|

市場調查報告書

商品編碼

2065556

石油天然氣產業企業資源計畫 (ERP):市場佔有率分析、產業趨勢與統計、成長預測 (2026-2031)Oil And Gas Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

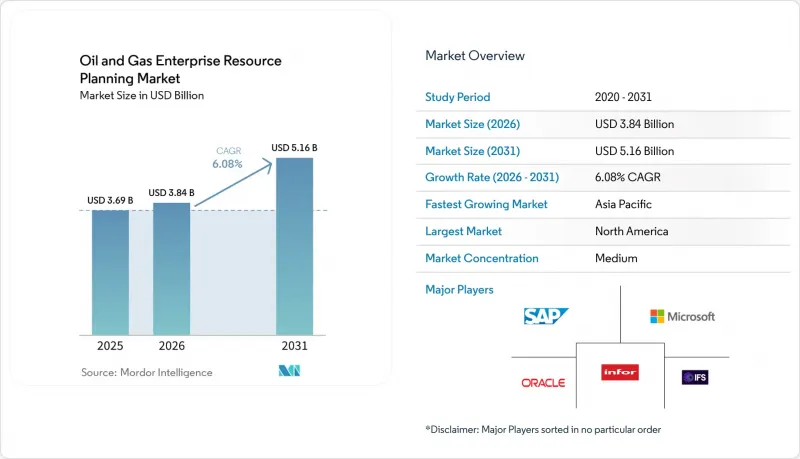

根據 Mordor Intelligence 預測,石油和天然氣行業的企業資源規劃 (ERP) 市場規模預計將在 2025 年達到 36.9 億美元,2026 年達到 38.4 億美元,到 2031 年達到 51.6 億美元,2026 年至 2031 年的複合年成長率為 6.08%。

本報告按組件(財務管理模組、資產管理模組、供應鏈管理模組及其他組件)、部署方式(雲端、本地部署、混合部署)、企業規模(中小企業、大型企業)、應用領域(上游工程、中游、下游、油田服務)和地區進行細分。市場預測以美元計價。

全球石油與天然氣產業ERP市場趨勢與分析

擴大雲端ERP解決方案的採用

隨著超大規模資料中心業者推出區域資料中心和產業認證的安全框架,預計到2025年,雲端將佔據石油和天然氣產業ERP市場62.10%的佔有率。 S-OIL將14個傳統模組整合到一個雲實例中,將其月末結算週期從12天縮短至5天。同時,沙迦國家石油公司將其財務和採購工作負載遷移到公共雲端,同時保留了本地生產資料。這種混合成長模式的複合年成長率高達13.10%,顯示營運商傾向於將企業功能遷移到彈性基礎設施,同時保留本地即時SCADA資料流。這一趨勢正在推動基於使用量的收費模式,該模式可為中小企業減少高達60%的初始投資。沙烏地阿拉伯和阿拉伯聯合大公國的資料居住保障進一步加速了這項轉型。

人工智慧驅動的預測性維護的興起

由於上游業者每次意外停機都會損失約3,800萬美元,預測性維護在短期內可提供最高的投資報酬率。整合到ERP資產管理模組中的分析套件可處理振動和壓力數據,提前30至45天預測故障,從而能夠在計劃的檢修期內進行維修。據阿布達比一家早期採用者稱,將採購與即時生產計畫同步,使庫存持有成本降低了15%。邊緣運算將演算法直接部署到井口,無需網路升級即可實現毫秒延遲。供應商現在將生成工具捆綁在一起,這些工具可以讀取維護日誌、自動生成工單並調度技術人員,從而將平均維修時間(MTTR)縮短了五分之一以上。

高昂的初始成本和轉換成本

總擁有成本 (TCO) 從 12 用戶雲端部署的 5 萬美元到跨國公司上游、中游和下游業務系統更換的 5,000 萬美元以上不等。遷移數十年的測井資料和合作夥伴公司記錄可能需要 18 到 24 個月,並可能使預算增加兩位數。由於員工需要適應新的工作流程,營運商也會產生變更管理成本。基於訂閱的許可將支出從資本支出轉移到營運預算,但即使對於中型生產商而言,多年合約的費用也可能超過每年 50 萬美元。當商品價格下跌時,這些經濟因素會減緩升級速度。

細分市場分析

資產管理模組預計在2025年佔總收入的29.40%。這主要是由於海上設施停工可能導致生產中斷數週,進而引發不可抗力罰款。隨著營運商安裝更多感測器並將即時數據輸入人工智慧引擎,與此模組相關的油氣產業ERP市場規模預計將穩定成長。能夠將自動化工單和財務日記帳分錄結合的供應商正被那些旨在實現整合報告的生產商迅速採用。相較之下,專案管理模組的複合年成長率(CAGR)為11.80%,這主要得益於合資鑽井專案中對精細成本追蹤的需求。

專案管理日益受到關注,尤其是在複雜的資本項目和深海盆地的合作夥伴配置方面。供應鏈管理對於管道、鑽井液和關鍵備件仍然至關重要,但由於許多公司已經最佳化了採購週期,因此其成長速度正在放緩。財務管理仍是基礎領域,但預算編制正轉向環境、社會和治理(ESG)以及預測分析附加元件。在安全認證續約要求嚴格的市場中,人力資本管理的重要性日益凸顯。

到2025年,雲端採用將佔石油和天然氣產業ERP市場佔有率的62.10%,但混合模式將以13.10%的複合年成長率實現最快成長。海灣國家的營運商正在將用於生產數據的公共雲端與用於企業功能的公共叢集相結合,以遵守當地法律並確保突發容量。延遲要求也是推動混合模式採用的重要因素,因為自動化井控流程要求往返時間小於50毫秒。石油和天然氣產業的本地部署解決方案市場規模持續萎縮,主要在受制裁地區和通訊基礎設施有限的地區仍然存在。

在混合環境中,嚴格的主資料管治至關重要,因為油井識別碼和供應商記錄的不一致會影響整合報告的準確性。企業通常會在中介軟體和 API 閘道上投入 20 萬至 50 萬美元來同步記錄。雖然這會增加複雜性,但該模型具有很高的彈性,因為它允許在故障或維護期間將工作負載在本地節點和雲端節點之間切換。

區域分析

基於對二疊紀盆地頁岩油氣生產和墨西哥灣深海開發的投資,預計到2025年,北美仍將維持44.90%的市場佔有率。美國證券交易委員會(SEC)的氣候變遷資訊揭露法規正在推動對碳排放綜合報告的需求成長,營運商正在整合企業資源計畫(ERP)系統和排放感測器以滿足審計期限要求。一家加拿大油砂公司正在添加客製化模組,以整合來自開採點和煉油廠的數據,而一家墨西哥服務公司則表示,透過對舊有系統進行現代化改造,其正常運作得到了提升。

亞太地區是成長最快的地區,預計到2031年複合年成長率將達到11.30%。中國國有石油公司正在升級其企業資源計畫(ERP)系統,將液化天然氣(LNG)接收站與長期銷售合約連接起來。印度一家上游營運商正在將克里希納-戈達瓦里深海區塊的合資帳簿數位化,以符合印度油氣總局的電子申報要求。一家澳洲LNG出口商正在利用ERP系統監控價值數十億美元的工程里程碑。

在中東,隨著大型本土企業多元化經營並與本地雲端服務供應商合作,ERP 的採用正在加速。沙烏地阿拉伯的資料主權法強制供應商將其系統託管在國內,而阿布達比國家石油公司 (ADNOC) 正在其 SAP 環境中部署數百種人工智慧工具。在歐洲,重點是改造北海棕地資產,這些資產仍運作著幾十年前的 SCADA 系統。非洲新興產油國傾向於使用雲端技術以避免巨額資本投資,但有限的近海頻寬導致即時複製出現延遲。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 將資產管理與財務管理結合,以提高營運效率

- 擴大雲端ERP解決方案的採用

- 加強石油和天然氣行業的監管和合規要求

- 人工智慧驅動的預測性維護模組的興起正在減少意外停機時間。

- 複雜夥伴關係模式下合資會計自動化的興起

- ERP套件中整合ESG和碳排放報告功能的需求

- 市場限制因素

- 高昂的初始設定成本和轉換成本

- 雲端採用中的資料安全和主權問題

- 石油和天然氣產業數位轉型中缺乏產業專用的ERP人員

- 將遺留生產系統整合到棕地資產中的複雜性

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章:預測市場規模與成長率

- 按組件

- 財務管理模組

- 資產管理模組

- 供應鏈管理模組

- 專案管理模組

- 人力資本管理模組

- 其他規則

- 透過部署方法

- 雲

- 現場

- 混合

- 按公司規模

- 小型企業

- 大公司

- 透過使用

- 上游工程

- 中游過程

- 下游產業

- 油田服務

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 奈及利亞

- 南非

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Infor, Inc.

- IFS AB

- Epicor Software Corporation

- Deltek, Inc.

- Enertia Software, Inc.

- Quorum Business Solutions, LLC

- P2 Energy Solutions, Inc.

- Unit4 NV

- Acumatica, Inc.

- Odoo SA

- Sage Group plc

- Ramco Systems Limited

- QAD Inc.

- Workday, Inc.

- ABB Ltd

- Honeywell International Inc.

- Siemens AG

第7章 市場機會與未來展望

According to Mordor Intelligence, the oil and gas ERP market size is projected to be USD 3.69 billion in 2025, USD 3.84 billion in 2026, and reach USD 5.16 billion by 2031, growing at a CAGR of 6.08% from 2026 to 2031.

This report is Segmented by Component (Financial Management Module, Asset Management Module, Supply Chain Management Module, and Other Components), Deployment Mode (Cloud, On-Premise, and Hybrid), Enterprise Size (Small and Medium Enterprises and Large Enterprises), Application (Upstream, Midstream, Downstream, and Oilfield Services), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Oil And Gas Enterprise Resource Planning Market Trends and Insights

Growing Adoption Of Cloud-Based ERP Solutions

Cloud captured 62.10% of the oil and gas ERP market in 2025 after hyperscalers launched region-specific data centers and industry-certified security frameworks. S-OIL consolidated 14 legacy modules into a single cloud instance and cut month-end close from 12 days to 5, while Sharjah National Oil Corporation moved finance and procurement workloads to public cloud but retained production data on-premise. Hybrid growth at a 13.10% CAGR shows that operators prefer to keep real-time SCADA streams local and shift corporate functions to elastic infrastructure. This pattern supports consumption-based pricing, which trims upfront capital outlay by up to 60% for smaller firms. Data residency guarantees in Saudi Arabia and the United Arab Emirates further accelerate migrations.

Rise Of AI-Driven Predictive Maintenance

Each unplanned shutdown costs an upstream operator nearly USD 38 million, so predictive maintenance drives the highest near-term ROI. Analytics suites embedded in ERP asset modules process vibration and pressure data to predict failures 30-45 days ahead, enabling repairs during planned turnarounds. Early adopters in Abu Dhabi report a 15% drop in inventory carrying costs after synchronizing procurement with real-time production schedules. Edge computing pushes algorithms to the wellhead, delivering millisecond latency without network upgrades. Vendors now bundle generative tools that read maintenance logs, auto-create work orders, and dispatch technicians, shrinking mean time to repair by more than one-fifth.

High Implementation And Switching Costs

Total cost of ownership ranges from USD 50,000 for a twelve-user cloud roll-out to more than USD 50 million for a multinational swap-out across upstream, midstream, and downstream units. Data migration of decades of well logs and partner records can stretch 18-24 months and lift budgets by double-digit percentages. Operators also absorb change-management expenses as employees adapt to new workflows. Subscription licenses shift spend from capital to operating budgets, yet multi-year commitments can still top USD 500,000 annually for midsize producers. Such economics dampen upgrade velocity when commodity prices soften.

Other drivers and restraints analyzed in the detailed report include:

- Integration Of Asset And Financial Management

- Increasing Regulatory And Compliance Demands

- Data Security And Sovereignty Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Asset Management retained 29.40% of 2025 revenue because offshore outages can halt production for weeks and trigger force majeure penalties. The oil and gas ERP market size tied to this module is set to expand steadily as operators install more sensors and feed real-time data into AI engines. Vendors that pair work-order automation with financial posting see faster adoption among producers striving for integrated reporting. In contrast, the Project Management Module grows at 11.80% CAGR as joint-venture drilling campaigns demand granular cost tracking.

Project Management gains traction in complex capital projects and partner allocations, particularly in deepwater basins. Supply Chain Management continues to matter for tubulars, drilling fluids, and critical spares, yet its growth lags because many firms have already optimized procurement cycles. Financial Management remains foundational, though budgets shift toward ESG and predictive analytics add-ons. Human Capital Management becomes more relevant in markets with strict safety certification renewal requirements.

Cloud deployment held 62.10% of the oil and gas ERP market share in 2025, yet hybrid models posted the fastest growth at a 13.10% CAGR. Operators in Gulf states mix on-premises clusters for production data with public cloud for corporate functions to comply with sovereignty laws and enable burst capacity. Hybrid adoption also stems from latency needs, as automated well-control sequences tolerate less than 50 milliseconds round-trip time. The oil and gas ERP market size for on-premises solutions continues to shrink, surviving mainly in sanctioned regions or areas with limited connectivity.

Hybrid environments require strict master data governance because inconsistent well identifiers or vendor records can corrupt consolidated statements. Firms often invest USD 200,000-500,000 in middleware and API gateways to synchronize records. Despite the added complexity, the model offers resilience because workloads can swing between local and cloud nodes during outages or maintenance windows.

Geography Analysis

North America retained 44.90% share in 2025, anchored by Permian shale output and Gulf of Mexico deepwater spends. SEC climate-disclosure rules drive demand for embedded carbon reporting, and operators integrate ERP with emissions sensors to meet audit timelines. Canadian oil sands firms add custom modules to blend data from mining dispatch and upgrader units, while Mexican service companies cite uptime gains after modernizing legacy systems.

Asia-Pacific is the fastest-growing region, with a 11.30% CAGR through 2031. National oil companies in China are upgrading ERPs to link liquefied natural gas terminals to long-term sales contracts. Indian upstream operators digitize joint venture ledgers for Krishna-Godavari deepwater blocks, complying with the Directorate General of Hydrocarbons' e-submission mandates. Australian liquefied natural gas exporters leverage ERP to monitor billion-dollar engineering milestones.

The Middle East sees rapid adoption as national champions pursue diversification agendas and local-cloud partnerships. Saudi data-sovereignty laws steer vendors toward in-kingdom hosting, while Abu Dhabi National Oil Company rolls out hundreds of AI tools inside its SAP landscape. Europe focuses on modernizing Brownfield North Sea assets where decades-old SCADA systems still run. Emerging African producers prefer cloud to avoid high capital outlays, though limited offshore bandwidth slows real-time replication.

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Infor, Inc.

- IFS AB

- Epicor Software Corporation

- Deltek, Inc.

- Enertia Software, Inc.

- Quorum Business Solutions, LLC

- P2 Energy Solutions, Inc.

- Unit4 N.V.

- Acumatica, Inc.

- Odoo S.A.

- Sage Group plc

- Ramco Systems Limited

- QAD Inc.

- Workday, Inc.

- ABB Ltd

- Honeywell International Inc.

- Siemens AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Integration of Asset and Financial Management to Improve Operational Efficiency

- 4.2.2 Growing Adoption of Cloud-Based ERP Solutions

- 4.2.3 Increasing Regulatory and Compliance Requirements in Oil and Gas Industry

- 4.2.4 Rise of AI-Driven Predictive Maintenance Modules Reducing Unplanned Downtime

- 4.2.5 Emergence of Joint Venture Accounting Automation for Complex Partnership Models

- 4.2.6 Demand for Integrated ESG and Carbon Reporting Capabilities within ERP Suites

- 4.3 Market Restraints

- 4.3.1 High Implementation and Switching Costs

- 4.3.2 Data Security and Sovereignty Concerns for Cloud Deployments

- 4.3.3 Shortage of Domain-Specific ERP Talent for Oil and Gas Digital Transformations

- 4.3.4 Legacy Production Systems Integration Complexity in Brownfield Assets

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.1.1 Bargaining Power of Suppliers

- 4.8.1.2 Bargaining Power of Buyers

- 4.8.1.3 Threat of Substitutes

- 4.8.1.4 Intensity of Competitive Rivalry

- 4.8.1 Threat of New Entrants

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Financial Management Module

- 5.1.2 Asset Management Module

- 5.1.3 Supply Chain Management Module

- 5.1.4 Project Management Module

- 5.1.5 Human Capital Management Module

- 5.1.6 Other Components

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premise

- 5.2.3 Hybrid

- 5.3 By Enterprise Size

- 5.3.1 Small and Medium Enterprises

- 5.3.2 Large Enterprises

- 5.4 By Application

- 5.4.1 Upstream

- 5.4.2 Midstream

- 5.4.3 Downstream

- 5.4.4 Oilfield Services

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 Nigeria

- 5.5.6.2 South Africa

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 Infor, Inc.

- 6.4.5 IFS AB

- 6.4.6 Epicor Software Corporation

- 6.4.7 Deltek, Inc.

- 6.4.8 Enertia Software, Inc.

- 6.4.9 Quorum Business Solutions, LLC

- 6.4.10 P2 Energy Solutions, Inc.

- 6.4.11 Unit4 N.V.

- 6.4.12 Acumatica, Inc.

- 6.4.13 Odoo S.A.

- 6.4.14 Sage Group plc

- 6.4.15 Ramco Systems Limited

- 6.4.16 QAD Inc.

- 6.4.17 Workday, Inc.

- 6.4.18 ABB Ltd

- 6.4.19 Honeywell International Inc.

- 6.4.20 Siemens AG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

企業資源計畫 (ERP) 市場:按組件、ERP 類型、來源類型、部署模式、組織規模和產業分類-2026-2032 年全球市場預測

企業資源計畫 (ERP) 市場:按組件、ERP 類型、來源類型、部署模式、組織規模和產業分類-2026-2032 年全球市場預測 2026-2030年全球企業資源規劃(ERP)軟體市場

2026-2030年全球企業資源規劃(ERP)軟體市場 醫療技術和生物製藥領域醫療設備CMO/CDMO市場:依產品類型、服務類型、器材分類和地區分類教育產業企業資源規劃 (ERP) 軟體市場:按組件、授權類型、部署類型、組織規模和最終用戶分類 - 2026-2032 年全球預測

醫療技術和生物製藥領域醫療設備CMO/CDMO市場:依產品類型、服務類型、器材分類和地區分類教育產業企業資源規劃 (ERP) 軟體市場:按組件、授權類型、部署類型、組織規模和最終用戶分類 - 2026-2032 年全球預測 先進製造市場預測至2034年:按技術、組件、部署模式、應用、產業和地區分類的全球分析

先進製造市場預測至2034年:按技術、組件、部署模式、應用、產業和地區分類的全球分析 2026年全球商業應用與開發市場報告2026年全球尖端材料與製造市場報告

2026年全球商業應用與開發市場報告2026年全球尖端材料與製造市場報告 ERP供應商生態系統市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP客製化服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP整合服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

ERP供應商生態系統市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP客製化服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP整合服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)