|

市場調查報告書

商品編碼

2065553

政府企業資源規劃(ERP):市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年)Government Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

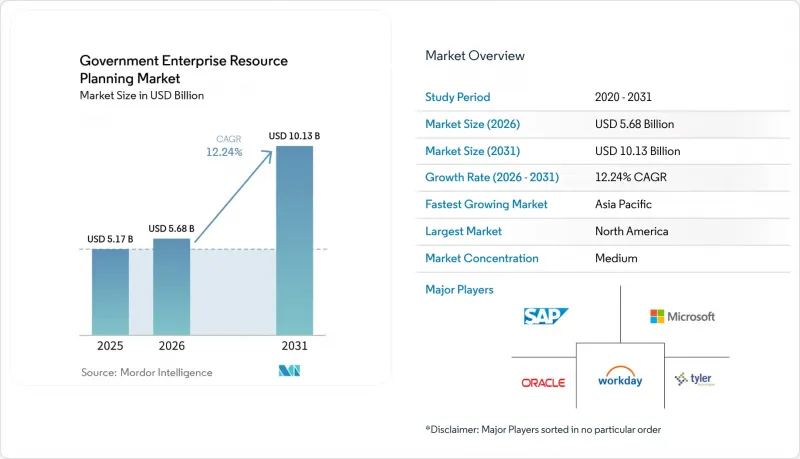

據 Mordor Intelligence 稱,政府企業資源規劃 (ERP) 市場預計將從 2025 年的 51.7 億美元成長到 2026 年的 56.8 億美元,到 2031 年達到 101.3 億美元,預計 2026 年至 2031 年的複合年成長率為 12.24%。

本報告依部署方式(本地部署ERP、雲端ERP、混合ERP)、模組(財務管理、人力資源管理及其他模組)、政府層級(聯邦/國家、州/地方/市級)、元件(軟體、服務)和地區進行細分。市場預測以美元計價。

全球政府企業資源規劃(ERP)市場趨勢與分析

政府強制推行數位轉型

強制推行「雲端優先」策略的指南正在加速淘汰已使用了數十年的大型主機。奧克拉荷馬州的2026-2028年計畫要求所有機構在2028財政年度之前採用雲端架構;田納西州在2026財政年度累計4,700萬美元用於逐步淘汰傳統ERP系統。佛蒙特州正在整合14個不同的帳簿,這種情況與美國數十個州類似,這些州淘汰COBOL系統的速度超過了人才招聘的速度。澳洲於2026年2月推出了預認證供應商小組,將採購前置作業時間從36個月縮短至12個月,並重啟了停滯的專案。這些強制性規定與截止日期和審計處罰相結合,確保了嚴格的預算分配,並在內部IT資源有限的情況下保證了穩定的需求。

透過雲端遷移降低成本

財務模型顯示,與本地部署解決方案相比,五年內的總擁有成本 (TCO) 可降低 30-40%,這使得雲端成為預算緊張的財政部門的理想選擇。 2025 年,英國與 Rackspace Technology 和 Rubrik 合作,建立了一個主權雲,既滿足資料居住法規的要求,又不影響超大規模可擴展性。同年,SAP 在法國部署了一個主權雲,在遵守歐洲隱私法的同時,維持全球支援。羅德島州在估算訂閱費用將比維護其傳統的 PeopleSoft 系統低 35% 後,採用了 Workday。節省下來的資金用於開發一個市民入口網站,該網站提高了用戶滿意度並降低了客服中心成本。

政府採購週期越來越長。

合約簽署週期長達24至48個月,阻礙了現代化改造專案的推進。美國國防部於2025年終止了CIO-SP4契約,迫使各機構重新競標IT服務,導致計畫延長長達18個月。在北卡羅來納州尤寧縣,儘管在2025年發布了兩階段進行的RFP(徵求提案),但預計要到2026年底才能確定供應商。英國公共會計師委員會報告稱,功能性缺陷導致預算超支和運作啟動延遲。這種停滯不前有利於現有供應商,阻礙了新進入者,從而減緩了整體市場的發展勢頭。

細分市場分析

混合型ERP正以14.80%的複合年成長率快速擴張,是所有部署類型中成長最快的。這是因為機構可以將敏感帳簿隔離在本地,同時利用雲端的擴充性進行分析。到2025年,雲端ERP將佔政府企業資源規劃(ERP)市場規模的42%,這主要得益於地方政府缺乏資料中心基礎設施。華盛頓州耗資5.18億美元的「一個華盛頓」計畫就是一個典型的例子,該計畫將薪資核算發放託管在州政府伺服器上,而將採購業務託管在微軟Azure政府雲端平台上。 SAP為法國提供的主權雲表明,類似的模式符合歐洲Schrems II裁決的要求。雖然編配的複雜性曾經是混合部署的障礙,但供應商現在正在整合低延遲連接器來同步子帳簿。隨著政府雲端區域的空氣間隙擴大,本地部署正在減少,但受高安全標準約束的國防和稅務機構除外。

供應商整合正在加速,因為只有擁有雙重程式碼庫的供應商才能贏得大規模競標。 Workday在羅德島州的一份合約包含一項條款,規定如果隱私法規更加嚴格,可以將資料送回其原籍國,這表明即使是優先考慮雲端服務的買家也在尋求退出的柔軟性。澳洲的2026年政策為聯邦政府機構的混合環境設定了預設標準,迫使超大規模資料中心業者資料中心營運商與當地資料中心營運商合作。北美政府機構正受惠於12個新近獲得FedRAMP認證的平台,降低了評估成本。競爭的重點正從純粹的功能轉向架構選擇,能夠實現跨環境無縫工作負載遷移的供應商備受青睞。

預計到2031年,津貼管理市場將以15.20%的複合年成長率成長,在政府機構應對不斷擴大的經濟獎勵策略和基礎設施支出之際,其成長速度將超過所有其他職能領域。到2025年,財務管理將佔政府企業資源規劃(ERP)市場佔有率的34%,為核心帳簿提供支撐,儘管對系統更新的需求正在趨於平穩。美國衛生與公眾服務部(HHS)的撥款解決方案每年處理超過1000億美元的撥款,並在間接成本檢驗和績效審計方面建立了合規標準。 REI Systems的人工智慧評分功能可在津貼發放前減少不當支付,而OpenGov和GrantWorks等供應商則在2025年前增加了基於里程碑的撥款功能。強制性透明度正在推動公民入口網站的發展,使申請人無需工作人員干預即可追蹤津貼發放狀態。

隨著嬰兒潮世代退休導致公共部門人才招聘短缺,人力資本管理模組的需求再次激增。採購套件正在整合法國、比利時和波蘭將於2026年前逐步實施的強制性電子帳單,這使得符合PEPPOL標準變得至關重要。資產管理模組在負責道路、供水系統和公共建築維護的市政部門中越來越受歡迎,因為預測性維護可以降低生命週期成本。隨著供應商將功能捆綁在一起,市民服務入口網站和案例管理工具正在整合到核心ERP系統中,從而擴大了政府企業資源規劃(ERP)的市場規模,而無需單獨採購。

區域分析

2025年,北美在政府企業資源規劃 (ERP) 市場佔據領先地位,銷售額佔比高達37%。這主要得益於聯邦技術現代化基金為聯邦系統升級提供的資金,以及華盛頓州等各州為升級已有40年歷史的系統而投入的5.18億美元。邁阿密市實施Oracle OPAL等地方政府案例表明,透明的儀錶板能夠有效提升信用評級。加拿大數位採納計畫為小型市政機構提供1.5萬加元(約1.17萬美元)的津貼和10萬加元(約7.8萬美元)的貸款,以加速小規模雲端遷移。 FedRAMP在2025年新增了12個認證平台,顯著降低了安全評估成本,並拓展了供應商選擇範圍。

亞太地區預計將成為成長最快的地區,到2031年複合年成長率(CAGR)預計為12.80%,這主要得益於印度的「數位印度2.0」藍圖、中國的政府綜合服務平台以及澳洲將採購週期縮短至12個月的供應商名錄。主權法律強制要求在國內進行託管,這促使全球供應商投資興建本地資料中心。泰國和馬來西亞已發布以澳洲CPS 230為藍本的指導方針,預計也將進行類似的彈性測試。印尼和菲律賓地方政府的數位化進程正在擴大政府企業資源規劃(ERP)解決方案的潛在市場,這兩個國家的寬頻普及率都超過70%。

在歐洲,商業機會與監管摩擦之間正尋求平衡。 Schrems II 裁決、GDPR 以及各國特定的電子帳單要求正迫使政府機構遷移到主權雲端平台。法國和德國已與 Mistral AI 和 SAP 組成聯盟,計劃從 2026 年起實施人工智慧賦能的 ERP 系統,但不包括美國超大規模資料中心業者營運商。比利時將於 2026 年 1 月強制要求 PEPPOL 合規,波蘭的 KSeF 系統將於 2026 年 2 月開始分階段運行,這將迫使 ERP 供應商與國家閘道器整合。英國已完成內政部的過渡,但國家審計署警告稱,如果不加強對供應商的管治,成本削減將難以實現。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 政府促進數位轉型的政策

- 透過雲端遷移降低成本

- 需要加強透明度和課責

- 將人工智慧和分析技術相結合以支援決策。

- 零信任安全要求正在推動ERP升級。

- 追蹤經濟刺激計畫資助的綠色休閒,用於永續發展報告。

- 市場限制因素

- 政府採購週期越來越長。

- 對資料安全和主權的擔憂

- 公部門ERP技能人才短缺

- 政府更迭會擾亂長期ERP計畫。

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章:預測市場規模與成長率

- 透過部署方法

- 本地部署的ERP系統

- 基於雲端的ERP

- 混合型ERP

- 模組特定

- 財務管理

- 人力資本管理

- 採購和供應鏈

- 資產和基礎設施管理

- 津貼管理

- 其他模組

- 按行政級別

- 聯邦/中央政府

- 州政府

- 地方政府/鎮/村

- 按組件

- 軟體

- 服務

- 按地區

- 北美洲

- 美國

- 加拿大

- 其他北美國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 肯亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Tyler Technologies, Inc.

- Infor, Inc.

- Oracle Corporation

- SAP SE

- Microsoft Corporation

- Workday, Inc.

- CGI Inc.

- Unit4 NV

- Accela, Inc.

- Deltek, Inc.

- Axelor SAS

- Adeaca Corp.

- OpenGov, Inc.

- IFS AB

- AccuFund, Inc.

- Appian Corporation

- ECOSIRE Global Solutions Limited

- Strada Global, LLC

- Zoho Corporation Pvt. Ltd.

- Unanet, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the government eRP market size is expected to increase from USD 5.17 billion in 2025 to USD 5.68 billion in 2026 and reach USD 10.13 billion by 2031, growing at a CAGR of 12.24% over 2026-2031.

This report is Segmented by Deployment Mode (On-Premises ERP, Cloud ERP, and Hybrid ERP), Module (Financial Management, Human Capital Management, and Other Modules), Government Level (Federal/National, State/Provincial, and Local/Municipal), Component (Software and Services), and Geography. Market Forecasts are Provided in Terms of Value (USD).

Global Government Enterprise Resource Planning Market Trends and Insights

Digital Transformation Mandates In Government

Mandatory cloud-first directives are making decades-old mainframes prime candidates for replacement. Oklahoma's 2026-2028 plan requires every agency to adopt cloud architectures by fiscal 2028, and Tennessee earmarked USD 47 million for legacy ERP retirement in FY2026. Vermont is consolidating 14 disparate ledgers, mirroring dozens of U.S. states where COBOL retirements outpace hiring pipelines. Australia shortened procurement lead times from 36 to 12 months by launching a pre-qualified vendor panel in February 2026, unlocking backlogged projects. Because these mandates couple deadlines with audit penalties, budget allocations are ring-fenced, ensuring consistent demand even where internal IT capacity is thin.

Cost Savings From Cloud Migration

Financial models show 30-40% lower five-year total cost of ownership versus on-premises, making cloud attractive for budget-pressed treasuries. The United Kingdom partnered with Rackspace Technology and Rubrik in 2025 to build a sovereign cloud that meets data-residency rules without sacrificing hyperscale elasticity. SAP introduced a France-hosted sovereign cloud in 2025 that satisfies European privacy laws while preserving global support. Rhode Island selected Workday after calculating that subscription fees would be 35% lower than maintaining its legacy PeopleSoft stack. Savings free funds to develop citizen-facing portals, enhancing satisfaction scores, and cutting call-center costs.

Lengthy Government Procurement Cycles

Award schedules of 24-48 months erode modernization business cases. The U.S. Department of Defense cancelled the CIO-SP4 vehicle in 2025, forcing agencies to re-compete IT services and adding up to 18 months to timelines. Union County, North Carolina, expects no vendor decision until late 2026, following a two-stage RFP issued in 2025. The U.K. Public Accounts Committee reported capability gaps that fuel overruns and delay go-lives. Such inertia favors incumbents and dissuades new entrants, slowing overall market momentum.

Other drivers and restraints analyzed in the detailed report include:

- Need For Enhanced Transparency And Accountability

- Integration Of AI And Analytics For Decision Support

- Data Security And Sovereignty Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid ERP is advancing at a 14.80% CAGR, the fastest among deployment modes, because agencies can partition sensitive ledgers on-premises while exploiting cloud elasticity for analytics. Cloud ERP held 42% of the government ERP market size in 2025, driven by municipalities that lack data-center infrastructure. Washington State's USD 518 million One Washington program illustrates the approach, hosting payroll on state servers and procurement on Microsoft Azure Government. SAP's France sovereign cloud shows that similar models satisfy European Schrems II rulings. Orchestration complexity once discouraged hybrid rollouts, but vendors now embed low-latency connectors that keep sub-ledgers synchronized. As air-gapped government cloud regions proliferate, on-premises deployments decline except in defense and revenue agencies bound by high-security baselines.

Vendor consolidation is accelerating because only providers with dual codebases can win large solicitations. Rhode Island's Workday contract contains repatriation options if privacy regulations tighten, proof that even cloud-first buyers want exit flexibility. Australia's 2026 policy makes hybrid the default for federal departments, pushing hyperscalers to partner with local data-center operators. North American agencies benefit from 12 newly FedRAMP-authorized platforms that reduce assessment costs. The competitive lens has shifted from pure functionality to architectural optionality, rewarding suppliers that deliver seamless workload mobility across environments.

Grant management is forecast to grow at a 15.20% CAGR through 2031, eclipsing every other functional pillar as agencies administer escalating stimulus and infrastructure disbursements. Financial management retained 34% of the government ERP market share in 2025, anchoring core ledgers, yet replacement demand has plateaued. HHS Grantsolutions handles more than USD 100 billion annually, setting the compliance bar for indirect-cost validation and performance audits. REI Systems' AI scoring cuts improper payments before awards are issued, and vendors such as OpenGov and GrantWorks added milestone-based disbursement features in 2025. Transparency mandates propel citizen portals that let applicants track award status without staff intervention.

Human-capital modules ride a separate wave of demand as baby-boomer retirements squeeze public-sector recruiting pipelines. Procurement suites integrate e-invoicing mandates that France, Belgium, and Poland phase in by 2026, making PEPPOL compatibility non-negotiable. Asset-management modules are gaining traction in cities that maintain roads, water systems, and public buildings, as predictive maintenance lowers lifecycle costs. Citizen-service portals and case-management tools are blending into core ERP as vendors bundle capabilities, expanding the addressable government ERP market size without requiring separate procurement.

Geography Analysis

North America led the government ERP market with a 37% revenue share in 2025, as the Technology Modernization Fund funded federal upgrades and states such as Washington committed USD 518 million to replace 40-year-old systems. Municipal deployments, such as Miami's Oracle OPAL roll-out, underscore how transparent dashboards enhance credit ratings. Canada's Digital Adoption Program issued CAD 15,000 (USD 11,700) grants and CAD 100,000 (USD 78,000) loans to accelerate cloud migration for small governments. FedRAMP added 12 authorized platforms in 2025, slashing security assessment costs and widening supplier pools.

Asia-Pacific exhibits the fastest 12.80% CAGR through 2031, driven by India's Digital India 2.0 roadmap, China's unifying Government Service Platform, and Australia's vendor panel that cuts procurement to 12 months. Sovereignty laws require in-country hosting, spurring local data-center investment by global vendors. Thailand and Malaysia issue guidelines modeled on Australia's CPS 230, anticipating similar resilience tests. Municipal digitization in Indonesia and the Philippines is expanding the addressable government ERP market, where broadband penetration exceeds 70%.

Europe balances opportunity with regulatory friction. Schrems II, GDPR and country-specific e-invoicing mandates push agencies toward sovereign clouds. France and Germany formed a consortium with Mistral AI and SAP to deploy AI-ready ERP starting 2026, excluding U.S. hyperscalers. Belgium enforced PEPPOL compliance in January 2026, and Poland's KSeF system entered phased go-live in February 2026, compelling ERP vendors to integrate national gateways. The U.K. completed its Home Office migration yet the National Audit Office warns savings remain elusive without stronger vendor governance.

- Tyler Technologies, Inc.

- Infor, Inc.

- Oracle Corporation

- SAP SE

- Microsoft Corporation

- Workday, Inc.

- CGI Inc.

- Unit4 N.V.

- Accela, Inc.

- Deltek, Inc.

- Axelor S.A.S.

- Adeaca Corp.

- OpenGov, Inc.

- IFS AB

- AccuFund, Inc.

- Appian Corporation

- ECOSIRE Global Solutions Limited

- Strada Global, LLC

- Zoho Corporation Pvt. Ltd.

- Unanet, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Digital Transformation Mandates in Government

- 4.2.2 Cost Savings from Cloud Migration

- 4.2.3 Need for Enhanced Transparency and Accountability

- 4.2.4 Integration of AI and Analytics for Decision Support

- 4.2.5 Zero-Trust Security Requirements Driving ERP Upgrades

- 4.2.6 Stimulus-Funded Green Ledger Tracking for Sustainability Reporting

- 4.3 Market Restraints

- 4.3.1 Lengthy Government Procurement Cycles

- 4.3.2 Data Security and Sovereignty Concerns

- 4.3.3 Shortage of Public-Sector ERP Skillsets

- 4.3.4 Political Turnover Disrupting Long-Term ERP Projects

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 On-Premises ERP

- 5.1.2 Cloud ERP

- 5.1.3 Hybrid ERP

- 5.2 By Module

- 5.2.1 Financial Management

- 5.2.2 Human Capital Management

- 5.2.3 Procurement and Supply Chain

- 5.2.4 Asset and Infrastructure Management

- 5.2.5 Grant Management

- 5.2.6 Other Modules

- 5.3 By Government Level

- 5.3.1 Federal / National Government

- 5.3.2 State / Provincial Government

- 5.3.3 Local / Municipal Government

- 5.4 By Component

- 5.4.1 Software

- 5.4.2 Services

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Kenya

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Tyler Technologies, Inc.

- 6.4.2 Infor, Inc.

- 6.4.3 Oracle Corporation

- 6.4.4 SAP SE

- 6.4.5 Microsoft Corporation

- 6.4.6 Workday, Inc.

- 6.4.7 CGI Inc.

- 6.4.8 Unit4 N.V.

- 6.4.9 Accela, Inc.

- 6.4.10 Deltek, Inc.

- 6.4.11 Axelor S.A.S.

- 6.4.12 Adeaca Corp.

- 6.4.13 OpenGov, Inc.

- 6.4.14 IFS AB

- 6.4.15 AccuFund, Inc.

- 6.4.16 Appian Corporation

- 6.4.17 ECOSIRE Global Solutions Limited

- 6.4.18 Strada Global, LLC

- 6.4.19 Zoho Corporation Pvt. Ltd.

- 6.4.20 Unanet, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

企業資源計畫 (ERP) 市場:按組件、ERP 類型、來源類型、部署模式、組織規模和產業分類-2026-2032 年全球市場預測

企業資源計畫 (ERP) 市場:按組件、ERP 類型、來源類型、部署模式、組織規模和產業分類-2026-2032 年全球市場預測 2026-2030年全球企業資源規劃(ERP)軟體市場

2026-2030年全球企業資源規劃(ERP)軟體市場 醫療技術和生物製藥領域醫療設備CMO/CDMO市場:依產品類型、服務類型、器材分類和地區分類教育產業企業資源規劃 (ERP) 軟體市場:按組件、授權類型、部署類型、組織規模和最終用戶分類 - 2026-2032 年全球預測

醫療技術和生物製藥領域醫療設備CMO/CDMO市場:依產品類型、服務類型、器材分類和地區分類教育產業企業資源規劃 (ERP) 軟體市場:按組件、授權類型、部署類型、組織規模和最終用戶分類 - 2026-2032 年全球預測 先進製造市場預測至2034年:按技術、組件、部署模式、應用、產業和地區分類的全球分析

先進製造市場預測至2034年:按技術、組件、部署模式、應用、產業和地區分類的全球分析 2026年全球商業應用與開發市場報告2026年全球尖端材料與製造市場報告

2026年全球商業應用與開發市場報告2026年全球尖端材料與製造市場報告 ERP供應商生態系統市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP客製化服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP整合服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

ERP供應商生態系統市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP客製化服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP整合服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)