|

市場調查報告書

商品編碼

2044276

英國汽車LED照明:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)United Kingdom Automotive LED Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

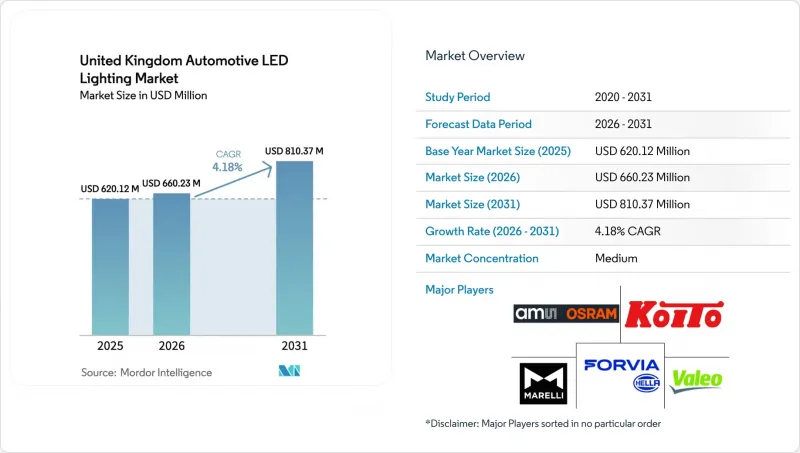

英國汽車LED照明市場預計到2025年將達到6.2012億美元,到2026年將達到6.6023億美元,到2031年將達到8.1037億美元,2026年至2031年的複合年成長率為4.18%。

這一穩步上升的趨勢反映了該國照明系統從鹵素燈向半導體照明的轉變,強制安裝LED前大燈、電動汽車(EV)註冊量的成長以及強調設計柔軟性和低功耗的蓬勃發展的改裝文化加速了這一轉變。雖然智慧高速公路的普及促進了主動式轉向頭燈的應用,但預計2023年至2025年間發光元件價格將下降15%至20%,這將削弱鹵素燈的成本優勢。氮化鎵晶片和稀土元素磷光體的供應鏈緊張仍然是限制因素,但一級供應商正在透過多元化採購和確保本地庫存來降低風險。諸如回收LED大燈等循環經濟措施正在緩解競爭,降低總擁有成本並擴大市場准入。

英國汽車LED照明市場趨勢與洞察

新車必須強制安裝LED頭燈。

隨著2024年新規生效,強制要求所有通過型式認證的新型車輛必須安裝LED或同等半導體頭燈,合規性已成為一項不容商榷的設計要求。 2024年,英國工廠將組裝779,584輛汽車,到2025年,英國道路上將有超過200萬輛新車,每輛車都將LED模組累計。一級供應商正在縮短檢驗週期,法雷奧(Valeo)和歐司朗(ams OSRAM)的聯合項目將環境照明整合時間從兩年縮短到不到一年,為前照燈部署樹立了新的標竿。諸如通過ECE R128認證的XLS LR6後LED等即用型產品正在縮短OEM測試週期,並進一步加速市場滲透。組裝正在進行升級以滿足溫度控管要求,這增加了資本投資,但降低了庫存過時的風險。整體而言,這項法規將使英國汽車LED照明市場的預期複合年成長率(CAGR)提高1.2個百分點。

降低LED元件成本,提高能源效率。

亞洲LED發送器產業叢集的過剩供應使得LED價格在2023年至2025年間降至原來的五分之一,使得曾經僅限於豪華車型的180流明尾燈模組如今也進入了大眾市場。全LED頭燈的能耗比鹵素燈低40%至60%,對於旨在提升WLTP續航里程的電動車製造商而言,這無疑是一項顯著的能源效率提升。到2025年,英國道路上將有175.9萬輛零排放汽車,將為節能照明提供堅實的需求基礎。馬瑞利(Marelli)的「LeanLight」架構在成本效益方面取得了顯著進展,成本降低了22%,組件數量減少了34%。雖然這些優勢提振了售後市場的需求,但隨著即插即用套件的價格已達到注重成本的消費者可以接受的水平,利潤空間也受到了擠壓。

與鹵素燈相比,LED模組的初始成本較高。

全LED大燈總成仍比鹵素燈泡貴40%至70%,導致其投資回收期比許多對成本敏感地區的車輛使用週期還要長。售後市場安裝一對LED大燈的成本可高達400英鎊(504美元),而鹵素燈泡的安裝成本僅為50英鎊(63美元),這限制了預算有限的駕駛員的接受度。 FORVIA HELLA公司2025年第9個月的利潤率被壓縮至2.7%,凸顯了盈利面臨的壓力,因為供應商自行承擔了增加的成本,而不是將其轉嫁給消費者。價格阻力最大的地區是北愛爾蘭和威爾士,這些地區二手車銷售占主導地位,這導致預計的複合年成長率下降了0.6個百分點。

細分市場分析

至2025年,售後市場將佔英國汽車LED照明市場68.11%的市佔率。這得歸功於英國4,196.4萬輛汽車的龐大保有量,平均車齡超過8年。獨立維修店正利用這項現有車源,提供維修安裝套件,以降低能耗並最大限度地減少更換燈泡造成的停機時間。雖然英國汽車LED照明市場的OEM(原廠配套)佔有率較小,但隨著原廠安裝的LED頭燈成為新型電動汽車和配備ADAS(高級駕駛輔助系統)車型的標配,預計OEM銷售額將以4.83%的複合年成長率成長。

2024 年的監管規定以及 ams OSRAM訂單。同時,由於零件成本下降,經銷商需要附加價值服務,以防止利潤率下滑。

到2025年,乘用車在英國汽車LED照明市場中佔62.36%的佔有率,這主要得益於乘用車註冊量高以及高階車型對LED的高採用率。然而,輕型商用車(LCV)市場預計到2031年將以每年5.12%的速度成長,這主要受「最後一公里」運輸業者貨車電氣化以及與智慧高速公路系統相容的自我調整LED的普及應用所驅動。

2025年第三季度,零排放輕型商用車佔註冊車輛總數的9.8%,高於去年同期的5.7%。車隊管理人員認為,LED燈的效率至關重要,因為LED燈比鹵素燈節能40%至60%,這對於續航里程和負載容量都至關重要。訂單,FORVIA HELLA與一家歐洲巴士製造商簽訂的2025年LED工作燈契約,就體現了LED技術對大型車輛的正面影響。雖然由於成本敏感性,摩托車的普及速度較為緩慢,但新興的微出行領域可能會在本世紀後半葉改變這種局面。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 新車必須強制安裝LED頭燈。

- LED組件成本更低,能源效率更高

- 電動車銷量的成長帶動了對先進照明產品的需求。

- 售後市場需求旨在提升外觀和性能。

- 智慧高速公路計畫旨在推廣主動式轉向頭燈。

- 國內半導體封裝稅收優惠

- 市場限制因素

- 與鹵素燈相比,LED模組的初始成本較高。

- 氮化鎵和稀土元素原料的供應鏈風險

- 英國嚴格的眩光法規限制了對高流明產品的改裝。

- 配備鹵素燈的二手車進口量正在迅速成長。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 新進入者的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 透過分銷管道

- OEM

- 售後市場

- 按車輛類型

- 搭乘用車

- 輕型商用車

- 大型商用車輛

- 摩托車

- 按安裝類型

- 新安裝

- 改造安裝

- 透過使用

- 外部照明

- 頭燈

- 日間行車燈

- 尾燈

- 霧燈

- 方向指示器

- 其他點火方式

- 室內照明

- 車頂燈和地圖燈

- 環境照明

- 儀表板和資訊娛樂系統背光

- 其他室內照明

- 外部照明

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Valeo SE

- Hella GmbH & Co. KGaA(FORVIA SE)

- Koito Manufacturing Co., Ltd.

- ams OSRAM AG

- Marelli Holdings Co., Ltd.

- Stanley Electric Co., Ltd.

- Hyundai Mobis Co., Ltd.

- Robert Bosch GmbH

- ZKW Group GmbH

- Lumileds Holding BV

- Lear Corporation

- Varroc Engineering Limited

- Denso Corporation

- Gentex Corporation

- Continental AG

- Panasonic Holdings Corporation

- Koninklijke Philips NV

- Eaton Corporation plc

- Signify NV

- Flex-N-Gate Corporation

第7章 市場機會與未來展望

The United Kingdom Automotive LED Lighting Market size is projected to be USD 620.12 million in 2025, USD 660.23 million in 2026, and reach USD 810.37 million by 2031, growing at a CAGR of 4.18% from 2026 to 2031.

The steady uptrend reflects the country's migration from halogen toward semiconductor-based illumination, a shift accelerated by mandatory LED head-lamp rules, expanding electric-vehicle (EV) registrations, and a vibrant retrofit culture that prizes design flexibility and lower energy draw. Rising smart-motorway coverage is pushing adaptive head-lamp adoption, while declining emitter prices down 15-20% between 2023 and 2025 are squeezing the halogen cost advantage. Supply-chain pressures for gallium-nitride wafers and rare-earth phosphors remain a constraint, yet Tier-1 suppliers are mitigating risk through multi-sourcing and localized inventories. Competitive intensity is tempered by circular-economy moves such as remanufactured LED head-lamps, which lower total cost of ownership and widen market access.

United Kingdom Automotive LED Lighting Market Trends and Insights

Mandatory LED Head-Lamp Regulations for New Vehicles

The 2024 rule requiring LED or equivalent semiconductor head-lamps on new type-approved vehicles has turned compliance into a non-negotiable design parameter. Domestic plants assembled 779,584 cars in 2024, and more than 2 million new vehicles reached UK roads in 2025, each now budgeting for LED modules. Tier-1 suppliers have compressed validation cycles joint programs between Valeo and ams OSRAM trimmed ambient-lighting integration from two years to under one setting a new pace for head-lamp rollouts. Ready-certified products such as the ECE R128-approved XLS LR6 rear LED shorten OEM testing, further accelerating penetration. Assembly lines have retooled for thermal-management demands, raising capital outlays yet lowering inventory obsolescence risk. Overall, this regulation adds 1.2 percentage points to the forecast CAGR of the United Kingdom automotive LED lighting market.

Declining LED Component Costs and Higher Energy Efficiency

Emitter oversupply in Asian fab clusters shaved up to one-fifth off LED prices between 2023 and 2025, unlocking mass-market adoption of 180-lumen rear modules once limited to premium trims. Power draw for full-LED head-lamps is 40-60% lower than halogen, an energy gain prized by EV makers seeking longer WLTP ranges. The United Kingdom counted 1.759 million zero-emission vehicles on the road in 2025, a captive base for energy-efficient lighting. Marelli's LeanLight architecture cut cost by 22% and parts count by 34%, illustrating the march toward cost parity. These gains lift retrofit appeal but compress margins, as plug-and-play kits reach price points acceptable to value-oriented drivers.

Higher Upfront Cost of LED Modules vs Halogen

Full-LED head-lamp assemblies still price 40-70% above halogen, producing payback periods longer than many ownership cycles in cost-sensitive regions. A retrofit pair can cost up to GBP 400 (USD 504) installed versus GBP 50 (USD 63) for halogen bulbs, limiting penetration among budget-constrained motorists. FORVIA HELLA's 9M 2025 margin squeezed to 2.7% as suppliers absorbed cost inflation rather than pass it through, underscoring profitability pressure. Price resistance is most acute in Northern Ireland and Wales, where used-vehicle sales dominate, clipping 0.6 percentage points from the forecast CAGR.

Other drivers and restraints analyzed in the detailed report include:

- Rising Electric-Vehicle Sales Boosting Demand for Advanced Lighting

- Aftermarket Demand for Aesthetic and Performance Upgrades

- Supply-Chain Risk for Gallium-Nitride and Rare-Earth Inputs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The aftermarket represented 68.11% of United Kingdom automotive LED lighting market revenue in 2025, buoyed by a 41.964 million-vehicle parc where the median age exceeds eight years. Independent garages leverage this installed base, offering retrofit kits that reduce energy draw and bulb-replacement downtime. The United Kingdom automotive LED lighting market size for OEM sales is smaller, yet OEM revenue is forecast to climb at a 4.83% CAGR as factory-fit LED head-lamps become standard equipment on new EVs and ADAS-enabled models.

OEM adoption is propelled by the 2024 mandate and by design-win pipelines exceeding EUR 2.5 billion (USD 2.83 billion) at ams OSRAM, evidencing long-term volume visibility. Valeo's April 2025 rollout of a remanufactured LED head-lamp blurs the aftermarket-OEM divide by offering OE quality at retrofit prices. Meanwhile, distributors need value-added services mobile fitting or subscription lighting upgrades to protect margins against falling component costs.

Passenger cars delivered 62.36% of United Kingdom automotive LED lighting market share in 2025 thanks to their registration volume and high LED take-rates in premium trims. Yet light commercial vehicles (LCVs) are expanding at 5.12% through 2031 as last-mile operators electrify vans and specify adaptive LEDs compatible with smart-motorway systems.

Zero-emission LCVs captured 9.8% of registrations in Q3 2025, up from 5.7% a year earlier. Fleet managers view LED efficiency 40-60% lower power draw than halogen as critical for range and payload. Orders such as FORVIA HELLA's 2025 LED work-lamp contract with a European bus maker confirm spillover into heavy vehicles. Two-wheelers lag due to cost sensitivity, but an emerging micro-mobility segment could shift that balance later in the decade.

The United Kingdom Automotive LED Lighting Market Report is Segmented by Sales Channel (OEM, and Aftermarket), Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, and Two-Wheelers), Installation Type (New Installation, and Retrofit Installation), Application (Exterior Lighting, and Interior Lighting). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Valeo SE

- Hella GmbH & Co. KGaA (FORVIA SE)

- Koito Manufacturing Co., Ltd.

- ams OSRAM AG

- Marelli Holdings Co., Ltd.

- Stanley Electric Co., Ltd.

- Hyundai Mobis Co., Ltd.

- Robert Bosch GmbH

- ZKW Group GmbH

- Lumileds Holding B.V.

- Lear Corporation

- Varroc Engineering Limited

- Denso Corporation

- Gentex Corporation

- Continental AG

- Panasonic Holdings Corporation

- Koninklijke Philips N.V.

- Eaton Corporation plc

- Signify N.V.

- Flex-N-Gate Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mandatory LED Head-Lamp Regulations for New Vehicles

- 4.2.2 Declining LED Component Costs and Higher Energy Efficiency

- 4.2.3 Rising Electric-Vehicle Sales Boosting Demand for Advanced Lighting

- 4.2.4 Aftermarket Demand for Aesthetic and Performance Upgrades

- 4.2.5 Smart-Motorway Projects Driving Adaptive Head-Light Adoption

- 4.2.6 Tax Incentives for Domestic Semiconductor Packaging

- 4.3 Market Restraints

- 4.3.1 Higher Upfront Cost of LED Modules vs. Halogen

- 4.3.2 Supply-Chain Risk for Gallium-Nitride and Rare-Earth Inputs

- 4.3.3 Stringent UK Glare Regulations Limiting High-Lumen Retrofits

- 4.3.4 Surge in Imported Second-Hand Cars with Halogen Lamps

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of Substitutes

- 4.8.4 Threat of New Entrants

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Sales Channel

- 5.1.1 OEM

- 5.1.2 Aftermarket

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Light Commercial Vehicles

- 5.2.3 Heavy Commercial Vehicles

- 5.2.4 Two-Wheelers

- 5.3 By Installation Type

- 5.3.1 New Installation

- 5.3.2 Retrofit Installation

- 5.4 By Application

- 5.4.1 Exterior Lighting

- 5.4.1.1 Headlamps

- 5.4.1.2 Daytime Running Lights

- 5.4.1.3 Taillights

- 5.4.1.4 Fog Lamps

- 5.4.1.5 Turn Signals

- 5.4.1.6 Other Exterior Lightings

- 5.4.2 Interior Lighting

- 5.4.2.1 Dome and Map Lights

- 5.4.2.2 Ambient Lighting

- 5.4.2.3 Instrument Cluster and Infotainment Back-Lighting

- 5.4.2.4 Other Interior Lightings

- 5.4.1 Exterior Lighting

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Valeo SE

- 6.4.2 Hella GmbH & Co. KGaA (FORVIA SE)

- 6.4.3 Koito Manufacturing Co., Ltd.

- 6.4.4 ams OSRAM AG

- 6.4.5 Marelli Holdings Co., Ltd.

- 6.4.6 Stanley Electric Co., Ltd.

- 6.4.7 Hyundai Mobis Co., Ltd.

- 6.4.8 Robert Bosch GmbH

- 6.4.9 ZKW Group GmbH

- 6.4.10 Lumileds Holding B.V.

- 6.4.11 Lear Corporation

- 6.4.12 Varroc Engineering Limited

- 6.4.13 Denso Corporation

- 6.4.14 Gentex Corporation

- 6.4.15 Continental AG

- 6.4.16 Panasonic Holdings Corporation

- 6.4.17 Koninklijke Philips N.V.

- 6.4.18 Eaton Corporation plc

- 6.4.19 Signify N.V.

- 6.4.20 Flex-N-Gate Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

汽車LED照明市場:依產品類型、技術、車輛類型及銷售管道分類-2026-2032年全球市場預測

汽車LED照明市場:依產品類型、技術、車輛類型及銷售管道分類-2026-2032年全球市場預測 全球汽車LED市場(2026年):照明與顯示產品趨勢

全球汽車LED市場(2026年):照明與顯示產品趨勢 汽車LED照明市場預測至2034年-依明位置、車輛類型、技術、銷售管道和地區分類的全球分析

汽車LED照明市場預測至2034年-依明位置、車輛類型、技術、銷售管道和地區分類的全球分析 汽車LED模組:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)歐洲汽車LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)汽車LED照明市場預測至2034年—按類型、銷售管道、安裝類型、應用和地區分類的全球分析

汽車LED模組:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)歐洲汽車LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)汽車LED照明市場預測至2034年—按類型、銷售管道、安裝類型、應用和地區分類的全球分析 2026年全球汽車LED照明市場報告日本汽車LED照明:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)

2026年全球汽車LED照明市場報告日本汽車LED照明:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年) 汽車LED照明市場-全球產業規模、佔有率、趨勢、機會、預測:按位置、車輛類型、自適應照明、地區和競爭格局分類,2021-2031年

汽車LED照明市場-全球產業規模、佔有率、趨勢、機會、預測:按位置、車輛類型、自適應照明、地區和競爭格局分類,2021-2031年 汽車LED照明市場規模、佔有率和成長分析(按技術類型、車輛類型、類型和地區分類)-產業預測(2026-2033年)

汽車LED照明市場規模、佔有率和成長分析(按技術類型、車輛類型、類型和地區分類)-產業預測(2026-2033年)