|

市場調查報告書

商品編碼

2066471

木漿:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Wood Pulp - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

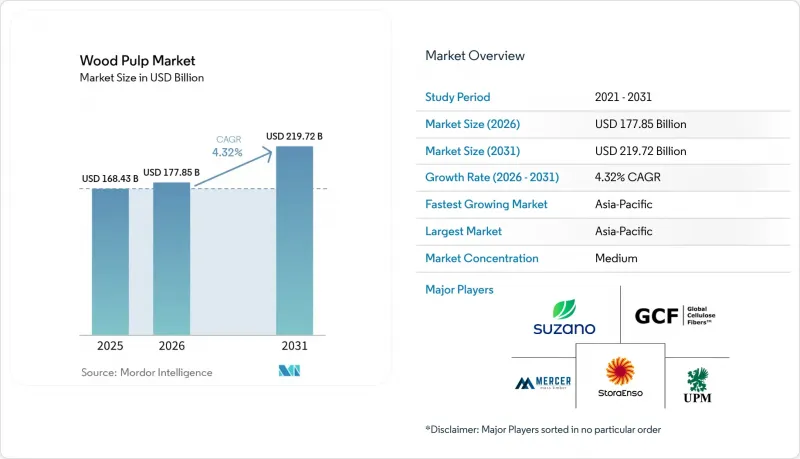

據 Mordor Intelligence 稱,2025 年木漿市場價值為 1,684 億美元,預計到 2031 年將達到 2,197 億美元,而 2026 年為 1,779 億美元,預測期(2026-2031 年)的複合年成長率為 4.3%。

本報告按纖維原料(硬木、軟木、非木漿)、終端用途行業(包裝和瓦楞紙板、紙巾和衛生用品、印刷和書寫用紙、其他)、加工工藝(化學、機械、其他)以及地區(北美、歐洲、亞太、南美、中東和非洲)進行細分。市場預測以價值(美元)和數量兩種形式呈現。

全球木漿市場趨勢與洞察

電子商務主導的瓦楞紙包裝需求

由於瓦楞紙板包裝仍是全球貿易和直接面對消費者配送的主要纖維消耗應用,木漿市場直接受到小包裹數量成長的影響。美國包裝公司(Packaging Corp. of America)報告稱,2024年第三季瓦楞紙板出貨量年增11.1%,反映出儘管再生纖維成本上升,但箱板紙系統的運轉率仍然很高。在中國,2025年1月至8月機制紙和機制紙板總產量達到1.06659億噸,凸顯了儘管國內產能過剩問題令人擔憂,但需求依然持續。為了滿足履約中心不斷變化的需求,買家優先考慮強度更高、壓縮性更強的瓦楞紙板,以減輕包裝重量,從而提升優質牛皮紙漿的價值。同時,模塑纖維包裝作為一次性塑膠的永續替代品正日益受到關注,進一步推動了各類消費品對木漿的需求。這些趨勢凸顯了對先進包裝的日益依賴,以支持電子商務和全球貿易。

新興市場對紙巾和衛生用品的需求不斷成長

木漿市場正受到紙巾和衛生用品需求成長的推動,尤其是在人均消費量遠低於全球平均的地區。在印度,預計到2026年初,紙巾年產能將達到41.7萬噸,而2024年預計為23.8萬至24.8萬噸,但人均消費量仍低於0.5公斤,遠低於5公斤的全球平均水準。同樣,在日本,儘管預計到2024年人均消費量將達到21.5公斤,但由於來自印尼和中國的供應比國內生產更具成本效益,紙巾市場仍然依賴進口。南亞和非洲部分地區的都市化、衛生基礎設施投資以及可支配收入的成長,進一步推動了紙巾和吸收性衛生用品的需求,而這些地區的消費水平仍然低於發展中國家的水平。這種不斷成長的需求凸顯了對短纖維硬木等級產品日益成長的需求,這些產品因其柔軟性、吸水性和成本效益而備受青睞,能夠滿足高級產品和大眾市場產品的需求。

對廢水、空氣排放和漂白進行更嚴格的監管。

隨著各國政府收緊對工業排放和污水管理的監管,木漿生產商遵守環境法規的成本日益增加。升級老舊生產設施以滿足不斷變化的環境標準,往往會佔用原本可用於擴大產能或改善營運的資金,尤其是在老舊造紙廠。這個問題在歐洲尤其突出,因為那裡的監管要求越來越嚴格。歐盟委員會修訂的《工業排放指令》(EU) 2024/1785於2024年8月生效,對工業設施提出了更嚴格的環境績效要求。預計遵守這些更新後的標準將需要對排放氣體控制、廢水處理和監測系統進行額外投資,這將導致成本壓力,並可能限制木漿產業的成長和盈利。

細分市場分析

到2025年,硬木將成為木漿市場的主要驅動力,佔57.3%的市場。這主要歸功於漂白桉木牛皮紙漿在衛生紙、高檔紙和瓦楞紙板等領域的成本效益。雖然漂白硬木牛皮紙漿仍然是大眾市場的主要等級,但隨著生產商將造紙產能轉向更高價值的纖維應用,用於溶解的硬木紙漿的需求也在不斷成長。根據Suzano SA估計,桉木優異的柔軟性和吸水性可能導致2025年,每年多達70萬噸的衛生紙需求從長纖維紙漿轉向短纖維紙漿。儘管有這種轉變,但由於其抗張強度,軟木仍然是瓦楞紙板襯紙和特殊包裝的重要原料,但歐洲和加拿大的成本壓力限制了其供應的柔軟性。

非木漿正成為成長最快的細分市場,預計2026年至2031年將以5.8%的複合年成長率成長,這反映了原料的多樣化。在中國,竹漿計畫正在貴州和四川等省份擴張,以支持生活紙和特種紙的生產。泰森集團正在貴州開發一個項目,計劃每年生產60萬噸生活用紙和竹漿,這反映了對非木漿供應鏈投資的增加。在印度和東南亞,隨著收集和加工系統的改進,以甘蔗渣和秸稈為原料的農業廢棄物紙漿正日益受到關注。儘管與闊葉木漿和針葉木漿相比,非木漿目前在全球紙漿產量中所佔佔有率較小,但其使用正在不斷擴大,以應對原料短缺問題,並在木漿市場中促進本地化和永續的纖維採購。

區域分析

亞太地區佔木漿市場最大佔有率,預計2025年將達42.5%。該地區也有望成為成長最快的市場,2026年至2031年的複合年成長率將達到5.4%。中國在2025年前八個月的機製紙和紙板產量達到1.06659億噸,加上2026年新計畫的獲批,凸顯了中國在該市場的主導地位。此外,印度紙巾產量的快速成長以及日本在2024年840萬噸的穩定需求(主要由衛生和包裝用紙驅動),也顯示該地區在市場中的地位日益重要。

儘管北美市場已趨於成熟,但由於其對包裝、衛生紙和絨毛漿的需求集中,因此仍具有重要的戰略意義。儘管受高成本環境影響,北美地區在2025年因合理化調整而導致產能減少600萬噸,但諸如喬治亞-太平洋公司(喬治亞-Pacific LLC)在阿拉巴馬州的River Cellulose工廠投資8億美元,目標是在2027年實現近100萬噸的產能等投資項目,表明了市場對長期需求的信心。加拿大由於剩餘木片供應減少而面臨成本壓力,而歐洲則透過轉向特種紙和生物基材料來應對這項挑戰。斯道拉恩索公司(Stora Enso Oyj)將其位於奧盧的工廠改造為包裝紙板生產廠,年產能達到75萬噸,這標誌著歐洲正在逐步擺脫對印刷紙的依賴。

南美洲仍是重要的紙漿供應基地,預計巴西將在2024年生產2,550萬噸紙漿。由於制裁限制了俄羅斯的作用,紙漿流向正從歐洲轉向亞洲。在中東,沙烏地阿拉伯的中東紙業公司(MEPCO)正在透過建造一座新的造紙廠來擴大其產能。該廠建成後,預計將使其年紙張產能翻倍,從45萬噸增加至90萬噸。同時,土耳其正崛起成為主要的紙巾供應國。在非洲,衛生意識的提高、都市化以及衛生設施改善計畫正在推動潛在的長期需求。這些區域性的變化凸顯了全球木漿市場相互關聯的演變,而這種演變受到供應鏈調整和消費模式變化的影響。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電子商務推動了對瓦楞紙板包裝的需求。

- 新興市場對紙巾和衛生用品的需求不斷成長

- 由於包裝法規,塑膠製品正被紡織品所取代。

- 擴大南美和亞太地區低成本硬木牛皮紙的生產能力。

- 生物精煉產品的特定產品貨幣化和碳價值獲取

- 利用人工智慧、數位雙胞胎和酵素進行製程最佳化

- 市場限制因素

- 紙漿木材、能源和運輸成本的波動

- 加強對廢水、空氣排放和漂白的監管。

- 履行紡織品可追溯性和森林砍伐方面的實質審查的負擔。

- 中國主導的產能過剩和透過關稅規避貿易

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 以纖維原料為基礎

- 闊葉樹

- 漂白硬木牛皮紙漿

- 未漂白硬木牛皮紙漿

- 用於溶解的硬木漿

- 針葉樹

- 漂白軟木牛皮紙漿

- 未漂白軟木牛皮紙漿

- 絨毛漿

- 非木漿

- 竹漿

- 甘蔗渣漿

- 農業殘餘物漿

- 闊葉樹

- 按最終用途行業分類

- 包裝和紙板

- 瓦楞紙板的襯板和紙芯。

- 折疊式紙盒和紙板

- 模塑纖維包裝

- 紙巾和衛生用品

- 廁所用衛生紙

- 紙巾

- 面紙和餐巾紙

- 女性用衛生用品及成人失禁用品

- 列印/書寫

- 無塗布的免費紙張

- 塗層紙

- 報紙紙張和磨木料

- 特種紙漿和溶解紙漿

- 紡織用溶解漿

- 濾紙和電工紙

- 纖維素衍生物及特殊應用

- 包裝和紙板

- 透過流程

- 化學品

- 工藝

- 亞硫酸鹽

- 機械的

- 熱機械漿

- 化學熱機械漿

- 磨木漿

- 再生纖維漿

- 脫墨紙漿

- 廢棄紙板漿

- 化學品

- 按地區

- 北美洲

- 美國

- 加拿大

- 其他北美國家

- 歐洲

- 德國

- 芬蘭

- 瑞典

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 印尼

- 澳洲

- 韓國

- 其他亞太國家

- 南美洲

- 巴西

- 智利

- 阿根廷

- 其他南美國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Suzano SA(Suzano Holding SA)

- Global Cellulose Fibers

- Mercer International Inc.

- Stora Enso Oyj

- UPM-Kymmene Oyj

- Celulosa Arauco y Constitucion SA(Empresas Copec SA)

- Domtar

- Canfor Corporation

- Metsaliitto Osuuskunta

- Empresas CMPC SA

- Klabin SA

- Oji Holdings Corporation

- Sappi Limited

- Nippon Paper Industries Co., Ltd.

- Sodra Skogsagarna ekonomisk forening

第7章 市場機會與未來展望

According to Mordor Intelligence, the wood pulp market size was valued at USD 168.4 billion in 2025 and is estimated to grow from USD 177.9 billion in 2026 to reach USD 219.7 billion by 2031, at a CAGR of 4.3% during the forecast period (2026-2031).

This report is Segmented by Fiber Source (Hardwood, Softwood, and Non-Wood Fibers), by End-Use Industry (Packaging and Cartonboard, Tissue and Hygiene, Printing and Writing, and More), by Process (Chemical, Mechanical, and More), and by Geography (North America, Europe, Asia-Pacific, South America, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume.

Global Wood Pulp Market Trends and Insights

E-commerce-led corrugated packaging demand

The wood pulp market is directly influenced by parcel growth, as corrugated packaging remains a key fiber-consuming application in global trade and direct-to-consumer delivery. Packaging Corp. of America reported an 11.1% year-over-year increase in corrugated packaging shipments during Q3 2024, reflecting high containerboard system utilization despite elevated recovered fiber costs. In China, machine-made paper and paperboard output totaled 106.659 million metric tons from January to August 2025, underscoring sustained demand even amid concerns about domestic overcapacity. To meet the evolving needs of fulfillment centers, buyers are prioritizing stronger corrugating grades for higher compression performance at reduced package weights, enhancing the value of premium kraft pulp. Simultaneously, molded fiber packaging is gaining traction as a sustainable alternative to single-use plastics, further driving demand for wood pulp across diverse consumer categories. Together, these trends highlight the growing reliance on advanced packaging solutions to support e-commerce and global trade.

Tissue and hygiene demand expansion in emerging markets

The wood pulp market is driven by growing tissue and hygiene demand in regions with per-capita usage significantly below global averages. In India, tissue paper production capacity, at 238,000-248,000 metric tons per year in 2024, is projected to reach 417,000 metric tons per year by early 2026, while per-capita consumption remains under 0.5 kilograms compared to the global average of 5 kilograms. Similarly, Japan's tissue segment, with a per-capita consumption of 21.5 kilograms in 2024, continues to rely on imports due to cost advantages of supply from Indonesia and China over local production. Rising urbanization, sanitation investments, and disposable income growth in South Asia and parts of Africa further bolster demand for tissue and absorbent hygiene products, which are still developing from a low base. This expanding demand underscores the preference for short-fiber hardwood grades, valued for their softness, absorbency, and cost efficiency, aligning with the needs of both premium and mass-market products.

Tightening wastewater, air emissions, and bleaching compliance

Environmental compliance is becoming increasingly costly for wood pulp producers as governments enforce stricter regulations on industrial emissions and wastewater management. Upgrading aging production facilities to meet these evolving environmental standards often diverts capital from capacity expansion and operational improvements, particularly for older mills. This issue is notably pronounced in Europe, where regulatory demands are intensifying. The European Commission's revised Industrial Emissions Directive (EU) 2024/1785, which came into effect in August 2024, imposes more stringent environmental performance requirements on industrial facilities. Adhering to these updated standards is anticipated to necessitate additional investments in emissions control, wastewater treatment, and monitoring systems, thereby creating cost pressures that could limit growth and profitability within the wood pulp industry.

Other drivers and restraints analyzed in the detailed report include:

- Plastic-to-fiber substitution from packaging regulation

- Artificial intelligence, digital twins, and enzyme-assisted process optimization

- Fiber traceability and deforestation due diligence compliance burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardwood dominated the wood pulp market with a 57.3% share in 2025, driven by the cost efficiency of bleached eucalyptus kraft grades used in tissue, fine paper, and folding carton applications. Bleached hardwood kraft pulp remains the primary volume grade, while dissolving hardwood pulp is gaining traction as producers shift paper-grade capacity toward higher-value textile applications. Suzano S.A. estimated that up to 700,000 metric tons of tissue demand could transition annually from long fiber to short fiber in 2025, as eucalyptus demonstrated superior softness and absorption. Despite this shift, softwood remains critical for corrugated liner and specialty packaging due to its tensile strength, though cost pressures in Europe and Canada are limiting its supply flexibility.

Non-wood fibers are emerging as the fastest-growing segment, with a projected CAGR of 5.8% for 2026-2031, reflecting diversification in furnish options. In China, bamboo pulp projects in provinces such as Guizhou and Sichuan are expanding to support the production of tissue and specialty paper. Taison Group is developing a 600,000 metric ton per year integrated tissue paper and bamboo pulp project in Guizhou Province, reflecting increased investment in non-wood fiber supply chains. In India and Southeast Asia, agricultural residue pulp derived from bagasse and straw is gaining prominence as collection and processing systems improve. Although non-wood fibers currently represent a smaller portion of global pulp production compared to hardwood and softwood, they are increasingly being utilized to address raw material constraints and promote localized, sustainable fiber sourcing within the wood pulp market.

Geography Analysis

The Asia-Pacific region holds the largest share of the wood pulp market, accounting for 42.5% in 2025. It is also projected to be the fastest-growing market, with a CAGR of 5.4% from 2026 to 2031. China's production of 106.659 million metric tons of machine-made paper and paperboard during the first eight months of 2025, along with the approval of new projects in 2026, emphasizes its market leadership. Additionally, India's rapid growth in tissue production and Japan's stable demand of 8.4 million metric tons in 2024, primarily driven by hygiene and packaging grades, further illustrate the region's expanding significance in the market.

North America, while mature, remains strategically relevant with demand concentrated on packaging, tissue, and fluff pulp. Despite a 6 million metric ton capacity reduction in 2025 due to rationalization in a high-cost environment, investments such as Georgia-Pacific LLC's USD 800 million upgrade to its Alabama River Cellulose mill, targeting nearly 1 million metric tons by 2027, signal confidence in long-term demand. Canada faces cost pressures from reduced residual chip supply, while Europe adapts through specialty grades and biomaterials. Stora Enso Oyj's Oulu mill conversion to 750,000 metric tons of packaging board exemplifies Europe's shift away from graphic paper.

South America remains a critical supply hub, with Brazil producing 25.5 million metric tons of pulp in 2024. Russia's constrained role due to sanctions has redirected pulp flows from Europe to Asia. In the Middle East, Saudi Arabia's Middle East Paper Company (MEPCO) is expanding its production capacity by constructing a new paper mill. This facility is projected to double the annual paper production capacity from 450,000 metric tons to 900,000 metric tons upon completion, while Turkey emerges as a growing tissue supplier. Africa's rising hygiene awareness, urbanization, and sanitation programs drive long-term demand potential. Together, these regional shifts underline the interconnected evolution of the global wood pulp market, shaped by supply chain adjustments and changing consumption patterns.

- Suzano S.A. (Suzano Holding S.A.)

- Global Cellulose Fibers

- Mercer International Inc.

- Stora Enso Oyj

- UPM-Kymmene Oyj

- Celulosa Arauco y Constitucion S.A. (Empresas Copec S.A.)

- Domtar

- Canfor Corporation

- Metsaliitto Osuuskunta

- Empresas CMPC S.A.

- Klabin S.A.

- Oji Holdings Corporation

- Sappi Limited

- Nippon Paper Industries Co., Ltd.

- Sodra Skogsagarna ekonomisk forening

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce-led corrugated packaging demand

- 4.2.2 Tissue and hygiene demand expansion in emerging markets

- 4.2.3 Plastic-to-fiber substitution from packaging regulation

- 4.2.4 Low-cost hardwood kraft capacity ramp-up in South America and Asia-Pacific

- 4.2.5 Biorefinery co-product monetization and carbon-value capture

- 4.2.6 Artificial intelligence, digital twins, and enzyme-assisted process optimization

- 4.3 Market Restraints

- 4.3.1 Pulpwood, energy, and freight cost volatility

- 4.3.2 Tightening wastewater, air emissions, and bleaching compliance

- 4.3.3 Fiber traceability and deforestation due-diligence compliance burden

- 4.3.4 China-led capacity overhang and tariff-driven trade diversion

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Fiber Source

- 5.1.1 Hardwood

- 5.1.1.1 Bleached Hardwood Kraft Pulp

- 5.1.1.2 Unbleached Hardwood Kraft Pulp

- 5.1.1.3 Dissolving Hardwood Pulp

- 5.1.2 Softwood

- 5.1.2.1 Bleached Softwood Kraft Pulp

- 5.1.2.2 Unbleached Softwood Kraft Pulp

- 5.1.2.3 Fluff Pulp

- 5.1.3 Non-wood Fibers

- 5.1.3.1 Bamboo Pulp

- 5.1.3.2 Bagasse Pulp

- 5.1.3.3 Agricultural Residue Pulp

- 5.1.1 Hardwood

- 5.2 By End-use Industry

- 5.2.1 Packaging and Cartonboard

- 5.2.1.1 Corrugated Linerboard and Medium

- 5.2.1.2 Folding Cartons and Boxboard

- 5.2.1.3 Molded Fiber Packaging

- 5.2.2 Tissue and Hygiene

- 5.2.2.1 Bath Tissue

- 5.2.2.2 Paper Towels

- 5.2.2.3 Facial Tissue and Napkins

- 5.2.2.4 Feminine Hygiene and Adult Incontinence

- 5.2.3 Printing and Writing

- 5.2.3.1 Uncoated Freesheet

- 5.2.3.2 Coated Paper

- 5.2.3.3 Newsprint and Groundwood Grades

- 5.2.4 Specialty and Dissolving Pulp

- 5.2.4.1 Textile-grade Dissolving Pulp

- 5.2.4.2 Filter and Electrical Papers

- 5.2.4.3 Cellulose Derivatives and Specialty Applications

- 5.2.1 Packaging and Cartonboard

- 5.3 By Process

- 5.3.1 Chemical

- 5.3.1.1 Kraft

- 5.3.1.2 Sulfite

- 5.3.2 Mechanical

- 5.3.2.1 Thermomechanical Pulp

- 5.3.2.2 Chemi-thermomechanical Pulp

- 5.3.2.3 Groundwood Pulp

- 5.3.3 Recycled Fiber Pulp

- 5.3.3.1 Deinked Pulp

- 5.3.3.2 Old Corrugated Container Pulp

- 5.3.1 Chemical

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 Finland

- 5.4.2.3 Sweden

- 5.4.2.4 Russia

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Indonesia

- 5.4.3.5 Australia

- 5.4.3.6 South Korea

- 5.4.3.7 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Chile

- 5.4.4.3 Argentina

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Turkey

- 5.4.5.4 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Egypt

- 5.4.6.3 Rest of Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Suzano S.A. (Suzano Holding S.A.)

- 6.4.2 Global Cellulose Fibers

- 6.4.3 Mercer International Inc.

- 6.4.4 Stora Enso Oyj

- 6.4.5 UPM-Kymmene Oyj

- 6.4.6 Celulosa Arauco y Constitucion S.A. (Empresas Copec S.A.)

- 6.4.7 Domtar

- 6.4.8 Canfor Corporation

- 6.4.9 Metsaliitto Osuuskunta

- 6.4.10 Empresas CMPC S.A.

- 6.4.11 Klabin S.A.

- 6.4.12 Oji Holdings Corporation

- 6.4.13 Sappi Limited

- 6.4.14 Nippon Paper Industries Co., Ltd.

- 6.4.15 Sodra Skogsagarna ekonomisk forening

7 Market Opportunities and Future Outlook

漂白桉樹牛皮紙漿:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)未漂白牛皮紙漿:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)漂白針葉樹牛皮紙漿:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)

漂白桉樹牛皮紙漿:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)未漂白牛皮紙漿:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)漂白針葉樹牛皮紙漿:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031) 漂白桉樹牛皮紙漿市場:依等級、產品形式、應用、通路,全球預測(2026-2032年)全球漂白硬木牛皮紙漿市場(按漂白技術、等級、紙漿形態、應用和分銷管道分類)預測(2026-2032年)北方漂白軟木牛皮紙市場按產品等級、認證、應用、最終用途和分銷管道分類 - 全球預測(2026-2032 年)漂白軟木牛皮紙市場按等級、應用、終端用戶產業和銷售管道,全球預測(2026-2032年)

漂白桉樹牛皮紙漿市場:依等級、產品形式、應用、通路,全球預測(2026-2032年)全球漂白硬木牛皮紙漿市場(按漂白技術、等級、紙漿形態、應用和分銷管道分類)預測(2026-2032年)北方漂白軟木牛皮紙市場按產品等級、認證、應用、最終用途和分銷管道分類 - 全球預測(2026-2032 年)漂白軟木牛皮紙市場按等級、應用、終端用戶產業和銷售管道,全球預測(2026-2032年) 日本木漿市場規模、佔有率、趨勢及預測(按類型、等級、最終用途行業和地區分類),2026-2034年

日本木漿市場規模、佔有率、趨勢及預測(按類型、等級、最終用途行業和地區分類),2026-2034年 木漿市場規模、佔有率和成長分析(按類型、製造流程、最終用途產業和地區分類)-2026-2033年產業預測

木漿市場規模、佔有率和成長分析(按類型、製造流程、最終用途產業和地區分類)-2026-2033年產業預測 漂白尤加利牛皮紙漿市場:全球2025-2029年

漂白尤加利牛皮紙漿市場:全球2025-2029年