|

市場調查報告書

商品編碼

2064510

高耐久性路由器:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年)Rugged Router - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

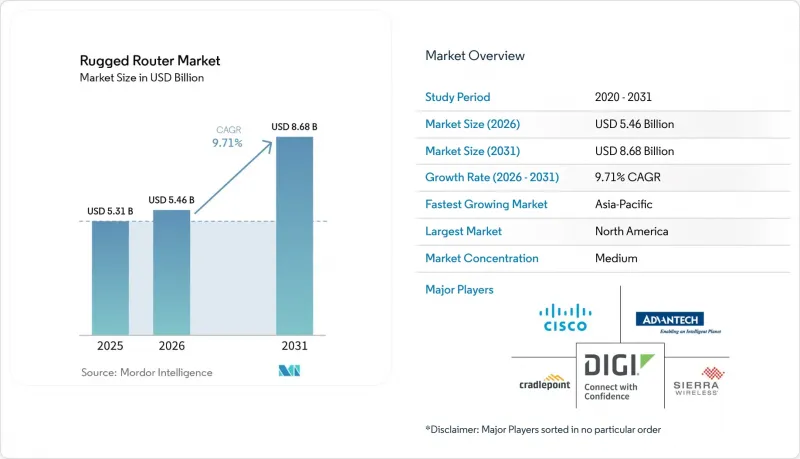

根據 Mordor Intelligence 預測,耐用型路由器的市場規模預計將從 2025 年的 53.1 億美元和 2026 年的 54.6 億美元成長到 2031 年的 86.8 億美元,2026 年至 2031 年的複合年成長率為 9.71%。

本報告按產品類型(蜂窩網路、工業乙太網路等)、連接技術(4G/LTE、5G、Wi-Fi 6/6E等)、終端用戶產業(能源和公用事業、運輸和物流、石油和天然氣、採礦、製造業等)、部署方式(固定、移動/移動、可攜式等)和地區進行細分。市場預測以美元(USD)計價。

全球高耐久性路由器市場趨勢與分析

邊緣運算在惡劣環境中的普及

傳統上在集中式或區域性資料中心處理的推理工作負載正擴大轉移到直接安裝在遠端井口的自主鑽機、鑽井系統和邊緣無風扇閘道器上。先進的鑽探平臺現在可以在本地以低於 50 毫秒的速度運行機器視覺和控制迴路,從而消除回程傳輸延遲,並在關鍵任務環境中實現即時決策。同樣,具有嵌入式 AI 運算能力和專用 LTE 連接的堅固耐用型邊緣設備在資產層級處理地震和運行數據,而不是將其發送到遠端雲端環境。這種轉變正在推動“矽融合”,即將計算、儲存和路由功能整合到緊湊的 IP67 防護等級機殼中,這些外殼的設計能夠承受 -40 度C至 +75 度C 的溫度,從而增加了對高性能、高耐用性路由器的需求。

5G NR在工業連接中的整合

獨立組網的 5G 網路在工業環境中效能顯著優於 4G,這得益於其引入的網路切片和時間敏感網路等特性。目前,大規模專用 5G 網路連接分佈在廣大營運區域的數千個資產,為關鍵基礎設施提供確定性、低延遲的通訊。同時,工業路由器整合了 5G、Wi-Fi 7 和 SD-WAN 等多射頻架構,透過將 SCADA 等營運技術 (OT) 流量與企業 IT 網路分離,提高了安全性和可靠性。此外,5G RedCap 模組的出現降低了邊緣設備和智慧電網感測器的功耗,從而降低了部署成本。因此,2026 年以後的新基礎設施項目越來越需要採用 5G 原生架構,而多射頻編配和無縫網路管理也成為關鍵的採購標準。

對強大的網路硬體進行大量初始投資

由於加固型網路硬體的前期成本遠高於商用級產品,因此在價格敏感型產業中,其普及應用面臨結構性障礙。一台符合 MIL-STD-810H 標準的路由器售價在 2,000 美元到 5,000 美元之間,而標準商用型號的售價約為 400 美元,這意味著在採礦等成本控制嚴格的行業,投資回收期可能超過五年。在國防應用中,由於嵌入式加密、多無線電整合和嚴苛的設計要求,戰術級系統的單價可能超過 15,000 美元。在鐵路行業,符合 EN 50155 標準會進一步增加總擁有成本,在整個部署生命週期內,每輛車的成本將增加 10,000 美元到 20,000 美元。像 Cradlepoint NetCloud 這樣的訂閱模式將支出轉移到營運支出 (OPEX),從而降低了初始資本負擔,但營運商仍然傾向於擁有資產所有權而非定期收費系統,這限制了其在保守採購環境中的普及。

細分市場分析

到2025年,工業乙太網路將佔據高耐久性路由器市場34.6%的佔有率,這反映了其在確定性有線工業網路中的穩固地位。然而,受國防現代化以及衝突地區對容錯多層通訊需求的推動,戰術路由器預計將以11.12%的複合年成長率成長。多波形綁定架構實現了無線、衛星和蜂窩電路之間的無縫容錯移轉,即使在發生干擾或節點故障的情況下也能確保通訊連續性。同時,工業平台的功能整合度也不斷提高,例如思科Catalyst IR8300等解決方案整合了SD-WAN和雙5G調變解調器,從而無需單獨的安全和路由設備,從而提高了營運效率。

價格差異仍然是決定性的結構性因素。工業乙太網路路由器的價格通常在 2,000 美元到 5,000 美元之間,而 4G 蜂巢設備的價格在 800 美元到 1,500 美元之間,5G 型號的價格在 1,800 美元到 3,500 美元之間。相比之下,戰術級系統憑藉其先進的加密、加固和多頻段整合功能,價格在 15,000 美元到 25,000 美元之間。儘管部署規模相對較小,但如此高的平均售價 (ASP) 卻不成比例地推高了收入。同時,對整合交換、路由和安全功能的需求不斷成長,導致機櫃面積縮小,並向整合式多功能設備轉變,從而有效地模糊了工業和公用事業領域的傳統設備分類。

2025年,4G和LTE路由器佔耐用型路由器出貨量的46.23%,這反映了它們在棕地工業環境中的可靠部署記錄和穩定性。然而,隨著專用頻譜部署和工業5G網路在公用事業、能源和交通運輸領域的擴展,5G路由器的年複合成長率(CAGR)正以9.87%的速度成長。供應商優先考慮向後相容性以減少過渡阻力,像Cradlepoint R2400這樣的平台允許回退到LTE,以確保分階段升級期間的連續性。這種混合方案降低了過渡風險,並支持分階段的資本投資,而無需完全更換基礎設施。

在架構層面,容錯性正成為採購中的強制性要求。尤其是在任務關鍵型營運中,能夠在50毫秒內實現蜂窩線路間容錯移轉的雙頻配置已被納入競標規範。此外,衛星通訊和蜂窩通訊的整合正在消除地面網路可靠性仍然較低的偏遠和災害易發地區的通訊盲區。 Meridian5G M1-R 等解決方案透過結合衛星和5G連接來防止指揮控制中斷,清晰地展現了這一轉變。這種向多路徑和軟體編配網路的演進正在重新定義效能基準,並加速混合通訊協定堆疊的採用。

區域分析

到2025年,北美將佔耐用型路由器全球銷售額的31.34%,這主要得益於聯邦政府強制推行的鐵路安全系統和國防網路現代化項目。列車自動控制系統(PTC)的部署持續需要雙蜂窩網路、整合GNSS的路由器,以確保龐大鐵路網路的即時列車間距和運行安全。同時,軍用網狀網路的發展也加速了對安全、容錯通訊基礎設施的需求。在加拿大礦區惡劣環境下的部署進一步提升了該地區的需求,這些路由器保證在-40 度C的低溫下運行,從而實現持續的遠端操作和視訊串流傳輸。該地區受益於強力的監管、較高的技術普及率以及交通運輸、國防和資源產業持續的資本投入。

亞太地區預計到2031年將以11.34%的複合年成長率成長,主要驅動力來自大規模基礎設施數位化和工業自動化。澳洲在自主採礦領域主導,營運商正在部署專用LTE和5G網路,以支援偏遠地區的即時車輛控制和分析。印度的「BharatNet」舉措正在擴大農村地區的寬頻普及率,國內供應商正在部署超過13萬台路由器,以連接服務不足的地區。同時,中國正在推動基於RedCap的物聯網部署,以實現經濟高效的工業連接。澳洲礦場的地下5G試點計畫表明,該地區對高頻寬、低延遲應用的投入不斷加強,進一步證實了亞太地區是成長最快的市場,其成長動力來自多元化的需求因素。

歐洲的成長與基於ETCS 2級和3級的鐵路數位化密切相關,這需要在整個跨境鐵路網路中建立安全且可互通的通訊系統。供應商正在將訊號控制和乘客通訊等多種功能整合到一個統一的平台中,以減少硬體冗餘。在中東,隨著能源產業的數位化大規模推進,投資正在加速成長,其中包括私有5G油田網路和用於上游作業的Sub-GHz頻段的廣域部署。在南美洲,智利和秘魯等礦業重鎮的5G部署正在穩步推進,但大宗商品價格波動限制了5G投資週期。非洲仍然是一個發展中市場,需求集中在南非的礦業和奈及利亞的石油作業。在這些地區,由於地面基礎設施有限,衛星回程傳輸仍然至關重要。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 邊緣運算在惡劣環境中的普及

- 將5G NR整合到工業連接中

- 能源產業對遠端資產監控的需求日益成長

- 軍事現代化計劃著重於戰術網路

- 智慧採礦中廣泛採用功能強大的物聯網閘道器。

- 監理機關為推廣鐵路列車自動控制系統(PTC)所做的努力

- 市場限制因素

- 對強大的網路設備進行高額初始投資

- 部署初期階段,可靠的5G組件供不應求

- 與傳統工業協議的兼容性問題

- 全球鐵路標準中複雜的認證要求

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 產業供應鏈分析

- 波特五力分析

第5章:預測市場規模與成長率

- 按類型

- 適用於蜂窩網路的高耐久性路由器

- 工業乙太網路路由器

- 無線網狀路由器

- 戰術/軍用級路由器

- 軟體定義高耐久性路由器

- 透過連接技術

- 4G/LTE

- 5G

- Wi-Fi 6/6E

- 雙重連接方式(蜂窩網路和 Wi-Fi)

- 相容於衛星回程傳輸

- 按最終用途行業分類

- 能源公用事業

- 運輸/物流

- 石油和天然氣

- 礦業

- 製造業

- 軍事/國防

- 公安

- 智慧城市/基礎設施

- 透過部署方法

- 固定式/獨立式

- 車載/移動

- 可攜式/手持式

- 海洋/近海

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Cisco Systems Inc.

- Digi International Inc.

- Advantech Co. Ltd.

- Sierra Wireless Inc.

- Cradlepoint Inc.

- Belden Inc.

- Juniper Networks Inc.

- Peplink International Ltd.

- Westermo Network Technologies AB

- Teltonika Networks UAB

- Moxa Inc.

- Aruba Networks LLC

- Fortinet Inc.

- Ubiquiti Inc.

- Encore Networks Inc.

- CalAmp Corp.

- Robustel Technologies Co. Ltd.

- Industrial Networking Solutions Inc.

- GE Vernova(formerly GE Digital Energy)

- RAD Data Communications Ltd.

- Siemens AG(Scalance)

- Schneider Electric SE

第7章 市場機會與未來展望

According to Mordor Intelligence, the rugged router market size is projected to expand from USD 5.31 billion in 2025 and USD 5.46 billion in 2026 to USD 8.68 billion by 2031, registering a CAGR of 9.71% between 2026 to 2031.

This report is Segmented by Product Type (Cellular, Industrial Ethernet, and More), Connectivity Technology (4G/LTE, 5G, Wi-Fi 6/6E, and More), End-Use Industry (Energy and Utilities, Transportation and Logistics, Oil and Gas, Mining, Manufacturing, and More), Deployment Mode (Fixed, Mobile Vehicle-Mounted, Portable, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Rugged Router Market Trends and Insights

Proliferation of Edge Computing In Harsh Environments

Inference workloads that were historically processed in centralized or regional data centers are increasingly shifting to edge-based, fanless gateways mounted directly on autonomous rigs, drilling systems, and remote wellheads. Advanced drilling platforms now execute sub-50 ms machine vision and control loops locally, eliminating backhaul latency and enabling real-time decision-making in mission-critical environments. Similarly, rugged edge devices equipped with embedded AI compute and private LTE connectivity process seismic and operational data at the asset level rather than transmitting it to distant cloud environments. This transition is driving silicon convergence, in which compute, storage, and routing functions are integrated into compact, IP67-rated enclosures engineered to withstand temperatures from -40 °C to +75 °C, thereby reinforcing demand for high-performance rugged routers.

Integration of 5G NR In Industrial Connectivity

Standalone 5G introduces capabilities such as network slicing and time-sensitive networking that materially exceed 4G performance in industrial environments. Large-scale private 5G grids are now connecting thousands of distributed assets across expansive operational areas, enabling deterministic, low-latency communication for critical infrastructure. Concurrently, industrial-grade routers are integrating multi-radio architectures that combine 5G, Wi-Fi 7, and SD-WAN to segment operational technology traffic, such as SCADA, from enterprise IT networks, thereby improving both security and reliability. Additionally, the emergence of 5G RedCap modules reduces power consumption for edge devices and smart-grid sensors, making deployments more cost-efficient. As a result, greenfield infrastructure projects from 2026 onward are increasingly specifying 5G-native architectures, positioning multi-radio orchestration and seamless network management as key procurement criteria.

High Initial Capital Expenditure for Rugged Networking Hardware

Rugged networking hardware has a materially higher upfront cost than commercial-grade alternatives, creating a structural adoption barrier in price-sensitive industries. A typical MIL-STD-810H compliant router ranges between USD 2,000-5,000, versus approximately USD 400 for standard commercial units, extending payback periods beyond 5 years in sectors such as mining, where cost discipline is strict. In defense applications, tactical-grade systems can exceed USD 15,000 per unit due to embedded encryption, multi-radio integration, and hardened design requirements. In rail, compliance with EN 50155 standards adds an incremental USD 10,000-20,000 per carriage over lifecycle deployments, further inflating the total cost of ownership. While subscription-based models such as Cradlepoint NetCloud shift expenditure toward OPEX and reduce initial capital burden, resistance persists among operators who prefer asset ownership over recurring fee structures, limiting penetration in conservative procurement environments.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Remote Asset Monitoring In Energy Sector

- Military Modernization Programs Focusing on Tactical Networking

- Limited Availability Of Rugged 5G Components During Early Roll-out

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Industrial Ethernet accounted for 34.6% of the rugged router market share in 2025, reflecting its entrenched role in deterministic, wired industrial networks. However, tactical routers are projected to grow at a 11.12% CAGR, driven by defense modernization and the need for resilient, multi-layered communications in contested environments. Multi-waveform bonding architectures enable seamless failover across radio, satellite, and cellular links, ensuring continuity even under jamming or node failure. Concurrently, industrial platforms are converging capabilities, with solutions such as Cisco Catalyst IR8300 integrating SD-WAN and dual 5G modems to eliminate standalone security and routing appliances, improving operational efficiency.

Pricing differentials remain a defining structural factor. Industrial Ethernet routers typically range from USD 2,000-5,000, while 4G cellular units range from USD 800-1,500, and 5G variants range from USD 1,800-3,500. In contrast, tactical-grade systems command USD 15,000-25,000 due to advanced encryption, ruggedization, and multi-radio integration. These elevated ASPs disproportionately inflate revenue contribution despite a relatively smaller installed base. At the same time, increasing demand for integrated switching, routing, and security functions is reducing cabinet footprint and driving procurement toward unified, multi-function appliances, effectively dissolving traditional device segmentation across industrial and utility deployments.

4G and LTE accounted for 46.23% of rugged router shipments in 2025, reflecting their entrenched installed base and reliability in brownfield industrial environments. However, 5G routers are expanding at a 9.87% CAGR as private spectrum deployments and industrial 5G networks scale across utilities, energy, and transport sectors. Vendors are prioritizing backward compatibility to reduce migration friction, with platforms such as Cradlepoint R2400 enabling LTE fallback to ensure continuity during phased upgrades. This hybrid approach reduces switching risk and supports gradual capital deployment, rather than requiring a full infrastructure replacement.

At the architecture level, resilience is becoming a non-negotiable procurement criterion. Dual-radio configurations capable of sub-50 ms failover between cellular links are now embedded in tender specifications, particularly for mission-critical operations. Additionally, satellite-cellular convergence is addressing coverage gaps in ultra-remote or disaster-prone regions, where terrestrial networks remain unreliable. Solutions such as Meridian5G M1-R illustrate this shift by bonding satellite and 5G connectivity to maintain uninterrupted command and control. This evolution toward multi-path, software-orchestrated networking is redefining performance benchmarks and accelerating adoption of hybrid communication stacks.

Geography Analysis

North America accounted for 31.34% of rugged router revenue in 2025, anchored by federally mandated rail safety systems and defense network modernization programs. Positive Train Control deployments continue to require dual-cellular, GNSS-integrated routers to ensure real-time train separation and operational safety across extensive rail networks. In parallel, military mesh networking initiatives are accelerating demand for secure, resilient communication infrastructure. Harsh-environment deployments in Canadian mining operations further reinforce regional demand, where routers rated for -40 °C enable continuous tele-remote operations and video streaming. The region benefits from strong regulatory enforcement, high technology adoption, and consistent capital allocation across transport, defense, and resource sectors.

Asia-Pacific is projected to grow at 11.34% CAGR through 2031, driven by large-scale infrastructure digitization and industrial automation. Australia leads in autonomous mining, with operators deploying private LTE and 5G networks to support real-time vehicle control and analytics in remote environments. India's BharatNet initiative is expanding rural broadband coverage, with domestic vendors scaling deployment of over 130,000 routers to connect underserved regions. Simultaneously, China is advancing RedCap-based IoT deployments to enable cost-efficient industrial connectivity. Underground 5G trials in Australian mines highlight the region's push toward high-bandwidth, low-latency applications, reinforcing Asia-Pacific as the fastest-growing market with diversified demand drivers.

Europe's growth is tied to railway digitization under ETCS Level 2 and 3, which requires secure, interoperable communication systems across cross-border rail networks. Vendors are integrating multiple functions such as signaling and passenger connectivity into unified platforms, reducing hardware redundancy. In the Middle East, investment is accelerating through large-scale energy sector digitization, including private 5G oilfield networks and sub-GHz wide-area deployments for upstream operations. South America shows steady adoption in mining-intensive economies such as Chile and Peru, although commodity price volatility constrains 5G investment cycles. Africa remains a nascent market, with demand concentrated in South African mining and Nigerian oil operations, where satellite backhaul remains critical due to limited terrestrial infrastructure.

- Cisco Systems Inc.

- Digi International Inc.

- Advantech Co. Ltd.

- Sierra Wireless Inc.

- Cradlepoint Inc.

- Belden Inc.

- Juniper Networks Inc.

- Peplink International Ltd.

- Westermo Network Technologies AB

- Teltonika Networks UAB

- Moxa Inc.

- Aruba Networks LLC

- Fortinet Inc.

- Ubiquiti Inc.

- Encore Networks Inc.

- CalAmp Corp.

- Robustel Technologies Co. Ltd.

- Industrial Networking Solutions Inc.

- GE Vernova (formerly GE Digital Energy)

- RAD Data Communications Ltd.

- Siemens AG (Scalance)

- Schneider Electric SE

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of Edge Computing in Harsh Environments

- 4.2.2 Integration of 5G NR in Industrial Connectivity

- 4.2.3 Rising Demand for Remote Asset Monitoring in Energy Sector

- 4.2.4 Military Modernization Programs Focusing on Tactical Networking

- 4.2.5 Growing Adoption of Ruggedized IoT Gateways in Smart Mining

- 4.2.6 Regulatory Push for Railway Positive Train Control Systems

- 4.3 Market Restraints

- 4.3.1 High Initial Capital Expenditure for Rugged Networking Hardware

- 4.3.2 Limited Availability of Rugged 5G Components During Early Roll-out

- 4.3.3 Compatibility Issues with Legacy Industrial Protocols

- 4.3.4 Complex Certification Requirements Across Global Rail Standards

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Impact of Macroeconomic Factors on the Market

- 4.7 Industry Supply-Chain Analysis

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Cellular Rugged Router

- 5.1.2 Industrial Ethernet Router

- 5.1.3 Wireless Mesh Router

- 5.1.4 Tactical Military-Grade Router

- 5.1.5 Software-Defined Rugged Router

- 5.2 By Connectivity Technology

- 5.2.1 4G / LTE

- 5.2.2 5G

- 5.2.3 Wi-Fi 6 / 6E

- 5.2.4 Dual Connectivity (Cellular and Wi-Fi)

- 5.2.5 Satellite Backhaul Enabled

- 5.3 By End-Use Industry

- 5.3.1 Energy and Utilities

- 5.3.2 Transportation and Logistics

- 5.3.3 Oil and Gas

- 5.3.4 Mining

- 5.3.5 Manufacturing

- 5.3.6 Military and Defense

- 5.3.7 Public Safety

- 5.3.8 Smart Cities / Infrastructure

- 5.4 By Deployment Mode

- 5.4.1 Fixed / Stationary

- 5.4.2 Mobile Vehicle-Mounted

- 5.4.3 Portable / Handheld

- 5.4.4 Marine / Offshore

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Cisco Systems Inc.

- 6.4.2 Digi International Inc.

- 6.4.3 Advantech Co. Ltd.

- 6.4.4 Sierra Wireless Inc.

- 6.4.5 Cradlepoint Inc.

- 6.4.6 Belden Inc.

- 6.4.7 Juniper Networks Inc.

- 6.4.8 Peplink International Ltd.

- 6.4.9 Westermo Network Technologies AB

- 6.4.10 Teltonika Networks UAB

- 6.4.11 Moxa Inc.

- 6.4.12 Aruba Networks LLC

- 6.4.13 Fortinet Inc.

- 6.4.14 Ubiquiti Inc.

- 6.4.15 Encore Networks Inc.

- 6.4.16 CalAmp Corp.

- 6.4.17 Robustel Technologies Co. Ltd.

- 6.4.18 Industrial Networking Solutions Inc.

- 6.4.19 GE Vernova (formerly GE Digital Energy)

- 6.4.20 RAD Data Communications Ltd.

- 6.4.21 Siemens AG (Scalance)

- 6.4.22 Schneider Electric SE

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

工業路由器市場:2026-2032年全球市場預測(依產品類型、連接技術、部署環境、最終用戶產業及銷售管道)

工業路由器市場:2026-2032年全球市場預測(依產品類型、連接技術、部署環境、最終用戶產業及銷售管道) 2026年全球電信級路由市場報告全球乙太網路路由器市場報告(2026 年)

2026年全球電信級路由市場報告全球乙太網路路由器市場報告(2026 年) 路由器市場規模、佔有率和成長分析:按產品類型、頻寬類型、技術、應用、銷售管道、最終用戶和地區分類-2026-2033年產業預測

路由器市場規模、佔有率和成長分析:按產品類型、頻寬類型、技術、應用、銷售管道、最終用戶和地區分類-2026-2033年產業預測 工業路由器市場:按產品類型、最終用戶和地區分類

工業路由器市場:按產品類型、最終用戶和地區分類 SOHO路由器:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)服務供應商的路由器:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)消費級路由器:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)2026年全球路由器市場報告2026年全球電信級路由系統(CRS)市場報告

SOHO路由器:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)服務供應商的路由器:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)消費級路由器:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)2026年全球路由器市場報告2026年全球電信級路由系統(CRS)市場報告