|

市場調查報告書

商品編碼

2063816

SOHO路由器:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)SOHO Router - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

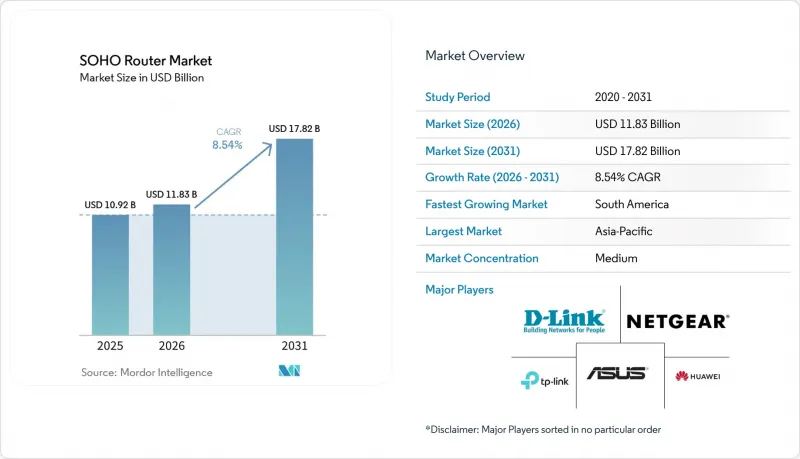

據 Mordor Intelligence 稱,2025 年 SOHO 路由器市值為 109.2 億美元,預計到 2031 年將從 2026 年的 118.3 億美元成長至 178.2 億美元,預測期(2026-2031 年)的複合年成長率為 8.54%。

本報告按頻段(單頻段、雙頻、三頻、四頻)、Wi-Fi 標準(Wi-Fi 4、Wi-Fi 5、Wi-Fi 6、Wi-Fi 6E、Wi-Fi 7)、應用領域(住宅、家庭辦公室、小規模辦公室等)、銷售管道(線路上零售、線下零售、ISP 捆綁式零售、ISP 合作夥伴 CPE 和企業區進行細分市場合作夥伴。市場預測以美元 (USD) 為單位。

全球SOHO路由器市場趨勢及洞察

透過將人工智慧加速器整合到路由器中,實現了即時流量最佳化。

整合神經處理單元的路由器正從被動資料包傳輸轉向主動編配。 Charter 頻譜報告稱,在 2025 年部署了配備設備端 AI 的 Wi-Fi 7 閘道器並實施動態擁塞重定向後,其支援諮詢量有所下降。高通在其 2025 年投資者簡報中確認,超過 250 種網路設計將採用帶有推理引擎的 Wi-Fi 7 晶片組。此類晶片無需手動設定 QoS(服務品質)規則即可對流量進行分類並優先處理對延遲敏感的資料包。同時運作視訊會議、雲端遊戲和物聯網感測器的家庭將受益於更低的抖動和更低的服務供應商解約率。偵測異常流量的預測警報為託管安全訂閱服務創造了提升銷售機會。

Wi-Fi 6 和 Wi-Fi 7 標準的快速普及

Wi-Fi聯盟在2024年認證了2.33億台Wi-Fi 7設備,並預測2028年這一數字將達到21億台,超過Wi-Fi 6的普及速度。聯發科的Filogic 880和660平台於2025年開始出貨,讓售價低於200美元的三頻路由器成為可能。隨後,博通和高通發布了採用320MHz頻道和4096-QAM調變的四頻參考設計,以實現40Gbps的吞吐量。 2026年1月,美國聯邦通訊委員會(FCC)批准了標準功率的6GHz頻段設備,取消了室內覆蓋範圍限制,加速了Wi-Fi 7在小規模辦公室和工業領域的普及。晶片組成本的降低和監管規定的明確化共同縮短了Wi-Fi 5硬體的更換週期。

通訊業者捆綁銷售的 5G 固定無線閘道帶來的替代方案威脅日益增加。

T-Mobile 透過將 Inseego 的 FX4200 和 FX4100 閘道器捆綁銷售,無需預付費用,並整合三頻 Wi-Fi 7 和 5G回程傳輸,成功搶佔了獨立路由器市場。高通的單晶片 Dragonwing 平台進一步降低了組件成本,使通訊業者能夠提供硬體補貼。尋求統一計費的中小型企業紛紛選擇這些閘道器,導致零售路由器銷售下降,尤其是在光纖覆蓋有限的地區。

細分市場分析

2025年,三頻路由器憑藉對延遲敏感的4K串流媒體和雲端遊戲的需求,在SOHO路由器市場中佔據了更大的市場佔有率。雖然雙頻系統仍主導中價位市場,但預計到2031年,三頻產品的出貨量成長速度將超過SOHO路由器市場的整體成長速度。由聯發科和博通推出的低成本Wi-Fi 7晶片已將零售價格降至200美元以下,使消費者能夠以實惠的價格享受到千兆Gigabit的Wi-Fi性能。

網狀網路是主要驅動力。四頻設計透過將 6 GHz 頻段的無線功能專門用於回程傳輸鏈路,無需乙太網路線即可實現確定性延遲。標準功率的 6 GHz 頻段無線設備已於 2026 年 1 月獲得監管部門批准,這使得三頻套件能夠覆蓋更廣泛的範圍,並促進其在郊區住宅中的普及。單頻段設備目前僅用於超低價位產品和嵌入式物聯網終端,但隨著晶片組成本的持續下降,預計最終將被淘汰。

儘管Wi-Fi 5在2025年仍將是入門級ISP套餐的基礎,但Wi-Fi 7 24.76%的複合年成長率使其成為2027年後SOHO路由器市場銷量成長的主要驅動力。 FCC對高功率6GHz頻段運作的批准擴大了實際覆蓋範圍,而晶片組廠商則競相整合320MHz頻道和多鏈路運作功能。遊戲和專業用戶等細分市場的早期採用者表現出在設備生命週期結束前就進行升級的意願,從而縮短了更新周期。

在企業級小規模辦公室中,Wi-Fi 6E 因其 OFDMA 效率和可延長物聯網設備電池續航時間的定向喚醒功能而日益普及。 Wi-Fi 4 及更早版本則逐漸式微,目前主要用於傳統工業控制器,直到獲得維修預算為止。隨著具備三頻無線電功能的客戶設備日益增多,互通性問題逐漸減少,供應商的替換機會也隨之增加。

區域分析

到了2025年,亞太地區佔據SOHO路由器市場的36.52%。這主要得益於中國的普及寬頻政策以及印度二線城市的光纖部署。小米透過其生態系統實現了9.046億台連網裝置的商業化,並利用限時搶購活動提升了路由器在印度(市佔率13.4%)和東南亞(市佔率16.7%)的滲透率。在日本,人口密集的多用戶住宅加速了Wi-Fi 6E的普及;而在澳大利亞,NBN升級促使老舊的ADSL設備更換。該地區的多元化需求導致了對雙頻產品和高階四頻產品之間的需求分化。

隨著通訊業者將光纖網路擴展到區域城市,南美洲正以10.46%的複合年成長率引領市場成長。至2024年底,巴西、智利、秘魯和墨西哥的光纖普及率將超過70%,屆時僅支援2.4GHz頻段的路由器的頻寬將日益凸顯。 TP-Link計劃在巴西建廠,這將縮短供應鏈並降低接收成本,而小米以17.9%的區域市佔率位居第二。儘管受經濟逆風和貨幣貶值的影響,消費者對價格更加敏感,但在聖保羅和布宜諾斯艾利斯等都市區,對網狀網路套裝的需求仍在成長。

儘管北美和歐洲的普及率已趨於成熟,但Wi-Fi 7的升級和託管服務的興起仍在持續推動設備的更換。在美國,預計到2025年9月,光纖連接數量將超過1億,這將促進支援Gigabit對稱吞吐量的路由器的普及。 Charter公司具備5G容錯移轉功能的Wi-Fi 7閘道已證明託管模式的有效性,它能夠減輕支援負擔並提高客戶滿意度。中東地區(例如阿拉伯聯合大公國和沙烏地阿拉伯)的智慧城市計畫正在推動對企業級路由器的需求,而非洲許多地區由於依賴行動寬頻,高階路由器的普及率仍然有限。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 光纖到府 (FTTH) 部署的加速推動了路由器的升級。

- Wi-Fi 6 和 6E 標準在小型辦公室/家庭辦公室 (SOHO) 環境中的快速普及

- 混合辦公和遠距辦公的普及需要企業級家庭網路。

- 利用網狀Wi-Fi系統消除通訊盲區

- 利用人工智慧驅動的流量最佳化,打造高階差異化優勢。

- 由網路服務供應商提供的安全訂閱服務捆綁銷售,縮短了續訂週期。

- 市場限制因素

- 新興市場對價格的敏感度阻礙了高階產品的廣泛普及。

- 由於技術快速過時導致產品生命週期縮短

- 6 GHz 頻段政策的分散化正在推遲 Wi-Fi 6E/7 的發布。

- 供應鏈中半導體短缺正在限制生產。

- 產業供應鏈分析

- 宏觀經濟因素對市場的影響

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按頻寬標準

- Wi-Fi 5

- Wi-Fi 6

- Wi-Fi 6E

- Wi-Fi 7

- 依產品類型

- 單頻段路由器

- 雙頻路由器

- 三頻路由器

- 網狀Wi-Fi系統

- 遊戲路由器

- 可攜式旅行路由器

- 透過分銷管道

- 線上零售

- 網路服務供應商/通訊業者配套服務

- 家用電器商店

- 大眾市場/大賣場

- 按應用程式/按使用者類型

- 住宅

- 小規模辦公室/家庭辦公室 (SOHO)

- 中小企業

- 遠距工作者

- 遊戲愛好者

- 智慧家庭/物聯網

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- TP-Link Corporation Limited

- NETGEAR-Inc.

- ASUSTeK Computer Inc.

- Shenzhen Tenda Technology Co., Ltd.

- AVM GmbH

- Linksys USA, Inc.

- D-Link Corporation

- Belkin International, Inc.

- Ubiquiti Inc.

- MikroTikls SIA

- Synology Inc.

- TRENDnet, Inc.

- GL Technologies(Hong Kong)Limited

- Peplink International Limited

- DrayTek Corp.

- Comtrend Corporation

- Ruijie Networks Co., Ltd.

- Mercusys Technologies Co., Ltd.

- Edimax Technology Co., Ltd.

- Xiaomi Communications Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the sOHO router market size was valued at USD 10.92 billion in 2025 and estimated to grow from USD 11.83 billion in 2026 to reach USD 17.82 billion by 2031, at a CAGR of 8.54% during the forecast period (2026-2031).

This report is Segmented by Frequency Band (Single-Band, Dual-Band, Tri-Band, and Quad-Band), Wi-Fi Standard (Wi-Fi 4, Wi-Fi 5, Wi-Fi 6, Wi-Fi 6E, and Wi-Fi 7), Application (Residential, Home Office, Small Office, and More), Distribution Channel (Online Retail, Offline Retail, ISP Bundled CPE, and Enterprise Channel Partners), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global SOHO Router Market Trends and Insights

Integration of AI Accelerators in Routers Enabling Real-Time Traffic Optimization

Routers embedding neural-processing units have shifted from passive packet forwarding to active orchestration. Charter Spectrum introduced Wi-Fi 7 gateways with on-device AI in 2025, reporting lower support calls after dynamic congestion rerouting. Qualcomm confirmed more than 250 networking designs using Wi-Fi 7 chipsets equipped with inference engines in its 2025 investor briefing. Such silicon classifies traffic flows and prioritizes latency-sensitive packets without manual quality-of-service rules. Households running simultaneous video conferences, cloud gaming, and IoT sensors benefit from lower jitter, reducing churn for service providers. Predictive alerts that flag anomalous traffic create upsell opportunities for managed security subscriptions.

Rapid Adoption of Wi-Fi 6 and Wi-Fi 7 Standards

The Wi-Fi Alliance certified 233 million Wi-Fi 7 devices in 2024 and forecasts 2.1 billion by 2028, eclipsing the ramp of Wi-Fi 6. MediaTek's Filogic 880 and 660 platforms began shipping in 2025, enabling sub-USD 200 tri-band routers. Broadcom and Qualcomm followed with quad-band reference designs that exploit 320-MHz channels and 4096-QAM to achieve 40 Gbps throughput. January 2026 FCC authorization for standard-power 6 GHz devices removed indoor-range limits, catalyzing small-office and industrial uptake. Together, lower chipset costs and regulatory clarity compress replacement windows for Wi-Fi 5 hardware.

Growing Substitution Threat from 5G Fixed-Wireless Gateways Bundled by Carriers

T-Mobile bundles Inseego's FX4200 and FX4100 gateways at zero upfront cost, integrating tri-band Wi-Fi 7 and 5G backhaul to displace standalone routers. Qualcomm's single-die Dragonwing platform further lowers bill-of-materials, letting carriers subsidize hardware. Small enterprises seeking unified billing opt for these gateways, eroding retail router volumes, especially in areas where fiber is scarce.

Other drivers and restraints analyzed in the detailed report include:

- Accelerated Rollout of Fiber and 5G Home Broadband Services

- ISPs Transitioning to Subscription-Based Managed Wi-Fi Services for SOHO Customers

- Cybersecurity Vulnerabilities and Firmware Update Negligence

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Tri-band routers boosted the SOHO router market share by capturing latency-sensitive 4K streaming and cloud gaming demand in 2025. Dual-band systems still dominate the mid-priced tiers, but tri-band shipments are forecast to grow faster than the overall SOHO router market through 2031. Lower-cost Wi-Fi 7 silicon from MediaTek and Broadcom lowered street prices beneath USD 200, bringing multi-gigabit capacity to mass-market budgets.

Mesh networking is the principal catalyst: quad-band designs dedicate a 6 GHz radio for backhaul, delivering deterministic latency without Ethernet cabling. Regulatory clearance for standard-power 6 GHz radios in January 2026 allows tri-band kits to cover larger floorplates, boosting attachment rates in suburban homes. Single-band devices linger only in ultra-low-cost brackets and embedded IoT endpoints, signaling eventual obsolescence as chipset costs continue to fall.

Wi-Fi 5 still anchors value-tier ISP bundles in 2025, yet Wi-Fi 7's 24.76% CAGR positions it as the volume engine for the SOHO router market size beyond 2027. FCC authorization for higher-power 6 GHz operation expanded viable coverage footprints, while chipset vendors raced to integrate 320 MHz channels and multi-link operation. Early adopters in gaming and prosumer niches validated willingness to upgrade ahead of device cycles, shortening refresh intervals.

Enterprise-grade small offices prize Wi-Fi 6E for its OFDMA efficiency and target wake time features that prolong IoT battery life. Wi-Fi 4 and earlier generations are in steady decline, limited to legacy industrial controllers pending retrofit budgets. As more client devices ship with tri-band radios, interoperability concerns recede, widening replacement opportunities for vendors.

Geography Analysis

Asia-Pacific contributed 36.52% to the SOHO router market in 2025, buoyed by China's universal-broadband policy and India's tier-2 fiber rollouts. Xiaomi monetized 904.6 million connected devices across its ecosystem, leveraging flash sales to lift router penetration in India (13.4% unit share) and Southeast Asia (16.7%). Japan's dense apartment clusters accelerated Wi-Fi 6E adoption, while Australia's NBN upgrades drove replacements of legacy ADSL hardware. The region's heterogeneity divides demand between cost-optimized dual-band units and premium quad-band offerings.

South America leads growth at 10.46% CAGR as carriers extend fiber to secondary cities. Brazil, Chile, Peru and Mexico each exceeded 70% fiber penetration by late 2024, exposing bandwidth constraints in 2.4 GHz-only routers. TP-Link's upcoming Brazilian factory will shorten supply chains and lower landed costs, while Xiaomi ranks second in regional share at 17.9%. Economic headwinds and currency depreciation heighten price sensitivity, but mesh bundles gain traction in urban Sao Paulo and Buenos Aires.

North America and Europe show mature penetration yet sustain replacement demand through Wi-Fi 7 upgrades and managed-service transitions. U.S. fiber passings crossed 100 million by September 2025, driving the adoption of routers capable of gigabit symmetric throughput. Charter's Wi-Fi 7 gateway with 5G failover reduced support overhead and improved customer satisfaction, validating the managed model. Middle East smart-city agendas in the UAE and Saudi Arabia drive enterprise-grade router demand, whereas much of Africa relies on mobile broadband, limiting high-end router adoption.

- TP-Link Corporation Limited

- NETGEAR-Inc.

- ASUSTeK Computer Inc.

- Shenzhen Tenda Technology Co., Ltd.

- AVM GmbH

- Linksys USA, Inc.

- D-Link Corporation

- Belkin International, Inc.

- Ubiquiti Inc.

- MikroTikls SIA

- Synology Inc.

- TRENDnet, Inc.

- GL Technologies (Hong Kong) Limited

- Peplink International Limited

- DrayTek Corp.

- Comtrend Corporation

- Ruijie Networks Co., Ltd.

- Mercusys Technologies Co., Ltd.

- Edimax Technology Co., Ltd.

- Xiaomi Communications Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Fibre-to-the-Home Roll-outs Boosting Router Upgrades

- 4.2.2 Rapid Adoption of Wi-Fi 6 and 6E Standards in SOHO Environments

- 4.2.3 Growth of Hybrid and Remote Work Requiring Enterprise-Grade Home Networking

- 4.2.4 Mesh Wi-Fi Systems Eliminating Coverage Dead Zones

- 4.2.5 AI-Enabled Traffic Optimisation Creating Premium Differentiation (Under-the-Radar)

- 4.2.6 ISP Bundled Security Subscriptions Increasing Refresh Cycles (Under-the-Radar)

- 4.3 Market Restraints

- 4.3.1 Price Sensitivity in Emerging Markets Limiting High-End Adoption

- 4.3.2 Rapid Technology Obsolescence Shortening Product Life Cycles

- 4.3.3 Fragmented 6 GHz Spectrum Policies Delaying Wi-Fi 6E/7 Launches (Under-the-Radar)

- 4.3.4 Supply-Chain Semiconductor Shortages Constraining Production (Under-the-Radar)

- 4.4 Industry Supply-Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Bandwidth Standard

- 5.1.1 Wi-Fi 5

- 5.1.2 Wi-Fi 6

- 5.1.3 Wi-Fi 6E

- 5.1.4 Wi-Fi 7

- 5.2 By Product Type

- 5.2.1 Single-band Router

- 5.2.2 Dual-band Router

- 5.2.3 Tri-band Router

- 5.2.4 Mesh Wi-Fi System

- 5.2.5 Gaming Router

- 5.2.6 Portable Travel Router

- 5.3 By Distribution Channel

- 5.3.1 Online Retail

- 5.3.2 ISP/Telecom Provider Bundles

- 5.3.3 Electronics Specialty Stores

- 5.3.4 Mass Market/Hypermarket

- 5.4 By Application/User Type

- 5.4.1 Residential Home

- 5.4.2 Small Office/Home Office (SOHO)

- 5.4.3 Small Business (SMB)

- 5.4.4 Remote Workforce

- 5.4.5 Gaming Enthusiasts

- 5.4.6 Smart Home/IoT

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 United Kingdom

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 TP-Link Corporation Limited

- 6.4.2 NETGEAR-Inc.

- 6.4.3 ASUSTeK Computer Inc.

- 6.4.4 Shenzhen Tenda Technology Co., Ltd.

- 6.4.5 AVM GmbH

- 6.4.6 Linksys USA, Inc.

- 6.4.7 D-Link Corporation

- 6.4.8 Belkin International, Inc.

- 6.4.9 Ubiquiti Inc.

- 6.4.10 MikroTikls SIA

- 6.4.11 Synology Inc.

- 6.4.12 TRENDnet, Inc.

- 6.4.13 GL Technologies (Hong Kong) Limited

- 6.4.14 Peplink International Limited

- 6.4.15 DrayTek Corp.

- 6.4.16 Comtrend Corporation

- 6.4.17 Ruijie Networks Co., Ltd.

- 6.4.18 Mercusys Technologies Co., Ltd.

- 6.4.19 Edimax Technology Co., Ltd.

- 6.4.20 Xiaomi Communications Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

工業路由器市場:2026-2032年全球市場預測(依產品類型、連接技術、部署環境、最終用戶產業及銷售管道)

工業路由器市場:2026-2032年全球市場預測(依產品類型、連接技術、部署環境、最終用戶產業及銷售管道) 2026年全球電信級路由市場報告全球乙太網路路由器市場報告(2026 年)

2026年全球電信級路由市場報告全球乙太網路路由器市場報告(2026 年) 路由器市場規模、佔有率和成長分析:按產品類型、頻寬類型、技術、應用、銷售管道、最終用戶和地區分類-2026-2033年產業預測

路由器市場規模、佔有率和成長分析:按產品類型、頻寬類型、技術、應用、銷售管道、最終用戶和地區分類-2026-2033年產業預測 工業路由器市場:按產品類型、最終用戶和地區分類

工業路由器市場:按產品類型、最終用戶和地區分類 高耐久性路由器:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年)服務供應商的路由器:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)消費級路由器:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)2026年全球路由器市場報告2026年全球電信級路由系統(CRS)市場報告

高耐久性路由器:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年)服務供應商的路由器:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)消費級路由器:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)2026年全球路由器市場報告2026年全球電信級路由系統(CRS)市場報告