|

市場調查報告書

商品編碼

2065505

汽車LED模組:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)Automotive LED Module - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

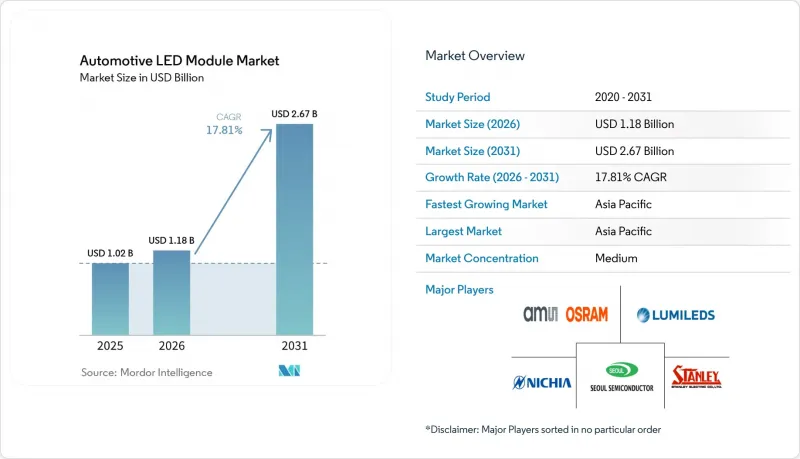

根據 Mordor Intelligence 預測,汽車 LED 模組市場規模預計在 2026 年達到 11.8 億美元,到 2031 年達到 26.7 億美元,2026 年至 2031 年的複合年成長率為 17.81%。

本報告按模組類型(COB LED模組、SMD LED模組、矩陣/像素LED模組等)、照明功能(外部照明、內部照明等)、車輛類型(乘用車、商用車)和地區(北美、歐洲、亞太、南美等)進行細分。市場預測以美元計價。

全球汽車LED模組市場趨勢及洞察

擴大ADAS(進階駕駛輔助系統)的應用

像素級光束控制可防止攝影機和雷射雷達影像過曝,促使原始設備製造商 (OEM) 採用具有超過 25,000 個可尋址點的高解析度模組。選擇性照明可降低高達 30% 的能耗,並透過減輕熱應力來延長使用壽命。軟體可程式設計光束無需機械部件即可相容於左舵和右舵駕駛標準,從而縮短開發週期。隨著 L3 和 L4 級自動駕駛技術的引入,能夠向行人傳達車輛意圖的照明將變得至關重要,這將進一步鞏固像素陣列作為頭燈標準技術的地位。

向電動車過渡需要節能照明

與鹵素燈110-130瓦的功耗相比,LED模組的功耗僅為40-60瓦,這使得緊湊型電動車的單次充電續航里程增加了2-4公里。如今,高階環境照明系統在維持95或更高顯色指數的同時,可將功耗降低30%,從而減輕電池冷卻迴路的負載。照明系統節省的每一瓦電力都可以重新分配給動力系統或空調系統,因此,汽車製造商幾乎在所有新型電動車平台上都指定使用LED燈,從而提高了每輛車上安裝的LED燈的數量和比例。

高功率LED模組的溫度控管挑戰

當流經結區的電流超過 1 安培時,溫度會升至 150 度C以上,加速光通量下降,並將目標壽命推低至 50,000 小時以下。雖然先進的基板、奈米碳管液體和主動冷卻技術可以降低發熱量,但它們會使每個模組的成本增加 8-12 美元,並增加保固的複雜性。在炎熱氣候下,這個問題會更加嚴重,迫使豪華車採用液冷板和微型風扇,但這些技術對於量產車型來說仍然無利可圖,從而減緩了像素技術在大批量生產領域的應用。

細分市場分析

到2025年,SMD LED模組將佔據汽車LED模組市場32.67%的佔有率,主要得益於成熟的供應鏈和可靠的散熱性能。像素和矩陣系統的汽車LED模組市場預計將以18.47%的複合年成長率成長,這主要得益於無需機械部件即可滿足UN ECE R149和NHTSA自我調整法規的軟體定義光束技術。目前,像素引擎包含超過16,000個微型LED,可監測每個發送器的電流和溫度,從而實現預測性維護並延長使用壽命。 COB封裝廣泛應用於高亮度聚光燈和霧燈,尤其是在商用車領域,因為在這些應用中,抗振性能比成本更為重要。雷射輔助混合式LED模組在磷光體穩定性和冷卻成本改善之前仍將屬於小眾產品,預計在2027年或之後開始量產。

像素架構之所以受歡迎,原因之一在於其售後韌體更新功能,可以添加新的動畫和通訊符號,而SMD陣列則無法實現這項功能。提供整合驅動IC且熱阻低於0.5kW的供應商正在贏得高階電動車專案的訂單,而純SMD封裝廠商則面臨著價格壓力,同時還要維持大規模生產的內燃機(ICE)模式。轉型時間表取決於散熱設計方面的突破和成本的進一步降低,但高像素密度模組的發展方向已經很明確。

區域分析

預計到2025年,亞太地區將佔據全球68.73%的市場佔有率,並在2031年之前以17.97%的複合年成長率持續成長。這主要是因為中國、日本和印度合計佔了全球大部分的LED產量。該地區集中生產mini-LED和micro-LED晶圓,縮短了前置作業時間,降低了封裝成本,進一步鞏固了該地區的優勢。中國一項旨在將新能源汽車滲透率提升至25%的補貼計劃,正在推動每輛車LED的安裝量成長。日本正在擴大其應用處理器模組的生產規模,將其國內工廠打造成為驅動IC和mini-LED背光燈的生產基地,這些產品用於車內照明和駕駛座顯示器。在印度,一台能夠生產2公尺長燈條的高噸位壓平機的投入使用,正在加速推進資本密集的尾燈專案。

在北美,消費者對可客製化內裝空間和軟體定義汽車平臺的需求正在推動成長。儘管美國國家公路交通安全管理局 (NHTSA) 對自我調整光束法規的謹慎執行減緩了超高像素密度顯示器的普及速度,但對矩陣陣列的需求仍然穩定。供應商正集中投資墨西哥和美國周邊地區,以供應國內組裝廠,同時降低關稅和物流風險。

在歐洲,聯合國ECE R149標準引領相關法規的發展,允許在整個歐洲大陸使用矩陣式LED日間行車燈,並遵循統一的測試標準。這鼓勵汽車製造商(OEM)為入門級車型配備LED燈,以滿足二氧化碳排放和安全目標。在南美洲和中東,LED市場規模雖小,但成長速度高於平均水準。這是因為出口商正在遵守歐盟照明標準,而且該地區的高階汽車買家也指定使用LED日行燈。非洲仍處於發展階段。雖然南非的高階市場正在採用LED燈,但大眾市場車型仍依賴鹵素燈來降低車輛價格。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- ADAS(進階駕駛輔助系統)的廣泛應用

- 向電動車過渡需要節能照明

- OEM廠商對模組化和擴充性照明架構的偏好

- LED燈每流明成本的下降正在推動其普及率的提高。

- 將動態像素照明整合到 V2X 通訊中

- 區域性夜間交通安全技術補貼

- 市場限制因素

- 高功率LED模組的溫度控管挑戰

- 矩陣/像素平台的初始模具成本較高

- 主要磷光體和外延材料的供應鏈波動

- 自我調整光束標準相關的監管不確定性

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按模組類型

- COB LED模組

- SMD LED模組

- 矩陣/像素 LED 模組

- 其他模組類型(雷射輔助模組、自適應模組)

- 按功能照明

- 戶外照明

- 頭燈

- 尾燈

- 日間行車燈(DRL)

- 其他戶外照明

- 室內照明

- 其他室內照明(環境氣氛照明、標誌投影)

- 戶外照明

- 車輛類型

- 搭乘用車

- 商用車輛

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 其他亞太國家

- 南美洲

- 中東和非洲

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Nichia Corporation

- Stanley Electric Co., Ltd.

- OSRAM GmbH

- LG Innotek Co., Ltd.

- Samsung Electronics Co., Ltd.

- Lumileds Holding BV

- Seoul Semiconductor Co., Ltd.

- Valeo SA

- Koito Manufacturing Co., Ltd.

- Hella GmbH & Co. KGaA

- Marelli Holdings Co., Ltd.

- Continental AG

- Denso Corporation

- Hyundai Mobis Co., Ltd.

- Varroc Engineering Limited

- ZKW Group GmbH

- Cree LED, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the automotive lED module market size is projected to be USD 1.18 billion in 2026 and reach USD 2.67 billion by 2031, growing at a CAGR of 17.81% from 2026 to 2031.

This report is Segmented by Module Type (COB LED Modules, SMD LED Modules, Matrix/Pixel LED Modules, and More), Lighting Function (Exterior Lighting, Interior Lighting, and More), Vehicle Type (Passenger Vehicles and Commercial Vehicles), and Geography (North America, Europe, Asia-Pacific, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Automotive LED Module Market Trends and Insights

Growing Adoption of Advanced Driver-Assistance Systems (ADAS)

Pixel-level beam control prevents camera and LiDAR wash-out, so OEMs are installing high-definition modules with more than 25,000 addressable points. Selective illumination cuts energy use by up to 30% and extends lifetime by reducing thermal stress. Software-programmable beams also enable left- and right-hand-drive compliance without mechanical parts, thereby shortening development cycles. As Level 3 and Level 4 features appear, lighting that communicates vehicle intent to pedestrians becomes essential, further entrenching pixel arrays as the default headlamp technology.

Shift Toward Electric Vehicles Requiring Energy-Efficient Lighting

LED modules draw 40-60 watts versus 110-130 watts for halogens, adding 2-4 kilometers of range per charge in compact EVs. Premium ambient systems now operate at 30% lower power while maintaining color-rendering indices above 95, easing load on battery cooling loops. Every watt saved in lighting is reallocated to drivetrain or climate control, so OEMs specify LEDs on nearly all new electric platforms, pushing both volume and content per vehicle higher.

Thermal Management Challenges in High-Power LED Modules

Currents above 1 ampere push junction temperatures past 150 °C, accelerating lumen loss and shortening life below the 50,000-hour target. Advanced substrates, carbon-nanotube fluids, and active cooling reduce heat but add USD 8-12 per module and increase warranty complexity. Hot climates intensify the problem, forcing premium cars to adopt liquid plates or micro-fans that remain uneconomic for mass models, thereby slowing pixel adoption in volume segments.

Other drivers and restraints analyzed in the detailed report include:

- OEM Preference for Modular, Scalable Lighting Architecture

- Declining LED Cost per Lumen Boosting Penetration

- High Up-Front Tooling Cost for Matrix/Pixel Platforms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

SMD LED modules accounted for 32.67% of the Automotive LED Module market share in 2025, thanks to mature supply chains and reliable thermal performance. The Automotive LED Module market size for pixel and matrix systems is projected to expand at an 18.47% CAGR, supported by software-defined beams that satisfy UN ECE R149 and NHTSA adaptive rules without mechanical parts. Pixel engines with more than 16,000 micro-LEDs now monitor current and temperature per emitter, enabling predictive maintenance and extending service life. COB packages serve high-intensity spot and fog functions, especially in commercial vehicles where vibration resistance matters more than cost. Laser-assisted hybrids remain niche until phosphor stability and cooling costs improve, with series production slated beyond 2027.

Pixel architectures advance partly because they enable firmware updates that add new animations or communication symbols post-sale, a feature SMD arrays cannot deliver. Suppliers offering integrated driver ICs and sub-0.5 K/W thermal resistance win premium EV programs, while pure SMD assemblers defend volume ICE models but face price compression. The transition timeline hinges on thermal breakthroughs and further cost declines, but the direction toward high-pixel-count modules is clear.

Geography Analysis

Asia Pacific commanded a 68.73% share in 2025 and will advance at a 17.97% CAGR through 2031, as China, Japan, and India together exceed a large amount of global output. Concentrated fabrication of Mini and Micro LED wafers shortens lead times and lowers package costs, reinforcing the region's dominance. Subsidies tied to China's 25% new-energy-vehicle penetration catalyze gains in LED content per car. Japan scales application-processor modules, positioning local plants as hubs for driver ICs and Mini LED backlights used in both interior lighting and cockpit displays. India accelerates tool-heavy rear-lamp programs thanks to new high-tonnage presses capable of two-meter light bars.

North America is catalyzed by consumer appetite for customizable cabins and software-defined vehicle platforms. NHTSA's cautious enforcement of its adaptive-beam rule slows ultra-high pixel counts but ensures stable demand for matrix arrays. Supplier investments cluster near Mexico and the United States to mitigate tariff and logistics risk while serving domestic assembly plants.

Europe sets the regulatory pace with UN ECE R149, allowing matrix beams across the continent under unified testing, encouraging OEMs to fit LEDs even on entry trims to meet CO2 and safety targets. South America and the Middle East show smaller bases but above-average gains, as exporters align with EU lighting standards and regional premium buyers specify LED daytime running lights. Africa remains nascent; premium segments in South Africa adopt LEDs, while mass models still rely on halogen to keep vehicle prices down.

- Nichia Corporation

- Stanley Electric Co., Ltd.

- OSRAM GmbH

- LG Innotek Co., Ltd.

- Samsung Electronics Co., Ltd.

- Lumileds Holding B.V.

- Seoul Semiconductor Co., Ltd.

- Valeo SA

- Koito Manufacturing Co., Ltd.

- Hella GmbH & Co. KGaA

- Marelli Holdings Co., Ltd.

- Continental AG

- Denso Corporation

- Hyundai Mobis Co., Ltd.

- Varroc Engineering Limited

- ZKW Group GmbH

- Cree LED, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Adoption of Advanced Driver-Assistance Systems (ADAS)

- 4.2.2 Shift Toward Electric Vehicles Requiring Energy-Efficient Lighting

- 4.2.3 OEM Preference for Modular, Scalable Lighting Architecture

- 4.2.4 Declining LED Cost per Lumen Boosting Penetration

- 4.2.5 Integration of Dynamic Pixel Lighting for Vehicle-to-X Communication

- 4.2.6 Regional Subsidies for Night-time Road-Safety Technologies

- 4.3 Market Restraints

- 4.3.1 Thermal Management Challenges in High-Power LED Modules

- 4.3.2 High Up-Front Tooling Cost for Matrix/Pixel Platforms

- 4.3.3 Supply-Chain Volatility of Key Phosphor and Epitaxy Materials

- 4.3.4 Regulatory Uncertainty Around Adaptive Beam Standards

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitute Products or Services

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Module Type

- 5.1.1 COB LED Modules

- 5.1.2 SMD LED Modules

- 5.1.3 Matrix / Pixel LED Modules

- 5.1.4 Other Module Type (laser-assisted, adaptive modules)

- 5.2 By Lighting Function

- 5.2.1 Exterior Lighting

- 5.2.1.1 Headlamps

- 5.2.1.2 Tail Lamps

- 5.2.1.3 Daytime Running Lights (DRL)

- 5.2.1.4 Others Exterior Lighting

- 5.2.2 Interior Lighting

- 5.2.3 Others Interior Lighting (ambient signature, logo projection)

- 5.2.1 Exterior Lighting

- 5.3 By Vehicle Type

- 5.3.1 Passenger Vehicles

- 5.3.2 Commercial Vehicles

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.5 Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 Stanley Electric Co., Ltd.

- 6.4.3 OSRAM GmbH

- 6.4.4 LG Innotek Co., Ltd.

- 6.4.5 Samsung Electronics Co., Ltd.

- 6.4.6 Lumileds Holding B.V.

- 6.4.7 Seoul Semiconductor Co., Ltd.

- 6.4.8 Valeo SA

- 6.4.9 Koito Manufacturing Co., Ltd.

- 6.4.10 Hella GmbH & Co. KGaA

- 6.4.11 Marelli Holdings Co., Ltd.

- 6.4.12 Continental AG

- 6.4.13 Denso Corporation

- 6.4.14 Hyundai Mobis Co., Ltd.

- 6.4.15 Varroc Engineering Limited

- 6.4.16 ZKW Group GmbH

- 6.4.17 Cree LED, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

汽車LED照明市場:依產品類型、技術、車輛類型及銷售管道分類-2026-2032年全球市場預測

汽車LED照明市場:依產品類型、技術、車輛類型及銷售管道分類-2026-2032年全球市場預測 全球汽車LED市場(2026年):照明與顯示產品趨勢

全球汽車LED市場(2026年):照明與顯示產品趨勢 汽車LED照明市場預測至2034年-依明位置、車輛類型、技術、銷售管道和地區分類的全球分析

汽車LED照明市場預測至2034年-依明位置、車輛類型、技術、銷售管道和地區分類的全球分析 歐洲汽車LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)汽車LED照明市場預測至2034年—按類型、銷售管道、安裝類型、應用和地區分類的全球分析英國汽車LED照明:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)

歐洲汽車LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)汽車LED照明市場預測至2034年—按類型、銷售管道、安裝類型、應用和地區分類的全球分析英國汽車LED照明:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年) 2026年全球汽車LED照明市場報告日本汽車LED照明:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)

2026年全球汽車LED照明市場報告日本汽車LED照明:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年) 汽車LED照明市場-全球產業規模、佔有率、趨勢、機會、預測:按位置、車輛類型、自適應照明、地區和競爭格局分類,2021-2031年

汽車LED照明市場-全球產業規模、佔有率、趨勢、機會、預測:按位置、車輛類型、自適應照明、地區和競爭格局分類,2021-2031年 汽車LED照明市場規模、佔有率和成長分析(按技術類型、車輛類型、類型和地區分類)-產業預測(2026-2033年)

汽車LED照明市場規模、佔有率和成長分析(按技術類型、車輛類型、類型和地區分類)-產業預測(2026-2033年)