|

市場調查報告書

商品編碼

2063854

歐洲汽車LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)Europe Automotive LED Package - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

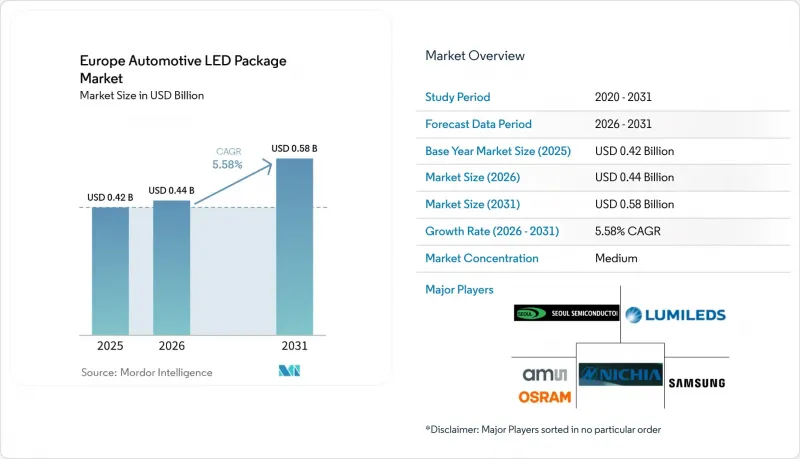

根據 Mordor Intelligence 預測,汽車LED構裝市場將從 2025 年的 4.2 億美元成長到 2026 年的 4.4 億美元,到 2031 年達到 5.8 億美元,2026 年至 2031 年的複合年成長率為 5.58%。

本報告依封裝結構(SMD、CSP、覆晶LED構裝、COB)、功率等級(0.5W以下低功率、0.5W至1W中功率、1W以上高功率)、應用(外部照明、內部照明等)、車輛類型(乘用車、商用車)及地區進行細分。市場預測以美元(USD)計價。

歐洲汽車LED構裝市場趨勢與洞察

從鹵素燈到LED大燈的快速過渡

2022年聯合國第37號法規的修訂為在鹵素燈安裝位置引入經認證的LED替換燈泡鋪平了道路。 2025年5月,歐司朗(ams OSRAM)將推出首款獲得ECE認證的H11 LED替換燈泡,承諾能耗降低五分之一,使用壽命延長六倍。一項涵蓋所有鹵素燈泡產品的分階段藍圖將持續到2028年,為擁有2.52億輛汽車的歐洲乘用車市場帶來數年的改裝機會。同時,Stellantis等OEM廠商正在推出緊湊型雙LED模組,這些模組在滿足鹵素燈亮度特性的同時,也能降低成本和功耗,顯示入門級新車對成本最佳化的LED產品也存在著類似的需求。因此,封裝供應商需要將產品系列分類為熱穩定性強的改裝方案和超緊湊型OEM解決方案,這兩種方案對電阻和驅動IC策略的要求各不相同。

對自我調整頭燈系統(AFLS)的需求不斷成長

聯合國第123號法規的協調統一降低了自我調整遠光燈(ADB)的型式認證門檻,使得這項功能得以從豪華車推廣到大眾市場車型。 Audi2026款Q3將首次搭載25,600像素的微型LED矩陣,而日亞化學工業株式會社的三級「像素化光源」系列產品則允許汽車製造商在無需更換外殼的情況下,將ADB功能從入門級車型擴展到高階車型。英飛凌的整合式LITIX驅動器可將城市駕駛工況下的待機功耗降低50%,滿足純電動車的能源效率目標。這些架構有利於那些將LED外延和ASIC聯合設計的供應商,加速了高像素模組市場「贏家通吃」的趨勢。

2025年及以後汽車產量變化

歐洲LED產量仍比疫情前尖峰時段低300萬台,供應商自2024年以來已損失超過10萬個工作機會。在英國,由於網路攻擊和關稅問題,預計2025年LED產量將下降15.5%。貨車和卡車的註冊量也分別下降了8.8%和6.2%。能源價格上漲、人手不足以及準時制生產中斷,都增加了LED製造商的營運資金成本,迫使那些尚未實現終端市場多元化的公司以低運轉率運作潔淨室,從而擠壓了利潤空間。

細分市場分析

預計到2025年,晶片級封裝(CSP)將在汽車LED構裝市場中佔據更大佔有率,並在2031年超越傳統的表面黏著型元件(SMD)。 CSP透過將晶片直接鍵合到基板,降低了熱阻,並實現了適用於自適應光束的像素間距。供應商正在微型LED陣列中應用CSP,其中每個晶片的尺寸小於100µm,支援超過25,000個像素的矩陣,同時抑制串擾。覆晶設計可為超過10,000坎德拉的頭燈光束提供更優異的電流分佈,但由於需要無空隙鍵合,因此需要更嚴格的製程控制。雖然傳統的SMD封裝在對成本敏感的日間行車燈領域仍然佔據主導地位,但隨著OEM廠商轉向將LED和驅動器整合在單塊基板的系統整合解決方案,其市場佔有率正在萎縮。板載晶片仍然是入門級反射器的低成本選擇,但其不可更換的特性與歐盟循環經濟的討論相衝突,可能會限制其廣泛應用。

儘管SMD在2025年仍將主導汽車LED構裝市場,但CSP正以6.01%的複合年成長率展現出最快的成長動能。高解析度自我調整照明、數位電子看板和格柵照明等應用均利用了CSP的低Z軸高度和導熱路徑優勢,從而實現超薄燈體,提升空氣動力性能。將CSP晶片與英飛凌和恩智浦的驅動ASIC晶片捆綁銷售的供應商正在提升系統穩定性,而僅限於通用SMD的供應商則面臨價格壓力。歐盟關於可互換LED光源的討論甚至可能促使市場需求回歸模組化封裝,從而在SMD、CSP和新興的插入式LED引擎標準之間形成競爭。

到2025年,功率超過1W的高功率封裝將佔汽車LED構裝市場收入的近60%。這是因為聯合國112號法規的光通量閾值已將頭燈鎖定在高亮度系統上。高階ADB模組的亮度通常超過2000流明,需要清潔和調平,但使用單一高功率晶片而非多個中功率晶片可以最佳化實現這些目標,從而簡化光學和佈線。中功率LED滿足了對亮度要求適中的彎道照明燈和訊號燈的細分市場,但其銷售不足以抵消價格下降的影響。低功率LED仍然是間接式車內照明和儀錶叢集背光必不可少的,但ISELED的智慧RGB裝置透過整合式硬碟模糊了功率與低功率LED之間的界限,將價值從分離式封裝轉移到半導體整合照明。

受投射式頭燈和微型LED陣列的推動,高功率LED的優勢預計將以5.94%的複合年成長率持續成長,但散熱設計限制仍然是一項真正的挑戰。供應商正在採用蒸氣室和石墨片等技術,將結溫控制在125°C以下,這是實現超過25,000小時L70壽命的必要條件。無法溫度控管的供應商將面臨被下一代頭燈市場淘汰的風險。同時,受可自訂內裝空間和純電動車(BEV)節能需求的推動,低功率車內LED正在成長,而可尋址RGB燈條則實現了與資訊娛樂系統同步的無線主題傳輸。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 從鹵素大燈到LED大燈的快速過渡

- 自我調整頭燈系統的需求日益成長

- 歐盟嚴格的二氧化碳排放法規正在推動節能照明的發展。

- 高階機型採用Mini-LED和Micro-LED技術

- 東歐供應鏈本地化獎勵

- 汽車網路安全標準要求使用紅外線LED

- 市場限制因素

- 2025年及以後汽車產量變化

- 功率超過 1 瓦時,溫度控管面臨挑戰。

- 歐洲專利保護期到期及持續進行的LED智慧財產權訴訟

- CBAM實施後,亞洲製造的LED構裝進口關稅提高。

- 產業供應鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 所以

- SMD(表面黏著型元件)

- CSP(晶片級封裝)

- 覆晶LED構裝

- COB(板載晶片)

- 按輸出類別

- 低功率(小於0.5瓦)

- 中功率(0.5–1 瓦)

- 高功率(超過 1 瓦)

- 透過使用

- 戶外照明

- 室內照明

- 感測/紅外線應用

- 其他用途(訊號傳遞等)

- 按車輛類型

- 搭乘用車

- 商用車輛

- 按地區

- 英國

- 德國

- 法國

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- ams OSRAM AG

- Nichia Corporation

- Lumileds Holding BV

- Seoul Semiconductor Co., Ltd.

- Samsung Electronics Co., Ltd.

- LG Innotek Co., Ltd.

- Cree LED

- Lite-On Technology Corporation

- Stanley Electric Co., Ltd.

- Toyoda Gosei Co., Ltd.

- EVERLIGHT Electronics Co., Ltd.

- Dominant Opto Technologies Sdn. Bhd.

- ROHM Co., Ltd.

- Lextar Electronics Corporation

- NationStar Optoelectronics Co., Ltd.

- Sanan Optoelectronics Co., Ltd.

- Refond Optoelectronics Co., Ltd.

- Hella GmbH & Co. KGaA

- Valeo SA

第7章 市場機會與未來展望

According to Mordor Intelligence, the automotive lED package market size is expected to increase from USD 0.42 billion in 2025 to USD 0.44 billion in 2026 and reach USD 0.58 billion by 2031, growing at a CAGR of 5.58% over 2026-2031.

This report is Segmented by Package Architecture (SMD, CSP, Flip-Chip LED Packages, and COB), Power Class (Low Power Less Than 0. 5 W, Mid Power 0. 5-1 W, and High Power Greater Than1 W), Application (Exterior Lighting, Interior Lighting, and More), Vehicle Type (Passenger Vehicles, and Commercial Vehicles), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Europe Automotive LED Package Market Trends and Insights

Rapid Shift From Halogen to LED Headlamps

UN Regulation 37 amendments in 2022 cleared the legal path for certified LED retrofit bulbs in halogen positions. In May 2025, ams OSRAM shipped the first ECE-approved H11 LED replacements, promising fivefold energy savings and six times longer life. A phased roadmap runs through 2028 to address the full halogen bulb family, opening a multiyear retrofit opportunity across Europe's 252 million-unit passenger fleet. Concurrently, OEMs like Stellantis have showcased compact Bi-LED modules that meet halogen photometry at lower cost and power, signaling parallel demand for cost-optimized LEDs in new entry vehicles. Package suppliers must therefore split portfolios between thermally robust retrofit formats and ultra-compact OEM solutions, each requiring different impedance and driver-IC strategies.

Growing Demand for Adaptive Front-Lighting Systems

UN Regulation 123 harmonization lowered homologation barriers for adaptive driving beam (ADB), shifting the feature from luxury to mass-market trims. Audi's 2026 Q3 debuts a micro-LED matrix with 25,600 pixels, while Nichia's three-tier Pixelated Light Source family lets OEMs scale from entry to premium ADB without new housings. Integrated Infineon LITIX drivers cut idle power by 50% during city cycles, meeting BEV efficiency targets. These architectures favor suppliers that combine LED epitaxy with ASIC co-design, accelerating a "winner-take-most" dynamic in high-pixel modules.

Volatility in Automotive Production Volumes Post-2025

European builds remain 3 million units below pre-pandemic peaks, with 100,000+ supplier jobs lost since 2024. UK output fell 15.5% in 2025 amid cyberattacks and tariff woes, and van plus truck registrations slid 8.8% and 6.2% respectively. Energy inflation, labor shortages, and just-in-time disruptions raise working-capital costs for LED makers, forcing those without diversified end markets to operate under-utilized cleanrooms that erode margins.

Other drivers and restraints analyzed in the detailed report include:

- Stringent EU CO2 Regulations Driving Energy-Efficient Lighting

- Mini-LED and Micro-LED Integration in Premium Models

- Thermal Management Challenges at Power Classes Above 1 W

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Chip-scale packages accounted for a rising slice of the Automotive LED package market size in 2025 and will out-grow legacy surface-mount devices through 2031. CSP attaches the die directly to the substrate, cutting thermal resistance and enabling pixel pitches fit for adaptive beams. Suppliers leverage CSP in micro-LED arrays where each die is <100 µm, limiting crosstalk while supporting >25,000-pixel matrices. Flip-chip variants offer superior current spreading for >10,000-candela headlamp beams yet demand void-free bonding, driving tighter process controls. Traditional SMD packages still dominate cost-sensitive daytime running lamps, but their share erodes as OEMs pivot to system-integrated solutions that combine LEDs and drivers on a single board. Chip-on-board remains the low-cost choice for entry reflectors, though its non-replaceability conflicts with EU circularity debates, a potential headwind to wide adoption.

The Automotive LED package market share leader in 2025 remained SMD, yet CSP's 6.01% CAGR gives it the steepest trajectory. High-pixel adaptive lighting, digital signage, and grille illumination all benefit from CSP's lower Z-height and thermal path, allowing thinner lamp profiles that improve aerodynamics. Suppliers that bundle CSP dies with Infineon or NXP driver ASICs gain system stickiness, while those limited to commodity SMD risk compression. EU discussions around replaceable LED sources may even tilt volume back to modular formats, creating a three-way contest among SMD, CSP, and emerging plug-in LED engine standards.

High-power packages above 1 W contributed nearly 60% of Automotive LED package market revenue in 2025 as UN Regulation 112 flux thresholds lock headlamps into high-luminous systems. Premium ADB modules routinely exceed 2,000 lumens and thus require cleaning and leveling, activities best met by single high-power dies rather than many mid-power chips, simplifying optics and wiring. Mid-power LEDs fill cornering and signal niches where intensity demands are moderate, but their unit volumes cannot offset falling prices. Low-power LEDs remain vital for ambient interiors and cluster backlighting; however, ISELED smart RGB devices blur the line by embedding drivers, which shifts value from discrete packages to semiconductor-integrated lights.

High-power dominance will persist, with a 5.94% CAGR driven by projection headlamps and micro-LED arrays, yet thermal ceilings are real. Suppliers integrate vapor chambers or graphite sheets to keep junctions under 125 °C, a requirement for L70 lifetime beyond 25,000 hours. Vendors unable to manage >10 W per square centimeter risk exclusion from next-gen headlamps. Conversely, low-power interior LEDs thrive on BEV demand for customizable cabins and energy savings, with addressable RGB strips enabling over-the-air themes that synchronize with infotainment.

List of Companies Covered in this Report:

- ams OSRAM AG

- Nichia Corporation

- Lumileds Holding B.V.

- Seoul Semiconductor Co., Ltd.

- Samsung Electronics Co., Ltd.

- LG Innotek Co., Ltd.

- Cree LED

- Lite-On Technology Corporation

- Stanley Electric Co., Ltd.

- Toyoda Gosei Co., Ltd.

- EVERLIGHT Electronics Co., Ltd.

- Dominant Opto Technologies Sdn. Bhd.

- ROHM Co., Ltd.

- Lextar Electronics Corporation

- NationStar Optoelectronics Co., Ltd.

- Sanan Optoelectronics Co., Ltd.

- Refond Optoelectronics Co., Ltd.

- Hella GmbH & Co. KGaA

- Valeo S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Shift From Halogen to LED Headlamps

- 4.2.2 Growing Demand for Adaptive Front-Lighting Systems

- 4.2.3 Stringent EU CO2 Regulations Driving Energy-Efficient Lighting

- 4.2.4 Mini-LED and Micro-LED Integration in Premium Models

- 4.2.5 Supply Chain Localization Incentives in Eastern Europe

- 4.2.6 Automotive Cyber-Security Standards Requiring IR LEDs

- 4.3 Market Restraints

- 4.3.1 Volatility in Automotive Production Volumes Post-2025

- 4.3.2 Thermal Management Challenges at >1 W Power Class

- 4.3.3 Patent Cliffs and Ongoing LED IP Litigations in Europe

- 4.3.4 Rising Import Duties on Asian LED Packages After CBAM Roll-out

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Package Architecture

- 5.1.1 SMD (Surface Mount Device)

- 5.1.2 CSP (Chip Scale Package)

- 5.1.3 Flip-Chip LED Packages

- 5.1.4 COB (Chip-on-Board)

- 5.2 By Power Class

- 5.2.1 Low Power (<0.5 W)

- 5.2.2 Mid Power (0.5-1 W)

- 5.2.3 High Power (>1 W)

- 5.3 By Application

- 5.3.1 Exterior Lighting

- 5.3.2 Interior Lighting

- 5.3.3 Sensing / IR Applications

- 5.3.4 Other Applications (Signaling, minor)

- 5.4 By Vehicle Type

- 5.4.1 Passenger Vehicles

- 5.4.2 Commercial Vehicles

- 5.5 By Geography

- 5.5.1 United Kingdom

- 5.5.2 Germany

- 5.5.3 France

- 5.5.4 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ams OSRAM AG

- 6.4.2 Nichia Corporation

- 6.4.3 Lumileds Holding B.V.

- 6.4.4 Seoul Semiconductor Co., Ltd.

- 6.4.5 Samsung Electronics Co., Ltd.

- 6.4.6 LG Innotek Co., Ltd.

- 6.4.7 Cree LED

- 6.4.8 Lite-On Technology Corporation

- 6.4.9 Stanley Electric Co., Ltd.

- 6.4.10 Toyoda Gosei Co., Ltd.

- 6.4.11 EVERLIGHT Electronics Co., Ltd.

- 6.4.12 Dominant Opto Technologies Sdn. Bhd.

- 6.4.13 ROHM Co., Ltd.

- 6.4.14 Lextar Electronics Corporation

- 6.4.15 NationStar Optoelectronics Co., Ltd.

- 6.4.16 Sanan Optoelectronics Co., Ltd.

- 6.4.17 Refond Optoelectronics Co., Ltd.

- 6.4.18 Hella GmbH & Co. KGaA

- 6.4.19 Valeo S.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

汽車LED照明市場:依產品類型、技術、車輛類型及銷售管道分類-2026-2032年全球市場預測

汽車LED照明市場:依產品類型、技術、車輛類型及銷售管道分類-2026-2032年全球市場預測 全球汽車LED市場(2026年):照明與顯示產品趨勢

全球汽車LED市場(2026年):照明與顯示產品趨勢 汽車LED照明市場預測至2034年-依明位置、車輛類型、技術、銷售管道和地區分類的全球分析

汽車LED照明市場預測至2034年-依明位置、車輛類型、技術、銷售管道和地區分類的全球分析 汽車LED模組:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)汽車LED照明市場預測至2034年—按類型、銷售管道、安裝類型、應用和地區分類的全球分析英國汽車LED照明:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)

汽車LED模組:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)汽車LED照明市場預測至2034年—按類型、銷售管道、安裝類型、應用和地區分類的全球分析英國汽車LED照明:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年) 2026年全球汽車LED照明市場報告日本汽車LED照明:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)

2026年全球汽車LED照明市場報告日本汽車LED照明:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年) 汽車LED照明市場-全球產業規模、佔有率、趨勢、機會、預測:按位置、車輛類型、自適應照明、地區和競爭格局分類,2021-2031年

汽車LED照明市場-全球產業規模、佔有率、趨勢、機會、預測:按位置、車輛類型、自適應照明、地區和競爭格局分類,2021-2031年 汽車LED照明市場規模、佔有率和成長分析(按技術類型、車輛類型、類型和地區分類)-產業預測(2026-2033年)

汽車LED照明市場規模、佔有率和成長分析(按技術類型、車輛類型、類型和地區分類)-產業預測(2026-2033年)