|

市場調查報告書

商品編碼

2035152

日本汽車LED照明:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)Japan Automotive LED Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

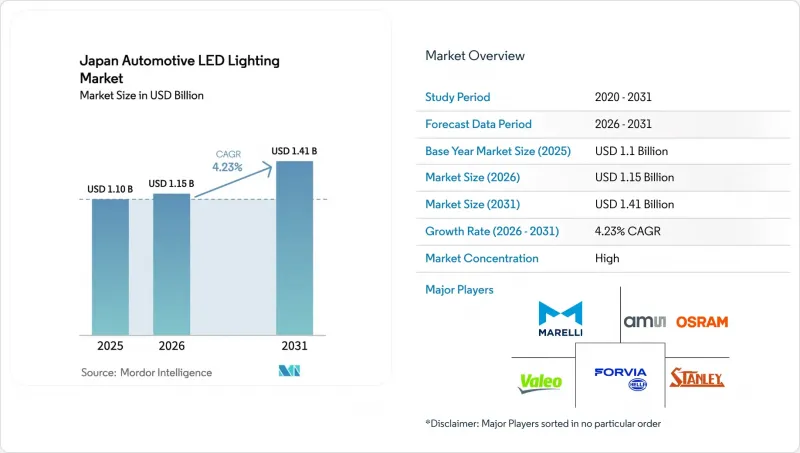

日本汽車LED照明市場預計將從2025年的11億美元成長到2026年的11.5億美元,然後從2026年到2031年以4.23%的複合年成長率成長,到2031年達到14.1億美元。

隨著電氣化政策的穩步推進、LED成本曲線趨於平穩以及2026年即將生效的嚴格能源效率法規,汽車製造商將低功耗、可軟體升級的照明系統整合到下一代電池式電動車(BEV)平台中,預計這一成長勢頭將得以保持。日本國內領先企業,如小糸製作所、Stanley Electric和一光產業株式會社,正透過集中研發自我調整遠光燈(ADB)、高解析度頭燈和感測器-照明融合技術,強化技術良性循環,助力日本汽車零件製造商(OEM)保持其在全球外部安全功能領域的領先地位。受中國鎵出口限制的影響,供應鏈壓力促使製造商採取多區域籌資策略。然而,持續的移動出行補貼在一定程度上緩解了利潤率面臨的壓力,而且可以肯定的是,2026年至2027年間推出的大多數車型都將標配全LED照明系統。此外,48V系統和分區電氣架構的廣泛應用,使得線束更加簡化輕便,從而確保了足夠的電力資源來應對新型資訊娛樂系統和自動駕駛系統的處理負載。

日本汽車LED照明市場趨勢與洞察

整車廠商對自我調整LED頭燈的需求激增。

小糸東的BladeScan MEMS型自適應數位大燈(ADB)相比靜態LED大燈,夜間能見度提升40%,並將於2025款車型年升級至16000像素版本,使車燈成為一套可與車聯網協同工作的預測性安全系統。豐田逐步將ADB引入其高階車型,表明ADB正從一項豪華配置轉變為一項標準安全配置,因此,能夠最佳化光學演算法、降低功耗並符合日本光強度標準的供應商的需求必將大幅成長。

LED成本快速降低和效率提升

採用單面鋁基基板和板載晶片(COB)技術可降低熱阻,並將模組組件成本降低30%以上,使LED即使在緊湊型轎車領域也能與鹵素燈在成本上相媲美。 48V主動矩陣驅動IC簡化了佈線,提高了可靠性。此外,由IEEE電子封裝協會資助的研究表明,新一代導熱界面材料可在超過10,000小時的佔空比下保持流明輸出。

在都市區以外的地區,摩托車採用LED燈的普及程度較低。

鄉村地區的騎乘者更重視維修的便利性而非先進的功能,而且由於經銷商網路分散,很少有商店備有符合日本光強度測試標準的LED改裝套件。因此,在分銷網路和技術培訓擴展之前,LED改裝套件的普及速度可能會比較緩慢。

細分市場分析

到2025年,OEM廠商將佔據日本汽車LED照明市場84.40%的佔有率。這壓倒性的市佔率源自於日本企業集團(keiretsu)體系特有的深度垂直整合。工廠預裝的系統整合了自我調整照明和ADAS域控制器,使得現場改裝變得不切實際,從而鞏固了OEM廠商的市場佔有率。以金額為準2025年,日本汽車LED照明OEM安裝市場規模將達9.3億美元。隨著汽車製造商將照明視為車輛安全評估的核心要素,OEM廠商對校準和線上程式解決方案的偏好,即使晶片價格下降,也支撐了市場需求。

隨著車主對鹵素燈車輛進行升級改造,售後市場正以5.38%的複合年成長率快速成長,但由於監管部門要求車輛維修店進行光度檢測,以及農村地區經銷商網路有限,該細分市場的成長仍然受到限制。雖然線上通路發展迅速,但銷售仍主要由PIAA和Carmate提供的專業安裝套裝主導,這些套裝包含光束模式檢驗設備,而對於DIY愛好者來說,由於該設備是車輛年檢的必要條件,因此難以獲得。

2025年,乘用車在日本汽車LED照明市場佔67.12%的比重。這反映了乘用車作為BladeScan、微型LED尾燈和迎賓燈等技術試驗場的地位。隨著純電動車(BEV)的日益普及,每輛車的LED數量不斷增加,使得該細分市場的複合年成長率(CAGR)達到8.29%,超過了其他所有細分市場。像2025年RAV4這樣的跨界車型將配備矩陣式頭燈和動態方向燈,這將加速一級供應商開發更高像素密度和低眩光演算法的步伐。

在商用貨車和輕型卡車中,LED燈主要因其耐用性而被採用。投資報酬率(ROI)更體現在延長維護週期上,而非品牌效應。在重型卡車領域,LED燈組正逐漸被整合式霧燈、日間行車燈和彎道輔助照明功能的LED叢集所取代,每個駕駛室最多可減輕3公斤的線束重量。摩托車LED燈的應用情況則呈現兩極化:在共享摩托車盛行且節能環保的人口稠密地區,LED燈發展迅速;而在高昂的初始成本驅動下,LED燈在農業地區的普及則停滯不前。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 整車廠商對自適應LED頭燈的需求激增

- LED成本快速下降,效率不斷提高

- 日本從 2026 年起實施的溫室氣體排放法規和能源效率標準將促進 LED 的普及。

- LED與ADAS感測器外殼的整合

- 聯網汽車造型客製化趨勢

- 電動車平台的發展需要低功耗照明

- 市場限制因素

- 都市區。

- 對進口高功率LED晶片的依賴

- 售後市場的價格競爭給利潤率帶來了壓力。

- 磷光體用稀土元素材料成本上漲

- 產業價值鏈分析

- 宏觀經濟因素對市場的影響

- 監理情勢

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 按銷售管道

- OEM

- 售後市場

- 車輛類型

- 搭乘用車

- 輕型商用車

- 大型商用車輛

- 摩托車

- 按安裝類型

- 新安裝

- 改造安裝

- 透過使用

- 外部照明

- 頭燈

- 日間行車燈

- 尾燈

- 霧燈

- 方向指示器

- 其他點火方式

- 室內照明

- 車頂燈和地圖燈

- 環境照明

- 儀表板和資訊娛樂系統背光

- 其他室內照明

- 外部照明

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Koito Manufacturing Co., Ltd.

- Stanley Electric Co., Ltd.

- Ichikoh Industries, Ltd.

- Valeo SA

- HELLA GmbH & Co. KGaA

- Magneti Marelli CK Holdings Co., Ltd.

- Varroc Engineering Limited

- Hyundai Mobis Co., Ltd.

- Denso Corporation

- Panasonic Automotive Systems Co., Ltd.

- Nichia Corporation

- Lumileds Holding BV

- LG Innotek Co., Ltd.

- ams-OSRAM AG

- Cree LED(SMART Global Holdings, Inc.)

- JW Speaker Corporation

- Texas Instruments Incorporated

- Renesas Electronics Corporation

- TDK Corporation

- Seoul Semiconductor Co., Ltd.

- Rohm Co., Ltd.

第7章 市場機會與未來展望

The Japan automotive LED lighting market size is expected to grow from USD 1.1 billion in 2025 to USD 1.15 billion in 2026 and is forecast to reach USD 1.41 billion by 2031 at 4.23% CAGR over 2026-2031.

Steady electrification mandates, shortening LED cost curves, and stringent efficiency rules effective as of 2026 keep the growth trajectory intact as automakers integrate low-power, software-updatable lighting into next-generation battery-electric vehicle (BEV) platforms. Domestic champions Koito Manufacturing, Stanley Electric, and Ichikoh Industries reinforce a technology flywheel by funneling research and development (R&D) into adaptive driving beams (ADB), high-resolution headlamps, and sensor-lighting fusion, which in turn enables Japanese original-equipment manufacturers (OEMs) to maintain global leadership in exterior safety features. Supply-chain pressures triggered by gallium export restrictions from China have prompted manufacturers to adopt multi-regional sourcing strategies. However, ongoing Mobility DX subsidies partially offset the margin squeeze, ensuring that most model launches in 2026-2027 will feature full-LED systems as standard. Widespread 48V and zone-based electrical architectures are also streamlining wiring looms, reducing weight, and freeing energy budgets for new infotainment and autonomous driving workloads.

Japan Automotive LED Lighting Market Trends and Insights

Surging OEM demand for adaptive LED headlamps

Koito's BladeScan MEMS-based ADB elevates nighttime visibility by 40% relative to static LEDs and will scale to 16,000-pixel versions for 2025 model years, transforming lamps into predictive safety systems that cooperate with vehicle-to-vehicle messages. Toyota's rollout across premium trims underscores how ADB is shifting from luxury to baseline safety equipment, guaranteeing deep pull-through for suppliers that can refine optical algorithms, reduce power draw, and meet Japanese photometric standards.

Rapid LED cost decline and efficiency gains

Single-sided aluminum substrates and chip-on-board (COB) packaging have cut thermal resistance and slashed module bill-of-materials by more than 30%, making LEDs cost-competitive with halogen even in kei-car classes. Active-matrix driver ICs operating at 48 V trim wiring bulk and boost reliability, while research funded by the IEEE Electronics Packaging Society shows next-gen thermal interface materials sustaining lumen output over 10,000 h duty cycles.

Slower two-wheeler LED uptake outside urban prefectures

Rural riders prize repairability over sophistication, and fragmented dealer networks rarely stock LED retrofit kits certified under Japan's photometric test regimen, muting penetration until distribution and training widen.

Other drivers and restraints analyzed in the detailed report include:

- Japan's 2026-onward GHG/efficiency norms boosting LED penetration

- Integration of LEDs with ADAS sensor housings

- Dependence on imported high-power LED chips

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The OEM segment accounted for 84.40% of Japan automotive LED lighting market share in 2025, a dominance rooted in the deep vertical collaboration typical of Japan's keiretsu arrangements. Factory-fitted systems marry adaptive luminaires with ADAS domain controllers, making field retrofits impractical and cementing OEM volume. In value terms, the Japan automotive LED lighting market size for OEM installations hit USD 0.93 billion in 2025. OEM preference for calibrated, in-line programming sustains demand even as chip prices fall, because automakers treat lighting as core to vehicle safety ratings.

Aftermarket avenues rise at 5.38% CAGR as owners modernize halogen fleets; yet the segment stays constrained by regulatory photometry checks that require certified workshops and by limited rural dealer density. Online channels grow briskly, but professional installation packages from PIAA and Car Mate dominate revenue because vehicle inspection compliance demands beam-pattern validation equipment unavailable to do-it-yourself enthusiasts.

Passenger cars contributed 67.12% of Japan automotive LED lighting market size in 2025, reflecting the class's role as a proving ground for BladeScan, micro-LED taillamps, and welcome-light scripts. The segment's 8.29% CAGR outpaces all others as BEV rollouts multiply LED points per vehicle. Crossovers such as the 2025 RAV4 embed matrix headlamps and animated turn signals, spurring tier-one suppliers to accelerate pixel counts and low-glare algorithms.

Commercial vans and light trucks adopt LEDs primarily for durability; ROI stems from longer service intervals rather than branding. Heavy trucks migrate to LED clusters that integrate fog, DRL, and cornering functions, reducing harness weight by up to 3 kg per cab. Two-wheeler adoption remains bipolar, thriving in dense prefectures where scooter sharing schemes favor energy savings yet stalling in agricultural regions sensitive to upfront premiums.

The Japan Automotive LED Lighting Market Report is Segmented by Sales Channel (OEM, and Aftermarket), Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, and Two-Wheelers), Installation Type (New Installation, and Retrofit Installation), Application (Exterior Lighting, and Interior Lighting). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Koito Manufacturing Co., Ltd.

- Stanley Electric Co., Ltd.

- Ichikoh Industries, Ltd.

- Valeo S.A.

- HELLA GmbH & Co. KGaA

- Magneti Marelli CK Holdings Co., Ltd.

- Varroc Engineering Limited

- Hyundai Mobis Co., Ltd.

- Denso Corporation

- Panasonic Automotive Systems Co., Ltd.

- Nichia Corporation

- Lumileds Holding B.V.

- LG Innotek Co., Ltd.

- ams-OSRAM AG

- Cree LED (SMART Global Holdings, Inc.)

- J.W. Speaker Corporation

- Texas Instruments Incorporated

- Renesas Electronics Corporation

- TDK Corporation

- Seoul Semiconductor Co., Ltd.

- Rohm Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging OEM demand for adaptive LED headlamps

- 4.2.2 Rapid LED cost decline and efficiency gains

- 4.2.3 Japan's 2026-onward GHG/efficiency norms boosting LED penetration

- 4.2.4 Integration of LEDs with ADAS sensor housings

- 4.2.5 Connected-car styling customisation trend

- 4.2.6 Growth of EV platforms needing low-power lighting

- 4.3 Market Restraints

- 4.3.1 Slower two-wheeler LED uptake outside urban prefectures

- 4.3.2 Dependence on imported high-power LED chips

- 4.3.3 Aftermarket price wars squeezing margins

- 4.3.4 Rising rare-earth material costs for phosphors

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Sales Channel

- 5.1.1 OEM

- 5.1.2 Aftermarket

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Light Commercial Vehicles

- 5.2.3 Heavy Commercial Vehicles

- 5.2.4 Two-Wheelers

- 5.3 By Installation Type

- 5.3.1 New Installation

- 5.3.2 Retrofit Installation

- 5.4 By Application

- 5.4.1 Exterior Lighting

- 5.4.1.1 Headlamps

- 5.4.1.2 Daytime Running Lights

- 5.4.1.3 Taillights

- 5.4.1.4 Fog Lamps

- 5.4.1.5 Turn Signals

- 5.4.1.6 Other Exterior Lightings

- 5.4.2 Interior Lighting

- 5.4.2.1 Dome and Map Lights

- 5.4.2.2 Ambient Lighting

- 5.4.2.3 Instrument Cluster and Infotainment Backlighting

- 5.4.2.4 Others Interior Lightings

- 5.4.1 Exterior Lighting

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Koito Manufacturing Co., Ltd.

- 6.4.2 Stanley Electric Co., Ltd.

- 6.4.3 Ichikoh Industries, Ltd.

- 6.4.4 Valeo S.A.

- 6.4.5 HELLA GmbH & Co. KGaA

- 6.4.6 Magneti Marelli CK Holdings Co., Ltd.

- 6.4.7 Varroc Engineering Limited

- 6.4.8 Hyundai Mobis Co., Ltd.

- 6.4.9 Denso Corporation

- 6.4.10 Panasonic Automotive Systems Co., Ltd.

- 6.4.11 Nichia Corporation

- 6.4.12 Lumileds Holding B.V.

- 6.4.13 LG Innotek Co., Ltd.

- 6.4.14 ams-OSRAM AG

- 6.4.15 Cree LED (SMART Global Holdings, Inc.)

- 6.4.16 J.W. Speaker Corporation

- 6.4.17 Texas Instruments Incorporated

- 6.4.18 Renesas Electronics Corporation

- 6.4.19 TDK Corporation

- 6.4.20 Seoul Semiconductor Co., Ltd.

- 6.4.21 Rohm Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment

汽車LED照明市場:依產品類型、技術、車輛類型及銷售管道分類-2026-2032年全球市場預測

汽車LED照明市場:依產品類型、技術、車輛類型及銷售管道分類-2026-2032年全球市場預測 全球汽車LED市場(2026年):照明與顯示產品趨勢

全球汽車LED市場(2026年):照明與顯示產品趨勢 汽車LED照明市場預測至2034年-依明位置、車輛類型、技術、銷售管道和地區分類的全球分析

汽車LED照明市場預測至2034年-依明位置、車輛類型、技術、銷售管道和地區分類的全球分析 汽車LED模組:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)歐洲汽車LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)汽車LED照明市場預測至2034年—按類型、銷售管道、安裝類型、應用和地區分類的全球分析英國汽車LED照明:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)

汽車LED模組:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)歐洲汽車LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)汽車LED照明市場預測至2034年—按類型、銷售管道、安裝類型、應用和地區分類的全球分析英國汽車LED照明:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年) 2026年全球汽車LED照明市場報告

2026年全球汽車LED照明市場報告 汽車LED照明市場-全球產業規模、佔有率、趨勢、機會、預測:按位置、車輛類型、自適應照明、地區和競爭格局分類,2021-2031年

汽車LED照明市場-全球產業規模、佔有率、趨勢、機會、預測:按位置、車輛類型、自適應照明、地區和競爭格局分類,2021-2031年 汽車LED照明市場規模、佔有率和成長分析(按技術類型、車輛類型、類型和地區分類)-產業預測(2026-2033年)

汽車LED照明市場規模、佔有率和成長分析(按技術類型、車輛類型、類型和地區分類)-產業預測(2026-2033年)