|

市場調查報告書

商品編碼

2063814

消費級路由器:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)Consumer Router - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

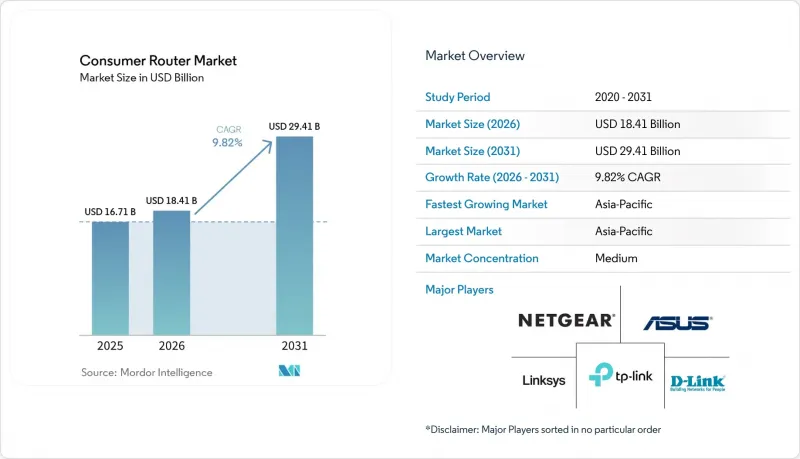

根據 Mordor Intelligence 預測,消費路由器市場規模預計將在 2025 年達到 167 億美元,2026 年達到 184.1 億美元,到 2031 年達到 294.1 億美元,2026 年至 2031 年的複合年成長率為 9.82%。

本報告按產品類型(單頻段、雙頻、三頻、網狀Wi-Fi系統)、技術標準(Wi-Fi 5、Wi-Fi 6、Wi-Fi 6E、Wi-Fi 7 Ready)、應用領域(住宅、小規模辦公室/家庭辦公室 (SOHO) 以及中小企業)、銷售管道(線上和線下)以及他地區(北美、中小企業及其地區)以及他地區(線上和線下)以及他地區(北美地區和線下)以及其他地區進行細分。市場預測以美元 (USD) 為單位。

全球消費路由器市場趨勢及洞察

Wi-Fi 6 和 Wi-Fi 6E 標準的快速普及

Wi-Fi 6E 在 6 GHz 頻段開放了七個 160 MHz 寬的頻道,緩解了傳統的頻道擁塞問題,並支援雲端遊戲和虛擬實境等對延遲敏感的應用場景。強制性的 WPA3 加密和雜湊到元素金鑰交換提高了安全標準,並減少了降級攻擊的攻擊面。 Wi-Fi 7 採用多鏈路操作,聚合 2.4、5 和 6 GHz頻寬,理論吞吐量可提升至 40 Gbps 以上,預計到 2029 年,其市場佔有率將佔消費級和企業級網路基地台出貨量的 90% 以上。華碩在 CES 2026 上透過 ROG NeoCore 展示了這項能力,揭示了主要標準兩年一次的發布週期以及產品生命週期的縮短。雖然亞太地區頻段分配不均增加了全球 SKU 規劃的難度,但在領先部署的地區,產品更新換代速度已加快。因此,路由器升級的投資回收期縮短了,這直接促進了消費路由器市場的發展。

智慧家庭和物聯網設備的安裝正在迅速增加。

目前,平均每個家庭擁有 17-18 台連網設備,高於 2022 年的 11 台。此外,預計到 2027 年,全球 68.6% 的家庭將擁有連網設備。由於超過 40 台設備爭奪頻寬,傳統的單頻段路由器已無法滿足需求,導致服務品質顯著下降。同時,安全風險也在不斷擴大。一項 2025 年的研究預測,每個物聯網設備每月將面臨 5200 次惡意連線試驗,其中 75% 的嘗試會利用路由器漏洞。 TP-Link 等廠商正在利用機器學習技術最佳化設備效能,以優先處理即時流量,並在非尖峰時段安排韌體下載。 Matter 認證生態系統的興起,對 IPv6 原生支援和持續低功耗連接提出了更高的要求,並為路由器晶片樹立了新的標準。這些趨勢共同推動了產品生命週期中期的升級,並重振了消費級路由器市場。

三頻和網狀系統的平均售價較高

NETGEAR Orbi 970 和 ASUS ZenWiFi Pro ET12 等旗艦級 Mesh 套裝售價在 1200 美元到 1500 美元之間,對許多家庭來說屬於高階價位。 NETGEAR 於 2025 年 7 月推出的 Orbi 370 雙包裝售價 599 美元,將入門門檻降低了 30%,但其價格仍然高於 150 美元以下的“最佳價位”,而這一價位目前主導著市場。雙頻產品目前佔出貨量的 65%,但總收入卻不到 40%,凸顯了利潤率面臨的壓力。廠商們陷入兩難:要嘛蠶食高價產品線,要嘛將高利潤市場拱手讓給競爭對手。這種價格兩極化抑制了消費者的升級意願,並對消費級路由器市場造成了沉重打擊。

細分市場分析

預計到2031年,網狀網路系統將以每年14.30%的速度成長,成為消費級路由器市場中成長最快的產品。雙頻路由器曾是行業標準,在2025年佔據了65.12%的出貨量,但隨著家庭用戶意識到兩個無線模組無法有效支援超過17個物聯網設備,其市場佔有率正在下降。三頻路由器憑藉其高頻寬回程傳輸,正在推動北美和歐洲市場的普及,這對於遊戲玩家和內容創作者來說,是實現低延遲上傳的關鍵。單頻段路由器目前在429元人民幣(約61美元)以下的價位區間佔據著一定的市場佔有率,例如在幾內亞的固定無線接入市場。

NETGEAR 的 Orbi 370(售價 599 美元)壓縮了性價比曲線,並普及了此前僅限於售價 1200 美元旗艦機型的 320MHz 頻道和 4K QAM 技術。 Wi-Fi 聯盟預計到 2026 年初將認證超過 1200 款 Wi-Fi 7 產品,由此產生的基準降低了晶片成本。中國廠商騰達憑藉售價 429 元人民幣(約 61 美元)的泰山 BE7200 Ultra 進一步降低了價格,迫使全球品牌維持利潤率。如今,廠商的成功取決於如何在 150 美元以下的雙頻產品中平衡吞吐量預期與高階網狀網路產品的差異化優勢,而這種權衡將在未來五年內決定消費級路由器市場的規模。

預計到2025年,Wi-Fi 6的出貨量佔有率將保持在45.21%,這表明其市場已趨於成熟,且設備相容性廣泛。同時,Wi-Fi 6E預計將以12.49%的年均成長率成長至2031年。推動這項轉變的主要因素是免授權的6GHz頻段,提供7160MHz的頻道,可以避免傳統頻寬的擁塞。預計支援Wi-Fi 7的設備出貨量將從2025年的5.83億台激增至2026年的11億台,增幅高達88%,超過了Wi-Fi標準以往的普及速度。

Wi-Fi 5 在售價低於 50 美元的低價路由器市場仍佔據 22% 的佔有率。華碩在 2026 年國際消費電子展 (CES) 上發布的支援 Wi-Fi 8 的 ROG NeoCore 平台,其產品週期為兩年,預計將縮短路由器的投資回收期,並擴大尖端消費級路由器市場。然而,持續的監管碎片化迫使廠商進行雙重認證,推高了研發成本。隨著更多地區統一 6 GHz 頻段的監管規定,產品藍圖也將更加標準化,從而提升採購議價能力,並縮短新產品上市時間。

區域分析

預計到2025年,亞太地區將以34.12%的營收佔有率主導消費級路由器市場,並在2031年之前維持11.13%的複合年成長率。光是在印度,到2025年就將新增2,800萬個光纖連接,這將繞過傳統的DSL網路,並推動二、三線城市對Gigabit路由器的需求。憑藉垂直整合和在地化韌體,中國廠商TP-Link、華為、小米和騰達佔據了超過70%的國內市場佔有率。小米將於2026年4月推出售價1799元人民幣(約248美元)的“BE3600 Pro”,華為也將推出售價2499元人民幣(約合364美元)的可攜式路由器“Wi-Fi X”,這凸顯了Wi-Fi 7在該地區快速普及的趨勢。

2025年,北美和歐洲合計約佔總銷售額的48%。儘管隨著產品更換週期延長至四年以上,年均成長率已放緩至8.5%,但三頻網狀網路設備的高滲透率仍維持較高的銷售密度。美國聯邦通訊委員會(FCC)於2026年3月禁止銷售某些外國製造的路由器,這迫使廠商改變設計並實現供應商多元化,可能會減緩產品創新。相較之下,歐盟統一的6GHz頻段框架正在加速Wi-Fi 6E設備的市場推廣。

預計南美市場將從2024年的14.5億美元成長到2034年的51.8億美元,複合年成長率達14.3%,其中巴西的消費額佔該地區總消費額的一半以上。中東和非洲地區仍處於發展初期,但潛力巨大,售價低於100美元的固定無線LTE路由器有助於彌補數位落差。進口關稅、外匯波動和多語言韌體等本地化壁壘促使利潤率較低的區域性公司進入市場,但能夠應對這些挑戰的跨國公司則有機會抓住機遇,進一步擴大其在消費路由器市場的佔有率。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 新興國家的寬頻普及率

- Wi-Fi 6 和 Wi-Fi 6E 標準的快速普及

- 智慧家庭和物聯網設備的普及率正在迅速提高。

- 遠距辦公和混合學習模式的擴展

- 通訊業者提供的優質路由器套餐

- 面向消費者的路由器中的人工智慧網路最佳化

- 市場限制因素

- 半導體供應短缺問題依然存在。

- 三頻和網狀系統的平均售價較高

- 消費者對Wi-Fi標準的認知度較低

- 網路安全和韌體維護挑戰

- 產業供應鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 依產品類型

- 單頻段路由器

- 雙頻路由器

- 三頻路由器

- 網狀Wi-Fi系統

- 依技術標準

- Wi-Fi 5(802.11ac)

- Wi-Fi 6(802.11ax)

- Wi-Fi 6E(6 GHz)

- Wi-Fi 7 Ready(802.11be)

- 透過使用

- 住宅

- 小型辦公室/家庭辦公室 (SOHO)

- 小規模企業

- 透過分銷管道

- 線上零售

- 線下零售

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他亞太國家

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 肯亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- TP-Link Technologies Co., Ltd.

- NETGEAR, Inc.

- ASUSTeK Computer Inc.

- D-Link Corporation

- Linksys Holdings, Inc.

- Ubiquiti Inc.

- MikroTikls SIA

- Zyxel Communications Corporation

- Shenzhen Tenda Technology Co., Ltd.

- Mercusys Technologies Co., Ltd.

- eero LLC

- Google LLC(Nest Devices)

- Buffalo Inc.

- AVM Computersysteme Vertriebs GmbH

- Edimax Technology Co., Ltd.

- Peplink International Limited

- DrayTek Corp.

- Comtrend Corporation

- Synology Inc.

- Huawei Device Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the consumer router market size is expected to be USD 16.7 billion in 2025, USD 18.41 billion in 2026, and reach USD 29.41 billion by 2031, growing at a CAGR of 9.82% from 2026 to 2031.

This report is Segmented by Product Type (Single-Band, Dual-Band, Tri-Band, and Mesh Wi-Fi Systems), Technology Standard (Wi-Fi 5, Wi-Fi 6, Wi-Fi 6E, and Wi-Fi 7 Ready), Application (Residential, Small Office / Home Office (SOHO), and Small Business), Distribution Channel (Online, and Offline), and Geography (North America, Asia Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Consumer Router Market Trends and Insights

Rapid Adoption Of Wi-Fi 6 And Wi-Fi 6E Standards

Wi-Fi 6E opens seven 160 MHz-wide channels in the 6 GHz band, eliminating legacy channel congestion and supporting latency-sensitive use cases such as cloud gaming and virtual reality. Mandatory WPA3 encryption and Hash-to-Element key exchange raise the security baseline, shrinking the attack surface for downgrade exploits. Wi-Fi 7 is forecast to exceed 90% of consumer and enterprise access-point shipments by 2029, driven by multi-link operation that aggregates 2.4, 5, and 6 GHz spectrum for theoretical throughput above 40 Gbps. ASUS showcased this capability at CES 2026 through the ROG NeoCore, revealing a two-year cadence between major standard releases and compressing product life cycles. Uneven spectrum allocation across Asia-Pacific complicates global SKU planning, yet early-moving jurisdictions are already recording accelerated replacement cycles. The net result is a shortening payback period for router upgrades, which directly lifts the consumer router market.

Surge In Smart-Home And IoT Device Installations

Households now average 17-18 connected endpoints, up from 11 in 2022, and device penetration is projected to reach 68.6% of global homes by 2027. Legacy single-band routers struggle when 40+ devices contend for airtime, leading to noticeable quality-of-service degradation. Security risks have scaled in parallel; a 2025 study reported 5,200 malicious connection attempts per IoT device each month, with 75% exploiting router vulnerabilities. Vendors such as TP-Link use on-device machine learning to prioritize real-time traffic and schedule firmware downloads during off-peak periods. The rise of Matter-certified ecosystems demands IPv6-native support and persistent low-power links, forcing a new baseline for router silicon. Collectively, these dynamics accelerate mid-cycle upgrades and uplift the consumer router market.

High Average Selling Prices Of Tri-Band And Mesh Systems

Flagship mesh kits such as NETGEAR Orbi 970 and ASUS ZenWiFi Pro ET12 list between USD 1,200 and USD 1,500, pricing many households out of the premium tier. NETGEAR's July 2025 Orbi 370 introduction at USD 599 for a two-pack narrowed the entry barrier by 30%, but it still exceeds the sub-USD 150 sweet spot that dominates unit volumes. Dual-band products now account for 65% of shipments yet generate under 40% of total revenue, underscoring margin compression. Vendors are caught between cannibalizing their own value portfolios and conceding the high-margin segment to rivals. This price bifurcation slows upgrade intent and weighs on the consumer router market.

Other drivers and restraints analyzed in the detailed report include:

- Growth Of Remote Work And Hybrid Learning Models

- Mainstream Broadband Penetration In Emerging Economies

- Persistent Semiconductor Supply Constraints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mesh systems are growing at 14.30% annually through 2031, the fastest within the consumer router market. Dual-band routers, once the default, accounted for 65.12% of 2025 unit volume, yet their share is eroding as households discover that two radios cannot efficiently serve 17+ IoT endpoints. Tri-band designs dedicate a high-band backhaul that gamers and content creators value for low-latency uploads, lifting attach rates in North America and Europe. Single-band models now play niche roles, such as in Guinea's fixed-wireless access market, priced at CNY 429 (USD 61) or less.

NETGEAR's Orbi 370 at USD 599 compresses the price-performance curve, democratizing 320 MHz channels and 4K QAM that were confined to USD 1,200 flagships. The Wi-Fi Alliance certified more than 1,200 Wi-Fi 7 products by early 2026, unleashing scale economies that lower silicon cost baselines. Chinese challenger Tenda pushed price walls further with the Taishan BE7200 Ultra at CNY 429 (USD 61), pressuring global brands to defend margins. Vendor success now hinges on balancing sub-USD 150 dual-band throughput expectations with premium mesh differentiation, a trade-off central to the trajectory of the consumer router market size over the next five years.

Wi-Fi 6 retained 45.21% shipment share in 2025, indicating maturity and broad device compatibility, while Wi-Fi 6E is climbing 12.49% annually through 2031. The shift is principally motivated by the unlicensed 6 GHz spectrum, which provides 7 160 MHz channels, bypassing congestion in older bands. Wi-Fi 7 device shipments jumped from 583 million in 2025 to 1.1 billion in 2026, signaling an 88% growth rate that eclipses prior adoption curves for Wi-Fi standards.

Wi-Fi 5 stubbornly clings to 22% share in low-cost routers priced below USD 50. ASUS's CES 2026 preview of a Wi-Fi 8-ready ROG NeoCore platform demonstrates a two-year cadence that will likely compress router amortization periods and expand the consumer router market in bleeding-edge segments. Persistent regulatory fragmentation, however, forces vendors to maintain dual certification pathways, which inflate engineering costs. As more jurisdictions harmonize 6 GHz rules, unified SKU roadmaps will emerge, offering procurement leverage and reducing time-to-market for new designs.

Geography Analysis

Asia-Pacific dominated the consumer router market in 2025 with 34.12% revenue share and is projected to post an 11.13% CAGR through 2031. India alone added 28 million fiber connections in 2025, leapfrogging legacy DSL and driving demand for multi-gigabit routers in tier-2 and tier-3 cities. Chinese vendors, TP-Link, Huawei, Xiaomi, and Tenda, maintain more than 70% domestic share, propped up by vertical integration and localized firmware. Xiaomi's April 2026 BE3600 Pro release at CNY 1,799 (USD 248) and Huawei's Wi-Fi X portable router at CNY 2,499 (USD 364) spotlight the rapid commoditization of Wi-Fi 7 in the region.

North America and Europe collectively contributed about 48% of 2025 revenue. Growth moderates to 8.5% annually as replacement cycles lengthen beyond 4 years, but high attach rates for tri-band mesh units keep revenue density elevated. The Federal Communications Commission's March 2026 ban on specified foreign-sourced routers is forcing redesigns and supplier diversification, potentially delaying product refreshes. The European Union's harmonized 6 GHz framework, in contrast, accelerates time-to-market for Wi-Fi 6E devices.

South America is slated to grow from USD 1.45 billion in 2024 to USD 5.18 billion by 2034, with a 14.3% CAGR, with Brazil capturing more than half of the regional spend. The Middle East and Africa remain early-stage but show outsized potential, with fixed-wireless LTE routers priced under USD 100 bridging the digital divide. Localization hurdles, including import duties, currency volatility, and multilingual firmware, favor lower-margin regional entrants, but multinationals that address these frictions can unlock incremental market share in the consumer router market.

- TP-Link Technologies Co., Ltd.

- NETGEAR, Inc.

- ASUSTeK Computer Inc.

- D-Link Corporation

- Linksys Holdings, Inc.

- Ubiquiti Inc.

- MikroTikls SIA

- Zyxel Communications Corporation

- Shenzhen Tenda Technology Co., Ltd.

- Mercusys Technologies Co., Ltd.

- eero LLC

- Google LLC (Nest Devices)

- Buffalo Inc.

- AVM Computersysteme Vertriebs GmbH

- Edimax Technology Co., Ltd.

- Peplink International Limited

- DrayTek Corp.

- Comtrend Corporation

- Synology Inc.

- Huawei Device Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mainstream Broadband Penetration in Emerging Economies

- 4.2.2 Rapid Adoption of Wi-Fi 6 and Wi-Fi 6E Standards

- 4.2.3 Surge in Smart-Home and IoT Device Installations

- 4.2.4 Growth of Remote Work and Hybrid Learning Models

- 4.2.5 Telecom ISP Bundling of Premium Routers

- 4.2.6 AI-Enabled Network Optimisation in Consumer Routers

- 4.3 Market Restraints

- 4.3.1 Persistent Semiconductor Supply Constraints

- 4.3.2 High Average Selling Prices of Tri-Band and Mesh Systems

- 4.3.3 Limited Consumer Awareness of Wi-Fi Standards

- 4.3.4 Cyber-security and Firmware Maintenance Challenges

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porters Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensiyt of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Single-Band Routers

- 5.1.2 Dual-Band Routers

- 5.1.3 Tri-Band Routers

- 5.1.4 Mesh Wi-Fi Systems

- 5.2 By Technology Standard

- 5.2.1 Wi-Fi 5 (802.11ac)

- 5.2.2 Wi-Fi 6 (802.11ax)

- 5.2.3 Wi-Fi 6E (6 GHz)

- 5.2.4 Wi-Fi 7 Ready (802.11be)

- 5.3 By Application

- 5.3.1 Residential

- 5.3.2 Small Office / Home Office (SOHO)

- 5.3.3 Small Business

- 5.4 By Distribution Channel

- 5.4.1 Online Retail

- 5.4.2 Offline Retail

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Kenya

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 TP-Link Technologies Co., Ltd.

- 6.4.2 NETGEAR, Inc.

- 6.4.3 ASUSTeK Computer Inc.

- 6.4.4 D-Link Corporation

- 6.4.5 Linksys Holdings, Inc.

- 6.4.6 Ubiquiti Inc.

- 6.4.7 MikroTikls SIA

- 6.4.8 Zyxel Communications Corporation

- 6.4.9 Shenzhen Tenda Technology Co., Ltd.

- 6.4.10 Mercusys Technologies Co., Ltd.

- 6.4.11 eero LLC

- 6.4.12 Google LLC (Nest Devices)

- 6.4.13 Buffalo Inc.

- 6.4.14 AVM Computersysteme Vertriebs GmbH

- 6.4.15 Edimax Technology Co., Ltd.

- 6.4.16 Peplink International Limited

- 6.4.17 DrayTek Corp.

- 6.4.18 Comtrend Corporation

- 6.4.19 Synology Inc.

- 6.4.20 Huawei Device Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

工業路由器市場:2026-2032年全球市場預測(依產品類型、連接技術、部署環境、最終用戶產業及銷售管道)

工業路由器市場:2026-2032年全球市場預測(依產品類型、連接技術、部署環境、最終用戶產業及銷售管道) 2026年全球電信級路由市場報告全球乙太網路路由器市場報告(2026 年)

2026年全球電信級路由市場報告全球乙太網路路由器市場報告(2026 年) 路由器市場規模、佔有率和成長分析:按產品類型、頻寬類型、技術、應用、銷售管道、最終用戶和地區分類-2026-2033年產業預測

路由器市場規模、佔有率和成長分析:按產品類型、頻寬類型、技術、應用、銷售管道、最終用戶和地區分類-2026-2033年產業預測 工業路由器市場:按產品類型、最終用戶和地區分類

工業路由器市場:按產品類型、最終用戶和地區分類 高耐久性路由器:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年)SOHO路由器:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)服務供應商的路由器:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)2026年全球路由器市場報告2026年全球電信級路由系統(CRS)市場報告

高耐久性路由器:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年)SOHO路由器:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)服務供應商的路由器:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)2026年全球路由器市場報告2026年全球電信級路由系統(CRS)市場報告