|

市場調查報告書

商品編碼

2064374

員工福祉平台:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Employee Wellbeing Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

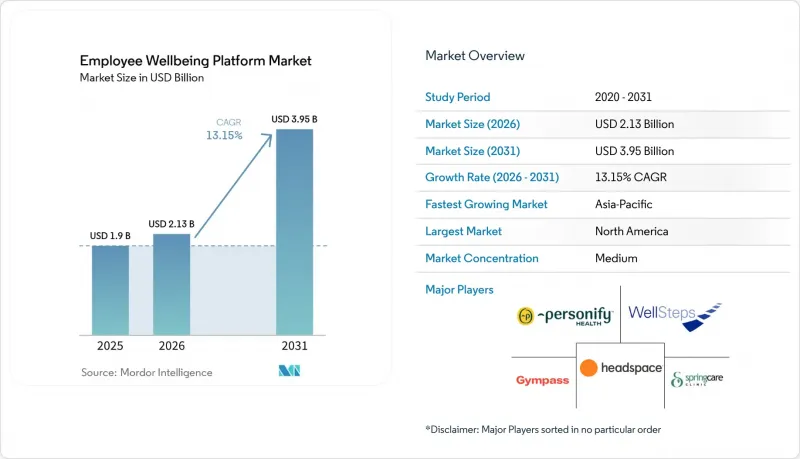

根據 Mordor Intelligence 預測,員工福祉平台市場規模預計在 2025 年達到 19 億美元,在 2026 年達到 21.3 億美元,在 2031 年達到 39.5 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 13.15%。

本報告按健康模組(例如,健康風險評估和篩檢)、部署方式(雲端部署、本地部署)、公司規模(大型企業、中小企業)、最終用戶行業(銀行、金融服務和保險、醫療保健/生命科學、零售/電子商務等)以及地區進行細分。市場預測以美元計價。

全球員工福祉平台市場趨勢及洞察。

知識型員工和第一線員工的職場壓力和職業倦怠感日益加劇。

壓力持續上升仍然是員工福祉平台市場短期成長要素。這是因為雇主比以往任何時候都更清楚地意識到工作環境對員工健康造成的傷害。根據2026年4月的報告,每年有超過84萬人死於與職場心理社會風險相關的疾病,經濟損失相當於全球GDP的1.37%。 2026年1月的一項調查發現,91%的英國成年人在過去一年中經歷了高度或極度壓力,35%的員工仍然不願向他們的直接主管傾訴壓力,這凸顯了建立私密數位管道的必要性。全球數據也揭示了雇主為何將心理健康置於支出決策的核心。憂鬱症和焦慮症每年導致120億個工作天的損失,造成1兆美元的生產力損失。員工福祉平台市場正在擴張,因為買家不再將倦怠視為抽象的文化問題,而是越來越尋求能夠識別風險、引導員工尋求關懷以及將計劃利用與業務成果聯繫起來的工具。

雇主要求降低醫療帳單成本、減少缺勤和減少帶病上班現象。

員工健康平台市場也正獲得雇主的青睞,他們希望更直接地了解與職場健康狀況下降相關的隱性成本。一項2025年的調查估計,美國雇主每年因員工倦怠造成的成本在每位員工3,999美元至20,683美元之間,其中89%的成本並非源於缺勤,而是源於「出勤主義」(即員工在崗但生產力下降)。這種成本結構意義重大,因為平台評估標準正從福利使用率轉向可衡量的醫療服務使用率、生產力和短期殘疾趨勢的變化。因此,雇主正在尋求一個平台能夠幫助減輕保險索賠壓力和緩解生產力下降的證據,這使得僅提供內容庫和基本健康挑戰的供應商面臨更高的進入門檻。事實上,在員工健康平台市場佔據主導地位的供應商是那些能夠將員工參與度轉化為可審計價值的供應商,因為買家需要能夠滿足其財務部門要求並在合約續約和成本審查中具有相關性的業績記錄。

員工敬業度持續低迷與投資報酬率證明之間的差距。

員工健康平台市場最大的商業性限制因素仍然是平台可用性與員工日常參與度之間的差距。 2025年下半年,儘管雇主支出持續成長,但只有29%的員工認為公司的健康計畫“良好”,低於2022年的41%。此外,2026年3月的報告指出,傳統的員工支援模式通常只能達到5%到10%的參與率,許多新興平台也難以將月參與率維持在30%以上。這一上限削弱了續約時的商業價值,因為低參與率難以令人信服地證明保險索賠的減少和生產力的提高。如果供應商未能將參與度與財務績效掛鉤,那麼當雇主削減開支時,他們更有可能轉而討論可自由支配的預算分配問題。這個問題減緩了員工健康平台市場的成長。這是因為成長不僅取決於採用率,還取決於雇主是否相信員工會在服務推出後繼續使用。

細分市場分析

到2025年,心理健康和壓力管理將成為最大的模組,佔員工福祉平台市場的26.41%。這是因為雇主發現,未治療的心理健康問題與勞動生產力下降之間有直接關聯。與其他許多模組相比,這一觀點得到了更有力的證據支持。 2024年的一份報告指出,憂鬱症和焦慮症每年導致120億個工作日損失和1兆美元的生產力損失,這也解釋了為什麼雇主們持續重視這一領域。在員工福祉平台市場中,該模組還提供了一條通往臨床指導治療、輔導和數位化分診的清晰路徑,這使得購買者更容易從實際效果的角度證明其支出的合理性。

「財務健康」是成長最快的模組,預計從2026年到2031年將以15.92%的複合年成長率成長。這是因為員工的財務負擔正日益影響其績效、留任率和福利使用。雇主正在擴大支持範圍,不再局限於體能活動和營養管理,尤其是在員工面臨債務壓力、對通貨膨脹敏感以及擔心自付醫療費用的情況下。這種轉變迫使供應商除了提供心理和生理健康服務外,還要提供財務管理支援、債務指導和福利使用支援。雖然健身和體能訓練、營養和體重管理以及健康風險評估等模組仍然很重要,但它們面臨著與慢性病管理和藥物支援相關的福利項目的競爭。睡眠健康和社交聯繫等其他模組也越來越受到關注。這是因為員工健康平台行業正在從單純關注工作量轉向更全面地觀點職業倦怠,包括恢復、隔離和日常壓力暴露。

到2025年,基於雲端的部署將佔據員工福祉平台市場71.23%的佔有率,這一主導地位既反映了員工分佈的趨勢,也體現了軟體即服務(SaaS)模式的實際優勢。雇主更傾向於雲端交付,因為與高度客製化的本地部署環境相比,雲端交付能夠提供更便利的更新管理、更輕鬆地跨地域擴展用戶存取權限,以及更便捷地與人力資源系統整合。這種模式也符合當前的採購趨勢,能夠實現快速部署,減輕內部IT部門的負擔,並為員工提供更一致的存取權限,無論他們是在辦公室還是遠距辦公。在員工福祉平台市場,對於那些希望在不為每個地區建立本地基礎設施的情況下實現廣泛覆蓋的企業而言,雲端部署正逐漸成為標準配置。

在政府機構、國防和某些受監管的金融服務業,本地部署仍然發揮著重要作用,因為這些行業的資料處理法規更為嚴格,內部控制仍然是強制性要求。然而,混合部署正成為最具活力的架構,預計到2031年將以14.38%的複合年成長率成長,因為跨國公司既需要覆蓋範圍,也需要對敏感資料進行更嚴格的控制。混合配置使供應商能夠簡化員工體驗,同時讓買家更好地控制特定記錄的處理或儲存位置。這種平衡在歐洲至關重要,因為資料主權和員工資料權利不僅要接受選型後的法律審查,而且也是採購討論的一部分。因此,儘管員工福祉平台產業仍然基於雲端,但成長越來越受到能夠降低跨境風險和縮短內部核准週期的架構的驅動,從而催生出更多多層部署。

區域分析

北美將成為最大的區域市場,到2025年將佔據員工健康平台市場的37.92%。這主要歸功於全部區域雇主提供的健康保險與人事費用管理之間的緊密聯繫。美國仍然是核心市場,其採購行為傾向於那些能夠在醫療保健成本壓力、心理健康服務和日常生產力支持方面展現價值的平台。這一趨勢迫使供應商拓展服務範圍,超越傳統的健康內容,涵蓋醫療導航、慢性病支援以及與福利工作流程的更直接整合。加拿大在員工健康平台市場也佔有重要地位。這得益於透過收購擴大市場規模,從而增加投保人數和供應商覆蓋範圍。 2025年5月的一項5億加元(扣除債務準備金後淨額為3.5億美元)的收購表明,隨著買家尋求更廣泛的服務深度和對跨國公司的支持,區域規模的重要性日益凸顯。

在墨西哥,隨著雇主開始履行與社會心理風險相關的法律義務,市場正向合規主導階段轉變,本地買家群體也從大型企業擴展到更廣泛的範圍。這一點意義重大,因為該地區的趨勢不再局限於美國公司和跨國公司總部,而是擴大涵蓋了需要更方便的實施和在地化支援的中型企業。因此,北美員工福祉平台市場整合了成熟的企業需求和與法規及勞動力穩定相關的新實施路徑。亞太地區是成長最快的地區,預計2026年至2031年的複合年成長率將達到16.73%,使其成為眾多供應商最重要的成長支柱。印度的成長主要得益於正式的合規變化,以及雇主對預防性醫療保健、零工經濟支持和數位化服務交付的關注,儘管買家在產品深度和投資回報率衡量方面仍存在差異。

亞太地區的市場現況主要受辦公室和外勤人員持續存在的職業倦怠風險所驅動,導致東南亞、日本、韓國、澳洲和紐西蘭等地區的需求持續高漲。 2026年3月澳洲的一系列收購表明,供應商認為該地區市場規模足夠大,足以支持整合和平台擴展。同時,歐洲的需求環境更為規範,資料處理、員工諮詢和GDPR合規性等要求與產品廣度一樣,都是選擇供應商的重要因素。這為能夠提供區域性資料處理、正式隱私文件和更具本地化客製化的部署模式的供應商創造了切實可行的進入機會。除歐洲外,中東地區的重要性日益凸顯,員工福祉工具正逐漸成為更廣泛的人才發展計畫的一部分。另一方面,非洲仍處於應用初期,目前主要依賴保險公司、跨國公司和數位化員工支援服務來建構員工福祉平台市場的第一層需求。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 知識型員工和第一線員工的職場壓力和職業倦怠感日益加劇。

- 雇主需要透過消除醫療帳單、減少缺勤和提高工作效率來降低成本。

- 混合式和分散式工作模式正在推動以數位化為先導的健康福祉的實現。

- 透過人工智慧、分析和穿戴式裝置實現個人化介入和可衡量的結果。

- 社會心理風險管治:將福祉指標轉化為採購標準

- GLP-1 與慢性病獲益管理:拓展平台的應用範圍

- 市場限制因素

- 員工敬業度持續偏低與投資報酬率體現之間的差距。

- 涉及敏感員工健康資料的隱私和網路安全問題

- 員工代表委員會的審核流程和資料本地化正在減緩多個國家的推廣速度。

- HCM套件的捆綁銷售和人工智慧功能的模仿給獨立平台的預算帶來了壓力。

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章:預測市場規模與成長率

- 健康模組

- 健康風險評估與篩檢

- 心理健康與壓力管理

- 健身和體育活動

- 營養與體重管理

- 財務健康

- 其他健康模組

- 透過部署方法

- 基於雲端的

- 現場

- 按公司規模

- 大公司

- 小型企業

- 按最終用戶行業分類

- 銀行、金融服務和保險業 (BFSI)

- 醫學與生命科學

- 零售與電子商務

- 工業/製造業

- 政府/公共部門

- 教育

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲和紐西蘭

- 韓國

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介。

- Personify Health, Inc.

- Wellable LLC

- Gympass US, LLC

- Modern Life, Inc.

- Spring Care, Inc.

- Lyra Health, Inc.

- Headspace Inc.

- Unmind Ltd

- Kyan Health AG

- WellSteps, LLC

- yuMuuv OU

- Burnalong, Inc.

- WellRight, Inc.

- ADURO, Inc.

- MediKeeper, Inc.

- CoreHealth Technologies Inc.

- BetterUp, Inc.

- OpenUp BV

- With Juno Ltd

- Thrive Global Holdings, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the employee wellbeing platform market size is projected to be USD 1.90 billion in 2025, USD 2.13 billion in 2026, and reach USD 3.95 billion by 2031, growing at a CAGR of 13.15% from 2026 to 2031.

This report is Segmented by Wellbeing Module (Health Risk Assessment and Screening, and More), Deployment Model (Cloud-Based and On-Premises), Enterprise Size (Large Enterprises and Small and Medium-Sized Enterprises), End-User Industry Vertical (BFSI, Healthcare and Life Sciences, Retail and E-Commerce, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Employee Wellbeing Platform Market Trends and Insights

Rising Workplace Stress And Burnout Across Knowledge And Frontline Roles

Rising stress remains the strongest near-term growth driver in the employee wellbeing platform market, as employers now face a much clearer record of harm tied to work conditions. In April 2026, it was reported that more than 840,000 deaths each year were linked to psychosocial workplace risks, with annual economic losses equal to 1.37% of global GDP. In January 2026, surveys showed that 91% of UK adults experienced high or extreme stress in the previous year, and 35% of workers remained uncomfortable disclosing their stress to line managers, which strengthens the case for private digital pathways. Global data has also shown why employers place mental health near the center of spending decisions, since depression and anxiety cause 12 billion lost working days each year and result in USD 1 trillion in lost productivity. The employee well-being platform market is benefiting because buyers no longer see burnout as an abstract cultural issue and increasingly want tools that can identify risk, guide members into care, and connect program use with business outcomes.

Employer Demand To Reduce Healthcare Claims, Absenteeism, And Presenteeism Costs

The employee well-being platform market is also gaining support from employers seeking a more direct handle on the hidden costs of poor health at work. A 2025 study estimated burnout costs to U.S. employers at USD 3,999 to USD 20,683 per worker each year, and 89% of that burden came from presenteeism rather than absence. That cost mix matters because it shifts platform evaluation away from benefit participation and toward measurable change in care use, productivity, and short-term disability patterns. Employers are therefore asking for proof that a platform can help lower claims pressure and reduce lost output, which is raising the bar for vendors that only offer content libraries or basic wellness challenges. In practice, the stronger vendors in the employee wellbeing platform market are those that can translate engagement into auditable value, since buyers want a finance-ready case that holds up during renewal cycles and cost reviews.

Low Sustained Employee Engagement And ROI Proof Gaps

The largest commercial restraint in the employee well-being platform market remains the gap between platform availability and regular employee use. In late 2025, only 29% of employees rated their company's wellness programs as good, down from 41% in 2022, even though employer spending continued to rise. In March 2026, it was also noted that older employee assistance models typically achieved only 5% to 10% utilization, and many newer platforms still struggle to maintain monthly engagement above 30%. That ceiling weakens the business case at renewal because low usage makes it harder to credibly demonstrate reductions in claims or improvements in productivity. Vendors that cannot connect engagement with finance-grade outcomes are more likely to fall back into discretionary budget discussions when employers tighten spending. This issue slows the employee wellbeing platform market because growth depends not only on adoption, but also on whether employers believe employees will keep using the service after launch.

Other drivers and restraints analyzed in the detailed report include:

- Hybrid And Distributed Work Models Favoring Digital-First Wellbeing Delivery

- AI, Analytics, And Wearables Enabling Personalized Interventions And Measurable Outcomes

- Sensitive Workforce Health Data Privacy And Cybersecurity Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mental health and stress management accounted for 26.41% of the employee wellbeing platform market in 2025, making it the largest module, as employers see a direct connection between untreated mental health issues and lost work output. A stronger evidence base than many other modules supports that position. In 2024, it was reported that depression and anxiety lead to 12 billion lost working days every year and cost USD 1 trillion in productivity, which helps explain why employers keep prioritizing this part of the offer. In the employee wellbeing platform market, this module also benefits from a clearer pathway to clinically guided therapy, coaching, and digital triage, making it easier for buyers to justify spend in terms of outcomes.

Financial well-being is the fastest-growing module and is projected to expand at a 15.92% CAGR from 2026 to 2031, because employee financial strain increasingly affects performance, retention, and benefit use. Employers are broadening the scope of support beyond physical activity and nutrition, especially where debt pressure, inflation sensitivity, and out-of-pocket healthcare concerns weigh on the workforce. This change is pushing vendors to offer budgeting support, debt guidance, and benefit navigation alongside mental and physical health services. Fitness and physical activity, nutrition and weight management, and health risk assessment modules still matter, but they face more competition from benefit programs tied to chronic condition management and medication support. Other modules, including sleep health and social connection, are also gaining attention as the employee wellbeing platform industry moves toward a fuller view of burnout that includes recovery, isolation, and daily stress exposure, rather than focusing solely on workload.

Cloud-based deployment held 71.23% of the employee wellbeing platform market share in 2025, and that lead reflects both workforce distribution and the practical advantages of software delivered as a service. Employers prefer cloud delivery because updates are easier to manage, user access is simpler to extend across locations, and integration with HR systems is more straightforward than in heavily customized local environments. This model also aligns with current buying patterns of faster rollouts, lighter internal IT lift, and more consistent employee access across offices and remote settings. In the employee wellbeing platform market, cloud deployment has become the standard for organizations seeking broad coverage without building local infrastructure in each geography.

On-premises deployment still has a place in parts of government, defense, and regulated financial services where data-handling rules are stricter and internal controls remain a hard requirement. Even so, hybrid deployment is emerging as the most dynamic architecture and is projected to grow at a 14.38% CAGR through 2031, as multinational employers seek both reach and tighter control over sensitive data. Hybrid configurations let vendors keep the employee-facing experience simple while giving buyers more say over where certain records are processed or stored. That balance matters in Europe, where data sovereignty and employee data rights have become part of the buying conversation, not just an issue for legal review after selection. The result is a more layered deployment picture in which the employee wellbeing platform industry still runs on cloud delivery, but growth increasingly comes from architectures that reduce cross-border risk and shorten internal approval cycles.

Geography Analysis

North America held 37.92% of the employee wellbeing platform market share in 2025, making it the largest regional market, as employer-sponsored healthcare and workforce cost management are closely linked across the region. The United States remains the anchor market, and its buyer behavior favors platforms that can show value in terms of medical cost pressure, mental health access, and daily productivity support. That pattern has pushed vendors to broaden their offerings beyond classic wellness content to include care navigation, chronic condition support, and more direct integration with benefits workflows. Canada is also important to the employee wellbeing platform market because scale is rising through acquisitions that expand covered lives and provider reach. In May 2025, a CAD 500 million acquisition (USD 350 million net of assumed debt) showed that regional scale is becoming increasingly important as buyers seek broader service depth and multinational support.

Mexico is moving into a more compliance-driven phase as employers respond to psychosocial risk obligations, which is widening the local buyer pool beyond very large organizations. This matters because the regional story is no longer limited to large U.S. employers and multinational headquarters, and it increasingly includes medium-sized employers that need easier deployment and localized support. The employee well-being platform market in North America, therefore, combines mature enterprise demand with newer adoption paths tied to regulation and workforce stabilization. Asia-Pacific is the fastest-growing region, projected to expand at a 16.73% CAGR from 2026 to 2031, making it the most important growth corridor for many vendors. Growth in India is being supported by formal compliance changes and by employer interest in preventive health, gig worker support, and digital service delivery, even though product depth and ROI measurement remain uneven across buyers.

The broader Asia-Pacific picture is strengthened by persistent burnout exposure across both office and frontline workforces, which keeps demand elevated across Southeast Asia, Japan, South Korea, Australia, and New Zealand. In March 2026, multiple acquisitions in Australia showed that vendors see the region as large enough to justify consolidation and platform scale-building. Europe presents a more regulated demand environment, where data handling, employee consultation, and GDPR expectations shape vendor selection as much as product breadth. That creates a practical opening for providers that can offer regional data processing, formal privacy documentation, and a more localized deployment model. Outside Europe, the Middle East is gaining relevance as well-being tools become part of broader workforce development agendas, while Africa remains earlier in adoption and depends more heavily on insurers, multinationals, and digital employee assistance services to build the first layer of demand in the employee well-being platform market.

- Personify Health, Inc.

- Wellable LLC

- Gympass US, LLC

- Modern Life, Inc.

- Spring Care, Inc.

- Lyra Health, Inc.

- Headspace Inc.

- Unmind Ltd

- Kyan Health AG

- WellSteps, LLC

- yuMuuv OU

- Burnalong, Inc.

- WellRight, Inc.

- ADURO, Inc.

- MediKeeper, Inc.

- CoreHealth Technologies Inc.

- BetterUp, Inc.

- OpenUp B.V.

- With Juno Ltd

- Thrive Global Holdings, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Workplace Stress and Burnout Across Knowledge and Frontline Roles

- 4.2.2 Employer Demand to Reduce Healthcare Claims, Absenteeism, and Presenteeism Costs

- 4.2.3 Hybrid and Distributed Work Models Favoring Digital-First Wellbeing Delivery

- 4.2.4 AI, Analytics, and Wearables Enabling Personalized Interventions and Measurable Outcomes

- 4.2.5 Psychosocial Risk Governance Turning Wellbeing Metrics Into Procurement Criteria

- 4.2.6 GLP-1 and Chronic Condition Benefit Management Expanding Platform Scope

- 4.3 Market Restraints

- 4.3.1 Low Sustained Employee Engagement and ROI Proof Gaps

- 4.3.2 Sensitive Workforce Health Data Privacy and Cybersecurity Concerns

- 4.3.3 Works Council Reviews and Data Localization Slowing Multicountry Rollouts

- 4.3.4 HCM Suite Bundling and AI Feature Copycats Compressing Standalone Platform Budgets

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS, VALUE (USD)

- 5.1 By Wellbeing Module

- 5.1.1 Health Risk Assessment and Screening

- 5.1.2 Mental Health and Stress Management

- 5.1.3 Fitness and Physical Activity

- 5.1.4 Nutrition and Weight Management

- 5.1.5 Financial Wellbeing

- 5.1.6 Other Wellbeing Modules

- 5.2 By Deployment Model

- 5.2.1 Cloud-Based

- 5.2.2 On-Premises

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-Sized Enterprises

- 5.4 By End User Industry Vertical

- 5.4.1 BFSI

- 5.4.2 Healthcare and Life Sciences

- 5.4.3 Retail and E-commerce

- 5.4.4 Industrial Manufacturing

- 5.4.5 Government and Public Sector

- 5.4.6 Education

- 5.4.7 Other End-user Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 Australia and New Zealand

- 5.5.4.5 South Korea

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 Personify Health, Inc.

- 6.4.2 Wellable LLC

- 6.4.3 Gympass US, LLC

- 6.4.4 Modern Life, Inc.

- 6.4.5 Spring Care, Inc.

- 6.4.6 Lyra Health, Inc.

- 6.4.7 Headspace Inc.

- 6.4.8 Unmind Ltd

- 6.4.9 Kyan Health AG

- 6.4.10 WellSteps, LLC

- 6.4.11 yuMuuv OU

- 6.4.12 Burnalong, Inc.

- 6.4.13 WellRight, Inc.

- 6.4.14 ADURO, Inc.

- 6.4.15 MediKeeper, Inc.

- 6.4.16 CoreHealth Technologies Inc.

- 6.4.17 BetterUp, Inc.

- 6.4.18 OpenUp B.V.

- 6.4.19 With Juno Ltd

- 6.4.20 Thrive Global Holdings, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2026年全球員工福利管理軟體市場報告

2026年全球員工福利管理軟體市場報告 員工福利技術:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)歐洲員工福利管理:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

員工福利技術:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)歐洲員工福利管理:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年) 2026-2030年全球員工福利管理服務市場2026年全球福利與獎勵管理市場報告亞太地區員工福利技術:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)2026年全球福利管理軟體市場報告

2026-2030年全球員工福利管理服務市場2026年全球福利與獎勵管理市場報告亞太地區員工福利技術:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)2026年全球福利管理軟體市場報告 福利管理軟體市場規模、佔有率和成長分析(按部署類型、最終用戶、功能提供、定價模式和地區分類)-2026-2033年產業預測

福利管理軟體市場規模、佔有率和成長分析(按部署類型、最終用戶、功能提供、定價模式和地區分類)-2026-2033年產業預測 員工福利技術平台市場:按解決方案類型、部署模式、組織規模和行業垂直領域分類 - 2026-2032 年全球預測2025年全球社會福利管理服務市場報告

員工福利技術平台市場:按解決方案類型、部署模式、組織規模和行業垂直領域分類 - 2026-2032 年全球預測2025年全球社會福利管理服務市場報告