|

市場調查報告書

商品編碼

2065551

製藥業企業資源規劃(ERP):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Pharmaceutical Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

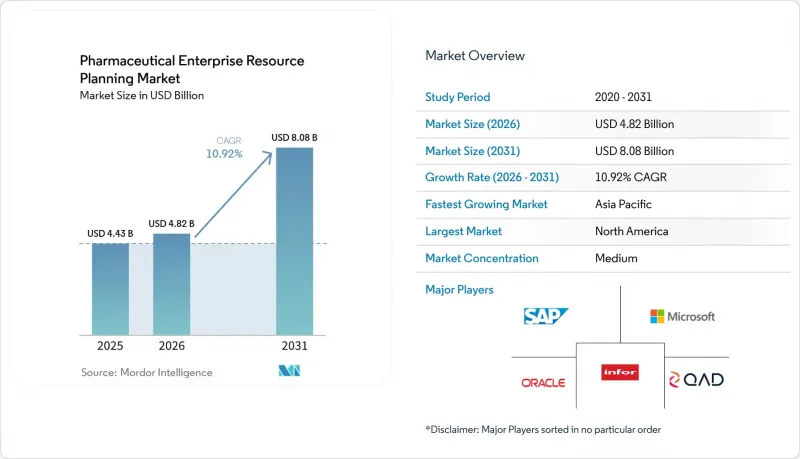

根據 Mordor Intelligence 預測,製藥業企業資源規劃 (ERP) 的市場規模預計將從 2025 年的 44.3 億美元和 2026 年的 48.2 億美元成長到 2031 年的 80.8 億美元,2026 年至 2031 年的年複合成長率(CAGR)率為 10.92%。

本報告按部署方式(雲端ERP、本地部署ERP、混合ERP)、模組(生產管理、品質與合規管理、供應鏈管理等)、組織規模(大型企業、中小企業)、最終用戶(製藥公司、合約生產商等)和地區進行細分。市場預測以美元計價。

全球醫藥企業資源規劃(ERP)市場趨勢與分析

對基於雲端的、經過認證的ERP平台的需求

製藥公司正將工作負載遷移到雲端,以降低資本支出、確保即時批次可見度並縮短驗證週期。 SAP、Oracle 和 Microsoft 已推出預先驗證的生命科學套件,並整合了 GxP 文檔,使企業無需維護本地環境即可符合 21 CFR Part 11 的要求。契約製造組織 (CMO) 更傾向於採用多租戶雲端架構,該架構共用通用品管模組,同時隔離委託方數據,從而實現電子批記錄的快速部署和標準化。然而,中國和俄羅斯的資料居住法規迫使企業採用混合部署模式,將公共雲端上的財務系統與本地生產執行系統結合。

全球序列化的截止日期臨近。

美國《藥品供應鏈安全法案》將於2025年完成分階段實施,屆時將要求製造商、批發商和藥劑師在其ERP系統中整合單元級追蹤溯源功能。歐盟《假藥指令》給予義大利和希臘寬限期至2027年,從而形成一種“雙層環境”,模組化、國別客製化的模板更具優勢。市場對支援區塊鏈的ERP整合方案的需求日益成長,此類方案可透過序列化提供防篡改的審計追蹤,並支援與國家資料庫進行即時檢驗(路透社)。

中小企業CSV成本高昂

對於中小企業而言,電腦系統驗證 (CSV) 的成本可能占到 ERP 專案預算的 30%,並可能導致系統上運作日期延遲長達一年。外部顧問的費用在每小時 150 至 250 美元之間,這無疑會給有限的 IT 預算帶來壓力。儘管供應商會提供共用的驗證文檔,但監管機構堅持認為,合規性的最終責任在於製造商。對於必須滿足每個委託方不同要求的契約製造而言,這項負擔更為沉重。

細分市場分析

到2025年,基於雲端的解決方案將占到收入的62%,預計到2031年,其在醫藥ERP市場的佔有率將以11.80%的複合年成長率成長。混合模式既能滿足限制病患資料傳輸的法規要求,又能利用雲端的擴充性來處理不受GxP約束的功能。到2031年,醫藥雲ERP的市場規模預計將佔據新增投資的大部分。早期採用者報告稱,從本地部署套件遷移後,驗證成本顯著降低。多租戶雲端能夠實現申辦方隔離和快速上線,主導促進契約製造組織(CMO)的採用。

在中國和俄羅斯,由於資料在地化法規依然嚴格,本地部署仍然普遍存在。使用傳統設備的工廠通常缺乏 OPC-UA 連接,這意味著遷移到公共雲端可能需要重新驗證整個生產線,這可能會產生巨額成本。混合架構允許製造商在將財務和人力資源系統遷移到雲端服務的同時,保留其本地製造執行系統 (MES)。提供自動化審計追蹤核對服務的供應商正在將 CSV 週期從 18 個月縮短至 6 個月,從而加速了製藥行業中注重合規性的企業對該技術的採用。

品質和合規性在2025年將佔銷售額的28.40%,反映出對法規的高度重視。這一在醫藥ERP市場佔有率中所佔的比例構成了所有主要實施項目的基礎,尤其是在DSCSA和歐盟FMD要求序列化的地區。生產管理模組協調排產、採購和維護,從而提供跨多站點網路的流程可視性。

隨著創新企業將人工智慧融入其配方設計和臨床試驗流程,研發模組預計將以12.60%的複合年成長率成長。儘管醫藥ERP市場中的研發工具市場規模仍小於品管市場,但由於人工智慧縮短了實驗週期,其成長速度最快。供應鏈模組正受益於區塊鏈的試點部署,以產生防篡改的產品來源資訊;人力資源管理工具則將員工培訓記錄與GxP任務關聯起來,確保只有合格員工才能執行關鍵任務。

區域分析

北美地區在嚴格的藥品供應鏈安全法案 (DSCSA) 法規和以創新為導向的製造業基礎的推動下,預計將引領市場,到 2025 年將佔據 34.90% 的銷售額。美國醫藥 ERP 市場正受益於早期雲端檢驗先導計畫和廣泛的人工智慧實驗。加拿大憑藉其與美國地理位置的接近性,已發展成為生技藥品的契約製造中心,因此跨境批次可視性至關重要。

歐洲保持第二的位置。歐盟的《反假藥指令》強制要求藥品序列化,《企業永續性報告指令》強制要求進行範圍3碳計量。這些法規更傾向於整合式ERP套件而非單一解決方案。 GDPR下的資料居住需求促使企業採用混合架構,將病患資料儲存在本地,並將財務資料遷移到全球雲端。

亞太地區是成長最快的地區,預計到2031年將以每年10.20%的速度成長。印度20億美元的獎勵計畫正幫助當地企業進入需要符合FDA和EMA規定的出口市場。中國15億美元的基礎建設和集中採購改革正推動國內合約生產商(CMO)採用國際GxP標準。日本正在試行應用人工智慧驅動的批次放行分析來應對人手不足。

儘管受宏觀經濟波動影響,南美洲的成長速度有所放緩,但巴西和阿根廷正在選擇性地投資於企業資源規劃(ERP)系統的現代化改造。中東和非洲地區仍在發展中,但其未來前景光明,因為沙烏地阿拉伯和阿拉伯聯合大公國正在建造本地製藥生產設施,以減少對進口的依賴。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 分析的前提條件、市場界定與分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對基於雲端的、檢驗的ERP平台的需求

- 全球更嚴格的序列化期限(DSCSA、歐盟FMD)

- 契約製造組織(CMO)的快速擴張

- 人工智慧驅動的預測品質和批次放行分析

- 政府對數位製藥廠的獎勵措施

- 對端對端 ESG 和碳核算的需求日益成長。

- 市場限制因素

- 中小企業電腦系統檢驗(CSV) 成本高昂

- 缺乏具備製藥業ERP實施專業知識的人員。

- 對公共雲端中的網路安全和資料儲存位置的擔憂

- 整合傳統MES/LIMS系統的複雜性

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章:預測市場規模與成長率

- 透過部署方法

- 基於雲端的ERP

- 本地部署的ERP系統

- 混合型ERP

- 模組特定

- 製造管理

- 品質與合規管理

- 供應鏈管理

- 財務管理

- 銷售與行銷

- 人力資源管理

- 其他模組

- 按組織規模

- 大公司

- 小型企業

- 最終用戶

- 製藥公司

- CMO(藥品契約製造組織)

- 藥品批發商

- 生技公司

- CRO(委外研發機構)

- 按地區

- 北美洲

- 美國

- 加拿大

- 其他北美國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Infor, Inc.

- QAD Inc.

- BatchMaster Software Pvt. Ltd.

- Aptean, Inc.

- Sage Group plc

- Epicor Software Corporation

- SYSPRO(Pty)Ltd.

- IFS AB

- Acumatica, Inc.

- Oracle NetSuite LLC

- Slingshot Enterprise Business Systems, Inc.

- RxERP LLC

- Dexciss Technology Private Limited

- Blue Link Associates Limited

- Deacom, LLC

- Plex Systems, Inc.

- Workday, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the pharmaceutical eRP market size is projected to expand from USD 4.43 billion in 2025 and USD 4.82 billion in 2026 to USD 8.08 billion by 2031, registering a CAGR of 10.92% between 2026 and 2031.

This report is Segmented by Deployment Mode (Cloud-Based ERP, On-Premise ERP, and Hybrid ERP), Module (Manufacturing Management, Quality and Compliance Management, Supply Chain Management, and More), Organization Size (Large Enterprises, Small and Medium Enterprises), End User (Pharmaceutical Manufacturers, Cmos, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Pharmaceutical Enterprise Resource Planning Market Trends and Insights

Demand for Cloud-Based Validated ERP Platforms

Pharmaceutical manufacturers are moving workloads to the cloud to reduce capital expenditure, unlock real-time batch visibility, and cut validation timelines. SAP, Oracle, and Microsoft introduced pre-validated life sciences suites that embed GxP documentation, enabling companies to comply with 21 CFR Part 11 without maintaining on-premises environments. Contract manufacturing organizations prefer multi-tenant cloud architectures that isolate sponsor data yet share common quality modules, enabling faster onboarding and harmonized electronic batch records. However, data-residency rules in China and Russia force hybrid deployments that blend public-cloud financials with on-premise manufacturing execution systems.

Tightening Global Serialization Deadlines

The United States Drug Supply Chain Security Act completed its phased rollout in 2025, requiring manufacturers, wholesalers, and dispensers to integrate unit-level track-and-trace into their ERP systems. The European Union Falsified Medicines Directive granted Italy and Greece extensions until 2027, creating a two-speed environment that favors modular, country-specific templates. Serialization drives demand for blockchain-enabled ERP integrations that provide immutable audit trails and real-time verification against national repositories REUTERS.COM.

High CSV Costs for SMEs

Computer system validation can consume up to 30% of an ERP project budget for small and medium enterprises, extending go-live dates by up to a year. External consultants bill USD 150-250 per hour, straining limited IT budgets. Vendors offer shared validation documentation, yet regulators insist that manufacturers retain ultimate responsibility for compliance. The burden is heavier for contract manufacturers that must satisfy divergent sponsor requirements.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Expansion of Contract Manufacturing Organizations

- AI-Enabled Predictive Quality and Batch-Release Analytics

- Shortage of Pharma-Savvy ERP Implementation Talent

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-based solutions accounted for 62% of revenue in 2025, and this share of the Pharmaceutical ERP market is set to grow at a 11.80% CAGR through 2031. Hybrid models satisfy jurisdictions that restrict patient data movement while unlocking cloud scalability for non-GxP functions. The Pharmaceutical ERP market size for cloud deployments is projected to command the majority of new spend by 2031. Early adopters report significantly lower validation costs after switching from on-premises suites. Contract manufacturing organizations dominate uptake because multi-tenant clouds enable sponsor segregation and rapid onboarding.

On-premises deployments persist in China and Russia, where data localization laws remain strict. Facilities with legacy equipment lack OPC-UA connectivity, so migrating to the public cloud can trigger costly re-validation of entire production lines. Hybrid architectures let manufacturers migrate financials and human resources to cloud services while retaining manufacturing execution on-site. Vendors that automate audit-trail reconciliation shorten CSV cycles from 18 months to six months, accelerating Pharmaceutical ERP market adoption among compliance-focused firms.

Quality and compliance accounted for 28.40% of 2025 revenue, reflecting the regulatory focus. This slice of the Pharmaceutical ERP market share underpins every major deployment, especially where DSCSA and EU FMD demand serialization. Manufacturing management modules orchestrate scheduling, procurement, and maintenance, offering process visibility across multi-site networks.

Research and development modules are expected to grow at a 12.60% CAGR as innovators integrate AI into formulation design and clinical-trial workflows. The Pharmaceutical ERP market for Research and Development tools, while still smaller than the quality management market, is growing fastest because AI shortens experimentation cycles. Supply chain modules benefit from blockchain pilots that create immutable product provenance, and human resources tools map employee training records to GxP tasks, ensuring only qualified staff perform critical operations.

Geography Analysis

North America led with 34.90% of 2025 revenue, driven by stringent DSCSA rules and an innovation-oriented manufacturing base. The Pharmaceutical ERP market size in the United States benefits from early cloud validation pilots and broad AI experimentation. Canada leverages proximity to the United States to position itself as a biologics contract manufacturing hub, making cross-border batch visibility a must-have.

Europe maintains second position. The EU Falsified Medicines Directive mandates serialization, and the Corporate Sustainability Reporting Directive compels Scope 3 carbon accounting. These rules favor integrated ERP suites over point solutions. Data-residency considerations under GDPR encourage hybrid architectures that host patient data locally and move financial data to global clouds.

Asia-Pacific is the fastest-growing region, expected to advance at 10.20% through 2031. India's USD 2 billion incentive propels local firms into export markets that demand FDA and EMA compliance. China's USD 1.5 billion infrastructure push and centralized procurement reforms motivate domestic CMOs to embrace international GxP standards. Japan pilots AI batch-release analytics to offset labor shortages.

South America is growing more slowly due to macroeconomic volatility, though Brazil and Argentina are investing selectively in ERP modernization. The Middle East and Africa remain nascent but promising, as Saudi Arabia and the United Arab Emirates develop local pharma manufacturing to reduce reliance on imports.

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Infor, Inc.

- QAD Inc.

- BatchMaster Software Pvt. Ltd.

- Aptean, Inc.

- Sage Group plc

- Epicor Software Corporation

- SYSPRO (Pty) Ltd.

- IFS AB

- Acumatica, Inc.

- Oracle NetSuite LLC

- Slingshot Enterprise Business Systems, Inc.

- RxERP LLC

- Dexciss Technology Private Limited

- Blue Link Associates Limited

- Deacom, LLC

- Plex Systems, Inc.

- Workday, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition * Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Demand for Cloud-Based Validated ERP Platforms

- 4.2.2 Tightening Global Serialization Deadlines (DSCSA, EU FMD)

- 4.2.3 Rapid Expansion of Contract Manufacturing Organizations

- 4.2.4 AI-Enabled Predictive Quality and Batch-Release Analytics

- 4.2.5 Government Incentives for Digital Pharma Plants

- 4.2.6 Growing Need for End-to-End ESG and Carbon Accounting

- 4.3 Market Restraints

- 4.3.1 High CSV (Computer System Validation) Costs for SMEs

- 4.3.2 Shortage of Pharma-Savvy ERP Implementation Talent

- 4.3.3 Cyber-Security and Data-Residency Concerns in Public Cloud

- 4.3.4 Legacy MES/LIMS Integration Complexities

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Intensity of Competitive Rivalry

- 4.7.2 Threat of New Entrants

- 4.7.3 Threat of Substitutes

- 4.7.4 Bargaining Power of Suppliers

- 4.7.5 Bargaining Power of Buyers

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Cloud-Based ERP

- 5.1.2 On-Premise ERP

- 5.1.3 Hybrid ERP

- 5.2 By Module

- 5.2.1 Manufacturing Management

- 5.2.2 Quality and Compliance Management

- 5.2.3 Supply Chain Management

- 5.2.4 Financial Management

- 5.2.5 Sales and Marketing

- 5.2.6 Human Resources Management

- 5.2.7 Other Modules

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By End User

- 5.4.1 Pharmaceutical Manufacturers

- 5.4.2 Contract Manufacturing Organizations

- 5.4.3 Pharmaceutical Distributors

- 5.4.4 Biotechnology Companies

- 5.4.5 Contract Research Organizations

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 Infor, Inc.

- 6.4.5 QAD Inc.

- 6.4.6 BatchMaster Software Pvt. Ltd.

- 6.4.7 Aptean, Inc.

- 6.4.8 Sage Group plc

- 6.4.9 Epicor Software Corporation

- 6.4.10 SYSPRO (Pty) Ltd.

- 6.4.11 IFS AB

- 6.4.12 Acumatica, Inc.

- 6.4.13 Oracle NetSuite LLC

- 6.4.14 Slingshot Enterprise Business Systems, Inc.

- 6.4.15 RxERP LLC

- 6.4.16 Dexciss Technology Private Limited

- 6.4.17 Blue Link Associates Limited

- 6.4.18 Deacom, LLC

- 6.4.19 Plex Systems, Inc.

- 6.4.20 Workday, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

企業資源計畫 (ERP) 市場:按組件、ERP 類型、來源類型、部署模式、組織規模和產業分類-2026-2032 年全球市場預測

企業資源計畫 (ERP) 市場:按組件、ERP 類型、來源類型、部署模式、組織規模和產業分類-2026-2032 年全球市場預測 2026-2030年全球企業資源規劃(ERP)軟體市場

2026-2030年全球企業資源規劃(ERP)軟體市場 醫療技術和生物製藥領域醫療設備CMO/CDMO市場:依產品類型、服務類型、器材分類和地區分類教育產業企業資源規劃 (ERP) 軟體市場:按組件、授權類型、部署類型、組織規模和最終用戶分類 - 2026-2032 年全球預測

醫療技術和生物製藥領域醫療設備CMO/CDMO市場:依產品類型、服務類型、器材分類和地區分類教育產業企業資源規劃 (ERP) 軟體市場:按組件、授權類型、部署類型、組織規模和最終用戶分類 - 2026-2032 年全球預測 先進製造市場預測至2034年:按技術、組件、部署模式、應用、產業和地區分類的全球分析

先進製造市場預測至2034年:按技術、組件、部署模式、應用、產業和地區分類的全球分析 2026年全球商業應用與開發市場報告2026年全球尖端材料與製造市場報告

2026年全球商業應用與開發市場報告2026年全球尖端材料與製造市場報告 ERP供應商生態系統市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP客製化服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP整合服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

ERP供應商生態系統市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP客製化服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP整合服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)