 市場限制因素

- 由於紙板、燃料和冷媒價格大幅上漲,單位成本上漲了 8% 以上。

- CSRD 強制要求的 ESG 審計正在增加 CEP 公司的合規相關成本。

- 針對追蹤 API 的網路攻擊日益加劇,導致因違反服務等級協定 (SLA) 而被罰款,並損害了品牌形象。

- 都市區取貨點和儲物櫃位置的飽和進一步限制了最後一公里配送密度的增加。

- 市場上的技術創新

- 波特五力分析

第5章 市場規模與成長預測

- 目的地

- 國內的

- 國際的

- 配送速度

- 表達

- 非加速

- 特定型號

- Business-to-Business(B2B)

- Business-to-Consumer(B2C)

- Consumer-to-Consumer(C2C)

- 負載能力

- 重載

- 輕型貨物

- 中等重量貨物

- 透過運輸方式

- 航空

- 路

- 其他

- 按最終用戶行業分類

- 電子商務

- 金融服務(BFSI)

- 衛生保健

- 製造業

- 一級產業

- 批發和零售貿易(線下)

- 其他

第6章 競爭情勢

- 市場集中度

- 關鍵策略趨勢

- 市佔率分析

- 公司簡介

- Correos Express

- DHL Group

- FedEx

- GEODIS

- La Poste Group(including SEUR)

- Logista

- MRW

- Paack

- Szendex

- International Distribution Services plc

- Amazon, Inc.

- CTT Express

- Envialia

- TIPSA

- Stuart Delivery

- Sending Transporte Urgente

- Rangel Logistics

- Zeleris

- ID Logistics

- United Parcel Service of America, Inc.(UPS)

第7章 市場機會與未來展望

According to Mordor Intelligence, the spain courier, express, and parcel market size was valued at USD 4.39 billion in 2025 and estimated to grow from USD 4.58 billion in 2026 to reach USD 5.48 billion by 2031, at a 3.67% CAGR during the forecast period (2026-2031).

Spain's double-digit e-commerce penetration, a persistently high 22% return rate, and growing demand for cold-chain services keep parcel volumes on an upward trajectory. This report is Segmented by Destination (Domestic, International), by Speed of Delivery (Express, Non-Express), by Model (Business-To-Business, and More), by Shipment Weight (Heavy Weight, Light Weight, Medium Weight), by Mode of Transport (Air, Road, Others), and by End User Industry (E-Commerce, Financial Services, and More). The Market Forecasts are Provided in Terms of Value (USD).

Spain Courier, Express, And Parcel (CEP) Market Trends and Insights

Surge in Reverse Logistics Driven by Spain's 22% E-Commerce Return Rate

Return rates near 22% make Spain one of Europe's most challenging e-commerce environments, prompting operators to rebuild hub-and-spoke networks for two-way flows while installing inspection and refurbishment lines inside depots. Fashion and footwear account for the bulk of returns and often exceed 30% due to size uncertainty and bracketing purchases. Peer-to-peer marketplaces add another layer of bidirectional traffic as every C2C shipment doubles touchpoints. Operators that invest in dedicated reverse logistics capacity and inventory-visibility platforms increasingly turn a traditional cost center into a source of differentiation. As more brands introduce take-back schemes, reverse flow volumes inside the Spain courier, express, and parcel market are projected to outpace forward shipment growth over the next five years.

AI-Powered Dynamic Route Planning and Load Balancing Cutting Cost per Kilometer

Machine-learning algorithms that ingest traffic, weather, and historical delivery patterns now trim 12-18% off line-haul and last-mile costs. Real-time re-sequencing raises stops per hour by more than 20% on dense Barcelona routes, allowing carriers to protect margins despite platform-driven rate pressure. Capital-intensive robotics hubs such as Amazon's Asturias facility combine AI sortation with automated guided vehicles to sustain peak-season throughput. Mid-tier providers unable to fund data-science talent increasingly adopt white-label SaaS optimization tools or partner with technology firms, widening the capability gap among competitors in the Spain courier, express, and parcel market.

Inflation Spikes in Corrugate, Fuel, and Refrigerants Adding More Than 8% to Unit Costs

Corrugate surged 15-20% on pulp shortages, diesel prices swung between EUR 1.20-1.60 per liter, and F-gas phase-downs inflated refrigerant costs, collectively compressing margins in 2025. Carriers hedged fuel and signed fixed-rate packaging contracts, yet high-volume platforms controlling over 80% of orders resisted price adjustments. Smaller providers found limited headroom to absorb spikes, prompting defensive mergers and stronger focus on AI efficiency levers inside the Spain courier, express, and parcel market.

Other drivers and restraints analyzed in the detailed report include:

- Cross-Border Grocery and Meal-Kit Boom Boosting Temperature-Controlled Parcel Demand

- EU-Funded Hydrogen Truck Pilots Lowering Long-Haul Emission Costs and Toll Exposure

- CSRD-Mandated ESG Auditing Increasing Compliance Overheads for CEP Firms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Manufacturing generated 32.41% of the Spain Courier, Express, and Parcel (CEP) market share in 2025, supported by steady automotive and machinery output in Catalonia and Navarre. The Spain courier, express, and parcel market linked to manufacturing remains resilient but posts modest mid-single-digit growth tied to industrial production cycles.

E-commerce parcels, including C2C resale, are forecast to grow 4.00% CAGR through 2031, buoyed by deepening online penetration in fashion, electronics, and homeware baskets. Manufacturers increasingly adopt B2B e-commerce portals for spare parts, driving predictable small-batch shipments, while fashion retailers leverage reverse logistics hubs to cope with returns exceeding 30%. Financial services sustain high-margin document couriers, and stricter GDP rules push healthcare senders toward premium express services. End-user diversification staves off sector-specific volatility and rewards operators able to run multi-vertical networks inside the Spain courier, express, and parcel market.

Domestic parcels represented 63.92% of the Spain Courier, Express, and Parcel (CEP) market size in 2025, yet face slowing growth as urban markets reach service saturation. International flows will register 3.80% CAGR to 2031, lifted by EU VAT harmonization and IOSS rules that cut customs friction for sub-EUR 150 shipments.

Cross-border growth clusters along Spain-France-Germany corridors supported by hydrogen truck pilots and rail-road services that eliminate 11,500 annual truck trips. Spanish exporters also tap UPS's Estafeta network to Latin America, capitalizing on cultural affinity and time-zone alignment. The widening international mix compels carriers to refine customs-brokerage capabilities and invest in multi-currency, multi-language customer portals across the Spain courier, express, and parcel market.

List of Companies Covered in this Report:

- Correos Express

- DHL Group

- FedEx

- GEODIS

- La Poste Group (including SEUR)

- Logista

- MRW

- Paack

- Szendex

- International Distribution Services plc

- Amazon, Inc.

- CTT Express

- Envialia

- TIPSA

- Stuart Delivery

- Sending Transporte Urgente

- Rangel Logistics

- Zeleris

- ID Logistics

- United Parcel Service of America, Inc. (UPS)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Demographics

- 4.3 GDP Distribution by Economic Activity

- 4.4 GDP Growth by Economic Activity

- 4.5 Inflation

- 4.6 Economic Performance and Profile

- 4.6.1 Trends in E-Commerce Industry

- 4.6.2 Trends in Manufacturing Industry

- 4.7 Transport and Storage Sector GDP

- 4.8 Export Trends

- 4.9 Import Trends

- 4.10 Fuel Price

- 4.11 Logistics Performance

- 4.12 Infrastructure

- 4.13 Regulatory Framework

- 4.14 Value Chain and Distribution Channel Analysis

- 4.15 Market Drivers

- 4.15.1 Surge in Reverse Logistics Driven by Spain's 22 % E-Commerce Return Rate

- 4.15.2 AI-Powered Dynamic Route-Planning and Load-Balancing Cutting Cost Per Kilometer

- 4.15.3 Cross-Border Grocery and Meal-Kit Boom Boosting Temperature-Controlled Parcel Demand

- 4.15.4 EU-Funded Hydrogen Truck Pilots Lowering Long-Haul Emission Costs and Toll Exposure

- 4.15.5 Stricter EU GDP Pharma Rules Expanding Cold-Chain Express Volumes

- 4.15.6 Rapid Rise of C2C Resale Platforms (Wallapop, Vinted) Multiplying Micro-Parcel Flows

- 4.16 Market Restraints

- 4.16.1 Inflation Spikes in Corrugate, Fuel, and Refrigerants Adding More Than 8 % to Unit Costs

- 4.16.2 CSRD-Mandated ESG Auditing Increasing Compliance Overheads for CEP Firms

- 4.16.3 Escalating Cyber-Attacks on Tracking APIs Causing SLA Penalties and Brand Damage

- 4.16.4 Saturation of Urban Pick-Up/Locker Points Limiting Further Last-Mile Density Gains

- 4.17 Technology Innovations in the Market

- 4.18 Porter's Five Forces Analysis

- 4.18.1 Threat of New Entrants

- 4.18.2 Bargaining Power of Buyers

- 4.18.3 Bargaining Power of Suppliers

- 4.18.4 Threat of Substitutes

- 4.18.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Destination

- 5.1.1 Domestic

- 5.1.2 International

- 5.2 By Speed of Delivery

- 5.2.1 Express

- 5.2.2 Non-Express

- 5.3 By Model

- 5.3.1 Business-to-Business (B2B)

- 5.3.2 Business-to-Consumer (B2C)

- 5.3.3 Consumer-to-Consumer (C2C)

- 5.4 By Shipment Weight

- 5.4.1 Heavy Weight Shipments

- 5.4.2 Light Weight Shipments

- 5.4.3 Medium Weight Shipments

- 5.5 By Mode of Transport

- 5.5.1 Air

- 5.5.2 Road

- 5.5.3 Others

- 5.6 By End User Industry

- 5.6.1 E-Commerce

- 5.6.2 Financial Services (BFSI)

- 5.6.3 Healthcare

- 5.6.4 Manufacturing

- 5.6.5 Primary Industry

- 5.6.6 Wholesale and Retail Trade (Offline)

- 5.6.7 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Correos Express

- 6.4.2 DHL Group

- 6.4.3 FedEx

- 6.4.4 GEODIS

- 6.4.5 La Poste Group (including SEUR)

- 6.4.6 Logista

- 6.4.7 MRW

- 6.4.8 Paack

- 6.4.9 Szendex

- 6.4.10 International Distribution Services plc

- 6.4.11 Amazon, Inc.

- 6.4.12 CTT Express

- 6.4.13 Envialia

- 6.4.14 TIPSA

- 6.4.15 Stuart Delivery

- 6.4.16 Sending Transporte Urgente

- 6.4.17 Rangel Logistics

- 6.4.18 Zeleris

- 6.4.19 ID Logistics

- 6.4.20 United Parcel Service of America, Inc. (UPS)

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

全球宅配、包裹及小包裹市場-2026-2032年市場預測

全球宅配、包裹及小包裹市場-2026-2032年市場預測 代出貨市場規模、佔有率和成長分析:按產品類型、經營模式、平台類型、供應商類型、公司規模、銷售管道、最終用戶和地區分類-2026-2033年產業預測

代出貨市場規模、佔有率和成長分析:按產品類型、經營模式、平台類型、供應商類型、公司規模、銷售管道、最終用戶和地區分類-2026-2033年產業預測 快遞小包裹宅配(CEP) 市場規模、佔有率和成長分析:按服務類型、目的地、運輸方式、遞送速度、包裹重量和地區分類-2026-2033 年產業預測

快遞小包裹宅配(CEP) 市場規模、佔有率和成長分析:按服務類型、目的地、運輸方式、遞送速度、包裹重量和地區分類-2026-2033 年產業預測 英國國內宅配( 小包裹):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

英國國內宅配( 小包裹):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 生鮮食品在地化配送市場:預測至 2034 年 -產品類型、配送模式、平台類型、訂單規模、支付方式、最終用戶和地區分類的全球分析德國戶外配送:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)全球宅配和小包裹市場預測至2034年-按服務類型、遞送速度、目的地、貨物類型、客戶類型、最終用戶產業和地區分類的分析智慧洗衣取送市場預測至2034年-全球服務類型、服務模式、預訂方式、技術、支付方式、最終用戶和區域分析英國高階配送服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

生鮮食品在地化配送市場:預測至 2034 年 -產品類型、配送模式、平台類型、訂單規模、支付方式、最終用戶和地區分類的全球分析德國戶外配送:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)全球宅配和小包裹市場預測至2034年-按服務類型、遞送速度、目的地、貨物類型、客戶類型、最終用戶產業和地區分類的分析智慧洗衣取送市場預測至2034年-全球服務類型、服務模式、預訂方式、技術、支付方式、最終用戶和區域分析英國高階配送服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 2026 年至 2035 年宅配、小包裹服務市場的市場機會、成長要素、產業趨勢與預測。

2026 年至 2035 年宅配、小包裹服務市場的市場機會、成長要素、產業趨勢與預測。