|

市場調查報告書

商品編碼

2065543

採購營運企業資源計畫(ERP):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Procurement Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

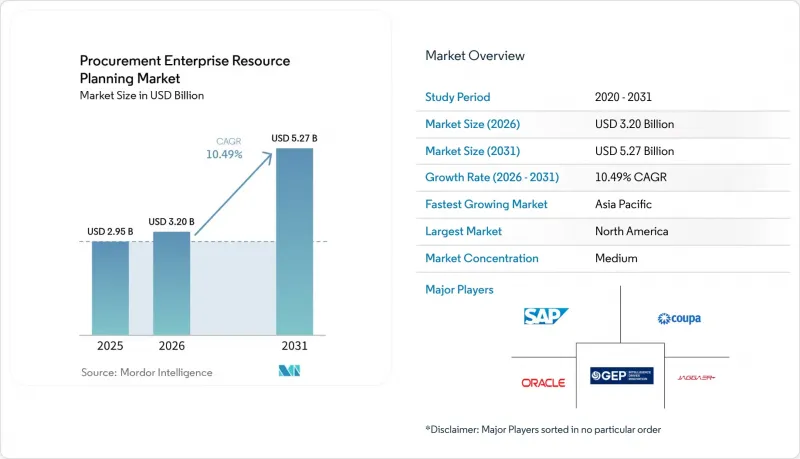

根據 Mordor Intelligence 預測,採購營運的企業資源計畫 (ERP) 市場規模預計將在 2026 年達到 32 億美元,到 2031 年達到 52.7 億美元,2026 年至 2031 年的複合年成長率為 10.49%。

本報告按部署方式(雲端、本地部署、混合部署)、模組(P2P、S2C 等)、組織規模(大型企業、中小企業)、最終用戶行業(製造業、零售/電子商務、醫療保健/製藥、IT/電信等)和地區進行細分。市場預測以美元計價。

全球採購營運企業資源規劃 (ERP) 市場趨勢與分析

加速採用雲端為基礎的採購套件

雲端採用使企業擺脫了硬體升級週期的束縛,並能在需求激增時實現彈性擴展。訂閱模式降低了初始授權成本,使中型企業也能使用高級功能。多租戶架構支援每季進行人工智慧增強,而無需進行中斷性升級。產業案例研究表明,遷移多個舊有系統後,週期時間縮短了 40%。在季節性產業中,利用雲端彈性有助於減少在淡季期間運算資源的過度分配,從而降低整體擁有成本 (TCO)。

將人工智慧和機器學習結合用於支出分析和供應商風險評估

機器學習引擎分析採購訂單、交貨記錄和外部風險數據,產生動態供應商評分卡。早期採用者報告稱,在整合尾部支出後的第一年就顯著節省了成本。自然語言處理技術自動提取付款條款和違約金條款,創建集中式債務日曆,從而促進主動重新談判。基於代理的人工智慧系統定期起草低價值採購訂單並設定核准流程,使品類經理能夠專注於策略採購活動。

整合傳統ERP系統的複雜性和高昂的遷移成本。

在過去幾十年沿用的系統中,採購資料以專有格式存儲,迫使企業建立成本高昂的客製化流程,這可能消耗其預算的40%,並將過渡期延長至18個月以上。重複的供應商記錄和客製化的工作流程需要簡化或重組。同時,採用準時制生產的製造商擔心過渡期間的停機會招致罰款。這些因素正在減緩雲端技術的普及,並阻礙ERP採購營運市場的整體成長。

細分市場分析

到2025年,基於雲端的解決方案將佔據採購營運ERP市場67.92%的佔有率。採購公司正在轉向訂閱模式,將資本支出轉化為可預測的營運成本,並加速在各子公司間的部署。供應商現在將基於人工智慧的支出儀錶板和協作工具捆綁銷售,這些工具依賴始終線上架構,進一步強化了雲端的吸引力。在因國家安全和主權資料法規而禁止外部託管的情況下,本地部署仍然被使用。諸如「RISE with SAP」等專案提供的混合拓撲結構支援模組的分階段遷移,從而降低業務中斷的風險並支援合規性。

對於那些既要滿足嚴格的審計要求又要兼顧可擴展創新需求的公司而言,混合模式極具吸引力。製藥公司通常會將間接採購遷移到雲端,同時保留本地原料採購;而製造商則會在同步之前,在本地邊緣節點上處理對延遲敏感的資料。能夠支援跨環境無縫資料流的供應商,正在為採購ERP市場的進一步成長建立競爭優勢。

到2025年,採購到付款(P2P)仍將佔總收入的55.12%,在實現從下單到付款流程的自動化方面發揮著至關重要的作用。同時,合約生命週期管理(CLM)正以11.01%的複合年成長率成長,這得益於其人工智慧驅動的文本提取功能,該功能可防止遺漏合約續約和價格調整條款。最新的平台將CLM與採購訂單創建直接整合,透過將協商條款轉換為可執行的採購訂單,無需人工重新錄入,從而確保透過談判節省成本。

支出分析引擎按類別預測需求,並識別尾部支出整合領域;供應商管理入口網站集中管理第三方風險評分。 S2C(採購到合約)套件將整個RFP(提案)生命週期數位化,並維護符合內部控制要求的可審計記錄。這種模組化且功能強大的系統使企業能夠隨著採購ERP市場的成熟而擴展策略能力。

區域分析

預計到2025年,北美將佔全球銷售額的33.64%。這主要得益於成熟的ERP生態系統和嚴格的透明度法規,這些法規要求採用統一的採購流程。強制性的氣候變遷資訊揭露推動了供應商層面碳排放追蹤平台的普及,而加拿大《強制勞動法》則要求提交年度實質審查報告,這些報告將透過ERP審計追蹤進行記錄。墨西哥近岸外包浪潮進一步刺激了對整合海關文件和品質指標的跨國採購套件的需求。

亞太地區是成長最快的地區,複合年成長率達10.76%。中國和印度的製造商正在推進採購流程數位化,以滿足出口標準並縮短週期;日本企業則將供應商績效整合到其「工業4.0」品質管理系統中。東南亞新興經濟體正在部署多語言且符合稅務規定的採購入口網站,以支援不斷成長的外國投資;代幣化支付基礎設施則有助於跨越分散的銀行網路向供應商付款。

歐洲市場正受到一系列指令的影響,這些指令強制要求進行人權和環境評估。德國汽車製造商在其ERP平台上管理數千家二級供應商,並追蹤ESG指標;而英國公司則需要在脫歐後協調英國和歐盟不同的合規要求。法國的反腐敗法促使供應商在入駐過程中進行利益衝突審查。在南美、中東和非洲,隨著各國政府實施電子競標平台,以及跨國公司在其本地子公司部署全球系統套件,採購營運的現代化進程正在加速,從而推動了採購ERP市場的擴張。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 加速採用雲端為基礎的採購套件

- 將人工智慧和機器學習應用於支出分析和供應商風險評估

- 大型企業對從採購到支付的端到端自動化需求日益成長。

- 監管機構日益重視供應鏈透明度和ESG合規性。

- 跨境代幣化支付基礎設施,實現供應商即時付款

- 基於代理商的採購機器人可縮短中型企業的採購週期。

- 市場限制因素

- 整合傳統ERP系統的複雜性以及高昂的遷移成本。

- 雲端採用過程中持續存在的資料安全和隱私問題

- 採購技術人員短缺,無法建構人工智慧工作流程

- 人工智慧驅動的供應商選擇引擎中存在的演算法偏見風險

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章:預測市場規模與成長率

- 透過部署方法

- 雲

- 現場

- 混合

- 模組特定

- P2P (Procure-to-Pay)

- S2C (Source-to-Contract)

- 合約生命週期管理(CLM)

- 支出分析

- 供應商管理

- 其他模組

- 按組織規模

- 大公司

- 中小企業

- 按最終用戶行業分類

- 製造業

- 零售與電子商務

- 醫療和藥品

- 銀行、金融服務和保險(BFSI)

- IT/通訊

- 政府/公共部門

- 能源公用事業

- 其他行業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- SAP SE

- Coupa Software Incorporated

- Oracle Corporation

- Jaggaer LLC

- Ivalua Inc.

- GEP Worldwide LLC

- Basware Oyj

- Zycus Inc.

- Proactis Holdings Limited

- Tradeshift Holdings Inc.

- Workday Inc.

- Infor Inc.

- Precoro Inc.

- Procurify Technologies Inc.

- Vroozi Inc.

- Medius Sverige AB

- Synertrade SES AG

- Xeeva Inc.

- Scanmarket A/S

- BirchStreet Systems LLC

第7章 市場機會與未來展望

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 加速採用雲端為基礎的採購套件

- 將人工智慧和機器學習應用於支出分析和供應商風險評估

- 大型企業對從採購到支付的端到端自動化需求日益成長。

- 監管機構日益重視供應鏈透明度和ESG合規性。

- 跨境代幣化支付基礎設施,實現供應商即時付款

- 基於代理商的採購機器人可縮短中型企業的採購週期。

- 市場限制因素

- 整合傳統ERP系統的複雜性以及高昂的遷移成本。

- 雲端採用過程中持續存在的資料安全和隱私問題

- 採購技術人員短缺,無法建構人工智慧工作流程

- 人工智慧驅動的供應商選擇引擎中存在的演算法偏見風險

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章:預測市場規模與成長率

- 透過部署方法

- 雲

- 現場

- 混合

- 模組特定

- P2P (Procure-to-Pay)

- S2C (Source-to-Contract)

- 合約生命週期管理(CLM)

- 支出分析

- 供應商管理

- 其他模組

- 按組織規模

- 大公司

- 中小企業

- 按最終用戶行業分類

- 製造業

- 零售與電子商務

- 醫療和藥品

- 銀行、金融服務和保險(BFSI)

- IT/通訊

- 政府/公共部門

- 能源公用事業

- 其他行業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- SAP SE

- Coupa Software Incorporated

- Oracle Corporation

- Jaggaer LLC

- Ivalua Inc.

- GEP Worldwide LLC

- Basware Oyj

- Zycus Inc.

- Proactis Holdings Limited

- Tradeshift Holdings Inc.

- Workday Inc.

- Infor Inc.

- Precoro Inc.

- Procurify Technologies Inc.

- Vroozi Inc.

- Medius Sverige AB

- Synertrade SES AG

- Xeeva Inc.

- Scanmarket A/S

- BirchStreet Systems LLC

第7章 市場機會與未來展望

According to Mordor Intelligence, the procurement enterprise resource planning(ERP) market size is projected to be USD 3.20 billion in 2026 and reach USD 5.27 billion by 2031, growing at a CAGR of 10.49% over 2026-2031.

This report is Segmented by Deployment Mode (Cloud, On-Premises, and Hybrid), Module (Procure-To-Pay, Source-To-Contract, and More), Organization Size (Large Enterprises and Small and Medium Enterprises), End-User Industry (Manufacturing, Retail and E-Commerce, Healthcare and Pharmaceutical, IT and Telecom, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Procurement Enterprise Resource Planning Market Trends and Insights

Accelerating Adoption of Cloud-Based Procurement Suites

Cloud deployment frees enterprises from hardware refresh cycles and supports elastic scaling during demand spikes. Subscription economics cut upfront license costs, making advanced capabilities accessible to mid-market buyers. Multi-tenant architectures deliver quarterly AI enhancements without disruptive upgrades, and industry examples show 40% reductions in cycle time after migrating multiple legacy systems. Seasonal sectors benefit from cloud elasticity, which curbs overprovisioned compute during off-peak months, improving the total cost of ownership.

Integration of AI and ML for Spend Analytics and Supplier Risk Scoring

Machine-learning engines mine purchase orders, delivery performance, and external risk data to generate dynamic supplier scorecards. Early adopters report considerable cost savings in the first year after consolidating tail spend. Natural-language processing automatically extracts payment terms and penalty clauses, creating centralized obligation calendars that trigger proactive renegotiations. Agentic AI routinely drafts low-value purchase orders and routes approvals, allowing category managers to focus on strategic sourcing.

Legacy ERP Integration Complexity and High Migration Costs

Decades-old systems store procurement data in proprietary formats, forcing costly custom pipelines that can consume 40% of the budget and extend cutover beyond 18 months. Duplicate supplier records and bespoke workflows must be cleansed or rebuilt, while just-in-time manufacturers fear downtime penalties during transition. Those factors delay cloud adoption and slow the overall growth of the Procurement ERP market.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for End-to-End Source-to-Pay Automation Among Large Enterprises

- Increasing Regulatory Emphasis on Supply-Chain Transparency and ESG Compliance

- Persistent Data Security and Privacy Concerns in Cloud Deployments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-based solutions commanded 67.92% of the Procurement ERP market share in 2025. Buyers are shifting to subscription models that convert capital expenses into predictable operating expenses and accelerate rollout across subsidiaries. Vendors now bundle AI-powered spend dashboards and collaboration tools that depend on always-connected architectures, reinforcing cloud preference. On-premises deployments persist where national security or sovereign data rules prohibit external hosting. Hybrid topologies, offered under programs like RISE with SAP, allow gradual module migration, mitigating disruption risk and supporting compliance.

Hybrid models appeal to companies balancing strict audit mandates with the need for scalable innovation. Pharmaceutical firms often keep ingredient sourcing on-premises while moving indirect procurement to the cloud, while manufacturers process latency-sensitive data at local edge nodes before synchronization. Vendors that support seamless data flow across environments position themselves for additional growth in the Procurement ERP market.

Procure-to-Pay retained 55.12% of 2025 revenue thanks to its foundational role in automating requisition-to-payment processes. However, Contract Lifecycle Management is growing at a 11.01% CAGR because AI text-extraction prevents missed renewals and uncaptured escalators. Modern platforms link CLM directly to requisition creation, turning negotiated terms into executable purchase orders without manual re-keying, which protects negotiated savings.

Spend-analysis engines forecast category demand and identify tail-spend consolidation, while supplier-management portals centralize third-party risk scores. Source-to-Contract suites now digitize the entire RFP life cycle, capturing auditable records that meet internal control requirements. This modular breadth enables enterprises to scale into strategic functionality as the Procurement ERP market maturity increases.

Geography Analysis

North America accounted for 33.64% of 2025 revenue, driven by mature ERP ecosystems and stringent transparency rules that compelled unified procurement processes. Climate-disclosure mandates drive the adoption of platforms that record supplier-level carbon emissions, and Canadian forced-labor laws require annual due diligence reports captured by ERP audit trails. Mexico's nearshoring wave further stimulates cross-border procurement suites that integrate customs documentation and quality metrics.

Asia-Pacific is the fastest-growing region at a 10.76% CAGR. Chinese and Indian manufacturers digitize procurement to meet export standards and reduce cycle times, while Japanese firms embed supplier performance into Industry 4.0 quality dashboards. Emerging Southeast Asian economies deploy multi-language, tax-compliant procurement portals to support rising foreign investment, and tokenized payment rails ease supplier settlement across fragmented banking networks.

Europe's market is shaped by directives mandating human rights and environmental assessments. German automotive giants manage thousands of tier-two suppliers on ERP platforms to track ESG metrics, and United Kingdom companies must reconcile divergent UK and EU compliance after Brexit. France's anti-corruption law drives conflict-of-interest checks at supplier onboarding. Procurement modernization is also accelerating in South America, the Middle East, and Africa as governments adopt e-tender portals and multinationals extend global suites to local subsidiaries, broadening the Procurement ERP market footprint.

List of Companies Covered in this Report:

- SAP SE

- Coupa Software Incorporated

- Oracle Corporation

- Jaggaer LLC

- Ivalua Inc.

- GEP Worldwide LLC

- Basware Oyj

- Zycus Inc.

- Proactis Holdings Limited

- Tradeshift Holdings Inc.

- Workday Inc.

- Infor Inc.

- Precoro Inc.

- Procurify Technologies Inc.

- Vroozi Inc.

- Medius Sverige AB

- Synertrade SES AG

- Xeeva Inc.

- Scanmarket A/S

- BirchStreet Systems LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Adoption of Cloud-Based Procurement Suites

- 4.2.2 Integration of AI and ML for Spend Analytics and Supplier Risk Scoring

- 4.2.3 Rising Demand for End-to-End Source-to-Pay Automation Among Large Enterprises

- 4.2.4 Increasing Regulatory Emphasis on Supply-Chain Transparency and ESG Compliance

- 4.2.5 Cross-Border Tokenized Payment Rails Enabling Real-Time Supplier Settlement

- 4.2.6 Agentic Procurement Bots Reducing Sourcing Cycle Time in Mid-Market Firms

- 4.3 Market Restraints

- 4.3.1 Legacy ERP Integration Complexity and High Migration Costs

- 4.3.2 Persistent Data Security and Privacy Concerns in Cloud Deployments

- 4.3.3 Shortage of Procurement-Tech Talent to Configure AI Workflows

- 4.3.4 Algorithmic Bias Risks in AI-Driven Supplier Selection Engines

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Cloud

- 5.1.2 On-Premise

- 5.1.3 Hybrid

- 5.2 By Module

- 5.2.1 Procure-to-Pay (P2P)

- 5.2.2 Source-to-Contract (S2C)

- 5.2.3 Contract Lifecycle Management (CLM)

- 5.2.4 Spend Analysis

- 5.2.5 Supplier Management

- 5.2.6 Other Modules

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By End-User Industry

- 5.4.1 Manufacturing

- 5.4.2 Retail and E-commerce

- 5.4.3 Healthcare and Pharmaceutical

- 5.4.4 Banking Financial Services and Insurance (BFSI)

- 5.4.5 Information Technology and Telecom

- 5.4.6 Government and Public Sector

- 5.4.7 Energy and Utilities

- 5.4.8 Other Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Coupa Software Incorporated

- 6.4.3 Oracle Corporation

- 6.4.4 Jaggaer LLC

- 6.4.5 Ivalua Inc.

- 6.4.6 GEP Worldwide LLC

- 6.4.7 Basware Oyj

- 6.4.8 Zycus Inc.

- 6.4.9 Proactis Holdings Limited

- 6.4.10 Tradeshift Holdings Inc.

- 6.4.11 Workday Inc.

- 6.4.12 Infor Inc.

- 6.4.13 Precoro Inc.

- 6.4.14 Procurify Technologies Inc.

- 6.4.15 Vroozi Inc.

- 6.4.16 Medius Sverige AB

- 6.4.17 Synertrade SES AG

- 6.4.18 Xeeva Inc.

- 6.4.19 Scanmarket A/S

- 6.4.20 BirchStreet Systems LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

企業資源計畫 (ERP) 市場:按組件、ERP 類型、來源類型、部署模式、組織規模和產業分類-2026-2032 年全球市場預測

企業資源計畫 (ERP) 市場:按組件、ERP 類型、來源類型、部署模式、組織規模和產業分類-2026-2032 年全球市場預測 2026-2030年全球企業資源規劃(ERP)軟體市場

2026-2030年全球企業資源規劃(ERP)軟體市場 醫療技術和生物製藥領域醫療設備CMO/CDMO市場:依產品類型、服務類型、器材分類和地區分類教育產業企業資源規劃 (ERP) 軟體市場:按組件、授權類型、部署類型、組織規模和最終用戶分類 - 2026-2032 年全球預測

醫療技術和生物製藥領域醫療設備CMO/CDMO市場:依產品類型、服務類型、器材分類和地區分類教育產業企業資源規劃 (ERP) 軟體市場:按組件、授權類型、部署類型、組織規模和最終用戶分類 - 2026-2032 年全球預測 先進製造市場預測至2034年:按技術、組件、部署模式、應用、產業和地區分類的全球分析

先進製造市場預測至2034年:按技術、組件、部署模式、應用、產業和地區分類的全球分析 2026年全球商業應用與開發市場報告2026年全球尖端材料與製造市場報告

2026年全球商業應用與開發市場報告2026年全球尖端材料與製造市場報告 ERP供應商生態系統市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP客製化服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP整合服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

ERP供應商生態系統市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP客製化服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP整合服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)