|

市場調查報告書

商品編碼

2065430

亞太地區員工福利技術:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)Asia-Pacific Benefits Technology - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

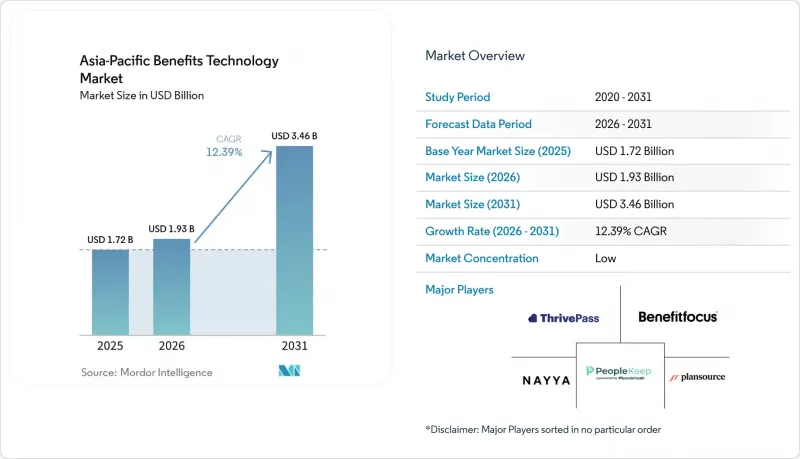

根據 Mordor Intelligence 預測,亞太地區員工福利技術市場規模將從 2025 年的 17.2 億美元成長到 2026 年的 19.3 億美元,然後在 2031 年達到 34.6 億美元,2026 年至 2031 年的複合年成長率為 12.39%。

本報告按元件(軟體、服務)、應用程式(例如員工福利管理)、部署模式(雲端、本地部署、混合部署)、組織規模(大型企業、中小企業)、最終用戶產業(例如銀行、金融服務和保險業)以及地區進行細分。市場預測以美元計價。

亞太地區員工福利技術市場趨勢與分析

基於雲端的人力資源和員工福利系統的現代化

在亞太地區的福利科技市場,雲端遷移正從長期計畫轉變為許多雇主的營運必要。雇主們正尋求將人力資源、薪資核算和福利功能遷移到一個統一的系統中,該系統能夠支援跨多個國家/地區的配置,而無需重複自訂。這項轉變意義重大,因為雲端平台使福利團隊能夠集中查看不同市場的使用模式、計畫註冊和管理例外。此外,亞太地區的福利科技市場的發展速度遠遠超過傳統的人力資源軟體生命週期。這是因為許多行動原生用戶將數位化管道作為存取福利的主要管道,而非作為輔助的桌面選項。住友金屬礦業採用Works Human Intelligence的整合平台「COMPANY」就是一個鮮明的例子。該平台將集團約7,000名員工整合到一個統一的人力資源平台中,取代了他們先前分散的系統。

實現註冊流程、合規性和薪資核算整合的自動化。

自動化是亞太地區福利技術市場的主要成長引擎。這是因為該地區的法律法規差異顯著,且各國法規的變更時間也各不相同。雇主通常需要在一個整合流程中處理員工登記、資格認定、薪資核算和報告等工作,但許多公司仍然依賴未整合的系統和人工交接來完成這些任務。當薪資上限、繳款規則和當地報告要求因國家而異,且更新時間不一時,這種營運模式就變得難以執行。因此,亞太地區福利科技市場對能夠將當地法律法規整合到產品中的平台的需求日益成長,而不是將核對工作留給內部團隊。 Ramco Systems指出,隨著雇主減少人工作業並整合薪資核算和福利工作流程,跨國薪資核算營運和人工智慧驅動的檢驗的重要性日益凸顯。隨著企業越來越重視合規的自動化和效率,預計市場將繼續發展。

健康和薪資資料中的資料隱私和網路安全風險

資料隱私是亞太地區福利科技市場面臨的一大障礙。這是因為健康和薪資數據經常在雇主、保險公司和薪資核算服務提供者共用的系統中流動。由於該地區缺乏統一的隱私框架,供應商必須根據不同國家/地區的具體情況自訂資料處理、儲存、通知和傳輸流程。因此,平台要實現跨國擴張,其最低產品標準(包括加密、存取控制、資料儲存位置設計和稽核準備)也隨之提高。對於小規模的SaaS供應商而言,挑戰更大,因為在收入達到區域規模之前,他們需要在本地化和安全方面投入更多資金。對於跨國公司而言,由於隱私審查如今會影響架構決策和合約條款,採購週期也不斷延長。

細分市場分析

預計到2025年,軟體將佔據亞太地區員工福利技術市場62.45%的佔有率,這意味著平台授權仍將是該地區最大的收入來源。這一主導地位反映了軟體主導的交付模式在員工註冊流程、合規管理、員工存取以及與薪資系統整合等方面發揮的關鍵作用。同時,隨著客戶日益需要無需耗時內部專案即可部署和在地化的平台,市場格局正在改變。目前,在亞太地區員工福利科技市場,供應商的價值不僅在於提供軟體,還在於提供跨多種語言、貨幣和國家法律體系的深度部署方案。

預計到2031年,服務業將以15.02%的複合年成長率成長,超過軟體產業。這凸顯了實施、整合、諮詢和支援服務日益成長的價值。這種轉變並非反映軟體需求的下降,而是因為許多雇主雖然已有多種產品選擇,但在跨多個國家實施時卻面臨諸多挑戰。因此,實施和整合服務正在推動亞太地區福利科技產業的需求顯著成長,尤其是在需要協調不同系統間的薪資核算和福利數據時。隨著區域監管政策的變化迫使雇主更新其薪資和福利邏輯,而非簡單地沿用現有的整合方案,這種需求變得更加迫切。 Ramco Systems在跨國薪資核算和基於人工智慧的檢驗的努力,正體現了這種更廣泛的服務需求,即僅靠產品本身,缺乏強大的整合能力,是遠遠不夠的。

到2025年,福利管理將佔亞太地區福利技術市場28.16%的佔有率,成為最大的應用層級。這個市場定位合理,因為註冊流程、資格驗證以及與保險公司和供應商的協調仍然是所有雇主實施福利計劃的基礎。雇主通常會在轉向更專業的模組之前,先實現這些工作流程的數位化。這確保了福利管理擁有廣泛的實施基礎,即使雇主正處於全面福利現代化改造的早期階段。

隨著雇主從標準化方案轉向員工主導的選擇模式,預計到2031年,彈性福利/個人化平台將以14.28%的複合年成長率成長。這項轉變的驅動力在於對決策支援、健康導航和更具針對性的福利溝通的需求不斷成長。怡安集團2025年的研究發現,許多跨國企業的員工希望在現有系統的基礎上獲得更高的個人化體驗。這解釋了為什麼選擇架構正成為平台發展藍圖的核心。此外,在亞太地區的福利科技市場,福利選擇、健康和溝通工具的融合趨勢日益明顯,促使許多供應商提供捆綁式的獎勵和互動功能,而不是單獨銷售模組。 CDP集團的「C-Benefits」平台正是這一趨勢的典型例證,該平台整合了商業保險、健康管理、靈活福利和獎勵服務,預計到2025年將為超過1000家公司和80萬名員工提供服務。隨著對個人化和整合的關注度不斷提高,福利科技市場有望迎來更多創新。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 基於雲端的人力資源和員工福利系統的現代化

- 實現註冊流程、合規性和薪資系統整合的自動化。

- 對行動優先的自助服務和員工福利體驗的需求

- 中小企業採用低成本SaaS員工福利平台

- 最佳化福利支付以因應醫療保健成本的通貨膨脹

- 亞太地區跨境法定福利的碎片化

- 市場限制因素

- 健康和薪資資料中的資料隱私和網路安全風險

- 將傳統人力資源資訊系統與薪資系統整合的複雜性

- 由於預算調整,新模組的淨採購已被推遲。

- 低利用率表明,福利和心理健康方面的訊號品質低。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章:預測市場規模與成長率

- 按組件

- 軟體

- 服務

- 部署和整合服務

- 諮詢和顧問服務

- 支援和維護服務

- 透過使用

- 員工福利管理

- 薪酬與獎勵管理

- 員工評估與敬業度平台

- 員工福利資訊提供和員工門戶

- 靈活的員工福利/個人化平台

- 其他用途

- 透過部署方法

- 基於雲端的

- 現場

- 混合

- 按組織規模

- 大公司

- 小型企業

- 按最終用戶行業分類

- 銀行、金融服務和保險業 (BFSI)

- IT/通訊

- 醫學與生命科學

- 製造業

- 零售與電子商務

- 公共部門/教育

- 其他終端用戶產業

- 按地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 東南亞

- 其他亞太國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Benefitfocus.com, Inc.

- Businessolver

- PlanSource Benefits Administration, Inc.

- bswift LLC

- Benefex Limited

- Employee Navigator

- PeopleKeep, Inc.

- ThrivePass, Inc.

- Darwinbox Digital Solutions Pvt. Ltd.

- Employment Hero Pty Ltd

- Bargain Technologies Private Limited

- Mednefits Singapore Pte. Ltd.

- Nayya Health, Inc.

- Forma Inc.

- League, Inc.

- Thanks Ben LTD

- SME HCI Limited

- Yu Life Ltd.

- Plum Benefits Insurance Brokers Pvt Ltd

- Invoq Loop Insurance Brokers Pvt Ltd

- Get Paz Insurance Brokers Pvt Ltd

第7章 市場機會與未來展望

According to Mordor Intelligence, the asia-Pacific benefits technology market size is expected to grow from USD 1.72 billion in 2025 to USD 1.93 billion in 2026 and is forecast to reach USD 3.46 billion by 2031 at 12.39% CAGR over 2026-2031.

This report is Segmented by Component (Software, and Services), Application (Benefits Administration, and More), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (Banking, Financial Services, and Insurance, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Benefits Technology Market Trends and Insights

Cloud-Based HR and Benefits Stack Modernization

Cloud migration has moved from a long-range plan to an operating need for many employers in the Asia-Pacific benefits technology market. Employers are trying to bring HR, payroll, and benefits functions onto unified systems that can support multi-country configurations without repeated custom builds. That shift matters because cloud platforms give benefit teams a single view of usage patterns, plan uptake, and administrative exceptions across different markets. The Asia-Pacific benefits technology market is also moving faster than older HR software cycles because many mobile-native workforces are accessing benefits digitally as their main channel rather than as a secondary desktop option. A clear example came when Sumitomo Metal Mining selected Works Human Intelligence's integrated COMPANY platform to unify around 7,000 group employees on a single HR foundation, replacing fragmented legacy arrangements.

Automation of Enrollment, Compliance, and Payroll Connectivity

Automation has become a major growth engine for the Asia-Pacific benefits technology market because statutory rules differ widely across the region and change on separate timelines. Employers often need one connected process for enrollment, eligibility, payroll calculation, and reporting, but many still run those tasks through disconnected systems or manual handoffs. That operating model becomes difficult when wage ceilings, contribution rules, and local filing requirements differ by country and are updated at different times of year. The Asia-Pacific benefits technology market is therefore seeing stronger demand for platforms that embed local statutory logic into the product, rather than leaving reconciliation work to internal teams. Ramco Systems highlighted that multi-country payroll operations and AI-supported verification are becoming more important as employers try to reduce manual effort and move toward connected payroll and benefits workflows. The market is expected to continue evolving as organizations increasingly prioritize automation and efficiency in compliance.

Data Privacy and Cybersecurity Exposure in Health and Payroll Data

Data privacy is a meaningful drag on the Asia-Pacific benefits technology market because health and payroll data move through systems that are often shared across employers, insurers, and payroll operators. The region does not operate under a single privacy framework, so vendors must adjust their data-handling, storage, notification, and transfer practices country by country. That raises the minimum product standard for encryption, access control, residency design, and audit readiness before a platform can scale across borders. Smaller SaaS vendors face a harder path because localization and security investment rise before revenue reaches regional scale. For multinational employers, the result is a slower buying cycle because privacy reviews now affect architectural decisions as much as contract terms.

Other drivers and restraints analyzed in the detailed report include:

- Mobile-First Self-Service and Benefits Experience Demand

- SME Adoption of Low-Cost SaaS Benefits Platforms

- Legacy HRIS and Payroll Integration Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software held 62.45% of the Asia-Pacific benefits technology market share in 2025, indicating that platform licenses still accounted for the largest revenue base in the region. That leadership reflects the strong role of software-led delivery models for enrollment, compliance management, employee access, and payroll connectivity. At the same time, the commercial center of gravity is shifting as customers increasingly need platforms that can be implemented and localized without lengthy internal projects. The Asia-Pacific benefits technology market is now rewarding vendors that can pair software with deployment depth across languages, currencies, and statutory frameworks.

Services are projected to expand at a 15.02% CAGR through 2031, faster than the software component, underscoring the value now in implementation, integration, advisory, and support work. The shift does not reflect weak software demand; it reflects the fact that many employers already have product options and instead struggle with execution across multiple countries. That is why implementation and integration services have become a core demand driver for the Asia-Pacific benefits technology industry, especially where payroll and benefits data must be reconciled across separate systems. Regional changes to statutory rules have added urgency, as employers have had to update payroll-benefit logic rather than leave older links in place. Ramco Systems' work around multi-country payroll and AI-based verification reflects this broader service demand, where the product alone is not enough without strong integration capability.

Benefits administration accounted for 28.16% of the Asia-Pacific benefits technology market in 2025, making it the largest application layer. That position is logical because enrollment, eligibility checks, and carrier or provider connectivity remain the foundation for every employer deployment. Employers usually digitize those workflows before they move into more specialized modules. This gives the administration layer a broad installed base, even when employers are still early in wider benefits modernization.

Flexible benefits and personalization platforms are projected to grow at a 14.28% CAGR through 2031 as employers move away from one-size-fits-all programs and toward employee-choice models. The shift is being reinforced by rising demand for decision support, health navigation, and more targeted benefit communication. A 2025 Aon research study found that many employees in multinational firms would trade their current arrangements for greater personalization, which helps explain why choice architecture is moving to the center of platform roadmaps. The Asia-Pacific benefits technology market is also seeing convergence among benefits selection, wellbeing, and communication tools, which is why many vendors now bundle recognition and engagement functions rather than sell isolated modules. CDP Group's C-Benefits platform exemplifies this direction by combining commercial insurance, health management, flexible benefits, and recognition services for more than 1,000 enterprises and 800,000 employees in 2025. The growing emphasis on personalization and integration is expected to drive further innovation in the benefits technology market.

List of Companies Covered in this Report:

- Benefitfocus.com, Inc.

- Businessolver

- PlanSource Benefits Administration, Inc.

- bswift LLC

- Benefex Limited

- Employee Navigator

- PeopleKeep, Inc.

- ThrivePass, Inc.

- Darwinbox Digital Solutions Pvt. Ltd.

- Employment Hero Pty Ltd

- Bargain Technologies Private Limited

- Mednefits Singapore Pte. Ltd.

- Nayya Health, Inc.

- Forma Inc.

- League, Inc.

- Thanks Ben LTD

- SME HCI Limited

- Yu Life Ltd.

- Plum Benefits Insurance Brokers Pvt Ltd

- Invoq Loop Insurance Brokers Pvt Ltd

- Get Paz Insurance Brokers Pvt Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-Based HR and Benefits Stack Modernization

- 4.2.2 Automation of Enrollment, Compliance, and Payroll Connectivity

- 4.2.3 Mobile-First Self-Service and Benefits Experience Demand

- 4.2.4 SME Adoption of Low-Cost SaaS Benefits Platforms

- 4.2.5 Medical Inflation-Led Benefits Cost Optimization

- 4.2.6 Cross-Border Statutory Benefits Fragmentation Across Asia-Pacific

- 4.3 Market Restraints

- 4.3.1 Data Privacy and Cybersecurity Exposure in Health and Payroll Data

- 4.3.2 Legacy HRIS and Payroll Integration Complexity

- 4.3.3 Budget Rebalancing Delaying Net-New Module Purchases

- 4.3.4 Low Utilization Signal Quality in Wellbeing and Mental Health Benefits

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.1.2.1 Implementation and Integration Services

- 5.1.2.2 Consulting and Advisory Services

- 5.1.2.3 Support and Maintenance Services

- 5.2 By Application

- 5.2.1 Benefits Administration

- 5.2.2 Compensation and Rewards Management

- 5.2.3 Employee Recognition and Engagement Platforms

- 5.2.4 Benefits Communication and Employee Portals

- 5.2.5 Flexible Benefits / Personalization Platforms

- 5.2.6 Other Applications

- 5.3 By Deployment Mode

- 5.3.1 Cloud-Based

- 5.3.2 On-Premises

- 5.3.3 Hybrid

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium-Sized Enterprises

- 5.5 By End-User Industry

- 5.5.1 Banking, Financial Services, and Insurance

- 5.5.2 IT and Telecommunications

- 5.5.3 Healthcare and Life Sciences

- 5.5.4 Manufacturing

- 5.5.5 Retail and E-Commerce

- 5.5.6 Public Sector and Education

- 5.5.7 Other End-User Industries

- 5.6 By Geography

- 5.6.1 China

- 5.6.2 Japan

- 5.6.3 India

- 5.6.4 South Korea

- 5.6.5 Australia and New Zealand

- 5.6.6 Southeast Asia

- 5.6.7 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Benefitfocus.com, Inc.

- 6.4.2 Businessolver

- 6.4.3 PlanSource Benefits Administration, Inc.

- 6.4.4 bswift LLC

- 6.4.5 Benefex Limited

- 6.4.6 Employee Navigator

- 6.4.7 PeopleKeep, Inc.

- 6.4.8 ThrivePass, Inc.

- 6.4.9 Darwinbox Digital Solutions Pvt. Ltd.

- 6.4.10 Employment Hero Pty Ltd

- 6.4.11 Bargain Technologies Private Limited

- 6.4.12 Mednefits Singapore Pte. Ltd.

- 6.4.13 Nayya Health, Inc.

- 6.4.14 Forma Inc.

- 6.4.15 League, Inc.

- 6.4.16 Thanks Ben LTD

- 6.4.17 SME HCI Limited

- 6.4.18 Yu Life Ltd.

- 6.4.19 Plum Benefits Insurance Brokers Pvt Ltd

- 6.4.20 Invoq Loop Insurance Brokers Pvt Ltd

- 6.4.21 Get Paz Insurance Brokers Pvt Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2026年全球員工福利管理軟體市場報告

2026年全球員工福利管理軟體市場報告 員工福利技術:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)歐洲員工福利管理:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

員工福利技術:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)歐洲員工福利管理:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年) 2026-2030年全球員工福利管理服務市場2026年全球福利與獎勵管理市場報告員工福祉平台:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)2026年全球福利管理軟體市場報告

2026-2030年全球員工福利管理服務市場2026年全球福利與獎勵管理市場報告員工福祉平台:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)2026年全球福利管理軟體市場報告 福利管理軟體市場規模、佔有率和成長分析(按部署類型、最終用戶、功能提供、定價模式和地區分類)-2026-2033年產業預測

福利管理軟體市場規模、佔有率和成長分析(按部署類型、最終用戶、功能提供、定價模式和地區分類)-2026-2033年產業預測 員工福利技術平台市場:按解決方案類型、部署模式、組織規模和行業垂直領域分類 - 2026-2032 年全球預測2025年全球社會福利管理服務市場報告

員工福利技術平台市場:按解決方案類型、部署模式、組織規模和行業垂直領域分類 - 2026-2032 年全球預測2025年全球社會福利管理服務市場報告