|

市場調查報告書

商品編碼

2063861

亞太地區GPU浸沒式散熱市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)Asia Pacific GPU Immersion Cooling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

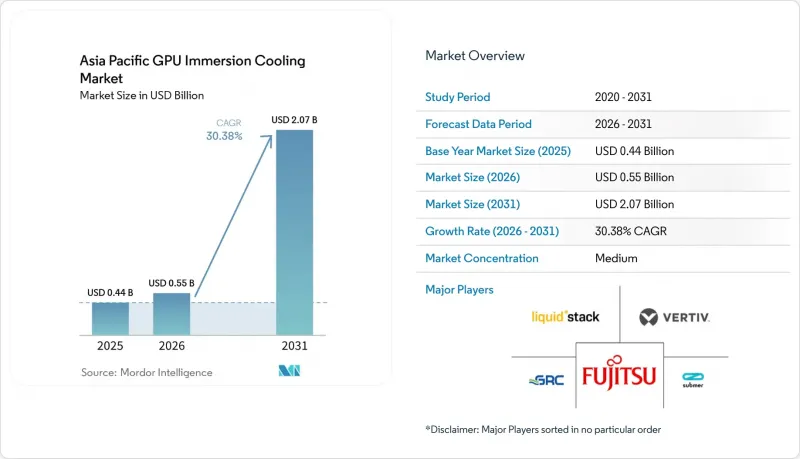

根據 Mordor Intelligence 預測,亞太地區 GPU 浸沒式冷卻市場規模預計將從 2025 年的 4.4 億美元成長到 2026 年的 5.5 億美元,然後在 2031 年達到 20.7 億美元,2026 年至 2031 年的複合年成長率為 30.38%。

本報告按浸沒式冷卻類型(單相浸沒式冷卻和兩相浸沒式冷卻)、冷卻液類型(浸沒式冷卻槽/系統、介電液等)、部署方式(超大規模雲、企業級、政府/科研高效能運算)、GPU功率密度(300W以下、300W-700W及其他)及地區進行細分。市場預測以美元計價。

亞太地區GPU浸沒式散熱市場趨勢與洞察。

超大規模資料中心中用於人工智慧和高效能運算的GPU部署激增

超大規模資料中心業者正在部署史上最大的加速器,將每個機架的功耗推高至 100kW 以上,並迫使業界迅速轉向浸沒式冷卻解決方案。位元組跳動計畫到 2025 年投資 140 億美元用於 GPU 採購,阿里雲也已撥款 1000 億美元用於 AI 基礎設施建設,兩家公司都在圍繞功耗約為 700W 的設備構建資料中心。 Naver 部署了 4000 台 NVIDIA B200 處理器,SK Telecom 也部署了 1000 台,這些都表明,使用液冷技術捕獲晶片熱量對於以額定性能持續運作至關重要。在日本耗資 120 億美元的 GMI 雲端園區,Blackwell 架構的叢集必須部署浸沒式冷卻槽。 NVIDIA 的藍圖顯示,TDP 超過 1000W 的設備預計將在兩個產品週期內推出,因此浸沒式冷卻不再是一種小眾的效率提升措施,而是實現具有競爭力的 AI 訓練吞吐量的必要溫度控管手段。

嚴格的能源效率法規和PUE目標

世界各國政府正利用PUE上限作為強而有力的工具來控制資料中心的電力需求。在日本,現有資料中心必須在2030年前達到1.4的PUE值,而新建設資料中心則必須從2029年起達到1.3,且政府也為浸沒式冷卻工程提供高達1,146億日圓(約10億美元)的補貼。新加坡將新建資料中心的PUE值限制在1.3或以下,並正在製定2026年實施專用液冷的相關法規。北京、上海和廣東省已經實施了1.2至1.3的閾值。成熟的液冷資料中心能夠穩定實現約1.02的PUE值,無需使用CRAH風扇和風管,同時也能降低高達90%的冷卻能耗。這些政策趨勢表明,在2020年代末之前,空氣冷卻將不再符合主要大都市地區的監管標準。

空氣冷卻系統初始投資成本高

從整體擁有成本 (TCO) 的角度來看,浸沒式冷卻對於每機架功率超過 50kW 的系統更具優勢,但許多公司的預算仍然專注於初始成本。由於儲槽、泵浦和進口冷卻液的採購成本高昂,印度業者在運作初期需支付 10% 至 20% 的額外成本。僅冷卻液一項,根據配方和儲罐容量的不同,每個機架的成本可能會增加 6,000 至 60,000 美元。在新加坡,殼牌和吉寶的案例表明,浸沒式冷卻可降低 40% 的生命週期成本,但投資回收期長達 18 個月的公司對這種轉變持謹慎態度。對進口零件的依賴,尤其是在南亞地區,關稅和物流成本進一步拉大了成本差距。

細分市場分析

截至2025年,單相設計在亞太地區的GPU浸沒式冷卻市場佔了79.45%的佔有率。營運商可以使用礦物油或合成酯類冷卻液,將標準伺服器浸入液體中而無需密封蓋,從而簡化了維護和維修項目,因此仍然很受歡迎。 Asperitas公司在資金籌措,並開始在泰國的熱帶氣候下部署這些系統。然而,隨著功耗超過700瓦的新一代GPU的出現,僅靠對流循環的冷卻能力正在下降。雙相解決方案透過汽化低沸點流體來實現更高的熱通量,隨著超大規模資料中心業者資料中心追求超過150千瓦的機架密度,雙相解決方案正日益受到青睞。 Sabey資料中心已完全摒棄了冷凍水,在其所有產品組合中部署了OptiCool冷媒循環系統。

未來,NVIDIA 的 Blackwell 系列預計將把單顆裝置的 TDP 推高至近 1000W,屆時雙相冷卻很可能成為雲端平台建置商的主流選擇。 SLiquid 的 C8000 機櫃已經擁有 200W/cm² 的散熱性能,並能處理 220kW 的負載。即便如此,單相冷卻也不會被淘汰。對於部署功耗低於 700W 的加速器的企業來說,他們仍然更傾向於其較低的複雜性;而在邊緣節點上,工程師可以直接接觸浸沒式基板,這一點也備受重視。因此,亞太地區的 GPU 浸沒式冷卻市場呈現兩極化的模式。對流循環在中功率部署中佔據主導地位,而相變水箱則在超高密度 AI 訓練集群中發揮核心作用。

水箱及相關系統是所有液冷系統的起點,預計到2025年,它們將佔據亞太地區GPU浸沒式冷卻市場55.34%的佔有率。例如,Green Revolution Cooling的CarnotJet單元目前正透過與三星物產的合作,銷往亞太地區的多個園區。同時,OEM廠商也紛紛推出專為浸沒式冷卻設計的電路板。富士通、超微和尼得科共同開發了一種無風扇底盤,無需散熱片和風扇,從而降低了高達15%的組件成本。 Wiwynn則投資建造了一條LiquidStack生產線,旨在從設計階段就融入浸沒式冷卻功能。

此類整合解決方案消除了與液體相容性相關的保固糾紛,並透過增加每個節點的GPU數量來提高每個機架的效能。因此,預計採用浸沒式冷卻最佳化的伺服器市場規模將以30.85%的複合年成長率超過罐式冷卻系統。罐式冷卻系統仍將作為一種供應方式,而價值創造將向上游轉移,轉向預先檢驗的運算模組,從而顯著降低超大規模和企業級買家的整合風險。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 超大規模資料中心中用於人工智慧和高效能運算的GPU部署快速成長

- 嚴格的能源效率法規和PUE目標

- 亞洲主要城市缺水問題正在推動液冷技術的應用。

- 加快部署邊緣沉浸式微型資料中心,以適應 5G 網路日益成長的密度。

- 政府資助的國家超級運算和主權人工智慧叢集

- 針對浸沒式水槽和介電解決方案的區域性製造業激勵措施

- 市場限制因素

- 初始投資成本高,且與空氣冷卻相比

- 業界標準和硬體認證有限

- 關於含氟液體的長期環境法規缺乏明確性

- 缺乏身臨其境型系統維護的專業技能

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模及成長預測(以金額為準,2025 年基準年)

- 浸入式

- 單相浸沒式冷卻

- 兩相浸沒式冷卻

- 按解決方案類型

- 浸入式冷卻罐/系統

- 介電液

- 針對液冷散熱最佳化的GPU伺服器系統

- 不同的發展

- 超大規模/雲

- 公司

- 政府和研究機構(高效能運算)

- 按GPU功率密度

- 小於300瓦

- 300W~700W

- 超過700瓦

- 按地區

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 東南亞

- 其他亞太國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Submer Technologies, SL

- LiquidStack Inc.

- Green Revolution Cooling Inc.

- Giga-Byte Technology Co., Ltd.

- Fujitsu Limited

- Wiwynn Corporation

- Iceotope Technologies Limited

- Engineered Fluids Inc.

- Vertiv Group Corp.

- CoolIT Systems Inc.

- Boyd Corporation

- nVent Electric plc

- SK Enmove Co., Ltd.

- HD Hyundai Oilbank Co., Ltd.

- Shell plc

- Huawei Technologies Co., Ltd.

- ExaScaler Inc.

- Chemours Company

- Alibaba Cloud Computing Co., Ltd.

- Super Micro Computer, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the asia pacific gPU immersion cooling market size is expected to grow from USD 0.44 billion in 2025 to USD 0.55 billion in 2026 and is forecast to reach USD 2.07 billion by 2031 at a 30.38% CAGR over 2026-2031.

This report is Segmented by Immersion Type (Single-Phase Immersion Cooling, and Two-Phase Immersion Cooling), Solution Type (Immersion Cooling Tanks/Systems, Dielectric Fluids, and More), Deployment (Hyperscale and Cloud, Enterprise, and Government and Research HPC), GPU Power Density (Below 300W, 300W-700W, and More), and Region. The Market Forecasts are Provided in Terms of Value (USD).

Asia Pacific GPU Immersion Cooling Market Trends and Insights

Surge in AI and HPC GPU Deployments Across Hyperscale Data Centers

Hyperscalers are acquiring record volumes of accelerators, pushing rack power beyond 100 kW and forcing a rapid pivot to immersion solutions. ByteDance committed USD 14 billion for GPU procurement in 2025, while Alibaba Cloud earmarked USD 100 billion for AI infrastructure, both sizing their halls around 700 W-class devices. Naver's 4,000-unit NVIDIA B200 roll-out and SK Telecom's 1,000-unit deployment show that sustained operation at nameplate performance requires liquid capture of chip heat. Japan's USD 12 billion GMI Cloud campus explicitly mandates immersion tanks for Blackwell-generation clusters. Because NVIDIA roadmaps indicate devices surpassing 1,000 W TDP within two product cycles, immersion is no longer a niche efficiency play, it is the thermal pre-requisite for competitive AI training throughput.

Stringent Energy-Efficiency Regulations and PUE Targets

Governments are weaponizing PUE caps to curb data-center electricity demand. Japan requires existing sites to hit 1.4 by 2030 and new builds to meet 1.3 from 2029, backed by subsidies up to JPY 114.6 billion (USD 1.0 billion) for immersion projects. Singapore limits new facilities to PUE more than 1.3 and is drafting a dedicated liquid-cooling code for 2026. Beijing, Shanghai, and Guangdong already enforce thresholds between 1.2 and 1.3. Demonstrated immersion fields routinely deliver PUE near 1.02, eliminating CRAH fans and ductwork while slashing cooling power by up to 90%. The policy trajectory suggests air cooling will be non-compliant across tier-1 metros well before the end of the decade.

High Upfront Capital Expenditure Versus Air Cooling

Total cost of ownership favors immersion above 50 kW per rack, yet many enterprise budgets still focus on initial price tags. Indian operators pay 10-20% more at commissioning because tanks, pumps, and imported fluids inflate procurement outlays. Fluid alone can add USD 6,000-60,000 per rack, depending on formulation and tank volume. Although Shell and Keppel showed 40% life-cycle savings in Singapore, enterprises operating on 18-month payback horizons hesitate to approve the switch. Reliance on imported components further widens the gap through tariffs and logistics, particularly in South Asia.

Other drivers and restraints analyzed in the detailed report include:

- Scarcity of Water Resources in Major Asian Metros Driving Liquid Cooling Adoption

- Accelerated Adoption of Edge Immersion Micro-Data Centers for 5G Densification

- Limited Industry Standards and Hardware Certification

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Single-phase designs held 79.45% of Asia Pacific GPU immersion cooling market share in 2025. They remain popular because mineral-oil and synthetic-ester fluids let operators submerge standard servers without sealed lids, easing maintenance and retrofit projects. Asperitas attracted USD 55.5 million in Series C funding and began rolling out such systems in Thailand's tropical climate. Yet next-wave GPUs topping 700 W are eroding the headroom of convection-only loops. Two-phase solutions, which vaporize low-boiling-point fluids for superior heat flux, are scaling as hyperscalers chase rack densities above 150 kW. Sabey Data Centers is integrating OptiCool refrigerant loops portfolio-wide, bypassing chilled water entirely.

Looking ahead, NVIDIA's Blackwell parts are expected to push per-device TDP near 1,000 W, at which point two-phase will mainstream among cloud builders. SLiquid's C8000 cabinet already claims 200 W/cm2 dissipation and 220 kW loads. Nevertheless, single-phase will not disappear; enterprises with <700 W accelerators still favor its lower complexity, and edge nodes prize direct technician access to submerged boards. The Asia Pacific GPU immersion cooling market therefore bifurcates: convection loops dominate mid-power deployments, while phase-change tanks anchor ultra-dense AI training farms.

Tanks and ancillary systems represented 55.34% of Asia Pacific GPU immersion cooling market size in 2025 because they are the starting point for any liquid build. Green Revolution Cooling's CarnotJet units, for example, are now shipping under a Samsung C&T alliance across multiple APAC campuses. OEMs, however, are unveiling boards purpose-engineered for submerged use. Fujitsu, Supermicro, and Nidec co-developed fan-less chassis that shed heatsinks and blowers, cutting bill of materials by up to 15%. Wiwynn invested in LiquidStack manufacturing lines to embed immersion readiness at design time.

Such integrated offerings eliminate warranty disputes about fluid compatibility and support higher GPU counts per node, translating to better performance per rack. As a result, immersion-optimized servers are projected to outgrow tanks at a 30.85% CAGR. Tanks will persist as the delivery vehicle, but value capture migrates up-stack toward pre-validated compute modules that slash integration risk for hyperscale and enterprise buyers.

List of Companies Covered in this Report:

- Submer Technologies, S.L.

- LiquidStack Inc.

- Green Revolution Cooling Inc.

- Giga-Byte Technology Co., Ltd.

- Fujitsu Limited

- Wiwynn Corporation

- Iceotope Technologies Limited

- Engineered Fluids Inc.

- Vertiv Group Corp.

- CoolIT Systems Inc.

- Boyd Corporation

- nVent Electric plc

- SK Enmove Co., Ltd.

- HD Hyundai Oilbank Co., Ltd.

- Shell plc

- Huawei Technologies Co., Ltd.

- ExaScaler Inc.

- Chemours Company

- Alibaba Cloud Computing Co., Ltd.

- Super Micro Computer, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in AI and HPC GPU Deployments Across Hyperscale Data Centers

- 4.2.2 Stringent Energy-Efficiency Regulations and PUE Targets

- 4.2.3 Scarcity of Water Resources in Major Asian Metros Driving Liquid Cooling Adoption

- 4.2.4 Accelerated Adoption of Edge Immersion Micro-Data Centers for 5G Densification

- 4.2.5 Government-Funded National Supercomputing and Sovereign AI Clusters

- 4.2.6 Local Manufacturing Incentives for Immersion Tanks and Dielectric Fluids

- 4.3 Market Restraints

- 4.3.1 High Upfront Capital Expenditure Versus Air Cooling

- 4.3.2 Limited Industry Standards and Hardware Certification

- 4.3.3 Uncertain Long-Term Environmental Rules on Fluorinated Fluids

- 4.3.4 Skill Shortages in Immersion-Specific Maintenance

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE and GROWTH FORECASTS (VALUE, 2025 BASE YEAR)

- 5.1 By Immersion Type

- 5.1.1 Single-Phase Immersion Cooling

- 5.1.2 Two-Phase Immersion Cooling

- 5.2 By Solution Type

- 5.2.1 Immersion Cooling Tanks / Systems

- 5.2.2 Dielectric Fluids

- 5.2.3 Immersion-Optimized GPU Server Systems

- 5.3 By Deployment

- 5.3.1 Hyperscale / Cloud

- 5.3.2 Enterprise

- 5.3.3 Government and Research (HPC)

- 5.4 By GPU Power Density

- 5.4.1 Below 300W

- 5.4.2 300W - 700W

- 5.4.3 Above 700W

- 5.5 By Region

- 5.5.1 Asia Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 South Korea

- 5.5.1.4 India

- 5.5.1.5 Southeast Asia

- 5.5.1.6 Rest of Asia Pacific

- 5.5.1 Asia Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Submer Technologies, S.L.

- 6.4.2 LiquidStack Inc.

- 6.4.3 Green Revolution Cooling Inc.

- 6.4.4 Giga-Byte Technology Co., Ltd.

- 6.4.5 Fujitsu Limited

- 6.4.6 Wiwynn Corporation

- 6.4.7 Iceotope Technologies Limited

- 6.4.8 Engineered Fluids Inc.

- 6.4.9 Vertiv Group Corp.

- 6.4.10 CoolIT Systems Inc.

- 6.4.11 Boyd Corporation

- 6.4.12 nVent Electric plc

- 6.4.13 SK Enmove Co., Ltd.

- 6.4.14 HD Hyundai Oilbank Co., Ltd.

- 6.4.15 Shell plc

- 6.4.16 Huawei Technologies Co., Ltd.

- 6.4.17 ExaScaler Inc.

- 6.4.18 Chemours Company

- 6.4.19 Alibaba Cloud Computing Co., Ltd.

- 6.4.20 Super Micro Computer, Inc.

7 MARKET OPPORTUNITIES and FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

中國GPU液冷市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲GPU浸沒式散熱:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

中國GPU液冷市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲GPU浸沒式散熱:市佔率分析、產業趨勢與統計及成長預測(2026-2031年) 2026年全球戶外微型資料中心機櫃市場報告

2026年全球戶外微型資料中心機櫃市場報告 液冷式伺服器市場報告:趨勢、預測與競爭分析(至2035年)

液冷式伺服器市場報告:趨勢、預測與競爭分析(至2035年) 貨櫃型資料中心市場:依解決方案組件、貨櫃類型、冷卻技術、機架數量、企業規模和最終用戶分類-2026-2032年全球市場預測2026年全球人工智慧資料中心市場報告2026年全球貨櫃型資料中心市場報告

貨櫃型資料中心市場:依解決方案組件、貨櫃類型、冷卻技術、機架數量、企業規模和最終用戶分類-2026-2032年全球市場預測2026年全球人工智慧資料中心市場報告2026年全球貨櫃型資料中心市場報告 貨櫃型資料中心市場分析及預測(至2035年):依類型、產品類型、服務、技術、元件、應用、形式、部署形式、最終使用者及模組分類

貨櫃型資料中心市場分析及預測(至2035年):依類型、產品類型、服務、技術、元件、應用、形式、部署形式、最終使用者及模組分類 貨櫃型資料中心市場規模、佔有率、趨勢和預測:按容器類型、組織規模、應用、最終用戶產業和地區分類,2026-2034 年貨櫃型資料中心:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年)

貨櫃型資料中心市場規模、佔有率、趨勢和預測:按容器類型、組織規模、應用、最終用戶產業和地區分類,2026-2034 年貨櫃型資料中心:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年)