|

市場調查報告書

商品編碼

2064532

後處理:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Post-Harvest Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

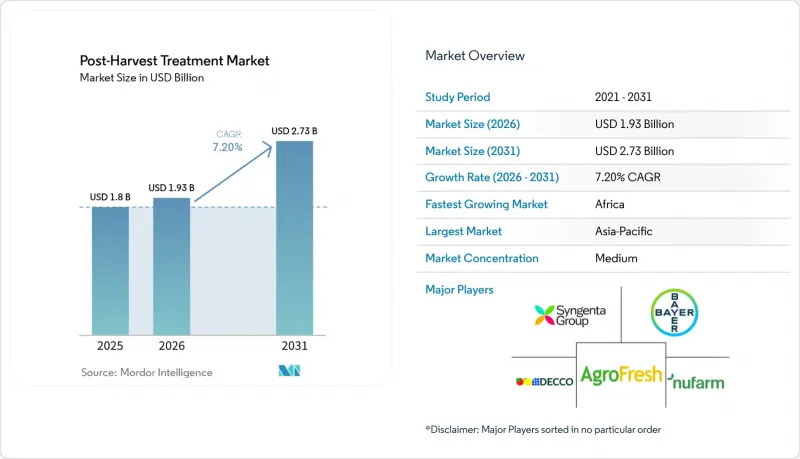

據 Mordor Intelligence 稱,2025 年收穫後後處理市場價值 18 億美元,預計將從 2026 年的 19.3 億美元成長到 2031 年的 27.3 億美元,2026 年至 2031 年的複合年成長率為 7.20%。

本報告按處理類型(塗料和薄膜、洗滌劑、殺菌劑、乙烯抑制劑等)、劑型(液體、粉末、氣體)、作物類型(水果、蔬菜、穀物等)、原料(天然、合成)和地區(北美、南美、歐洲、亞太、中東和非洲)進行細分。市場預測以美元計價。

全球收穫後後處理市場趨勢及洞察

新興市場低溫運輸的擴張

冷藏基礎設施不足持續造成嚴重的採後損失,凸顯了低溫運輸基礎設施的必要性。根據聯合國糧食及農業組織(糧農組織)統計,每年有5.26億噸糧食因冷藏不足而損失,約佔全球糧食產量的12%。這強調了投資建造冷藏倉庫、分類設施和物流網路以改善生鮮農產品處理流程的必要性。此類投資也將有助於推廣殺菌劑、塗層和乙烯控制技術等採後後處理解決方案,最終推動市場需求。

超級市場需遵守嚴格的殘留物標準

主要零售市場對農藥殘留量的限制日益嚴格,提高了生產商和出口商的合規要求。例如,歐盟委員會根據第2025/1163號條例,將馬鈴薯中氯丙胺的最大殘留基準值從0.35毫克/公斤降至0.2毫克/公斤。這一降幅反映了食品安全標準日益嚴格、允許殘留量降低的整體監管趨勢。因此,生產商正在採用精準噴灑技術、符合殘留限量標準的殺菌劑以及生物基採後後處理,以滿足零售商的要求,這也推動了採後後處理市場的成長。

加強對某些消毒劑的監管

隨著監管機構實施更嚴格的安全和風險降低措施,對合成殺菌劑的監管力道也不斷加強。 2025年1月,美國環保署(EPA)宣布了Chlorothalonil、Thiophanate methyl和Carbendazim的初步登記審查決定,並發布了新的法規以降低其對人類健康和環境的潛在風險。這些措施符合農藥監管日益嚴格以及對常用殺菌劑進行重新評估的總體趨勢。隨著合規要求的日益嚴格,生產商正在投資研發更安全的配方和替代方案,這導致產品系列發生變化,並影響著採後後處理市場的成長模式。

細分市場分析

預計到2025年,塗層和薄膜領域將佔據採後後處理市場41.0%的佔有率,凸顯其在維持蔬果新鮮度和最大限度減少水分流失方面的重要作用。這些解決方案因其與現有供應鏈的兼容性以及符合出口標準而被廣泛應用。對符合殘留物標準和生物基塗層的需求不斷成長,進一步鞏固了其市場地位,尤其是在食品安全法規嚴格且有機產品消費量不斷成長的地區。

預計2026年至2031年間,發芽抑制劑細分市場的採後後處理市場規模將以10.8%的複合年成長率(CAGR)高速成長,主要受馬鈴薯和洋蔥等長保存期限作物需求成長的推動。對傳統化學品的監管限制正在加速向更安全、更有效的替代發芽抑制劑方法的轉變。此外,乙烯抑制劑和殺菌劑在保鮮策略中繼續發揮重要作用,而清潔和消毒劑在確保採後後處理設施的衛生標準方面也變得越來越重要。

截至2025年,液體製劑仍將維持其最大的市場佔有率,佔採後後處理市場58.0%的佔有率。這主要得益於其在包裝廠噴灑和浸泡等應用中的廣泛使用。這些製劑因其易於施用、覆蓋均勻以及與現有基礎設施的高度相容性而備受青睞。它們適用於多種作物和處理方法,鞏固了其在商業性採後後處理作業中的主導地位。

受控氣調儲槽和乙烯管理系統日益普及的推動,預計氣體配方儲槽市場將在2026年至2031年間以9.4%的複合年成長率實現最高增速。由於能夠精確控制成熟和腐敗過程,這些配方儲罐在長途貿易中尤其重要。同時,粉末配方儲槽在糧食儲存領域的需求依然穩定,隨著管理機制的進步,其效率和效果也不斷提升。

區域分析

到2025年,亞太地區將佔據全球33.0%的採後後處理市場佔有率,這主要得益於農業生產的擴張和低溫運輸基礎設施投資的增加。中國和印度等國家正在加強其採後後處理體系,以最大限度地減少食物浪費並提升出口競爭力。塗層和氣調貯藏等先進保鮮技術的日益普及進一步推動了該地區的需求。此外,快速的都市化和生鮮食品消費量的成長也促進了採後後處理解決方案在整個供應鏈中的整合。

預計非洲將呈現最高的成長率,2026年至2031年複合年成長率將達到9.7%,主要得益於各方努力減少嚴重的收穫後損失並加強糧食安全。各國政府和國際組織正在投資建設倉儲基礎設施並推動供應鏈現代化。園藝產品出口的擴大和人們對保鮮技術的日益了解,都促進了市場成長。儘管基礎設施仍存在差距,但冷藏和處理設施的改善正逐步推動收穫後後處理解決方案在全部區域的實施。

由於先進的農業技術和嚴格的食品安全法規結構,預計到2025年,北美將在全球銷售額中佔據重要佔有率。對農藥殘留和食品安全合規性的監管日益嚴格,促使生產商和經銷商採用更有效的保鮮方案。該地區成熟的零售和出口導向供應鏈要求延長保存期限並維持產品品質穩定。這導致國內外市場擴大採用塗層、殺菌劑和乙烯控制技術,以最大限度地減少腐敗、提高儲存效率並滿足嚴格的食品安全標準。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 新興市場低溫運輸的擴張

- 超級市場需遵守嚴格的殘留物標準

- 氣調包裝線的廣泛應用

- 食品級抗菌塗層的應用日益廣泛

- 電子商務食品履約中心的興起

- 人工智慧驅動的保存期限預測與分析

- 市場限制因素

- 加強對某些消毒劑的監管

- 消費者對合成化學品的抗拒情緒日益高漲

- 生物基原物料價格波動

- 開發中國家收穫後機械化程度的差異

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 治療類型

- 塗層和薄膜

- 清潔劑

- 消毒劑

- 乙烯抑制劑

- 發芽抑制劑

- 其他

- 配方

- 液體

- 粉末

- 氣體

- 按作物類型

- 水果

- 蔬菜

- 糧食

- 花卉和觀賞植物

- 按原產地

- 自然的

- 合成

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 其他北美國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Syngenta AG

- AgroFresh Solutions, Inc.

- Bayer AG

- Decco Post-Harvest Inc.(UPL Limited)

- Nufarm Limited

- John Bean Technologies Corporation

- Xeda International SA

- Citrosol, SA

- Fomesa Fruitech, SLU

- bio-ferm GmbH(Andermatt Group AG)

- Lytone Enterprise, Inc.

- Janssen PMP(Janssen Pharmaceutica NV)

第7章 市場機會與未來展望

According to Mordor Intelligence, the post-harvest treatment market size was valued at USD 1.80 billion in 2025 and is projected to grow from USD 1.93 billion in 2026 to USD 2.73 billion by 2031, registering a CAGR of 7.20% between 2026 and 2031.

This report is Segmented by Treatment Type (Coatings and Films, Cleaners, Fungicides, Ethylene Blockers, and More), by Formulation (Liquid, Powder, and Gas), by Crop Type (Fruits, Vegetables, Grains, and More), by Origin (Natural and Synthetic), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Post-Harvest Treatment Market Trends and Insights

Cold-chain Expansion in Emerging Markets

Inadequate refrigeration infrastructure continues to result in substantial post-harvest losses, emphasizing the need for cold-chain development. According to the Food and Agriculture Organization (FAO), 526 million metric tons of food, accounting for approximately 12% of global production, are lost due to insufficient refrigeration. This highlights the necessity of investing in cold storage facilities, packhouses, and logistics networks to improve the handling of perishable produce. Such investments also facilitate the adoption of post-harvest treatment solutions, including fungicides, coatings, and ethylene management technologies, thereby driving market demand.

Stringent Supermarket Residue Specifications

Stringent residue specifications in major retail markets are increasing compliance demands on growers and exporters. For instance, the European Commission has reduced the maximum residue level for chlorpropham in potatoes from 0.35 mg/kg to 0.2 mg/kg under Regulation (EU) 2025/1163. This reduction reflects a broader regulatory trend toward stricter food safety standards and lower tolerance levels. Consequently, producers are adopting precision application technologies, residue-compliant fungicides, and bio-based post-harvest treatments to meet retailer requirements, driving growth in the post-harvest treatment market.

Regulatory Tightening on Certain Fungicides

Regulatory scrutiny of synthetic fungicides is increasing as authorities enforce stricter safety and risk mitigation measures. In January 2025, the United States Environmental Protection Agency issued interim registration review decisions for chlorothalonil, thiophanate-methyl, and carbendazim, introducing updated controls to mitigate potential risks to human health and the environment. These measures align with a broader trend of tightening pesticide regulations and reassessing commonly used fungicides. As compliance requirements grow more stringent, manufacturers are investing in safer formulations and alternative solutions, leading to changes in product portfolios and influencing growth patterns in the post-harvest treatment market.

Other drivers and restraints analyzed in the detailed report include:

- Proliferation of Controlled-Atmosphere Packaging Lines

- Increasing Adoption of Edible Antimicrobial Coatings

- Growing Consumer Resistance to Synthetic Chemicals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The coatings and films segment accounted for the largest 41.0% of the post-harvest treatment market share in 2025, highlighting their essential role in maintaining freshness and minimizing moisture loss in fruits and vegetables. These solutions are widely utilized due to their compatibility with existing supply chains and compliance with export standards. The growing demand for residue-compliant and bio-based coatings is further reinforcing their market position, particularly in regions with stringent food safety regulations and increasing consumption of organic produce.

The post-harvest treatment market size for the sprout inhibitors segment is projected to grow at the fastest CAGR of 10.8% from 2026 to 2031, driven by increasing demand in storage-intensive crops such as potatoes and onions. Regulatory limitations on traditional chemicals are accelerating the shift toward safer and alternative sprout control methods. Additionally, ethylene blockers and fungicides continue to play a key role in preservation strategies, while cleaners and disinfectants are gaining significance in ensuring hygiene standards across post-harvest handling facilities.

The liquid formulations segment held the largest 58.0% of the post-harvest treatment market share in 2025, driven by their extensive use in spray and dip applications within pack-houses. These formulations are favored for their ease of application, uniform coverage, and compatibility with existing infrastructure. Their versatility across various crop types and treatment methods supports their dominant role in commercial post-harvest operations.

The gas segment is projected to grow at the fastest CAGR of 9.4% from 2026 to 2031, fueled by the increasing adoption of controlled atmosphere storage and ethylene management systems. These formulations allow precise control over ripening and spoilage processes, making them particularly valuable in long-distance trade. Meanwhile, powder formulations continue to see steady demand in grain storage applications, with advancements in delivery mechanisms further improving their efficiency and effectiveness.

Geography Analysis

Asia-Pacific accounted for the largest 33.0% of the post-harvest treatment market share in 2025, driven by expanding agricultural output and increased investment in cold-chain infrastructure. Countries such as China and India are enhancing post-harvest handling systems to minimize food losses and boost export competitiveness. The growing adoption of advanced preservation technologies, such as coatings and controlled atmosphere storage, is further driving regional demand. Additionally, rapid urbanization and rising consumption of fresh produce are fostering the integration of post-harvest treatment solutions across supply chains.

Africa is projected to grow at the fastest CAGR of 9.7% from 2026 to 2031, supported by initiatives to reduce significant post-harvest losses and enhance food security. Governments and international organizations are investing in storage infrastructure and modernizing supply chains. The expansion of horticulture exports and increasing awareness of preservation technologies are contributing to market growth. While infrastructure gaps remain, improved access to cold storage and handling facilities is gradually enabling the adoption of post-harvest treatment solutions across the region.

North America also accounted for a significant share of global revenue in 2025, driven by advanced agricultural practices and strict regulatory frameworks related to food safety. Heightened regulatory focus on pesticide residues and food safety compliance is encouraging growers and distributors to implement more effective preservation solutions. The region's well-structured retail and export-oriented supply chains demand extended shelf life and consistent product quality. This has led to increased adoption of coatings, fungicides, and ethylene management technologies to minimize spoilage, enhance storage efficiency, and meet stringent food safety standards in both domestic and international markets.

- Syngenta AG

- AgroFresh Solutions, Inc.

- Bayer AG

- Decco Post-Harvest Inc. (UPL Limited)

- Nufarm Limited

- John Bean Technologies Corporation

- Xeda International S.A.

- Citrosol, S.A.

- Fomesa Fruitech, S.L.U.

- bio-ferm GmbH (Andermatt Group AG)

- Lytone Enterprise, Inc.

- Janssen PMP (Janssen Pharmaceutica NV)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cold-chain expansion in emerging markets

- 4.2.2 Stringent supermarket residue specifications

- 4.2.3 Proliferation of controlled-atmosphere packaging lines

- 4.2.4 Increasing adoption of edible antimicrobial coatings

- 4.2.5 Rise of e-commerce grocery fulfillment centers

- 4.2.6 AI-enabled shelf-life prediction analytics

- 4.3 Market Restraints

- 4.3.1 Regulatory tightening on certain fungicides

- 4.3.2 Growing consumer resistance to synthetic chemicals

- 4.3.3 Price volatility of bio-based raw materials

- 4.3.4 Post-harvest mechanization gaps in developing countries

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Treatment Type

- 5.1.1 Coatings and Films

- 5.1.2 Cleaners

- 5.1.3 Fungicides

- 5.1.4 Ethylene Blockers

- 5.1.5 Sprout Inhibitors

- 5.1.6 Others

- 5.2 By Formulation

- 5.2.1 Liquid

- 5.2.2 Powder

- 5.2.3 Gas

- 5.3 By Crop Type

- 5.3.1 Fruits

- 5.3.2 Vegetables

- 5.3.3 Grains

- 5.3.4 Flowers and Ornamentals

- 5.4 By Origin

- 5.4.1 Natural

- 5.4.2 Synthetic

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Syngenta AG

- 6.4.2 AgroFresh Solutions, Inc.

- 6.4.3 Bayer AG

- 6.4.4 Decco Post-Harvest Inc. (UPL Limited)

- 6.4.5 Nufarm Limited

- 6.4.6 John Bean Technologies Corporation

- 6.4.7 Xeda International S.A.

- 6.4.8 Citrosol, S.A.

- 6.4.9 Fomesa Fruitech, S.L.U.

- 6.4.10 bio-ferm GmbH (Andermatt Group AG)

- 6.4.11 Lytone Enterprise, Inc.

- 6.4.12 Janssen PMP (Janssen Pharmaceutica NV)

7 Market Opportunities and Future Outlook

全球收穫後處理市場

全球收穫後處理市場 收穫後後處理市場:2026-2030 年全球市場預測,按處理類型、作物類型、配方、應用方法、應用、最終用戶和分銷管道分類。

收穫後後處理市場:2026-2030 年全球市場預測,按處理類型、作物類型、配方、應用方法、應用、最終用戶和分銷管道分類。 全球收穫後處理市場規模、佔有率、趨勢和成長分析報告:2026-2034年

全球收穫後處理市場規模、佔有率、趨勢和成長分析報告:2026-2034年 2026年全球採後後處理市場報告

2026年全球採後後處理市場報告 收穫後後處理市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、作物類型、產地、地區和競爭格局分類,2021-2031年

收穫後後處理市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、作物類型、產地、地區和競爭格局分類,2021-2031年 收穫後加工市場規模、佔有率和趨勢分析報告:按產地、產品、應用、地區和細分市場預測,2025 年至 2033 年全球收穫後加工市場規模(按產品類型、作物類型、區域覆蓋範圍和預測)

收穫後加工市場規模、佔有率和趨勢分析報告:按產地、產品、應用、地區和細分市場預測,2025 年至 2033 年全球收穫後加工市場規模(按產品類型、作物類型、區域覆蓋範圍和預測) 2032 年收穫後加工產品市場預測:按產品類型、作物類型、產地、應用和地區進行的全球分析2032 年收穫後加工市場預測:按類型、作物類型、產地、應用和地區進行的全球分析

2032 年收穫後加工產品市場預測:按產品類型、作物類型、產地、應用和地區進行的全球分析2032 年收穫後加工市場預測:按類型、作物類型、產地、應用和地區進行的全球分析 2025 年至 2029 年全球收穫後加工市場

2025 年至 2029 年全球收穫後加工市場