|

市場調查報告書

商品編碼

2065540

製造業企業資源計畫(ERP):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Manufacturing Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

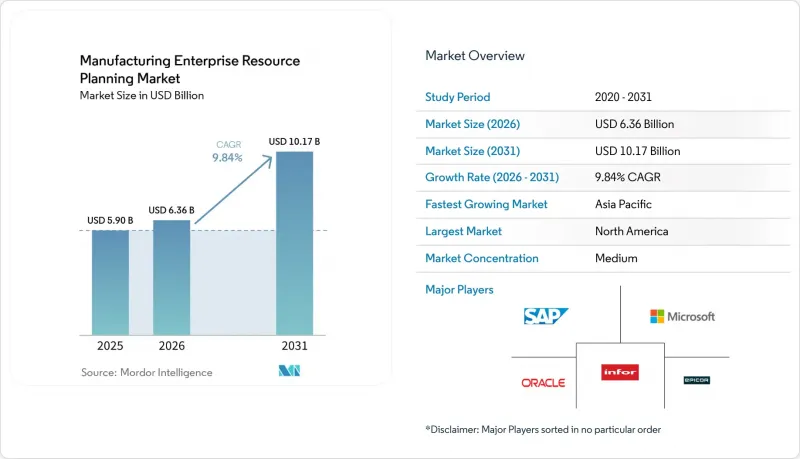

根據 Mordor Intelligence 預測,製造業企業資源規劃 (ERP) 市場規模將從 2025 年的 59 億美元和 2026 年的 63.6 億美元成長到 2031 年的 101.7 億美元,2026 年至 2031 年的年複合成長率(CAGR)。

本報告按部署方式(雲端、本地部署、混合部署)、組織規模(大型企業、中小企業)、製造方式(離散製造、流程製造、混合製造)、最終用戶產業(汽車、航太與國防、電子與高科技、食品飲料、工業機械、製藥等)以及地區進行細分。市場預測以美元計價。

全球製造業企業資源規劃 (ERP) 市場趨勢與分析

製造業中以雲端為先的數位轉型 (DX) 舉措

製造商正大規模地將交易處理工作負載遷移到公共雲端基礎設施,預計到2025年,雲端將佔據55.40%的市場。訂閱式定價模式免除了中型企業的前期授權費用,而強大的運算能力則使全球分散的設計和採購團隊能夠即時協作。在2025年半導體短缺期間,這種能力幫助電子供應商在數小時內重新分配了供應緊張的半導體。根據美國的「晶片與科學法案」(CHIPS and Science Act)撥款計劃,數位雙胞胎和雲端分析能力是強制性的,這使得現代化成為獲得聯邦津貼的先決條件。歐洲的《機械法規2023/1230》也採取了類似的立場,強制要求在2026年前實施數位產品護照。為了平衡主權方面的考量,工廠在本地管理生產配方,同時依靠雲端進行需求預測,預計混合雲採用率將達到18.00%。

工業物聯網、即時分析和ERP平台的整合

來自數控工具工具機和組裝機器人的Terabyte感測器資料(TB級)通常被置於計劃週期之外進行處理,但現代ERP系統現在可以接收MQTT和OPC-UA資料流,從而觸發預測性維護並自動重新安排訂單。一家一級汽車零件供應商透過實現這一閉迴路,在2025年減少了意外停機時間,提高了準時交貨率,並確立了自身作為首選供應商的地位。亞太地區的電子組裝製造商正在引領這項技術的普及,因為他們擁有高混合度的生產線,良率下降會轉化為巨大的成本。邊緣閘道器透過將需要毫秒響應的控制邏輯保留在本地,同時將匯總的關鍵績效指標(KPI)發送到雲端的ERP儀表板,證明了在分層架構中,延遲和洞察力可以共存。

對於擁有大量老舊設備的工廠而言,總體擁有成本 (TCO) 高且實施複雜。

仍在運作已有30年歷史控制器的棕地工廠,其整合成本比待開發區工廠高出40%至60%,因為需要客製化中間件來相容於其專有協定。一項2025年的調查顯示,北美38%的工廠使用基於MS-DOS的現場系統,這些系統無法交換即時數據,迫使用戶進行手動並行輸入,削弱了自動化帶來的優勢。更換過時的自動化系統通常成本超過軟體預算,專案週期可能長達24至36個月。在此期間,由於諮詢顧問需要對未記錄的客製化功能進行逆向工程,資金將被佔用,而且在過渡期間生產效率也會下降。

細分市場分析

隨著企業在雲端敏捷性和資料儲存監管要求之間尋求平衡,混合部署模式下製造業ERP市場正以18.00%的複合年成長率快速成長。到2025年,雲端將佔據製造業ERP市場55.40%的佔有率,但國防和製藥等受監管產業的工廠仍傾向於採用本地部署管理,以保護受出口管制的資料。由於歐洲的GDPR和中國的網路安全法規,生產配方和客戶文件仍需保留在國家境內,企業被迫轉向分層架構,將匿名化的計畫資料與公共雲端中的分析引擎進行同步。

邊緣閘道器可在本地以毫秒速度處理遙測數據,並將匯總的關鍵績效指標 (KPI) 傳送到雲端控制面板。隨著供應商提供可在任何有運算資源的地方運作的容器化服務,混合環境正成為預設的折衷方案,尤其對於必須遵守不同監管規則的跨國汽車製造商而言更是如此。

儘管大型企業仍佔據市場主導地位,但製造業ERP市場成長最快的細分市場是中小企業(SME),複合年成長率(CAGR)高達17.00%。訂閱模式消除了永久授權50萬美元的資本支出(CAPEX)門檻,而預先配置的產業專用的SaaS套件則將部署時間從18個月縮短至約8週。在新工廠中,由於舊有系統負擔極輕,管理人員可以透過直接遷移到行動原生介面,擺脫桌面工作站的束縛。

此外,繼任計畫的壓力正在推動數位轉型,即將退休的創辦人將他們在企業現場累積的專業知識系統化為軟體,以吸引買家。美國和歐洲的區域性津貼進一步降低了小規模工廠現代化的風險,並加速了向雲端的轉型。

區域分析

到2025年,北美將佔全球整體收入的38.60%。這主要得益於《晶片與科學法案》的獎勵,該法案將津貼與基於雲端的數位雙胞胎掛鉤,並鼓勵半導體工廠從一開始就運作最新的ERP系統。製造業回流以及墨西哥近岸外包的蓬勃發展,正在北美自由貿易北美自由貿易組織(NAFTA)貿易走廊內推廣標準化平台。同時,加拿大工廠正在部署碳排放追蹤系統,為未來可能徵收的邊境調節課稅做好準備。

在歐洲,為遵守《企業永續性報告指令》(CSRD) 範圍 3 的排放揭露要求,企業資源計畫 (ERP) 系統已成為碳計量的資料基礎。由於德國的「工業 4.0」計劃以及機械法規中對數位通行證的要求,汽車和機械行業叢集的支出正在加速成長。南歐的工廠正在利用歐盟數位化基金支付訂閱費用,從而縮小與北歐的數位化差距。

亞太地區是成長最快的地區,複合年成長率達8.80%。在印度,生產連結獎勵計畫(PLI)正與使用ERP系統進行的生產報告結合。在中國,國有企業被要求實施國產ERP系統,以遏制智慧財產權外流,這為本土供應商創造了新的機會。東南亞的契約製造製造商正在採用雲端套件,以滿足電子產品OEM廠商提出的即時可視性標準。儘管南美、中東和非洲的市場規模總合仍然較小,但存在一些快速普及的熱點地區,尤其是在海灣合作理事會(GCC)國家的石化行業和巴西的電動車供應鏈中。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 製造業中的雲端優先數位轉型計劃

- 工業物聯網、即時分析和ERP平台的整合

- 全球供應鏈可追溯性和合規性面臨的監管壓力

- 向人工智慧驅動的預測性維護和品管轉型

- 向中小製造業推廣產業專用的SaaS ERP解決方案。

- 強制要求永續發展報告,以鼓勵企業資源計畫(ERP)系統實施環境、社會和治理(ESG)資料管理。

- 市場限制因素

- 對於擁有眾多舊有系統。

- 對基於雲端的部署中的網路安全和智慧財產權盜竊問題的擔憂。

- 製造地缺乏熟練的ERP實施專家

- 對組織變革的抗拒和對既定生產流程的破壞。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章:預測市場規模與成長率

- 透過部署方法

- 雲

- 現場

- 混合

- 按組織規模

- 大公司

- 中小企業

- 透過製造方法

- 離散製造

- 工藝製造

- 混合製造

- 按報廢行業分類

- 車

- 航太/國防

- 電子產品與高科技

- 食品/飲料

- 工業機械

- 製藥

- 其他報廢工業部門

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Infor, Inc.

- Epicor Software Corporation

- QAD Inc.

- IFS AB

- Plex Systems, Inc.

- SYSPRO(Pty)Ltd.

- Abas Software GmbH

- Acumatica, Inc.

- Rootstock Software

- Aptean, Inc.

- Global Shop Solutions, Inc.

- Cetec ERP, LLC

- Priority Software Ltd.

- MRPeasy Ltd.

- DELMIAWorks(Dassault Systemes SE)

- Syspro Group(UK)Limited

第7章 市場機會與未來展望

According to Mordor Intelligence, the manufacturing ERP market size is projected to expand from USD 5.90 billion in 2025 and USD 6.36 billion in 2026 to USD 10.17 billion by 2031, registering a CAGR of 9.84% between 2026 and 2031.

This report is Segmented by Deployment Model (Cloud, On-Premise, and Hybrid), Organization Size (Large Enterprises, and SMEs), Manufacturing Mode (Discrete, Process, and Mixed-Mode), End-Industry Vertical (Automotive, Aerospace and Defense, Electronics and High-Tech, Food and Beverage, Industrial Machinery, Pharmaceuticals, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Manufacturing Enterprise Resource Planning Market Trends and Insights

Cloud-First Digital Transformation Initiatives in Manufacturing

Manufacturers are relocating transactional workloads to public-cloud infrastructure at scale, lifting cloud adoption to 55.40% market share in 2025. Subscription pricing eliminates upfront license fees for mid-tier firms, and elastic compute lets globally distributed design and procurement teams collaborate in real time, a capability that helped electronics suppliers reroute constrained semiconductors within hours during the 2025 shortage. United States subsidy programs under the CHIPS and Science Act require digital-twin and cloud analytics capabilities, turning modernization into a prerequisite for federal grants. Europe's Machinery Regulation 2023/1230 sets a similar tone by mandating digital product passports by 2026. To balance sovereignty concerns, plants keep recipes on-premises while offloading demand planning to the cloud, which underpins the 18.00% CAGR expected for hybrid deployments.

Integration of IIoT and Real-Time Analytics with ERP Platforms

Terabytes of sensor data from CNC machines and assembly robots often reside outside planning cycles, yet modern ERP suites now ingest MQTT and OPC-UA streams to trigger predictive maintenance and automatically reschedule orders. Tier-one automotive suppliers that closed this loop cut unplanned downtime in 2025, boosting on-time delivery and preferred-supplier status. APAC electronics assemblers lead adoption due to high-mix lines where yield losses are costly. Edge gateways retain millisecond-sensitive control logic on site, while summarized KPIs flow to cloud ERP dashboards, proving that latency and insight can coexist in a tiered architecture.

High Total Cost of Ownership and Complex Implementation for Legacy-Heavy Plants

Brownfield facilities still running three-decade-old controllers face integration costs 40-60% above greenfield benchmarks because proprietary protocols demand custom middleware. A 2025 survey found 38% of North American plants using MS-DOS shop-floor systems that cannot exchange live data, forcing parallel manual entry that erodes automation gains. Replacing antiquated automation often exceeds the software budget, so projects stretch 24-36 months while consultants reverse-engineer undocumented customizations, tying up capital and depressing output during cut-over phases.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Pressure for Traceability and Compliance Across Global Supply Chains

- Shift Toward AI-Enabled Predictive Maintenance and Quality Management

- Cybersecurity and IP Theft Concerns in Cloud-Based Deployments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The manufacturing ERP market size for hybrid deployments is advancing at an 18.00% CAGR as companies reconcile cloud agility with residency laws. In 2025, cloud held 55.40% of the manufacturing ERP market share, yet plants in regulated sectors such as defense and pharmaceuticals still favor on-premises control for export-controlled data. The European GDPR and China's Cybersecurity Law keep recipes and customer files within national borders, pushing firms toward tiered architectures that sync anonymized planning data into public cloud analytics engines.

Edge gateways process millisecond-grade telemetry locally, then post aggregated KPIs to cloud dashboards. As vendors deliver containerized services that run wherever compute resides, hybrid has become the default compromise, particularly for multinational automakers juggling divergent jurisdictional rules.

Large enterprises still account for the majority of purchasing, yet SMEs are the fastest-growing cohort in the manufacturing ERP market, with a 17.00% CAGR. Subscription models eliminate the USD 500,000 capex hurdle of perpetual licenses, while pre-configured vertical SaaS suites compress implementation from 18 months to roughly 8 weeks. Greenfield shops with minimal legacy baggage jump directly to mobile-native interfaces, freeing supervisors from desktop workstations.

Succession-planning pressures also spur digitization as retiring founders codify shop-floor knowledge in software to attract buyers. Regional grants in the United States and Europe further de-risk modernization for smaller plants, accelerating the pivot toward cloud.

Geography Analysis

North America generated 38.60% of global revenue in 2025 as the CHIPS and Science Act incentives tied grants to cloud-based digital twins, prompting semiconductor plants to standardize on modern ERP from day one. reshoring efforts and Mexico's nearshoring boom extend standardized platforms across NAFTA trade corridors, while Canadian factories adopt carbon-tracking features to prepare for prospective border-adjustment levies.

Europe invests heavily to meet the CSRD's Scope 3 emission-disclosure mandate that makes ERP the data backbone for carbon accounting. Germany's Industrie 4.0 and the Machinery Regulation's digital passport requirement accelerate spending in automotive and machinery clusters. Southern European plants tap EU digitization funds to offset subscription fees, narrowing the digital divide with the north.

Asia-Pacific is the fastest-growing region, with a 8.80% CAGR. India links Production-Linked Incentive payouts to ERP-driven production reporting. China mandates domestic ERP systems for state-owned firms to curb IP leakage, opening the door for local vendors. Southeast Asian contract manufacturers adopt cloud suites to meet real-time visibility standards imposed by electronics OEMs. South America, the Middle East, and Africa together remain smaller but show hotspots of rapid adoption, notably in GCC petrochemicals and Brazilian EV supply chains.

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Infor, Inc.

- Epicor Software Corporation

- QAD Inc.

- IFS AB

- Plex Systems, Inc.

- SYSPRO (Pty) Ltd.

- Abas Software GmbH

- Acumatica, Inc.

- Rootstock Software

- Aptean, Inc.

- Global Shop Solutions, Inc.

- Cetec ERP, LLC

- Priority Software Ltd.

- MRPeasy Ltd.

- DELMIAWorks (Dassault Systemes SE)

- Syspro Group (UK) Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-First Digital Transformation Initiatives in Manufacturing

- 4.2.2 Integration of IIoT and Real-Time Analytics with ERP Platforms

- 4.2.3 Regulatory Pressure for Traceability and Compliance Across Global Supply Chains

- 4.2.4 Shift Toward AI-Enabled Predictive Maintenance and Quality Management

- 4.2.5 Proliferation of Industry-Specific SaaS ERP Offerings for SMB Manufacturers

- 4.2.6 Sustainability Reporting Mandates Driving ERP Adoption for ESG Data

- 4.3 Market Restraints

- 4.3.1 High Total Cost of Ownership and Complex Implementation for Legacy-Heavy Plants

- 4.3.2 Cybersecurity and IP Theft Concerns in Cloud-Based Deployments

- 4.3.3 Shortage of Skilled ERP Implementation Professionals in Manufacturing Hubs

- 4.3.4 Organisational Change Resistance and Disruption to Established Production Workflows

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 Cloud

- 5.1.2 On-Premise

- 5.1.3 Hybrid

- 5.2 By Organization Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium-Sized Enterprises (SMEs)

- 5.3 By Manufacturing Mode

- 5.3.1 Discrete Manufacturing

- 5.3.2 Process Manufacturing

- 5.3.3 Mixed-Mode Manufacturing

- 5.4 By End-Industry Vertical

- 5.4.1 Automotive

- 5.4.2 Aerospace and Defense

- 5.4.3 Electronics and High-Tech

- 5.4.4 Food and Beverage

- 5.4.5 Industrial Machinery

- 5.4.6 Pharmaceuticals

- 5.4.7 Other End-Industry Verticals

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 Infor, Inc.

- 6.4.5 Epicor Software Corporation

- 6.4.6 QAD Inc.

- 6.4.7 IFS AB

- 6.4.8 Plex Systems, Inc.

- 6.4.9 SYSPRO (Pty) Ltd.

- 6.4.10 Abas Software GmbH

- 6.4.11 Acumatica, Inc.

- 6.4.12 Rootstock Software

- 6.4.13 Aptean, Inc.

- 6.4.14 Global Shop Solutions, Inc.

- 6.4.15 Cetec ERP, LLC

- 6.4.16 Priority Software Ltd.

- 6.4.17 MRPeasy Ltd.

- 6.4.18 DELMIAWorks (Dassault Systemes SE)

- 6.4.19 Syspro Group (UK) Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

企業資源計畫 (ERP) 市場:按組件、ERP 類型、來源類型、部署模式、組織規模和產業分類-2026-2032 年全球市場預測

企業資源計畫 (ERP) 市場:按組件、ERP 類型、來源類型、部署模式、組織規模和產業分類-2026-2032 年全球市場預測 2026-2030年全球企業資源規劃(ERP)軟體市場

2026-2030年全球企業資源規劃(ERP)軟體市場 醫療技術和生物製藥領域醫療設備CMO/CDMO市場:依產品類型、服務類型、器材分類和地區分類教育產業企業資源規劃 (ERP) 軟體市場:按組件、授權類型、部署類型、組織規模和最終用戶分類 - 2026-2032 年全球預測

醫療技術和生物製藥領域醫療設備CMO/CDMO市場:依產品類型、服務類型、器材分類和地區分類教育產業企業資源規劃 (ERP) 軟體市場:按組件、授權類型、部署類型、組織規模和最終用戶分類 - 2026-2032 年全球預測 先進製造市場預測至2034年:按技術、組件、部署模式、應用、產業和地區分類的全球分析

先進製造市場預測至2034年:按技術、組件、部署模式、應用、產業和地區分類的全球分析 2026年全球商業應用與開發市場報告2026年全球尖端材料與製造市場報告

2026年全球商業應用與開發市場報告2026年全球尖端材料與製造市場報告 ERP供應商生態系統市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP客製化服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP整合服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

ERP供應商生態系統市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP客製化服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP整合服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)