|

市場調查報告書

商品編碼

2063862

中國GPU液冷市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)China GPU Immersion Cooling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

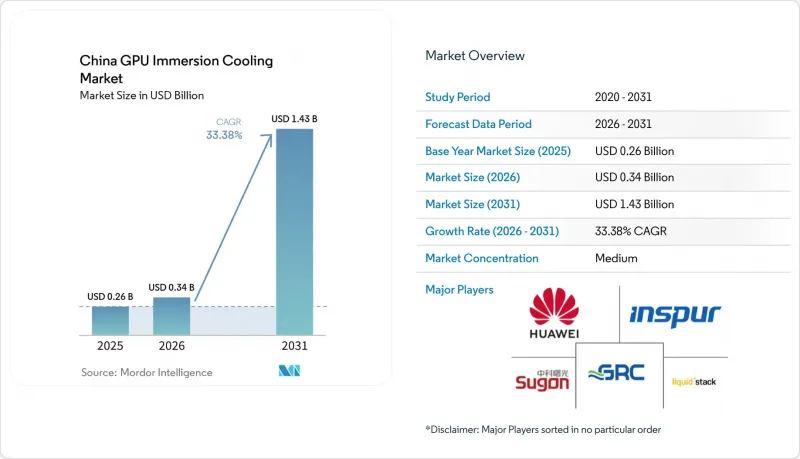

根據 Mordor Intelligence 預測,中國 GPU 浸沒式散熱市場規模預計在 2026 年達到 3.4 億美元,到 2031 年將達到 14.3 億美元,2026 年至 2031 年的複合年成長率為 33.38%。

本報告按浸沒方式(單相和兩相)、解決方案類型(槽式/系統、介電液和浸沒式最佳化GPU伺服器系統)、部署方式(超大規模/雲端、企業級以及面向政府和研究機構的高效能運算)、GPU功率密度(低於300W、300W-700W和高於700W)以及地區進行細分。市場預測以美元(USD)計價。

中國GPU液冷市場趨勢與洞察

中國資料中心人工智慧模型訓練工作負載激增

預計2024年至2025年間,中國部署的AI級GPU數量將增加三倍,工信部預測,到2026年,國內產量將達到30萬顆。模型訓練叢集,例如DeepSeek計畫在內蒙古建設的擁有5萬顆GPU的設施,其單晶片持續功耗高達350瓦至700瓦,如此高的熱密度僅靠風冷散熱難以運作。曙光科技在鄭州建設的6萬顆GPU的設施表明,浸沒式冷卻架構可以透過省去熱通道封閉系統和輔助冷卻設備,減少40%的占地面積。雖然邊緣推理節點數量不斷增加,但持續功耗最高的訓練任務正在主導浸沒式冷卻技術的應用。國家演算法註冊法規要求敏感資料必須在本地進行計算,這增加了對GPU的需求,並進一步收緊了散熱設計要求。

政府碳中和義務旨在降低資料中心的PUE(電源使用效率)。

國家發展與改革委員會於2025年2月發布的指令規定,新建資料中心的PUE值必須低於1.3,現有資料中心必須在2027年前維修至1.5。北京市對此政策進行補充,對PUE值超過1.35的設施加收每千瓦時0.10元人民幣(約合0.013美元)的費用,對於10兆瓦的設施,罰款可達數百萬元。阿里巴巴杭州園區採用單相浸沒式冷卻系統,PUE值達到1.09,與風冷系統的1.25相比,輔助功率降低了30%至35%。工信部「綠色資料中心」認證優先考慮PUE值低於1.2的項目併網,而像海靈格這樣的縣市除了電力公司提供的折扣外,還提供1%的補貼,這使得浸沒式冷卻系統具有顯著的投資回報率。

國內優質絕緣液供應鏈短缺

隨著3M公司於2025年8月停止供應Novec,氟化烴的主要來源之一就此消失,迫使營運商對國內替代品進行認證,例如統一石化生產的IMF F6210。單相流體的價格已從2024年的每噸64萬元人民幣(8.9萬美元)暴跌至2026年初的每噸20萬元人民幣(2.79萬美元),但供應集中在三家生產商手中,增加了採購風險。由於國內製造商缺乏中沸點化學品,兩相流體仍然稀缺且昂貴。殼牌和中石化於2026年1月成立的合資企業計劃到2027年實現年產5000噸的產能,但由於超大規模資料中心業者企業提前購買了相當於18至24個月的庫存,其營運資金正在迅速膨脹。

細分市場分析

到2025年,單相設計將佔中國GPU浸沒式冷卻市場78.22%的比重。這是因為礦物油基冷卻液的成本在每噸3.5萬至10.5萬元人民幣(約4860至14583美元)之間,遠低於雙相氟化化合物冷卻液。阿里巴巴杭州和張北園區採用單相儲槽實現了1.05的PUE值,顯示複雜的相變迴路並非實現效率目標的必要條件。另一方面,雙相系統提取潛熱並將其用於建築供暖,使得鄭州超級計算節點在冬季整體能耗降低了18%。

未來,在北方省份,由於環境溫度較低,被動散熱成為可能,兩相系統的部署量預計將以33.67%的複合年成長率成長。然而,能否實現價格競爭力取決於2028年後國內含氟冷媒產量的擴大。目前,由於單相系統易於維護且第三方服務網路成熟,企業更傾向於選擇單相系統。另一方面,政府高效能運算採購負責人越來越重視能源回收積分,這正逐步推動市場結構轉向兩相系統。

預計到2025年,針對浸沒式散熱最佳化的GPU伺服器系統將佔據中國GPU浸沒式散熱市場55.34%的佔有率,穩居市場佔有率榜首,並將繼續成為主要的成長引擎。曙光科技的I980-G80機架式散熱器將部署時間從六週縮短至十天,並免去了現場改造的需要。浪潮的NF5498散熱器採用耐液體塗層,將散熱檢驗的責任轉移給OEM廠商,讓注重安全性的CIO們更加安心。

絕緣液的成本可在5-7年內攤銷,進而降低整體成本。而伺服器則每3年更換一次。獨立水箱製造商正面臨國內新興廠商的價格壓力,這些廠商提供的歐美設備價格通常比獨立水箱低30-40%。供應商目前正將多年期的液體服務合約捆綁銷售,將資本支出(Capex)轉化為營運支出(OpEx),使預算與雲端經營模式保持一致。這正在推動中國GPU浸沒式冷卻產業的廣泛應用。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 中國資料中心人工智慧模型訓練工作負載激增

- 政府碳中和義務旨在降低資料中心的PUE(電源使用效率)。

- 國內GPU製造產能擴張正加速。

- 主要城市電費上漲正在推動熱效率的提升。

- 氣候較涼爽的北部各州可提供津貼的工業園區

- OEM廠商發表身臨其境型700W+ GPU參考設計。

- 市場限制因素

- 國內高品質介電解決方案供應鏈的限制因素

- 消防安全法規和建築規範延緩了浸入式設備的引進。

- 在資本投資方面具有競爭力的水性保溫材料替代方案

- GPU廠商對身臨其境型應用中保固風險的認知

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 浸沒法

- 單相浸沒式冷卻

- 兩相浸沒式冷卻

- 按解決方案類型

- 浸入式冷卻罐/系統

- 介電液

- 針對液冷散熱最佳化的GPU伺服器系統

- 不同的發展

- 超大規模/雲

- 公司

- 政府和研究機構(高效能運算)

- 按GPU功率密度

- 小於300瓦

- 300W~700W

- 超過700瓦

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Sugon Information Industry Co., Ltd.

- Huawei Technologies Co., Ltd.

- Inspur Electronic Information Industry Co., Ltd.

- Lenovo Group Limited

- Tencent Holdings Limited

- Alibaba Group Holding Limited

- Baidu, Inc.

- China Mobile Communications Corporation

- GRC(Green Revolution Cooling, Inc.)

- LiquidStack Holdings Inc.

- Submer Technologies SL

- CoolIT Systems Inc.

- Iceotope Technologies Limited

- Shenzhen Immersion Cooling Technology Co., Ltd.

- Zhejiang Tiangong Cooling Technology Co., Ltd.

- Qingdao Haier Intelligent Cooling Technology Co., Ltd.

- Chemours Chemical(Shanghai)Co., Ltd.

- Shell plc

- Sinopec Lubricants Company

第7章 市場機會與未來展望

According to Mordor Intelligence, the china gPU immersion cooling market size is expected to be USD 0.34 billion in 2026 and reach USD 1.43 billion by 2031, growing at a CAGR of 33.38% from 2026 to 2031.

This report is Segmented by Immersion Type (Single-Phase, and Two-Phase), Solution Type (Tanks/Systems, Dielectric Fluids, and Immersion-Optimized GPU Server Systems), Deployment (Hyperscale/Cloud, Enterprise, and Government and Research HPC), GPU Power Density (Below 300W, 300W-700W, and Above 700W), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

China GPU Immersion Cooling Market Trends and Insights

Surging AI Model Training Workloads in Chinese Data Centers

China's installed base of AI-oriented GPUs tripled between 2024 and 2025, and MIIT projects domestic output to hit 300,000 units in 2026. Model-training clusters such as DeepSeek's planned 50,000-GPU facility in Inner Mongolia run at sustained loads of 350 W-700 W per chip, driving thermal densities beyond the economic reach of air cooling. Sugon's 60,000-GPU installation in Zhengzhou demonstrates that immersion architectures reclaim 40% floor area by removing hot-aisle containment and supplemental chillers. Although inference nodes proliferate at the edge, training jobs dominate immersion adoption because they draw the highest continuous power. National algorithm-registration rules that compel on-premises compute for sensitive data amplify GPU demand, further tightening the thermal envelope.

Government Carbon-Neutrality Mandates for Data Center PUE Reduction

The National Development and Reform Commission's February 2025 directive obliges new data centers to achieve PUE below 1.3, while existing sites must retrofit to 1.5 by 2027. Beijing augments the policy with a CNY 0.10 (USD 0.013) kWh surcharge on sites above PUE 1.35, imposing multi-million-yuan penalties on a 10 MW facility. Alibaba's Hangzhou campus records a 1.09 PUE with single-phase immersion versus 1.25 under air flow, thanks to 30%-35% auxiliary-power savings. MIIT's Green Data Center badge fast-tracks grid connections for projects under PUE 1.2, and counties such as Helinge'er layer 1% subsidies atop utility discounts, tipping return-on-capital decisively toward immersion.

Limited Domestic Supply Chain for High-Grade Dielectric Fluids

3M's August 2025 Novec exit removed the dominant fluorocarbon source, forcing operators to qualify domestic substitutes such as Uni-President Petrochemical's IMF F6210. Prices for single-phase fluid plunged from CNY 640,000 (USD 89,000) t-1 in 2024 to CNY 200,000 (USD 27,900) t-1 by early 2026, yet supply is concentrated among three producers, raising procurement risk. Two-phase fluids remain scarcer and costlier because local producers lack mid-boiling-point chemistries. Shell and Sinopec's January 2026 joint venture targets 5,000 t annual capacity by 2027, but hyperscalers pre-buy 18-24 months of stock, inflating working capital.

Other drivers and restraints analyzed in the detailed report include:

- Emergence of Immersion-Ready 700 + W GPU Reference Designs From OEMs

- Accelerating Expansion of Domestic GPU Manufacturing Capabilities

- Fire Codes and Building Standards Lagging Immersion Installations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Single-phase designs held 78.22% of China GPU immersion cooling market size in 2025 because mineral-oil fluids cost CNY 35,000-105,000 (USD 4,860-14,583) t-1, far below two-phase fluorocarbons. Alibaba's Hangzhou and Zhangbei campuses validated 1.05 PUE with single-phase tanks, proving that complex phase-change loops are not mandatory for efficiency targets. Two-phase systems, however, extract latent heat and return it as building warming, cutting total facility energy use by 18% during winter at the Zhengzhou supercomputing node.

Looking ahead, two-phase capacity is set to rise at a 33.67% CAGR because northern provinces can exploit low ambient temperatures for passive rejection. Yet price parity hinges on domestic fluorocarbon output scaling after 2028. For now, enterprises favor single-phase because maintenance is simpler and third-party service networks are mature. Government HPC buyers weigh energy-recovery credits more heavily, nudging the segment mix slowly toward two-phase.

Immersion-optimized GPU server systems secured the biggest slice of China GPU immersion cooling market share at 55.34% in 2025 and will remain the primary growth engine. Sugon's I980-G80 rack cuts deployment from six weeks to ten days, eliminating field retrofits. Inspur's NF5498 arrives with fluid-resistant coatings, shifting thermal-validation liability to the OEM and reassuring risk-averse CIOs.

Dielectric fluids present lower invoice totals because they amortize over five-to-seven years, whereas servers refresh triennially. Stand-alone tank makers face price pressure from new domestic entrants who discount Western gear by 30%-40%. Vendors now bundle multi-year fluid-service contracts, turning capex into opex and aligning budgets with cloud business models, which supports uptake across the China GPU immersion cooling industry.

List of Companies Covered in this Report:

- Sugon Information Industry Co., Ltd.

- Huawei Technologies Co., Ltd.

- Inspur Electronic Information Industry Co., Ltd.

- Lenovo Group Limited

- Tencent Holdings Limited

- Alibaba Group Holding Limited

- Baidu, Inc.

- China Mobile Communications Corporation

- GRC (Green Revolution Cooling, Inc.)

- LiquidStack Holdings Inc.

- Submer Technologies SL

- CoolIT Systems Inc.

- Iceotope Technologies Limited

- Shenzhen Immersion Cooling Technology Co., Ltd.

- Zhejiang Tiangong Cooling Technology Co., Ltd.

- Qingdao Haier Intelligent Cooling Technology Co., Ltd.

- Chemours Chemical (Shanghai) Co., Ltd.

- Shell plc

- Sinopec Lubricants Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging AI Model Training Workloads in Chinese Data Centers

- 4.2.2 Government Carbon-Neutrality Mandates for Data Center PUE Reduction

- 4.2.3 Accelerating Expansion of Domestic GPU Manufacturing Capabilities

- 4.2.4 Rising Electricity Tariffs in Tier-1 Cities Encouraging Thermal Efficiency

- 4.2.5 Availability of Subsidized Industrial Parks in Cooler Northern Provinces

- 4.2.6 Emergence of Immersion-Ready 700+ W GPU Reference Designs from OEMs

- 4.3 Market Restraints

- 4.3.1 Limited Domestic Supply Chain for High-Grade Dielectric Fluids

- 4.3.2 Fire Codes and Building Standards Lagging Immersion Installations

- 4.3.3 Water-Based Adiabatic Alternatives Competing on Capex

- 4.3.4 Perceived Warranty Risk by GPU Vendors for Immersion Use

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE and GROWTH FORECASTS

- 5.1 By Immersion Type

- 5.1.1 Single-Phase Immersion Cooling

- 5.1.2 Two-Phase Immersion Cooling

- 5.2 By Solution Type

- 5.2.1 Immersion Cooling Tanks / Systems

- 5.2.2 Dielectric Fluids

- 5.2.3 Immersion-Optimized GPU Server Systems

- 5.3 By Deployment

- 5.3.1 Hyperscale / Cloud

- 5.3.2 Enterprise

- 5.3.3 Government and Research (HPC)

- 5.4 By GPU Power Density

- 5.4.1 Below 300W

- 5.4.2 300W - 700W

- 5.4.3 Above 700W

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Sugon Information Industry Co., Ltd.

- 6.4.2 Huawei Technologies Co., Ltd.

- 6.4.3 Inspur Electronic Information Industry Co., Ltd.

- 6.4.4 Lenovo Group Limited

- 6.4.5 Tencent Holdings Limited

- 6.4.6 Alibaba Group Holding Limited

- 6.4.7 Baidu, Inc.

- 6.4.8 China Mobile Communications Corporation

- 6.4.9 GRC (Green Revolution Cooling, Inc.)

- 6.4.10 LiquidStack Holdings Inc.

- 6.4.11 Submer Technologies SL

- 6.4.12 CoolIT Systems Inc.

- 6.4.13 Iceotope Technologies Limited

- 6.4.14 Shenzhen Immersion Cooling Technology Co., Ltd.

- 6.4.15 Zhejiang Tiangong Cooling Technology Co., Ltd.

- 6.4.16 Qingdao Haier Intelligent Cooling Technology Co., Ltd.

- 6.4.17 Chemours Chemical (Shanghai) Co., Ltd.

- 6.4.18 Shell plc

- 6.4.19 Sinopec Lubricants Company

7 MARKET OPPORTUNITIES and FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

亞太地區GPU浸沒式散熱市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲GPU浸沒式散熱:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

亞太地區GPU浸沒式散熱市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲GPU浸沒式散熱:市佔率分析、產業趨勢與統計及成長預測(2026-2031年) 2026年全球戶外微型資料中心機櫃市場報告

2026年全球戶外微型資料中心機櫃市場報告 液冷式伺服器市場報告:趨勢、預測與競爭分析(至2035年)

液冷式伺服器市場報告:趨勢、預測與競爭分析(至2035年) 貨櫃型資料中心市場:依解決方案組件、貨櫃類型、冷卻技術、機架數量、企業規模和最終用戶分類-2026-2032年全球市場預測2026年全球人工智慧資料中心市場報告2026年全球貨櫃型資料中心市場報告

貨櫃型資料中心市場:依解決方案組件、貨櫃類型、冷卻技術、機架數量、企業規模和最終用戶分類-2026-2032年全球市場預測2026年全球人工智慧資料中心市場報告2026年全球貨櫃型資料中心市場報告 貨櫃型資料中心市場分析及預測(至2035年):依類型、產品類型、服務、技術、元件、應用、形式、部署形式、最終使用者及模組分類

貨櫃型資料中心市場分析及預測(至2035年):依類型、產品類型、服務、技術、元件、應用、形式、部署形式、最終使用者及模組分類 貨櫃型資料中心市場規模、佔有率、趨勢和預測:按容器類型、組織規模、應用、最終用戶產業和地區分類,2026-2034 年貨櫃型資料中心:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年)

貨櫃型資料中心市場規模、佔有率、趨勢和預測:按容器類型、組織規模、應用、最終用戶產業和地區分類,2026-2034 年貨櫃型資料中心:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年)