|

市場調查報告書

商品編碼

2065554

區塊鏈整合ERP:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Blockchain-Integrated ERP - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

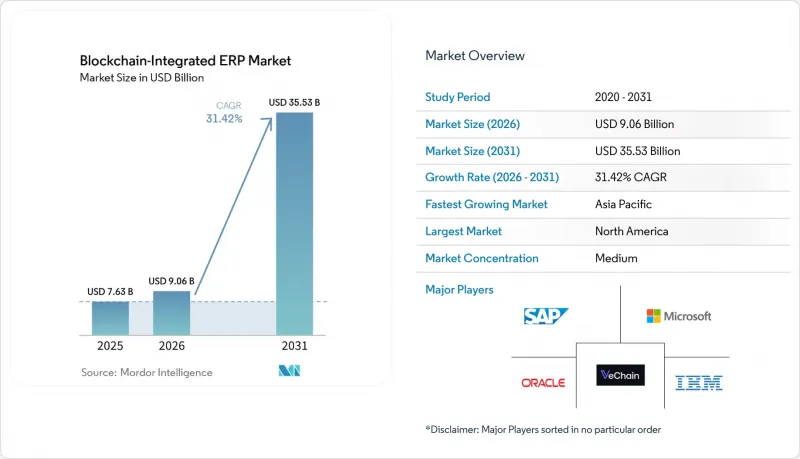

根據 Mordor Intelligence 預測,區塊鏈整合 ERP(企業資源計畫)市場規模將從 2025 年的 76.3 億美元成長到 2026 年的 90.6 億美元,然後在 2031 年達到 355.3 億美元,2026 年至 2031 年的複合年成長率為 31.4%。

本報告按組件(平台、服務)、部署方式(公共雲端、私有雲端、混合雲端)、企業規模(大型企業、中小企業)、應用領域(供應鏈、金融、其他應用)、行業(製造業、零售/電子商務、銀行、金融服務和保險、醫療保健、運輸/物流、政府等)和地區進行細分。市場預測以美元計價。

全球區塊鏈整合ERP市場趨勢與分析

基於區塊鏈的供應鏈融資模組快速擴展

一種基於加密交貨證明的供應鏈融資模組正在取代傳統的應收帳款承購,從而釋放營運資金。 IBM 的實地試驗表明,該模組可將爭議解決時間縮短 68%,並將供應商現金流量的可預測性提高 52%。與微軟的合作將在 2025 年前為中小企業釋放價值 12 億美元的應收帳款,這表明基於區塊鏈的信貸基礎設施可以惠及服務不足的供應商。 ConsenSys 為一家德國汽車零件供應商實現了信用證的自動化開立,從而降低了 30% 的銀行費用。 ISO 22739 標準將為貿易融資智慧合約引入通用語意。這一影響在東南亞和拉丁美洲尤其顯著,因為這些地區的資金籌措最大,供應鏈分散,且替代信貸選擇有限。

高度監管領域對不可篡改的審計追蹤的監管要求

加密貨幣市場的監管要求數位資產公司維護防篡改日誌,如今這項要求也延伸至處理代幣化證券的ERP系統。美國證券交易委員會(SEC)的「加密項目」(Project Crypto)賦予檢查人員對結算帳簿的唯讀進入許可權。經合組織(OECD)的「加密資產報告架構」(Crypto Asset Reporting Framework)要求48個司法管轄區提交標準化的XML交易文件。美國食品藥物管理局(FDA)的試驗計畫要求將藥品批次資訊記錄在區塊鏈上。供應商目前正將鏈下資料儲存與鏈上哈希技術結合,以滿足GDPR的擦除要求和可審計性。由於超過全球銷售額4%的篡改行為將受到處罰,防篡改帳簿已成為金融和生命科學領域不可或缺的基礎。

異質區塊鏈協議與傳統ERP系統之間的互通性問題

根據 Phoenix Strategy Group 發布的 2025 年指南,SAP 表到 Hyperledger 通道映射中的中間件缺陷導致 62% 的專案延遲六個月或更久。 Corda 的 UTXO 模型與以太坊基於帳戶的狀態模型衝突,迫使企業運行獨立的對帳層。 ISO 的 TC 307 旨在製定跨鏈 API,但供應商之間的衝突導致批准延遲。擁有 20 年歷史的財務模組的企業無法證明完全系統替換遷移的合理性,這導致耗時且脆弱的點對點整合、專案延遲以及支援成本增加。由於北美和歐洲的製造商擁有各種各樣的舊有系統,因此首當其衝受到影響。

細分市場分析

平台授權在2025年佔總收入的55.20%,但隨著新的促進因素與受監管的工作流程交織,以及實施複雜性的增加,預計到2031年,服務領域的成長速度將超過授權領域,複合年成長率將達到46.30%。諮詢服務目前佔專案總預算的40-50%,涵蓋架構藍圖、管治策略和零信任設計等領域。由於缺乏人員監控節點效能或修補共識用戶端,託管服務訂閱在中小型企業中廣受歡迎。 IBM、Infosys和Accenture公司正在將監控、金鑰管理和智慧合約稽核納入年度服務協定中。

預計到2029年,區塊鏈整合ERP服務市場收入將超過平台收入。供應商的差異化優勢並非體現在其核心帳本引擎上,而是體現在其行業特定的專業知識上(例如製藥業的序列化、汽車業的品質審核以及銀行業抵押結算)。 SAP、 Oracle和微軟分別透過將其業務技術平台、Fusion Cloud ERP和Dynamics 365整合Hyperledger Fabric、Corda或自有區塊鏈來降低授權解約率。 VeChain和ConsenSys等純區塊鏈公司則透過承諾管治柔軟性和開放原始碼工具集來吸引新客戶。雖然預計在整個預測期內,自動化程式碼產生和人工智慧驅動的測試獵人將減少開發工作量,但在高度監管的行業中,專家諮詢服務仍然至關重要。

預計到2025年,混合雲端將佔總營收的38.10%,複合年成長率(CAGR)為42.10%。企業正在拆分工作負載,將個人資料和財務帳簿放置在企業防火牆內的私有節點上,同時將敏感度較低的事件發佈到公共鍊或聯盟鏈上,以確保生態系統的可見性。公共雲端主要由亞馬遜託管區塊鏈和Azure機密帳本驅動,約佔總營收的35%。由於身分驗證流程中強制要求單一租戶隔離,私有雲端正在國防、醫療保健和政府部門佔據主導地位。

諸如中國的《網路安全法》和歐盟的《一般資料保護規範》(GDPR) 等資料在地化法規正在加速混合部署的進程。 SAP 將於 2026 年 2 月發布的更新將允許客戶跨多個區域複製鏈狀態,確保歐洲的帳單不會離開歐盟。 Oracle 的多重雲端藍圖將使相同的智慧合約能夠在 Oracle 雲端基礎架構、Azure 和 AWS 區域運行,從而降低供應商中斷和廠商鎖定帶來的風險。邊緣原生部署也在穩步推進,工廠在閘道器設備上運行輕量級的 Raft 共識機制,並每小時與雲端錨點同步,以降低生產線延遲。

區域分析

北美地區在金融、科技和醫療保健等早期試點計畫的支持下,預計將引領區塊鏈發展,到2025年將佔全球支出的36.50%。懷俄明州、德拉瓦和德克薩斯州已頒布有利於區塊鏈發展的法律,美國證券交易委員會(SEC)也明確了審計要求。加拿大正在資助一個關於採礦供應鏈的試點項目,追蹤鈷從礦場到電池工廠的整個過程。儘管北美地區在區塊鏈領域主導,但各州法律的差異使得合規變得複雜,並延緩了跨州部署的進程。

亞太地區是成長最快的地區,預計年複合成長率將達到49.20%。中國的區塊鏈服務網路(BSSN)提供低成本的節點託管和跨鏈API。印度電子資訊技術部強制要求政府採購中使用分散式帳本,從而創造了內部需求。新加坡資訊通訊媒體發展局(IMDA)正在津貼貿易數位化,將清關時間從幾天縮短到幾分鐘。韓國的智慧港口計畫透過將非同質化代幣(NFT)與貨櫃掛鉤來降低倉儲費用。

預計到2025年,歐洲將貢獻約28%的收入。歐盟的ViDA指令強制要求即時電子帳單,推動了德國、法國和其他國家的汽車和奢侈品製造地進行區塊鏈升級。 GDPR(一般資料保護規則)和資料主權條款正在促進混合混合雲端的普及。在中東,以阿拉伯聯合大公國和沙烏地阿拉伯的「2030願景」為指導,區塊鏈已成為智慧城市計畫的核心,涵蓋從土地登記到海關清關等各個環節。預計到2025年,非洲和南美洲的收入佔比均不足5%,但它們在匯款管道、農產品原產地追蹤和小額信貸試點計畫等方面的潛力顯而易見。

整體而言,區塊鏈整合ERP市場面臨監管與創新之間的衝突。監管最清晰的地區最初將吸引平台投資,但在地化法規將要求架構具有靈活性,這反過來又會提升專業服務的收入。隨著全球供應鏈圍繞共用帳本進行重組,能夠巧妙利用跨境資料框架的公司將獲得主導市場佔有率。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 基於區塊鏈的供應鏈融資模組快速擴展

- 將後量子密碼技術整合到面向未來的ERP平台中

- 高度監管領域中關於防篡改審計追蹤的監管義務

- 將物聯網和代幣化資產追蹤整合到ERP工作流程中

- 智慧合約在採購自動化領域的廣泛應用。

- 供應商和員工訪問的分散式身分框架的興起

- 市場限制因素

- 異質區塊鏈協議與傳統ERP系統互通性面臨的挑戰

- 缺乏具備區塊鏈技術專業知識的ERP實施人員。

- 跨境鏈上資料儲存位置缺乏全球標準。

- 人們對無需許可的區塊鏈架構中高能耗的擔憂

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章:預測市場規模與成長率

- 按組件

- 平台

- 服務

- 透過部署方法

- 公共雲端

- 私有雲端

- 混合雲端

- 按公司規模

- 大公司

- 小型企業

- 透過使用

- 供應鍊和物流管理

- 財務管理和審計

- 智慧合約自動化

- 識別及存取管理

- 支付系統

- 其他用途

- 按行業

- 製造業

- 零售與電子商務

- 銀行、金融服務和保險業 (BFSI)

- 醫療保健

- 運輸/物流

- 政府

- 能源公用事業

- 其他工業部門

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Oracle Corporation

- SAP SE

- International Business Machines Corporation

- Microsoft Corporation

- VeChain Technology Co., Ltd.

- ConsenSys Software Inc.

- Chainstack Pte. Ltd.

- Monax Industries Limited

- Accenture Plc

- Huawei Technologies Co., Ltd.

- Infosys Limited

- Inetum SA

- Synergix Technologies Pte. Ltd.

- Verizon Communications Inc.

- Wakuu Enterprises Inc.

- Oracle NetSuite LLC

- BlockApps Inc.

- Oracle Corporation(Hyperledger-based ERP)

- Infor, Inc.

- R3 HoldCo LLC

- SAP SE(SAP Business Network Blockchain)

第7章 市場機會與未來展望

According to Mordor Intelligence, the blockchain-integrated ERP market size is expected to grow from USD 7.63 billion in 2025 to USD 9.06 billion in 2026 and is forecast to reach USD 35.53 billion by 2031 at 31.42% CAGR over 2026-2031.

This report is Segmented by Component (Platform and Services), Deployment Mode (Public, Private, and Hybrid Cloud), Enterprise Size (Large Enterprisesand SMEs), Application (Supply Chain, Financial, and Other Applications), Industry Vertical (Manufacturing, Retail and E-Commerce, BFSI, Healthcare, Transportation and Logistics Government, and More), and Geography. Market Forecasts are in Value (USD).

Global Blockchain-Integrated ERP Market Trends and Insights

Rapid Expansion of Blockchain-Enabled Supply Chain Finance Modules

Supply-chain finance modules that release working capital upon cryptographic proof of delivery are displacing traditional factoring. IBM field trials showed dispute-resolution times falling 68% and supplier cash-flow predictability improving 52%. Microsoft partnerships unlocked USD 1.2 billion of invoices for small businesses in 2025, proving blockchain credit rails can reach underserved suppliers. ConsenSys automated letter-of-credit issuance for German automotive suppliers, cutting bank fees 30%. ISO 22739 definitions will bring common semantics to trade-finance smart contracts. Because financing spreads are widest in Southeast Asia and Latin America, the impact is pronounced in regions with fragmented supply chains and scarce alternative credit.

Regulatory Mandates for Immutable Audit Trails in Highly Regulated Sectors

Markets in Crypto-Assets Regulation requires digital-asset firms to maintain tamper-proof logs, which now extend to ERP systems processing tokenized securities. The U.S. SEC's Project Crypto grants examiners read-only access to settlement ledgers. OECD's Crypto-Asset Reporting Framework compels 48 jurisdictions to submit standardized XML transaction files. FDA pilots require pharmaceutical batch events to be written on a chain. Vendors now combine off-chain data stores with on-chain hashes to square GDPR erasure rules with auditability. Penalties exceeding 4% of global revenue have made immutable ledgers a non-negotiable foundation in finance and life sciences.

Interoperability Issues Between Heterogeneous Blockchain Protocols and Legacy ERP Systems

Phoenix Strategy Group's 2025 guide found that 62% of projects slipped by more than 6 months due to middleware failures that map SAP tables to Hyperledger channels. Corda's UTXO model clashes with Ethereum's account-based state, forcing firms to run separate reconciliation layers. ISO's TC 307 aims to draft cross-chain APIs, but vendor rivalries postpone ratification. Companies with 20-year-old finance modules cannot justify rip-and-replace migrations, so brittle point-to-point integrations linger, inflating latency and support bills. North American and European manufacturers feel the pain first because they operate diversified legacy estates.

Other drivers and restraints analyzed in the detailed report include:

- Post-Quantum Cryptography Integration to Future-Proof ERP Platforms

- Growing Adoption of Smart-Contract-Driven Procurement Automation

- Uncertain Global Standards Governing Cross-Border On-Chain Data Residency

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Platform licenses accounted for 55.20% of 2025 revenue, but services are forecast to outgrow licenses at a 46.30% CAGR through 2031 as implementation complexity increases as new drivers intersect regulated workflows. Consulting now swallows 40-50% of total project budgets, covering architecture blueprints, governance policies, and zero-trust design. Managed-services subscriptions are popular among small enterprises that lack staff to monitor node performance and patch consensus clients. IBM, Infosys, and Accenture bundle monitoring, key-management, and smart contract auditing into annual retainers.

The blockchain-integrated ERP services market is projected to eclipse platform revenue by 2029. Vendors differentiate by vertical expertise, pharma serialisation, automotive quality audits, or banking collateral settlements, rather than by core ledger engine. SAP, Oracle, and Microsoft keep license churn low by embedding Hyperledger Fabric, Corda, or proprietary chains into Business Technology Platform, Fusion Cloud ERP, and Dynamics 365, respectively. Pure-play VeChain and ConsenSys win greenfield deals by promising governance flexibility and open-source tooling. Over the forecast horizon, automated code-generation and AI-assisted test harnesses will reduce development hours, yet specialized advisory work will remain essential in highly regulated verticals.

Hybrid cloud commanded 38.10% of 2025 revenue and is on track for a 42.10% CAGR. Enterprises partition workloads so personal data and financial ledgers reside on private nodes behind corporate firewalls, while non-sensitive events post to public or consortium chains for ecosystem visibility. Public cloud attracted roughly 35% of revenue, anchored by Amazon Managed Blockchain and Azure Confidential Ledger. Private cloud is dominant in defense, healthcare, and government because certification processes mandate single-tenant isolation.

Data-localization statutes such as China's Cybersecurity Law and the European Union's GDPR intensify hybrid adoption. SAP's February 2026 updates allow clients to replicate chain state across multiple regions, ensuring that European invoices never leave the bloc. Oracle's multi-cloud blueprint enables identical smart contracts to run across Oracle Cloud Infrastructure, Azure, and AWS regions, hedging against provider outages and vendor lock-in. Edge-native deployments are emerging as factories host lightweight Raft consensus on gateway appliances, synchronizing with cloud anchors hourly to cut latency on production lines.

Geography Analysis

North America led with 36.50% of 2025 spending, buoyed by early pilots in finance, tech, and healthcare. Wyoming, Delaware, and Texas enacted friendly legislation, while SEC guidance clarifies audit expectations. Canada funds mining supply chain pilots, tracking cobalt from pit to battery plant. Despite leadership, fragmented state laws introduce compliance complexity, slowing multi-state rollouts.

Asia-Pacific is the fastest-growing region at a projected 49.20% CAGR. China's Blockchain-based Service Network provides low-cost node hosting and cross-chain APIs. India's Ministry of Electronics and Information Technology mandates the use of distributed ledgers for government procurement, thereby seeding captive demand. Singapore's Infocomm Media Development Authority subsidizes trade digitization that cuts customs clearance times from days to minutes. South Korea's smart-port program attaches non-fungible tokens to containers, reducing demurrage fees.

Europe accounted for about 28% of 2025 revenue. The European Union's ViDA directive makes real-time e-invoicing compulsory, driving blockchain upgrades in automotive and luxury goods manufacturing hubs such as Germany and France. GDPR and data-sovereignty clauses spur adoption of hybrid cloud. The Middle East, spearheaded by the United Arab Emirates and Saudi Arabia's Vision 2030, is placing blockchain at the core of smart-city initiatives, from land registries to customs. Africa and South America each accounted for less than 5% of 2025 revenue, yet remittance corridors, agricultural provenance, and microfinance pilots demonstrate latent potential.

Overall, the blockchain-integrated ERP market faces a regulatory-innovation tension. Regions with the clearest rules attract platform spending first, but localization laws necessitate architectural gymnastics that lift professional-services revenue. Companies capable of navigating cross-border data frameworks will capture an outsized share as global supply networks rewire around shared ledgers.

- Oracle Corporation

- SAP SE

- International Business Machines Corporation

- Microsoft Corporation

- VeChain Technology Co., Ltd.

- ConsenSys Software Inc.

- Chainstack Pte. Ltd.

- Monax Industries Limited

- Accenture Plc

- Huawei Technologies Co., Ltd.

- Infosys Limited

- Inetum S.A.

- Synergix Technologies Pte. Ltd.

- Verizon Communications Inc.

- Wakuu Enterprises Inc.

- Oracle NetSuite LLC

- BlockApps Inc.

- Oracle Corporation (Hyperledger-based ERP)

- Infor, Inc.

- R3 HoldCo LLC

- SAP SE (SAP Business Network Blockchain)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Expansion of Blockchain-Enabled Supply Chain Finance Modules

- 4.2.2 Post-Quantum Cryptography Integration to Future-Proof ERP Platforms

- 4.2.3 Regulatory Mandates for Immutable Audit Trails in Highly Regulated Sectors

- 4.2.4 Convergence of IoT and Tokenized Asset Tracking within ERP Workflows

- 4.2.5 Growing Adoption of Smart-Contract-Driven Procurement Automation

- 4.2.6 Rise of Decentralized Identity Frameworks for Vendor and Employee Access

- 4.3 Market Restraints

- 4.3.1 Interoperability Issues Between Heterogeneous Blockchain Protocols and Legacy ERP Systems

- 4.3.2 Scarcity of Blockchain-Savvy ERP Implementation Talent

- 4.3.3 Uncertain Global Standards Governing Cross-Border On-Chain Data Residency

- 4.3.4 High Energy Consumption Concerns for Permissionless Blockchain Architectures

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Platform

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Public Cloud

- 5.2.2 Private Cloud

- 5.2.3 Hybrid Cloud

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Application

- 5.4.1 Supply Chain and Logistics Management

- 5.4.2 Financial Management and Auditing

- 5.4.3 Smart Contracts Automation

- 5.4.4 Identity and Access Management

- 5.4.5 Payment Systems

- 5.4.6 Other Applications

- 5.5 By Industry Vertical

- 5.5.1 Manufacturing

- 5.5.2 Retail and e-Commerce

- 5.5.3 Banking, Financial Services and Insurance

- 5.5.4 Healthcare

- 5.5.5 Transportation and Logistics

- 5.5.6 Government

- 5.5.7 Energy and Utilities

- 5.5.8 Others Industry Verticals

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Oracle Corporation

- 6.4.2 SAP SE

- 6.4.3 International Business Machines Corporation

- 6.4.4 Microsoft Corporation

- 6.4.5 VeChain Technology Co., Ltd.

- 6.4.6 ConsenSys Software Inc.

- 6.4.7 Chainstack Pte. Ltd.

- 6.4.8 Monax Industries Limited

- 6.4.9 Accenture Plc

- 6.4.10 Huawei Technologies Co., Ltd.

- 6.4.11 Infosys Limited

- 6.4.12 Inetum S.A.

- 6.4.13 Synergix Technologies Pte. Ltd.

- 6.4.14 Verizon Communications Inc.

- 6.4.15 Wakuu Enterprises Inc.

- 6.4.16 Oracle NetSuite LLC

- 6.4.17 BlockApps Inc.

- 6.4.18 Oracle Corporation (Hyperledger-based ERP)

- 6.4.19 Infor, Inc.

- 6.4.20 R3 HoldCo LLC

- 6.4.21 SAP SE (SAP Business Network Blockchain)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

企業資源計畫 (ERP) 市場:按組件、ERP 類型、來源類型、部署模式、組織規模和產業分類-2026-2032 年全球市場預測

企業資源計畫 (ERP) 市場:按組件、ERP 類型、來源類型、部署模式、組織規模和產業分類-2026-2032 年全球市場預測 2026-2030年全球企業資源規劃(ERP)軟體市場

2026-2030年全球企業資源規劃(ERP)軟體市場 醫療技術和生物製藥領域醫療設備CMO/CDMO市場:依產品類型、服務類型、器材分類和地區分類教育產業企業資源規劃 (ERP) 軟體市場:按組件、授權類型、部署類型、組織規模和最終用戶分類 - 2026-2032 年全球預測

醫療技術和生物製藥領域醫療設備CMO/CDMO市場:依產品類型、服務類型、器材分類和地區分類教育產業企業資源規劃 (ERP) 軟體市場:按組件、授權類型、部署類型、組織規模和最終用戶分類 - 2026-2032 年全球預測 先進製造市場預測至2034年:按技術、組件、部署模式、應用、產業和地區分類的全球分析

先進製造市場預測至2034年:按技術、組件、部署模式、應用、產業和地區分類的全球分析 2026年全球商業應用與開發市場報告2026年全球尖端材料與製造市場報告

2026年全球商業應用與開發市場報告2026年全球尖端材料與製造市場報告 ERP供應商生態系統市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP客製化服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP整合服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

ERP供應商生態系統市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP客製化服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP整合服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)