|

市場調查報告書

商品編碼

2065546

企業資源規劃(ERP)在資產管理的應用:市佔率分析、產業趨勢與統計、成長預測(2026-2031)Asset Management Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

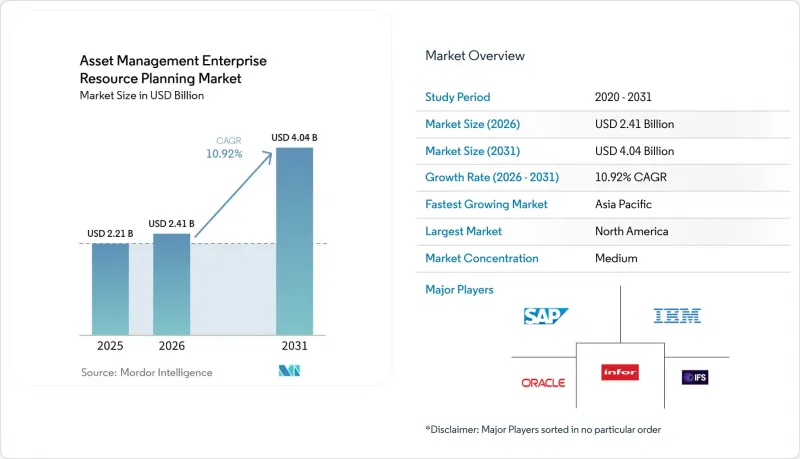

根據 Mordor Intelligence 預測,資產管理企業資源規劃 (ERP) 市場規模將從 2025 年的 22.1 億美元成長到 2026 年的 24.1 億美元,然後在 2031 年達到 40.4 億美元,2026 年至 2031 年的複合成長率為 10.92%。

本報告按部署方式(雲端、本地部署、混合部署)、組織規模(大型企業、中小企業)、產業(製造業、能源與公用事業、醫療保健等)、模組(資產生命週期管理、工單管理、庫存與備件管理等)和地區進行細分。市場預測以美元計價。

全球資產管理企業資源規劃 (ERP) 市場趨勢與分析

快速轉向基於雲端的部署模式

雲端原生套件能夠幫助企業減輕基礎設施負擔、加快功能交付速度,並根據實際使用情況調整成本。到 2027 年,雲端 ERP 支出將轉向人工智慧解決方案,其中將顯著轉向那些將機器學習融入估值和折舊免稅額工作流程的平台。據 NetSuite 稱,混合架構仍然佔據主導地位,88% 的企業在私有雲端中維護敏感帳簿,同時在公共雲端中擴展分析功能。容器化正在主要生產環境中得到應用,提高了資產模組在雲端之間的可移植性,並簡化了災害復原。然而,意外成本導致少數企業將工作負載遷移回本地,凸顯了財務營運 (FinOps)管治和自動化成本管理的重要性。總體而言,雲端採用的加速推動了物聯網 (IoT) 的快速整合和預測分析,這是企業資源規劃 (ERP) 資產管理市場最大的成長要素。

擴大物聯網感測器的應用,以實現預測性維護

IEEE 的一項案例研究表明,將感測器與 ERP 系統整合可以實現維護請求處理和故障閾值警報的自動化,從而減少人工輸入並實現預測性工作流程。公用事業公司是這項技術的早期採用者。 DNV 的 Cascade 將 SCADA 歷史資料與資產評分系統整合,而 SAS 分析系統則可偵測渦輪機異常情況,從而實現主動調度。安全仍然是一個挑戰。大多數物聯網設備缺乏代理,並且在出廠時預先配置了預設憑證,這迫使企業依賴微隔離和網路偵測來保護 ERP 介面。隨著覆蓋範圍的逐步完善,預測性維護將在企業資源規劃 (ERP) 資產管理市場中繼續超越其他模組。

與傳統ERP系統整合相關的初始成本很高。

數十年的自訂程式碼和缺乏文件的介面使得現代化改造成本高昂。流程挖掘工具能夠揭示隱藏的低效率環節。例如,它們可能會發現生產狀態比記錄滯後兩天,或者材料清單(BOM) 中存在錯誤的切換規則,從而凸顯出在運作前修正主資料的必要性。未能採取此步驟的組織可能會自動化不當的工作流程,從而潛在地損害其企業資源計畫 (ERP) 系統實施的投資報酬率。

細分市場分析

到2025年,雲端採用將佔企業資源規劃(ERP)市場佔有率的48.50%,預計到2031年,該細分市場將以12.30%的複合年成長率成長。企業傾向於選擇供應商管理的基礎設施和快速的功能發布,而容器化微服務則提高了混合策略的可移植性。隨著人工智慧驅動的服務將維護分析和碳核算與運算能力更緊密地結合起來,與雲端採用相關的企業資源規劃(ERP)市場規模預計將會擴大。

在延遲和資料主權要求至關重要的行業,尤其是國防和監管嚴格的公用事業領域,本地部署解決方案仍然佔據主導地位。目前,88% 的企業採用混合模式,透過在私有雲端中維護敏感帳本並利用公共雲端擴展分析能力來平衡這些限制。由於 54% 的企業未能準確追蹤其雲端支出,這可能會抵消硬體減少帶來的成本節約,因此財務營運 (FinOps) 安全措施正逐漸成為標準。整體而言,部署選擇越來越受到監管和延遲因素的驅動,而非技術能力的差異。

預計到2025年,大型企業將佔銷售額的60.30%,而中小企業(SME)正以11.60%的複合年成長率(CAGR)快速成長,這得益於供應商付費使用制、低程式碼模板和託管服務。中小企業企業資源規劃(ERP)解決方案的市場規模將受惠於實施難度降低和資本支出減少。

資源限制仍然是中小企業面臨的一大挑戰,但隨著整合財務、供應鏈和資產管理模組並具備自動化主資料清洗功能的SaaS套件的出現,功能上的差距正在縮小。在亞太地區和南美洲,政府對雲端優先解決方案和包含外匯對沖功能的訂閱計畫的獎勵,進一步降低了採用門檻。隨著付費使用制的成熟,預計在預測期內,中小企業將推動需求成長的更大比例。

區域分析

北美地區憑藉著成熟的雲端基礎設施和早期採用人工智慧驅動的分析技術,在2025年貢獻了33.40%的收入。在2027年截止日期前從SAP ECC遷移到S/4HANA正在加速交易,但資料清理的複雜性卻讓進度更加緊張。隨著歐盟《網路彈性法案》的域外適用,美國供應商正積極改進其產品,例如整合漏洞報告和SBOM功能,以維持其在歐洲市場的准入。

亞太地區以11.40%的複合年成長率成為成長最快的地區,這主要得益於中國和印度的大規模基礎設施投資,以及超過5,000億美元的私人投資推動半導體產能擴張。東南亞各地的中小企業正利用訂閱式授權模式,在無需承擔資本負擔的情況下獲得企業級功能,這進一步刺激了區域需求。

在歐洲,嚴格的網路安全和永續性要求使得整合合規能力至關重要。中東、非洲和南美洲雖然仍在發展中,但未來潛力大。阿拉伯聯合大公國一家企業集團採用 Infor M3,以及巴西一家中型製造商採用 NetSuite 的 SaaS 平台,都反映出人們對雲端區域的興趣日益濃厚,因為在這些區域,外匯對沖定價可以降低宏觀經濟風險。政府強制推行的「雲端優先」計劃,例如肯亞的「可信任資料區」項目,顯示主權雲端法規正在加速國有公用事業和交通運輸機構採用雲端技術。除非發生重大經濟衝擊,否則預計到 2031 年,該地區的雲端採用率將穩定成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 快速轉向基於雲端的部署模式

- 物聯網感測器的廣泛應用實現了預測性維護。

- 資產密集型產業對減少意外停機時間的需求日益成長。

- 整合 EAM 模組和永續性報告模組,以實現範圍 3排放合規性。

- 人工智慧驅動的主資料清洗工具的引入正在加速提高投資報酬率。

- 中型製造商採用基於使用量的訂閱定價模式的現狀

- 市場限制因素

- 與傳統ERP系統整合相關的高昂初始成本

- 互聯資產生態系中的網路安全與資料隱私問題

- 資產管理企業資源規劃(ERP)認證實施專家短缺。

- 由於專有資料模型和互通性標準的局限性,存在供應商鎖定風險。

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 透過部署方法

- 雲

- 現場

- 混合

- 按組織規模

- 大公司

- 小型企業

- 按行業

- 製造業

- 能源公用事業

- 運輸/物流

- 政府/公共部門

- 醫療保健

- 其他應用領域

- 模組特定

- 資產生命週期管理

- 工單管理

- 庫存和備件管理

- 預測性保護

- 財務資產會計

- 其他模組

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- IBM Corporation

- SAP SE

- Oracle Corporation

- Infor, Inc.

- IFS AB

- Hexagon AB

- ABB Ltd.

- Aptean, Inc.

- CGI Inc.

- CMMS Data Group, Inc.

- Ramco Systems Limited

- IPS Intelligent Process Solutions GmbH

- AVEVA Group plc

- Bentley Systems, Incorporated

- ServiceNow, Inc.

- UpKeep Technologies, Inc.

- Asset Panda, Inc.

- AssetWorks LLC

- Fluke Corporation

- Trimble Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the asset management enterprise resource planning (ERP) market size is expected to grow from USD 2.21 billion in 2025 to USD 2.41 billion in 2026 and is forecast to reach USD 4.04 billion by 2031 at 10.92% CAGR over 2026-2031.

This report is Segmented by Deployment Model (Cloud, On-Premise, and Hybrid), Organization Size (Large Enterprises, and SMEs), Application Vertical (Manufacturing, Energy and Utilities, Healthcare, and More), Module and Functionality (Asset Lifecycle Management, Work Order Management, Inventory and Spare Parts Management, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Asset Management Enterprise Resource Planning Market Trends and Insights

Rapid Migration to Cloud-Based Deployment Models

Cloud-native suites let enterprises offload infrastructure, accelerate feature delivery, and align expenses with consumption. Cloud ERP spending will shift toward AI-enabled solutions by 2027, highlighting a pivot toward platforms that embed machine learning into valuation and depreciation workflows. According to NetSuite, Hybrid architectures remain prevalent, with 88% of organizations retaining sensitive ledgers on private clouds while scaling analytics in the public cloud. Containerization has been adopted in significant production environments, making asset modules portable across clouds and simplifying disaster recovery. However, several percent of enterprises have repatriated workloads amid unforeseen costs, underscoring the need for FinOps governance and automated cost controls. Overall, cloud acceleration is unlocking rapid IoT integration and predictive analytics, making it the largest single growth lever for the Asset Management Enterprise Resource Planning (ERP) market.

Growing Adoption of IoT Sensors Enabling Predictive Maintenance

IEEE case studies confirm that sensor-to-ERP integration automates maintenance request processing and failure threshold alerts, reducing manual entry and enabling predictive workflows. Utilities are early adopters: DNV's Cascade links SCADA historians to asset scores, while SAS analytics detect turbine anomalies to enable proactive scheduling. Security remains a hurdle because most IoT devices lack agents and ship with default credentials, forcing enterprises to rely on micro-segmentation and network detection to safeguard ERP interfaces. As coverage gaps close, predictive maintenance will continue to outpace other modules within the Asset Management Enterprise Resource Planning (ERP) market.

High Upfront Integration Cost with Legacy ERP Systems

Decades of custom code and undocumented interfaces make modernization expensive. Process-mining tools reveal hidden inefficiencies: production often lags records by two days, and BOMs misstate changeover rules, underscoring the need for master-data remediation before go-live. Organizations that neglect this step risk automating poor workflows and eroding the ROI of the Asset Management Enterprise Resource Planning (ERP) market rollout.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand to Reduce Unplanned Downtime in Asset-Intensive Industries

- Convergence of EAM and Sustainability Reporting for Scope 3 Compliance

- Cybersecurity and Data-Privacy Concerns in Connected Asset Ecosystems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud deployments accounted for 48.50% of the Asset Management Enterprise Resource Planning (ERP) market share in 2025, and the segment is forecast to grow at a 12.30% CAGR through 2031. Organizations prefer vendor-managed infrastructure and rapid feature releases, while containerized microservices improve portability for hybrid strategies. The Asset Management Enterprise Resource Planning (ERP) market size attached to cloud deployments will expand as AI-enabled services move maintenance analytics and carbon accounting closer to compute power.

On-premise solutions persist where latency and data-sovereignty mandates prevail, especially in defense and heavily regulated utilities. Hybrid models, now embraced by 88% of enterprises, balance these constraints by keeping sensitive ledgers on private clouds and using public regions for scaling analytics. FinOps guardrails are becoming standard because 54% of enterprises cannot accurately track cloud spend, threatening to offset savings from hardware avoidance. Overall, the deployment choice now hinges more on regulatory and latency considerations than on technical capability differentials.

Large enterprises accounted for 60.30% of 2025 revenue, but small and medium enterprises are expanding at a 11.60% CAGR as vendors roll out consumption-based pricing, low-code templates, and managed services. The Asset Management Enterprise Resource Planning (ERP) market size accruing to SMEs will benefit from easier onboarding and reduced capital expenditure.

Resource constraints still challenge SMEs, yet SaaS suites that bundle finance, supply chain, and asset modules with automated master-data cleansing narrow the capability gap. In APAC and South America, cloud-first government incentives and currency-hedged subscription offers further lower adoption barriers. As usage-based pricing matures, SMEs are expected to drive a larger share of incremental demand over the forecast period.

Geography Analysis

North America accounted for 33.40% of 2025 revenue, supported by mature cloud infrastructure and early adoption of AI-driven analytics. Migration from SAP ECC to S/4HANA before the 2027 deadline is accelerating deals, though data-cleansing complexity is stretching timelines. The extraterritorial reach of the EU Cyber Resilience Act is prompting U.S. vendors to harden their products preemptively, embedding vulnerability-reporting and SBOM features to maintain European market access.

Asia-Pacific, the fastest-growing region at 11.40% CAGR, benefits from large-scale infrastructure investment in China and India and semiconductor capacity expansion backed by private commitments exceeding USD 500 billion. SMEs across Southeast Asia are leveraging subscription licensing to access enterprise-grade functionality without capital strain, further lifting regional demand.

Europe faces stringent cybersecurity and sustainability requirements, making integrated compliance features a must-have. The Middle East and Africa and South America remain nascent but promising. UAE conglomerates rolling out Infor M3 and Brazilian mid-market manufacturers adopting NetSuite SaaS platforms reflect rising interest where cloud regions and foreign-exchange-hedged pricing mitigate macro risks. Government cloud-first mandates, such as Kenya's trusted data zone projects, illustrate how sovereign-cloud provisions unlock adoption among state-owned utilities and transportation agencies. Absent major economic shocks, regional uptake is expected to broaden steadily through 2031.

- IBM Corporation

- SAP SE

- Oracle Corporation

- Infor, Inc.

- IFS AB

- Hexagon AB

- ABB Ltd.

- Aptean, Inc.

- CGI Inc.

- CMMS Data Group, Inc.

- Ramco Systems Limited

- IPS Intelligent Process Solutions GmbH

- AVEVA Group plc

- Bentley Systems, Incorporated

- ServiceNow, Inc.

- UpKeep Technologies, Inc.

- Asset Panda, Inc.

- AssetWorks LLC

- Fluke Corporation

- Trimble Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Migration to Cloud-Based Deployment Models

- 4.2.2 Growing Adoption of IoT Sensors Enabling Predictive Maintenance

- 4.2.3 Rising Demand to Reduce Unplanned Downtime in Asset-Intensive Industries

- 4.2.4 Convergence of EAM and Sustainability Reporting Modules for Scope 3 Emissions Compliance

- 4.2.5 Uptake of AI-Driven Master-Data Cleansing Tools Improving ROI Acceleration

- 4.2.6 Availability of Usage-Based Subscription Pricing for Mid-Tier Manufacturers

- 4.3 Market Restraints

- 4.3.1 High Upfront Integration Cost with Legacy ERP Systems

- 4.3.2 Cybersecurity and Data-Privacy Concerns in Connected Asset Ecosystems

- 4.3.3 Shortage of Certified Asset Management ERP Implementation Specialists

- 4.3.4 Vendor Lock-In Risk Due to Proprietary Data Models and Limited Interoperability Standards

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 Cloud

- 5.1.2 On-Premise

- 5.1.3 Hybrid

- 5.2 By Organization Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium Enterprises

- 5.3 By Application Vertical

- 5.3.1 Manufacturing

- 5.3.2 Energy and Utilities

- 5.3.3 Transportation and Logistics

- 5.3.4 Government and Public Sector

- 5.3.5 Healthcare

- 5.3.6 Other Application Verticals

- 5.4 By Module

- 5.4.1 Asset Lifecycle Management

- 5.4.2 Work Order Management

- 5.4.3 Inventory and Spare Parts Management

- 5.4.4 Predictive Maintenance

- 5.4.5 Financial Asset Accounting

- 5.4.6 Other Modules

- 5.5 BY GEOGRAPHY

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 SAP SE

- 6.4.3 Oracle Corporation

- 6.4.4 Infor, Inc.

- 6.4.5 IFS AB

- 6.4.6 Hexagon AB

- 6.4.7 ABB Ltd.

- 6.4.8 Aptean, Inc.

- 6.4.9 CGI Inc.

- 6.4.10 CMMS Data Group, Inc.

- 6.4.11 Ramco Systems Limited

- 6.4.12 IPS Intelligent Process Solutions GmbH

- 6.4.13 AVEVA Group plc

- 6.4.14 Bentley Systems, Incorporated

- 6.4.15 ServiceNow, Inc.

- 6.4.16 UpKeep Technologies, Inc.

- 6.4.17 Asset Panda, Inc.

- 6.4.18 AssetWorks LLC

- 6.4.19 Fluke Corporation

- 6.4.20 Trimble Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

企業資源計畫 (ERP) 市場:按組件、ERP 類型、來源類型、部署模式、組織規模和產業分類-2026-2032 年全球市場預測

企業資源計畫 (ERP) 市場:按組件、ERP 類型、來源類型、部署模式、組織規模和產業分類-2026-2032 年全球市場預測 2026-2030年全球企業資源規劃(ERP)軟體市場

2026-2030年全球企業資源規劃(ERP)軟體市場 醫療技術和生物製藥領域醫療設備CMO/CDMO市場:依產品類型、服務類型、器材分類和地區分類教育產業企業資源規劃 (ERP) 軟體市場:按組件、授權類型、部署類型、組織規模和最終用戶分類 - 2026-2032 年全球預測

醫療技術和生物製藥領域醫療設備CMO/CDMO市場:依產品類型、服務類型、器材分類和地區分類教育產業企業資源規劃 (ERP) 軟體市場:按組件、授權類型、部署類型、組織規模和最終用戶分類 - 2026-2032 年全球預測 先進製造市場預測至2034年:按技術、組件、部署模式、應用、產業和地區分類的全球分析

先進製造市場預測至2034年:按技術、組件、部署模式、應用、產業和地區分類的全球分析 2026年全球商業應用與開發市場報告2026年全球尖端材料與製造市場報告

2026年全球商業應用與開發市場報告2026年全球尖端材料與製造市場報告 ERP供應商生態系統市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP客製化服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP整合服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

ERP供應商生態系統市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP客製化服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP整合服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)