|

市場調查報告書

商品編碼

2064516

歐洲人力資源分析:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Europe HR Analytics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

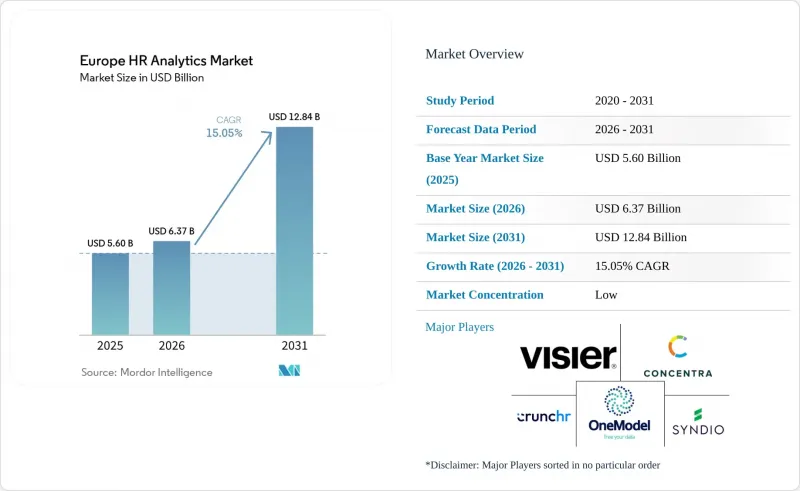

根據 Mordor Intelligence 預測,歐洲人力資源分析市場規模預計在 2025 年達到 56 億美元,2026 年達到 63.7 億美元,2031 年達到 128.4 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 15.05%。

本報告按組件(解決方案、服務)、部署類型(雲端、本地部署、混合部署)、企業規模(大型企業等)、應用(人才招聘和培訓等)、最終用戶行業(銀行、金融服務和保險、醫療保健和生命科學、IT和電信等)以及地區進行細分。市場預測以價值(美元)表示。

歐洲人力資源分析市場趨勢與洞察

採用雲端原生人力資源分析技術可以加速平台整合。

雲端遷移是影響整個全部區域軟體選擇的最重要結構性因素。由於SaaS產品更新速度更快、維護成本更低,且更容易採用新的分析功能,雇主們正逐漸放棄本地部署的報告環境。這種轉變在德國尤其顯著,預計到2025年3月,德國薪資和保險業的企業價值將達到55億歐元(62.2億美元),企業收入將超過3億歐元(3.39億美元),年成長率超過20%。雲端遷移也暴露了長期以來隱藏在孤立的人力資源和薪資系統中的資料品質問題。隨著這些問題的出現,企業需要更多支援來進行整合、管治和持續的模型調整。在歐洲人力資源分析市場,這一趨勢導致供應商在初始部署後更多地參與其中,並提升了服務的商業性重要性。

以數據驅動的方式最佳化人才招聘和保留,將改變人才經濟的運作方式。

鑑於歐洲普遍且持續的勞動力短缺,招聘分析正成為產業計畫不可或缺的一部分。歐洲職業培訓發展中心(Cedefop)的勞動力和技能短缺指數顯示,所有高、中、低技能職位類別都面臨壓力,這意味著雇主不能再僅依賴基本的就業市場追蹤。採購人員越來越重視那些能夠將內部技能儲備與外部勞動力市場趨勢和未來需求預測進行比較的平台。這正將商業性關注點從單純的應徵者追蹤工具轉向更廣泛的人才情報系統。人才保留分析也遵循類似的路徑,因為隨著留住稀缺人才變得越來越困難,雇主需要及早預警。因此,歐洲人力資源分析市場正受益於「招募回報」的更廣泛定義,將技能差距、招募品質和內部調動整合到單一的工作流程中。

GDPR和敏感員工資料管治成為分析的障礙。

在歐洲許多部署專案中,資料管治仍然是最迫切的營運限制因素。雖然人力資源部門通常擁有技術上必要的數據,但如果沒有新的法律依據和更強力的控制結構,他們可能無法在與薪資核算、績效評估、招聘和員工流動相關的流程中重複使用這些數據。當雇主進行使用者畫像、特殊類別資料或跨國資料處理時,問題會變得更加複雜,因為這些用例需要更詳細的審查和嚴格的文件記錄。國家法規也是關鍵因素,尤其是在那些對就業隱私期望嚴格、內部協商要求較正式的市場。因此,供應商必須實施「隱私設計」架構,限制資料訪問,並在專案早期階段就設定更細粒度的權限。在歐洲人力資源分析市場,這些控制措施是建立長期信任的基礎,但同時也延長了引進週期,並推高了短期部署成本。

細分市場分析

截至2025年,解決方案在歐洲人力資源分析市場佔據62.37%的佔有率,而服務領域預計到2031年將以16.94%的複合年成長率成長。這一差距反映了市場結構的變化:軟體仍然是合約價值的基礎,而服務作為專案成功和合約續約品質的決定性因素正變得越來越重要。隨著供應商加入預測性人員流動模型、生成式人工智慧助理和技能圖譜功能,部署需求也變得更加專業化。買家現在不太可能將部署視為一次性設置,而更傾向於將其視為持續的營運項目。

這種轉變使專業服務受益,因為雇主需要資料遷移、模型校準、變更管理和管治方面的支援。隨著企業從廣泛的人力資本管理 (HCM) 報告轉向必須與現有人力資源資訊系統 (HRIS) 和薪資核算系統整合的專用勞動力智慧平台,這一點尤其明顯。在歐洲人力資源分析市場,能夠將軟體與深度諮詢能力相結合的供應商備受青睞,因為如今的價值很大程度上取決於實施效果和結果質量,以及許可證的獲取。軟體仍然佔據收入的大部分,尤其是在與大型企業和公共部門客戶簽訂的多年期 SaaS 合約中。同時,德國雲端人力資源的發展勢頭強勁,以 P&I 的成長和估值趨勢為標誌,這表明隨著平台的普及,服務的重要性日益凸顯。

到2025年,雲端採用率將佔市場佔有率的68.41%,證實了SaaS已成為新型人力資源分析部署決策的事實標準架構。雲端系統之所以具有吸引力,是因為供應商可以更快地交付產品更新,更輕鬆地支援即時資料管道,並且無需客戶進行大規模升級即可應對合規性變更。混合部署是成長最快的模式,2026年至2031年的複合年成長率將達到17.86%。這是因為有些雇主仍然需要對部分技術堆疊進行更嚴格的內部控制。這種趨勢在銀行、醫療保健、政府機構和其他受監管行業尤為明顯,因為這些行業的資料儲存位置、採購規則或現有基礎設施成本仍然很高。

儘管本地部署的相對佔有率正在下降,但它並未完全從該地區消失。尤其是在德國,一些成熟的公共機構和工業組織仍然保留內部託管,用於存放高度敏感的員工記錄和長期存在的IT資產。因此,混合環境並非只是暫時的例外,而是一種過渡方案,使組織能夠在無需一次性重寫整個資料架構的情況下,實現分析能力的現代化。雖然歐洲人力資源分析市場正在向雲端遷移,但這種轉型的速度在不同產業和國家之間仍然不均衡。擁有靈活部署選項、自主託管架構和強大整合層的供應商,在吸引受監管員工和跨境交易方面具有優勢。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 實施雲端原生人力資源分析

- 數據驅動的招募與留任最佳化

- 預測性人力資源規劃,預見技能短缺問題

- 擴展員工體驗與敬業度分析

- 為遵守歐盟工資透明指令所做的準備工作

- CSRD 和 ESRS S1 項下的員工資訊揭露要求

- 市場限制因素

- GDPR的複雜性以及敏感員工資料的管治

- 分散的人力資源資訊系統和薪資資料環境跨越多個國家

- 關於與員工代表機構就監測相關分析進行磋商的要求

- 高風險人工智慧就業遵守歐盟人工智慧法律的負擔

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 按組件

- 解決方案

- 服務

- 透過部署方法

- 雲

- 現場

- 混合

- 按最終用戶公司規模分類

- 大公司

- 小型企業

- 透過使用

- 人才招聘和培訓

- 員工留任與流失管理

- 人員規劃

- 績效和生產力管理

- 薪資和薪資差距

- 員工敬業度與體驗

- 學習與技能分析

- 能源部檢查 (DEI) 和勞動力合規性分析

- 其他用途

- 按最終用戶行業分類

- 銀行、金融服務和保險業 (BFSI)

- 醫學與生命科學

- IT/通訊

- 零售與電子商務

- 工業/製造業

- 政府/公共部門

- 按地區

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 荷蘭

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介。

- Visier, Inc.

- One Model Inc.

- Crunchr BV

- Concentra Analytics Limited

- Syndio Solutions, Inc.

- Eightfold AI, Inc.

- Culture Amp Pty Ltd.

- Hi Bob, Inc.

- Beamery Inc.

- Humanyze, Inc.

- Leapsome GmbH

- Degreed, Inc.

- peopleIX GmbH

- functionHR GmbH

- HumanPanel Sp. z oo

- Firstmind ApS

- Scorius BV

- Panalyt Inc.

- 365Talents SAS

- retrain.ai Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the europe hR analytics market size is projected to be USD 5.60 billion in 2025, USD 6.37 billion in 2026, and reach USD 12.84 billion by 2031, growing at a CAGR of 15.05% from 2026 to 2031.

This report is Segmented by Component (Solutions, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and More), Application (Talent Acquisition and Onboarding, and More), End-User Industry (BFSI, Healthcare and Life Sciences, Information Technology and Telecom, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Europe HR Analytics Market Trends and Insights

Cloud-Native HR Analytics Adoption Accelerates Platform Consolidation

Cloud migration has become the strongest structural force shaping software selection across the region. Employers are moving away from on-premises reporting environments because SaaS delivery provides faster updates, lower maintenance costs, and a simpler path to rolling out new analytics features. That shift is especially visible in Germany, where P and I's valuation reached EUR 5.5 billion (USD 6.22 billion) in March 2025, and the company's revenue moved past EUR 300 million (USD 339 million) with annual growth above 20%. Cloud migration is also exposing data-quality issues that had been hidden inside siloed HR and payroll systems for years. Once those issues surface, organizations need more support for integration, governance, and ongoing model tuning. In the Europe HR analytics market, that dynamic is extending vendor involvement after the initial deployment and raising the commercial importance of services.

Data-Driven Recruitment and Retention Optimization Reshapes Talent Economics

Recruitment analytics is moving closer to core business planning because labor shortages remain broad and persistent across Europe. Cedefop's Labor and Skills Shortage Index shows pressure across high-, medium-, and low-skilled occupations, indicating that employers can no longer rely solely on basic vacancy tracking. Buyers are placing more value on platforms that can compare internal skills inventories with external labor signals and expected future demand. That is shifting commercial traction away from narrow applicant-tracking tools and toward broader talent-intelligence systems. Retention analytics is following the same path because employers need earlier warning signs as scarce talent becomes harder to retain. The European HR analytics market is therefore benefiting from a broader definition of recruiting return, encompassing skill gaps, hiring quality, and internal mobility within a single workflow.

GDPR and Sensitive Employee Data Governance Creates Analytics Friction

Data governance remains the most immediate operating constraint for many deployments across Europe. HR teams often hold the data they need in technical terms, but they cannot always reuse it across payroll, performance, recruiting, and attrition workflows without a fresh legal basis or stronger controls. The issue becomes more complex when employers move into profiling, special-category data, or cross-border processing, because those use cases can trigger deeper review and heavier documentation. National overlays also matter, especially in markets where employment privacy expectations are stricter and internal consultation requirements are more formal. That pushes vendors toward privacy-by-design architecture, narrower data access, and more granular permissions from the start of the project. In the Europe HR analytics market, these controls support long-term trust, but they also lengthen implementation cycles and raise near-term delivery costs.

Other drivers and restraints analyzed in the detailed report include:

- Predictive Workforce Planning Addresses EU-Wide Skills Shortages

- Employee Experience and Engagement Analytics Expansion Targets Continuous Listening

- Fragmented Multicountry Data Estates Constrain Cross-Border Workforce Intelligence

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions held 62.37% of the Europe HR analytics market share in 2025, while services are projected to expand at a 16.94% CAGR through 2031. That spread reflects a market structure in which software still anchors contract value, but services increasingly determine project success and renewal quality. As vendors add predictive attrition models, generative AI assistants, and skills graph capabilities, implementation demands are becoming more specialized. Buyers are now less likely to treat deployment as a one-time setup and more likely to view it as a continuous operating program.

Professional services are benefiting from that shift because employers need support for data migration, model calibration, change management, and governance. This is particularly true when organizations are moving from broad HCM reporting to dedicated workforce intelligence platforms that must connect with existing HRIS and payroll stacks. The European HR analytics market is rewarding vendors that can pair software with advisory depth, because value now depends on adoption and output quality as much as on license access. Software still accounts for the larger revenue pool, especially in multi-year SaaS contracts with large enterprises and public-sector clients. At the same time, Germany's cloud-HR momentum, illustrated by P and I's growth and valuation trajectory, shows why service intensity is rising alongside platform adoption

Cloud deployment accounted for 68.41% of the market in 2025, which confirms that SaaS has become the default architecture for most new HR analytics buying decisions. Cloud systems are attractive because vendors can push product updates faster, support real-time data pipelines more easily, and handle compliance changes without large customer-side upgrade cycles. Hybrid deployment is the fastest-growing model, with a 17.86% CAGR from 2026 to 2031, because some employers still need part of the stack to remain under tighter internal control. That pattern is strongest in banking, healthcare, government, and other regulated settings where data residency, procurement rules, or sunk infrastructure costs still matter.

The on-premises segment is losing relative weight, but it is not disappearing from the region. Established public institutions and industrial organizations, especially in Germany, still maintain internal hosting for sensitive employee records and long-governed IT estates. Hybrid environments, therefore, act as a bridge, not simply as a temporary exception, because they let organizations modernize analytics without rewriting the full data architecture at once. The European HR analytics market is seeing a rise in cloud concentration, but the transition remains uneven across sectors and countries. Vendors with flexible deployment options, sovereign hosting arrangements, and strong integration layers are better placed to win regulated accounts and cross-border deals.

List of Companies Covered in this Report:

- Visier, Inc.

- One Model Inc.

- Crunchr B.V.

- Concentra Analytics Limited

- Syndio Solutions, Inc.

- Eightfold AI, Inc.

- Culture Amp Pty Ltd.

- Hi Bob, Inc.

- Beamery Inc.

- Humanyze, Inc.

- Leapsome GmbH

- Degreed, Inc.

- peopleIX GmbH

- functionHR GmbH

- HumanPanel Sp. z o.o.

- Firstmind ApS

- Scorius B.V.

- Panalyt Inc.

- 365Talents SAS

- retrain.ai Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-Native HR Analytics Adoption

- 4.2.2 Data-Driven Recruitment and Retention Optimization

- 4.2.3 Predictive Workforce Planning for Skills Shortages

- 4.2.4 Employee Experience and Engagement Analytics Expansion

- 4.2.5 EU Pay Transparency Directive Compliance Readiness

- 4.2.6 CSRD and ESRS S1 Workforce Disclosure Requirements

- 4.3 Market Restraints

- 4.3.1 GDPR and Sensitive Employee Data Governance Complexity

- 4.3.2 Fragmented Multicountry HRIS and Payroll Data Estates

- 4.3.3 Works Council Consultation Requirements for Monitoring-Adjacent Analytics

- 4.3.4 EU AI Act Compliance Burden for High-Risk Employment AI

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Comptetive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By End User Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-Sized Enterprises

- 5.4 By Application

- 5.4.1 Talent Acquisition and Onboarding

- 5.4.2 Retention and Attrition Management

- 5.4.3 Workforce Planning

- 5.4.4 Performance and Productivity Management

- 5.4.5 Compensation and Pay Equity

- 5.4.6 Employee Engagement and Experience

- 5.4.7 Learning and Skills Analytics

- 5.4.8 DEI and Workforce Compliance Analytics

- 5.4.9 Other Applications

- 5.5 By End User Industry

- 5.5.1 BFSI

- 5.5.2 Healthcare and Life Sciences

- 5.5.3 Information Technology and Telecom

- 5.5.4 Retail and E-commerce

- 5.5.5 Industrial Manufacturing

- 5.5.6 Government and Public Sector

- 5.6 By Geography

- 5.6.1 Germany

- 5.6.2 United Kingdom

- 5.6.3 France

- 5.6.4 Italy

- 5.6.5 Spain

- 5.6.6 Russia

- 5.6.7 Netherlands

- 5.6.8 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 Visier, Inc.

- 6.4.2 One Model Inc.

- 6.4.3 Crunchr B.V.

- 6.4.4 Concentra Analytics Limited

- 6.4.5 Syndio Solutions, Inc.

- 6.4.6 Eightfold AI, Inc.

- 6.4.7 Culture Amp Pty Ltd.

- 6.4.8 Hi Bob, Inc.

- 6.4.9 Beamery Inc.

- 6.4.10 Humanyze, Inc.

- 6.4.11 Leapsome GmbH

- 6.4.12 Degreed, Inc.

- 6.4.13 peopleIX GmbH

- 6.4.14 functionHR GmbH

- 6.4.15 HumanPanel Sp. z o.o.

- 6.4.16 Firstmind ApS

- 6.4.17 Scorius B.V.

- 6.4.18 Panalyt Inc.

- 6.4.19 365Talents SAS

- 6.4.20 retrain.ai Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment

2034 年神經多樣性人力資源和人才分析平台市場預測——全球平台類型、分析重點領域、部署方法、經營模式、產業、最終用戶和地區分析——產業特定分析

2034 年神經多樣性人力資源和人才分析平台市場預測——全球平台類型、分析重點領域、部署方法、經營模式、產業、最終用戶和地區分析——產業特定分析 銀行、金融服務和保險 (BFSI) 行業的人力分析:市場佔有率分析、行業趨勢與統計數據、成長預測(2026-2031 年)

銀行、金融服務和保險 (BFSI) 行業的人力分析:市場佔有率分析、行業趨勢與統計數據、成長預測(2026-2031 年) 人力資源分析市場規模、佔有率和趨勢分析報告:按解決方案、服務、部署類型、企業規模、最終用途、地區和細分市場預測(2026-2033 年)

人力資源分析市場規模、佔有率和趨勢分析報告:按解決方案、服務、部署類型、企業規模、最終用途、地區和細分市場預測(2026-2033 年) 人力資源分析市場:按組件、企業規模、部署模式和產業分類-2026-2032年全球市場預測

人力資源分析市場:按組件、企業規模、部署模式和產業分類-2026-2032年全球市場預測 人力資源分析市場-全球產業規模、佔有率、趨勢、機會和預測,按解決方案、部署方式、企業規模、最終用途、服務、地區和競爭格局分類,2021-2031年預測

人力資源分析市場-全球產業規模、佔有率、趨勢、機會和預測,按解決方案、部署方式、企業規模、最終用途、服務、地區和競爭格局分類,2021-2031年預測 人力資源分析市場規模、佔有率和成長分析(按解決方案、服務、部署類型、公司規模、最終用途和地區分類)-2026-2033年產業預測

人力資源分析市場規模、佔有率和成長分析(按解決方案、服務、部署類型、公司規模、最終用途和地區分類)-2026-2033年產業預測 人力資源與人事分析軟體市場(按解決方案、服務、類型和地區):未來預測(2026-2032 年)人力資源分析市場規模:2026-2032 年,依組件、實施類型、產品、產業垂直和地區分類人力資源分析:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

人力資源與人事分析軟體市場(按解決方案、服務、類型和地區):未來預測(2026-2032 年)人力資源分析市場規模:2026-2032 年,依組件、實施類型、產品、產業垂直和地區分類人力資源分析:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)