|

市場調查報告書

商品編碼

2063863

歐洲GPU浸沒式散熱:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)Europe GPU Immersion Cooling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

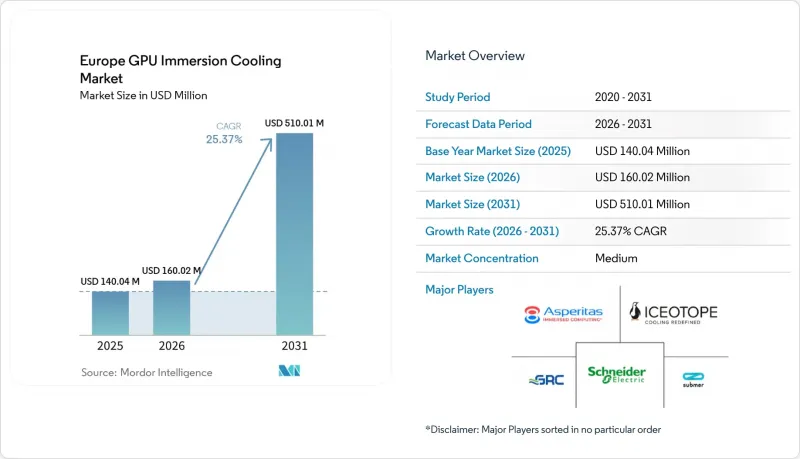

根據 Mordor Intelligence 預測,歐洲 GPU 液冷市場規模預計在 2025 年達到 1.4004 億美元,在 2026 年達到 1.6002 億美元,在 2031 年達到 5.1001 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 25.37%。

本報告按浸沒方式(單相和兩相)、解決方案類型(儲罐/系統、介電液和浸沒式最佳化GPU伺服器)、部署類型(超大規模/雲端、企業級以及面向政府和研究機構的高效能運算)、GPU功率密度(低於300W、300W-700W和高於700W)以及地區細分(德國、法國等)以及地區細分。市場預測以美元計價。

歐洲GPU浸沒式散熱市場趨勢與洞察

人工智慧和高效能運算工作負載的激增正在推動高密度GPU的普及。

以NVIDIA H100和H200加速器為核心的生成式AI訓練機架,其功耗通常超過120千瓦,這一水準已超出傳統空氣冷卻方式的經濟極限。各國和歐洲範圍內的研究舉措正在資助數十億歐元的基礎設施項目,這些項目從一開始就強制要求採用液冷技術,為其他企業樹立了可效仿的典範。由EuroHPC支持的匈牙利和瑞典超級超級電腦計畫(將於2025年投入使用)明確規定,必須採用浸沒式冷卻設計來應對千兆次級(petaflop)的熱負載。這些旗艦系統強化了大規模應用的良性循環,降低了商業買家的技術風險。隨著即將推出的B系列GPU,以及單晶片功耗超過1千瓦,浸沒式冷卻正從實驗性方案轉變為維持機架吞吐量而不增加設施電力需求的必要手段。

歐盟資料中心永續性法規與碳排放目標

根據基於能源效率指令的授權法規,從2025年起,所有超過500千瓦的設施都必須公佈年度電力使用效率(PUE)和用水效率(WUE)指標。此資訊揭露制度將有利於採用液冷系統且PUE值達到1.05左右的設施。同時,氣候中和資料中心協議要求到2030年實現淨零排放運營,這有效地將液冷技術融入擴建計畫中。像Asperitas這樣的營運商已經展示了單相設計,其冷卻劑溫度足以直接供應區域供熱,從而滿足了協議中的廢熱條款。新近獲準的天然酯基絕緣液IEC標準提供了一種認證途徑,簡化了競標流程,進一步加速了其應用。

與傳統空氣冷卻系統相比,初始資本投入較高。

承包液冷機架的成本在 3 萬至 5 萬美元之間,遠高於傳統機架 1,000 至 2,000 美元的價格。然而,從整個設施的角度來看,考慮到規模經濟,液冷可能更具優勢。在現有設施的試點項目中,業主通常面臨 40% 的成本增加,因為他們必須重新鋪設冷凍水循環管道、加固地板荷載並安裝與絕緣油相容的監控系統。對於融資有限且遵循三年投資回報規則的公司而言,很難平衡這些經濟因素,尤其是在分階段升級空冷系統可以帶來短期效益的情況下。雖然「冷卻即服務」和租賃模式正在興起,但它們仍處於發展階段,對短期資本配置的影響有限。

細分市場分析

到2025年,單相液冷將佔據歐洲GPU液冷市場78.56%的佔有率,主要得益於其流體穩定性和簡易操作性方面的廣泛認可。隨著殼牌和Perstorp等供應商將不含PFAS的碳氫化合物冷卻液推向市場,歐洲GPU液冷市場中與單相設計相關的市場規模正在穩步成長,這不僅降低了成本,也降低了監管風險。企業對這些系統與現有冷凍水循環系統的兼容性表示讚賞,因為這有助於縮短維修時間。在都市區邊緣地區,Asperitas公司展示的無泵自然對流系統因其運行安靜且能夠產生55°C的出水溫度而備受關注,使其適用於區域供熱。

預計到2031年,兩相系統將以25.55%的複合年成長率成長,但目前仍主要集中在超大規模資料中心和機架密度超過150千瓦的研究設施。由於含氟流體的損耗、壓力控制的複雜性以及對專用密封材料的需求,兩相系統在這些細分市場之外的應用受到限制。由SINTEF共同資助的CoolHeatDC計畫旨在將直接連接到熱泵的兩相模組商業化。如果現場測試證實了預期的維護需求,這種配置可能會更具吸引力。雖然隨著GPU單一功耗接近1千瓦,兩相設計可望逐步獲得市場佔有率,但預計單相系統在本世紀末仍將佔據主導地位。

2025年,由於早期採用者分別機殼和伺服器,水箱和熱交換系統佔歐洲GPU浸沒式冷卻市場規模的55.34%。然而,隨著戴爾、惠普企業、聯想和超微等廠商推出包含伺服器底盤、冷板和認證冷卻液相容性的浸沒式最佳化SKU,這種採購模式正在改變。歐洲GPU浸沒式冷卻產業的觀察家指出,這些承包解決方案將縮短引進週期並消除保固糾紛,預計到2031年,整合式伺服器的成長率將達到25.63%,成為成長率最高的解決方案。

流體供應商正將永續性指標作為差異化優勢,例如Perstorp的無PFAS Synmerse系列和Oleon的植物來源配方。 DCX和Baltimore Aircoil等儲液罐製造商也積極響應,公開其標準化模組的面積,將大批量訂單的前置作業時間縮短至兩個月以內。分析師預測,一旦伺服器OEM廠商完成其GPU產品系列中液冷產品的擴展,營收重心將轉向整合系統。同時,獨立式儲液罐仍將在超大規模客製化開發和設施維修中發揮至關重要的作用。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 人工智慧和高效能運算工作負載的激增正在推動高密度GPU的普及。

- 絕緣油的價格大幅下降。

- 西歐不斷上漲的電價正在推動節能冷卻技術的應用。

- 歐盟關於資料中心永續性的法規和碳排放目標

- 歐洲浸沒式冷卻新創企業創業融資增加

- 歐洲都市區對邊緣資料中心的興趣日益濃厚

- 市場限制因素

- 獲得GPU認證的防水損壞保護保固服務的供應有限。

- 與傳統空氣冷卻系統相比,初始資本投入較高

- 歐盟各地介電液標準有差異

- 高性能儲槽和密封件的供應鏈限制因素

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 浸沒法

- 單相浸沒式冷卻

- 兩相浸沒式冷卻

- 按解決方案類型

- 浸入式冷卻罐/系統

- 介電液

- 針對液冷散熱最佳化的GPU伺服器系統

- 不同的發展

- 超大規模/雲

- 公司

- 政府和研究機構(高效能運算)

- 按GPU功率密度

- 小於300瓦

- 300W~700W

- 超過700瓦

- 按地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 歐洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Submer Technologies SL

- Asperitas BV

- Iceotope Technologies Limited

- Green Revolution Cooling Inc.

- Schneider Electric SE

- DCX-The Liquid Cooling Company Sp. z oo

- LiquidStack Inc.

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

- Lenovo Group Limited

- Atos SE

- Fujitsu Limited

- Super Micro Computer Inc.

- Rittal GmbH and Co. KG

- Vertiv Group Corp.

- Midas Green Technologies LLC

- Boston Limited

- Inspur Systems Inc.

- ASUS Tek Computer Inc.

- Trane Technologies plc

第7章 市場機會與未來展望

According to Mordor Intelligence, the europe gPU immersion cooling market size is expected to be USD 140.04 million in 2025, USD 160.02 million in 2026, and reach USD 510.01 million by 2031, growing at a CAGR of 25.37% from 2026 to 2031.

This report is Segmented by Immersion Type (Single-Phase, and Two-Phase), Solution Type (Tanks/Systems, Dielectric Fluids, and Immersion-Optimized GPU Servers), Deployment (Hyperscale/Cloud, Enterprise, and Government and Research HPC), GPU Power Density (Below 300W, 300W-700W, and Above 700W), and Geography (Germany, France, and More). The Market Forecasts are Provided in Terms of Value (USD).

Europe GPU Immersion Cooling Market Trends and Insights

Surging AI and HPC Workloads Driving Higher-Density GPU Deployments

Generative-AI training racks built around NVIDIA H100 and H200 accelerators routinely exceed 120 kilowatts, a level that outstrips the economic ceiling of raised-floor air cooling. National and pan-European research initiatives have funded billion-euro infrastructure projects that specify liquid cooling from day one, creating reference blueprints that enterprises can emulate. EuroHPC-backed supercomputers in Hungary and Sweden, both announced in 2025, openly mandate immersion-ready designs to cope with petaflop-scale heat loads. These flagship systems reinforce a virtuous cycle of volume commitments that lower technology risk for commercial buyers. As the forthcoming B-series GPU family pushes individual chip power past 1 kilowatt, immersion transitions from an experimental option to a necessity for maintaining rack throughput without a parallel rise in facility power.

EU Data Center Sustainability Regulations and Carbon Targets

The delegated regulation under the Energy Efficiency Directive compels sites above 500 kilowatts to publish annual power-usage-effectiveness and water-usage-effectiveness metrics beginning in 2025, a disclosure regime that favors immersion-equipped plants achieving PUE near 1.05. Parallel commitments under the Climate Neutral Data Centre Pact demand net-zero operations by 2030, effectively hard-coding liquid cooling into expansion blueprints. Operators such as Asperitas have demonstrated single-phase designs that deliver coolant temperatures high enough for direct district-heating export, addressing waste-heat clauses within the Pact. Newly approved IEC standards covering natural-ester dielectric fluids provide certification pathways that streamline tender procedures, further accelerating adoption.

High Up-Front Capex Versus Traditional Air Cooling

Turnkey immersion racks cost USD 30,000-50,000, dwarfing the USD 1,000-2,000 price of a conventional rack, even though whole-facility comparisons can favor immersion when scale effects are considered. Retrofit pilots often face a 40% cost premium because owners must re-plumb chilled-water loops, upgrade floor loading, and commission dielectric-compatible monitoring systems. Cash-constrained enterprises that operate under three-year payback rules struggle to reconcile those economics, particularly when incremental air-cooling upgrades deliver near-term relief. Cooling-as-a-service and leasing schemes are emerging but remain embryonic, limiting near-term impact on capital allocations.

Other drivers and restraints analyzed in the detailed report include:

- Escalating Electricity Prices in Western Europe Encouraging Energy-Efficient Cooling

- Rapid Decline in Dielectric Fluid Costs

- Limited Availability of GPU-Qualified Immersion-Ready Warranties

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Single-phase immersion cooling held 78.56% of the Europe GPU immersion cooling market share in 2025, underscoring widespread confidence in its fluid stability and simple operations. The Europe GPU immersion cooling market size tied to single-phase designs is expanding steadily as suppliers such as Shell and Perstorp bring PFAS-free hydrocarbon fluids to market, reducing both cost and regulatory risk. Enterprises value the compatibility of these systems with existing chilled-water loops, a factor that shortens retrofit timelines. In urban edge sites, pumpless natural-convection variants demonstrated by Asperitas are proving attractive because they operate quietly and generate 55-degree-Celsius outlet temperatures suitable for district heating.

Two-phase systems are on track for a 25.55% CAGR through 2031, yet they remain concentrated in hyperscale and research settings where rack densities cross 150 kilowatts. Fluorocarbon fluid loss, pressure-control complexity, and specialised seals have limited penetration outside those niches. The CoolHeatDC project, co-funded by SINTEF, aims to commercialise two-phase modules tied directly to heat pumps, a configuration that could broaden appeal if field trials validate maintenance expectations. As GPUs inch toward 1 kilowatt per device, two-phase designs will likely capture incremental share, though single-phase is set to maintain the majority position for the remainder of the decade.

Tanks and heat-exchange systems represented 55.34% of the Europe GPU immersion cooling market size in 2025 because early adopters sourced enclosures and servers separately. That procurement model is shifting as Dell, Hewlett Packard Enterprise, Lenovo, and Supermicro release immersion-optimized SKUs that bundle server chassis, cold plates, and certified fluid compatibility. Europe GPU immersion cooling industry observers note that these turnkey offers compress deployment cycles and eliminate warranty disputes, positioning integrated servers for the strongest growth at 25.63% through 2031.

Fluid suppliers are differentiating through sustainability metrics, with Perstorp's PFAS-free Synmerse range and Oleon's plant-based formulations highlighting the trend. Tank manufacturers such as DCX and Baltimore Aircoil have responded by publishing standardised module footprints, cutting lead times to under two months for high-volume orders. Analysts expect that once server OEMs finish extending liquid-ready lines across their full GPU portfolios, the balance of revenue will tilt toward integrated systems, while standalone tanks will retain relevance for hyperscale custom builds and facility retrofits.

List of Companies Covered in this Report:

- Submer Technologies SL

- Asperitas BV

- Iceotope Technologies Limited

- Green Revolution Cooling Inc.

- Schneider Electric SE

- DCX -The Liquid Cooling Company Sp. z o.o.

- LiquidStack Inc.

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

- Lenovo Group Limited

- Atos SE

- Fujitsu Limited

- Super Micro Computer Inc.

- Rittal GmbH and Co. KG

- Vertiv Group Corp.

- Midas Green Technologies LLC

- Boston Limited

- Inspur Systems Inc.

- ASUS Tek Computer Inc.

- Trane Technologies plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging AI and HPC Workloads Driving Higher-Density GPU Deployments

- 4.2.2 Rapid Decline in Dielectric Fluid Costs

- 4.2.3 Escalating Electricity Prices in Western Europe Encouraging Energy-Efficient Cooling

- 4.2.4 EU Data Center Sustainability Regulations and Carbon Targets

- 4.2.5 Increased Venture Funding for European Immersion Cooling Start-ups

- 4.2.6 Growing Preference for Edge Data Centers in Urban Europe

- 4.3 Market Restraints

- 4.3.1 Limited Availability of GPU-Qualified Immersion-Ready Warranties

- 4.3.2 High Up-Front Capex Versus Traditional Air Cooling

- 4.3.3 Fragmented Dielectric Fluid Standards Across EU

- 4.3.4 Supply Chain Constraints for High-Performance Tanks and Seals

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Immersion Type

- 5.1.1 Single-Phase Immersion Cooling

- 5.1.2 Two-Phase Immersion Cooling

- 5.2 By Solution Type

- 5.2.1 Immersion Cooling Tanks / Systems

- 5.2.2 Dielectric Fluids

- 5.2.3 Immersion-Optimized GPU Server Systems

- 5.3 By Deployment

- 5.3.1 Hyperscale / Cloud

- 5.3.2 Enterprise

- 5.3.3 Government and Research (HPC)

- 5.4 By GPU Power Density

- 5.4.1 Below 300W

- 5.4.2 300W - 700W

- 5.4.3 Above 700W

- 5.5 By Region

- 5.5.1 Europe

- 5.5.1.1 Germany

- 5.5.1.2 United Kingdom

- 5.5.1.3 France

- 5.5.1.4 Italy

- 5.5.1.5 Rest of Europe

- 5.5.1 Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Submer Technologies SL

- 6.4.2 Asperitas BV

- 6.4.3 Iceotope Technologies Limited

- 6.4.4 Green Revolution Cooling Inc.

- 6.4.5 Schneider Electric SE

- 6.4.6 DCX -The Liquid Cooling Company Sp. z o.o.

- 6.4.7 LiquidStack Inc.

- 6.4.8 Dell Technologies Inc.

- 6.4.9 Hewlett Packard Enterprise Company

- 6.4.10 Lenovo Group Limited

- 6.4.11 Atos SE

- 6.4.12 Fujitsu Limited

- 6.4.13 Super Micro Computer Inc.

- 6.4.14 Rittal GmbH and Co. KG

- 6.4.15 Vertiv Group Corp.

- 6.4.16 Midas Green Technologies LLC

- 6.4.17 Boston Limited

- 6.4.18 Inspur Systems Inc.

- 6.4.19 ASUS Tek Computer Inc.

- 6.4.20 Trane Technologies plc

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

中國GPU液冷市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區GPU浸沒式散熱市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

中國GPU液冷市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區GPU浸沒式散熱市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年) 2026年全球戶外微型資料中心機櫃市場報告

2026年全球戶外微型資料中心機櫃市場報告 液冷式伺服器市場報告:趨勢、預測與競爭分析(至2035年)

液冷式伺服器市場報告:趨勢、預測與競爭分析(至2035年) 貨櫃型資料中心市場:依解決方案組件、貨櫃類型、冷卻技術、機架數量、企業規模和最終用戶分類-2026-2032年全球市場預測2026年全球人工智慧資料中心市場報告2026年全球貨櫃型資料中心市場報告

貨櫃型資料中心市場:依解決方案組件、貨櫃類型、冷卻技術、機架數量、企業規模和最終用戶分類-2026-2032年全球市場預測2026年全球人工智慧資料中心市場報告2026年全球貨櫃型資料中心市場報告 貨櫃型資料中心市場分析及預測(至2035年):依類型、產品類型、服務、技術、元件、應用、形式、部署形式、最終使用者及模組分類

貨櫃型資料中心市場分析及預測(至2035年):依類型、產品類型、服務、技術、元件、應用、形式、部署形式、最終使用者及模組分類 貨櫃型資料中心市場規模、佔有率、趨勢和預測:按容器類型、組織規模、應用、最終用戶產業和地區分類,2026-2034 年貨櫃型資料中心:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年)

貨櫃型資料中心市場規模、佔有率、趨勢和預測:按容器類型、組織規模、應用、最終用戶產業和地區分類,2026-2034 年貨櫃型資料中心:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年)