|

市場調查報告書

商品編碼

2063847

GDDR記憶體:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)GDDR Memory - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

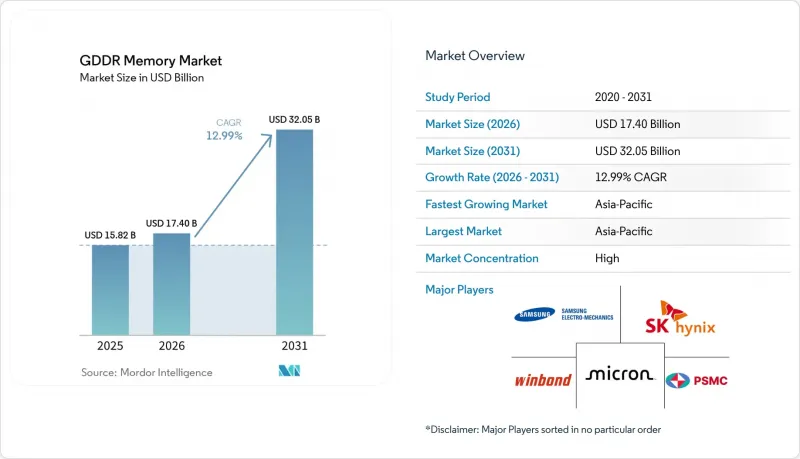

根據 Mordor Intelligence 預測,gDDR 記憶體市場預計將從 2025 年的 158.2 億美元成長到 2026 年的 174 億美元,到 2031 年達到 320.5 億美元,2026 年至 2031 年的複合年預計成長率為 12.99%。

本報告按記憶體類型(GDDR5、GDDR5X、GDDR6 和 GDDR6X)、應用領域(遊戲圖形、專業視覺化、人工智慧和計算、其他)、容量(8Gb 或以下、8-16Gb、其他)、資料速率(12Gbps 或以下終端、12-16Gbps、其他地區家用電子電器、用戶區和其他地區。市場預測以美元 (USD) 為單位。

全球 GDDR 記憶體市場趨勢及洞察

AAA 遊戲對即時射線追蹤的需求日益成長

NVIDIA 的 GeForce RTX 50 系列顯示卡於 2025 年 1 月發布,採用 30 Gbps 的 GDDR7 記憶體。這使得 RTX 5090 的總合頻寬達到 1.7 TB/s,從而實現了先前只能離線渲染的路徑追蹤光照管線。同年,DLSS 4 的應用範圍擴大到 250 多款遊戲,像素級精確反射和世界光照的頻寬需求也隨之增加。 AMD 的 Radeon RX 9000 系列顯示卡於 2025 年 2 月發布,採用 18-20 Gbps 的 GDDR6 顯存以支援主流射線追蹤工作負載,GDDR6 由此成為量產節點,而 GDDR7 則繼續保持著效能巔峰的地位。根據 Micron 的數據,在 1080p 到 4K 解析度的測試中,配備 GDDR7 顯存的影格速率比 GDDR6 提升了 30%,證實了頻寬是影響效能的關鍵因素。隨著工作室流程從光柵化轉向混合追蹤,GPU 供應商將持續記憶體吞吐量作為關鍵規格,這正在推動 GDDR 記憶體市場的發展。

需要高頻寬記憶體的人工智慧加速卡的擴展

對於邊緣推理與工作站AI工作負載,GDDR7顯存正逐漸取代昂貴的HBM顯存。 NVIDIA將於2025年3月發布的RTX PRO 6000 Blackwell顯示卡整合了96GB GDDR7顯存,讀寫速度高達1.79 TB/s,支援大規模本地語言模型推理和生成式影像合成。三星將於2024年10月發表的24GB GDDR7顯存採用PAM3訊號方案,透過時脈門控和雙VDD供電設計,實現了超過40Gbps的讀寫速度,同時耗電量降低了30%以上。美光的基準測試顯示,與32Gbps GDDR6顯存相比,GDDR7顯存的推理延遲降低了20%。這些效能和成本的趨勢正推動GDDR顯存市場從遊戲領域擴展到企業級AI硬體領域。

地緣政治緊張局勢導致供應鏈中斷

2024年12月,美國收緊了出口限制,將140家中國當地企業列入實體清單,並限制了10nm DRAM生產線所需的現場工具服務。長信儲存科技已儲備了足夠供應至2027年的備件,但其小眾微影術模組的前置作業時間仍超過60週。韓國的半導體出口預計將在2025年達到1,734億美元,其市場主導地位造成了單點故障(SPOF),而海運瓶頸加劇了這一風險。據稱,2025年12月發生的5兆韓元(約35.6億美元)智慧財產權外洩醜聞凸顯了競爭帶來的風險。目前,買家持有相當於40週庫存的貨源,這增加了營運資金,擠壓了OEM廠商的利潤空間,並阻礙了GDDR記憶體市場的成長。

細分市場分析

預計到2025年,GDDR6的市佔率將達到53.84%,反映出其在遊戲、工作站和汽車顯示卡領域的廣泛應用。其持續18-20Gbps的頻寬和成熟的良率確保了成本優勢,使GDDR6成為主流顯示卡的首選。 GDDR6X在發燒級GPU領域發展勢頭最為強勁,預計複合年成長率將達到13.79%,反映出市場對20-23Gbps通道的需求不斷成長。在尖端領域,美光和三星已開始提供性能為32-40Gbps的GDDR7樣品,預計將系統頻寬提升60%,並重新定義效能預期。中期來看,OEM廠商預計將實現工作流程多元化,將GDDR6用於注重性價比的產品,將GDDR7用於旗艦產品,從而在GDDR記憶體市場格局中保持多節點的良好需求。

向下相容的 GDDR5 和 GDDR5X 記憶體仍然在支援主機和入門級 GPU 方面發揮著至關重要的作用,為這些領域提供了具成本效益的解決方案。然而,隨著這些製程節點逐漸過時,晶圓分配量減少,淘汰進程正在進行中,預計 2028 年完成。三星開始提供 24Gbps GDDR6 樣品,顯示該公司致力於延長現有製程節點的生命週期,並在 GDDR7 產能更加普及之前維持其重要性。因此,買家將面臨一個漫長的過渡期,在此期間,GDDR5、GDDR5X 和 GDDR6 將在市場上共存。在此期間,買家需要仔細權衡物料清單 (BOM) 預算和效能需求,以做出最佳的採購決策。

到2025年,遊戲顯示卡將佔據GDDR顯存市場佔有率的59.32%,這主要得益於PC廠商和主機OEM廠商對獨立GPU出貨量的穩定需求。然而,該領域的出貨量成長已顯露出放緩跡象,供應商正將重點轉向新興的人工智慧和運算工作流程。這些工作流程目前正以13.68%的複合年成長率(CAGR)呈現最高成長。配備96GB顯存的RTX PRO 6000 Blackwell正是這項策略轉變的典型例證。它表明,GDDR7顯存正被廣泛採用,成為推理卡中HBM顯存的一種經濟高效的替代方案,尤其是在延遲和基板級簡化比實現每秒數Terabyte的聚合性能更為重要的場景下。

在專業視覺化領域,將傳統遊戲技術與先進人工智慧功能相結合的混合方案正日益受到市場的青睞。同時,在汽車叢集嵌入式圖形領域,由於該領域認證週期較長,成熟製程節點較受青睞,中速GDDR6顯存正逐漸成為主流。各行各業都在從純粹的光柵化管線轉向射線追蹤和人工智慧增強型工作負載的組合,這進一步強化了對高頻寬圖形DRAM的結構性需求,並鞏固了其在支援次世代應用程式的關鍵作用。

區域分析

預計到2025年,亞太地區將佔據GDDR記憶體市場68.42%的佔有率,並將以14.19%的複合年成長率持續成長至2031年。韓國位置全球一些最大的DRAM晶圓廠,包括三星位於平澤的工廠以及SK海力士位於利川和龍仁的工廠,這些工廠生產的GDDR晶圓佔全球總產量的65%以上。三星已將其在西安NAND快閃記憶體領域的投資年增67.5%,達到4,654億韓元(約3.088億美元),用於保障人工智慧工作負載的記憶體容量。同時,SK海力士已投資21.6兆韓元(約152億美元),將其龍仁潔淨室的運作提前至2027年2月,使其成為全球首個量產1年DRAM的叢集。中國長鑫儲存技術股份有限公司在政府資金支持下,計劃在上海進行 42 億美元的 IPO,預計到 2025 年第三季度,其全球 DRAM 市場佔有率將增至約 5%。

北美正經歷製造地策略轉型最快的時期。美光科技已為2026會計年度撥款200億美元資本累計,用於在愛達荷州和紐約州新建DRAM製造工廠,並在新加坡投資70億美元建設先進封裝工廠。這項巨額投資得到了《晶片與科學法案》(CHIPS and Science Act)的支持,該法案已向美光科技提供了61.65億美元的直接撥款,向英特爾提供了78.65億美元的直接津貼。這些津貼旨在建立一個強大的國內後端生態系統,並減少對海外生產的依賴。相較之下,歐洲的《歐盟晶片與科學法案》(EU CHIPS Act)仍處於小規模試點階段,該地區仍高度依賴進口來滿足半導體需求。

南美洲、中東和非洲目前在全球半導體市場僅佔極小佔有率。然而,預計這些地區的需求將以兩位數左右的速度成長,主要受遊戲PC和透過OEM廠商分銷的產品進口的推動。儘管如此,由於缺乏本地組裝能力和半導體政策不完善,這些地區難以發展成為重要的製造地。因此,預計在整個預測期內,這些地區將繼續依賴亞太地區生產的晶片,從而維持其在GDDR記憶體市場的現有佔有率。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- AAA 遊戲對即時射線追蹤的需求日益成長

- 需要高頻寬記憶體的人工智慧加速卡的普及。

- 4K/8K顯示器在家用電子電器。

- 資料中心中GPU部署增加,用於雲端遊戲服務

- 10nm級DRAM節點的成熟使得生產具有成本效益的GDDR6成為可能。

- 政府對國內半導體製造業的支持措施

- 市場限制因素

- 地緣政治緊張局勢導致供應鏈中斷

- 與加密貨幣挖礦週期相關的平均售價(ASP)波動性增加。

- 高密度 GDDR 封裝的熱設計限制

- 在高效能運算領域與HBM3的競爭

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按記憶體類型

- GDDR5

- GDDR5X

- GDDR6

- GDDR6X

- 透過使用

- 遊戲畫面

- 專業視覺化

- 人工智慧與運算

- 嵌入式和工業圖形

- 按密度

- 8 GB 或更少

- 8~16 Gb

- 16 GB 或更多

- 按數據速率

- 12 Gbps 或更低

- 12~16 Gbps

- 超過 16 Gbps

- 按最終用戶行業分類

- 家用電子設備(遊戲、遊戲機)

- IT 與資料中心(人工智慧、雲端運算推理)

- 媒體與娛樂(渲染、視覺特效)

- 工業和醫療保健

- 航太/國防

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞

- 其他亞太國家

- 南美洲

- 巴西

- 其他南美國家

- 中東和非洲

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Samsung Electronics Co., Ltd.

- SK hynix Inc.

- Micron Technology, Inc.

- Winbond Electronics Corporation

- Powerchip Semiconductor Manufacturing Corporation

- Yangtze Memory Technologies Co., Ltd.

- Nanya Technology Corporation

- ADATA Technology Co., Ltd.

- Kingston Technology Corporation

- SMART Modular Technologies, Inc.

- G.Skill International Enterprise Co., Ltd.

- Corsair Memory, Inc.

- PNY Technologies, Inc.

- Patriot Memory LLC

- TeamGroup Inc.

- Apacer Technology Inc.

- Galax

- ChangXin Memory Technologies

- Windbond Electronics Corporation

- Xi'an UniIC Semiconductors Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the GDDR memory market size is expected to increase from USD 15.82 billion in 2025 to USD 17.4 billion in 2026 and reach USD 32.05 billion by 2031, growing at a CAGR of 12.99% over 2026-2031.

This report is Segmented by Memory Type (GDDR5, GDDR5X, GDDR6, and GDDR6X), Application (Gaming Graphics, Professional Visualization, AI and Compute, and More), Density (≤ 8 Gb, 8-16 Gb, and More), Data Rate (≤ 12 Gbps, 12-16 Gbps, and More), End-User Industry (Consumer Electronics, IT and Data Centers, Media and Entertainment, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global GDDR Memory Market Trends and Insights

Growing Demand for Real-Time Ray Tracing in AAA Games

NVIDIA's GeForce RTX 50 series debuted in January 2025 with GDDR7 running at 30 Gbps, delivering 1.7 TB/s aggregate bandwidth on the RTX 5090 and enabling path-traced lighting pipelines previously limited to offline renders. DLSS 4 adoption expanded to more than 250 titles the same year, escalating bandwidth needs for pixel-accurate reflections and global illumination. AMD's Radeon RX 9000 family, released in February 2025, relied on 18-20 Gbps GDDR6 to service mainstream ray-traced workloads, reinforcing GDDR6 as the volume node while ceding the performance crown to GDDR7. Micron data shows 30% higher frame rates for GDDR7-equipped boards across 1080p to 4K tests relative to GDDR6, confirming bandwidth as the critical performance lever. As studio pipelines shift from rasterization to hybrid tracing, GPU vendors market sustained memory throughput as a headline spec, propelling the GDDR memory market.

Expansion of AI Accelerator Cards Requiring High-Bandwidth Memory

Edge inference and workstation AI workloads increasingly opt for GDDR7 over costly HBM stacks. NVIDIA's RTX PRO 6000 Blackwell, launched in March 2025, integrates 96 GB of GDDR7 memory, delivering 1.79 TB/s and supporting local large-language-model inference and generative image synthesis. Samsung's 24 Gb GDDR7, introduced in October 2024, uses PAM3 signaling to exceed 40 Gbps while cutting power draw by more than 30% through clock-gating and dual-VDD rails. Micron benchmarks suggest 20% lower inference latency than GDDR6 at 32 Gbps. These performance and cost dynamics widen the GDDR memory market beyond gaming into enterprise AI hardware.

Supply Chain Disruptions Due to Geopolitical Tensions

U.S. export rules tightened in December 2024, adding 140 mainland Chinese entities to the Entity List and restricting on-site tool service critical for 10 nm DRAM lines. ChangXin Memory Technologies stockpiled spares to buffer until 2027, but lead times for niche lithography modules still exceed 60 weeks. South Korea's dominance, with USD 173.4 billion in semiconductor exports in 2025, creates single points of failure, amplified by maritime choke points. Alleged intellectual-property leaks worth KRW 5 trillion (USD 3.56 billion) in December 2025 underscore rivalry risks. Buyers now carry 40-week inventories, inflating working capital and pressuring OEM margins, a drag on the GDDR memory market growth vector.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Adoption of 4K/8K Displays in Consumer Electronics

- Rising Data Center GPU Deployments for Cloud Gaming Services

- Rising ASP Volatility Linked to Cryptocurrency Mining Cycles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

GDDR6's market share reached 53.84% in 2025, reflecting broad design wins across gaming, workstation, and automotive boards. Sustained 18-20 Gbps speed bins and mature yield profiles enable cost advantages that keep GDDR6 the default choice for mainstream cards. Momentum for GDDR6X is strongest in enthusiast GPUs, where its 13.79% forecast CAGR mirrors rising appetite for 20-23 Gbps lanes. At the cutting edge, Micron and Samsung now sample GDDR7 with 32-40 Gbps capability, promising 60% higher system bandwidth and resetting performance expectations. Over the medium term, OEMs are expected to split workflows: cost-sensitive SKUs on GDDR6, flagship parts on GDDR7, and sustain healthy multi-node demand within the GDDR memory market share landscape.

Backward-compatible GDDR5 and GDDR5X continue to play a significant role in supporting consoles and value GPUs, providing a cost-effective solution for these segments. However, the increasing obsolescence of these nodes and the reduction in wafer allocations indicate their gradual phase-out, which is expected to be completed by 2028. Samsung's strategy of sampling 24 Gbps GDDR6 highlights the company's focus on extending the lifecycle of the current node, ensuring its relevance until GDDR7 production capacity becomes more widely available. As a result, buyers will face an extended transition period where GDDR5, GDDR5X, and GDDR6 coexist in the market. During this time, they will need to carefully balance their bill-of-materials (BOM) budgets with their performance requirements to make optimal purchasing decisions.

Gaming graphics captured 59.32% of the GDDR memory market share in 2025, driven primarily by the consistent demand for discrete GPU shipments to PC builders and console OEMs. However, unit growth in this segment is showing signs of plateauing, prompting suppliers to shift their focus to emerging AI and compute workflows. These workflows are now demonstrating the fastest growth, with a compound annual growth rate (CAGR) of 13.68%. The RTX PRO 6000 Blackwell, with a 96 GB frame buffer, is a prime example of this strategic shift. It highlights the adoption of GDDR7 as a cost-effective alternative to HBM for inference cards, particularly in scenarios where latency and board-level simplicity take precedence over achieving multi-terabyte-per-second aggregates.

In the professional visualization segment, the market is increasingly adopting a hybrid approach that blends traditional gaming technologies with advanced AI capabilities. Meanwhile, embedded graphics for automotive clusters are leaning toward mid-speed GDDR6, as the extended qualification cycles in this sector favor the use of mature nodes. Across various verticals, the ongoing transition from pure raster pipelines to a combination of ray-traced and AI-enhanced workloads is further reinforcing the structural demand for high-bandwidth graphics DRAM, ensuring its critical role in supporting next-generation applications.

Geography Analysis

Asia-Pacific accounted for 68.42% of the GDDR memory market share in 2025 and is projected to expand at a 14.19% CAGR to 2031. South Korea hosts the world's largest DRAM mega-fabs, including Samsung's Pyeongtaek and SK hynix's Icheon and Yongin campuses, which together churn out more than 65% of global GDDR wafers. Samsung increased Xi'an NAND investment by 67.5% year on year to KRW 465.4 billion (USD 308.8 million), diverting capital toward memory capacity for AI workloads. SK hynix, meanwhile, committed KRW 21.6 trillion (USD 15.2 billion) to accelerate Yongin's cleanroom start to February 2027, positioning the cluster as the first high-volume 1Y DRAM site. China's ChangXin Memory Technologies crept to roughly 5% global DRAM share by Q3 2025, buoyed by state-backed funds and a planned USD 4.2 billion Shanghai IPO.

North America represents the fastest strategic shift in fabrication localization. Micron's USD 20 billion FY 2026 CAPEX is allocated to finance new DRAM fabrication facilities in Idaho and New York, as well as a USD 7 billion advanced-packaging hub in Singapore. This significant investment is supported by the CHIPS and Science Act, which awarded Micron USD 6.165 billion and Intel USD 7.865 billion in direct grants. These grants aim to anchor a robust domestic back-end ecosystem, reducing reliance on overseas production. In contrast, Europe's EU Chips Act lags behind with smaller pilot lines, leaving the region heavily dependent on imports to meet its semiconductor needs.

South America and the Middle East and Africa currently account for marginal volumes in the global semiconductor market. However, these regions are experiencing low-teens demand growth, driven primarily by the import of gaming rigs and OEM-distributed products. Despite this growth, limited local assembly capacity and underdeveloped semiconductor policies hinder their ability to establish a significant manufacturing presence. As a result, these regions are expected to continue relying on Asia-Pacific-produced dies throughout the forecast period, maintaining their current share in the GDDR memory market.

- Samsung Electronics Co., Ltd.

- SK hynix Inc.

- Micron Technology, Inc.

- Winbond Electronics Corporation

- Powerchip Semiconductor Manufacturing Corporation

- Yangtze Memory Technologies Co., Ltd.

- Nanya Technology Corporation

- ADATA Technology Co., Ltd.

- Kingston Technology Corporation

- SMART Modular Technologies, Inc.

- G.Skill International Enterprise Co., Ltd.

- Corsair Memory, Inc.

- PNY Technologies, Inc.

- Patriot Memory LLC

- TeamGroup Inc.

- Apacer Technology Inc.

- Galax

- ChangXin Memory Technologies

- Windbond Electronics Corporation

- Xi'an UniIC Semiconductors Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for Real-Time Ray Tracing in AAA Games

- 4.2.2 Expansion of AI Accelerator Cards Requiring High-Bandwidth Memory

- 4.2.3 Increasing Adoption of 4K/8K Displays in Consumer Electronics

- 4.2.4 Rising Data Center GPU Deployments for Cloud Gaming Services

- 4.2.5 Maturing 10 nm-Class DRAM Node Enabling Cost-Effective GDDR6 Production

- 4.2.6 Government Incentives for Domestic Semiconductor Manufacturing

- 4.3 Market Restraints

- 4.3.1 Supply Chain Disruptions Due to Geopolitical Tensions

- 4.3.2 Rising ASP Volatility Linked to Cryptocurrency Mining Cycles

- 4.3.3 Thermal Design Constraints in High-Density GDDR Packages

- 4.3.4 Competition From HBM3 in High-Performance Computing

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Memory Type

- 5.1.1 GDDR5

- 5.1.2 GDDR5X

- 5.1.3 GDDR6

- 5.1.4 GDDR6X

- 5.2 By Application

- 5.2.1 Gaming Graphics

- 5.2.2 Professional Visualization

- 5.2.3 AI and Compute

- 5.2.4 Embedded and Industrial Graphics

- 5.3 By Density

- 5.3.1 <= 8 Gb

- 5.3.2 8-16 Gb

- 5.3.3 Above 16 Gb

- 5.4 By Data Rate

- 5.4.1 <= 12 Gbps

- 5.4.2 12-16 Gbps

- 5.4.3 Above 16 Gbps

- 5.5 By End-User Industry

- 5.5.1 Consumer Electronics (Gaming, Consoles)

- 5.5.2 IT and Data Centers (AI, Cloud Inference)

- 5.5.3 Media and Entertainment (Rendering, VFX)

- 5.5.4 Industrial and Healthcare

- 5.5.5 Aerospace and Defense

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Southeast Asia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Samsung Electronics Co., Ltd.

- 6.4.2 SK hynix Inc.

- 6.4.3 Micron Technology, Inc.

- 6.4.4 Winbond Electronics Corporation

- 6.4.5 Powerchip Semiconductor Manufacturing Corporation

- 6.4.6 Yangtze Memory Technologies Co., Ltd.

- 6.4.7 Nanya Technology Corporation

- 6.4.8 ADATA Technology Co., Ltd.

- 6.4.9 Kingston Technology Corporation

- 6.4.10 SMART Modular Technologies, Inc.

- 6.4.11 G.Skill International Enterprise Co., Ltd.

- 6.4.12 Corsair Memory, Inc.

- 6.4.13 PNY Technologies, Inc.

- 6.4.14 Patriot Memory LLC

- 6.4.15 TeamGroup Inc.

- 6.4.16 Apacer Technology Inc.

- 6.4.17 Galax

- 6.4.18 ChangXin Memory Technologies

- 6.4.19 Windbond Electronics Corporation

- 6.4.20 Xi'an UniIC Semiconductors Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

邏輯裝置用矽晶圓:市場佔有率分析、產業趨勢與統計資料以及成長預測(2026-2031 年)

邏輯裝置用矽晶圓:市場佔有率分析、產業趨勢與統計資料以及成長預測(2026-2031 年) 記憶體處理單元 (MPU) 市場預測至 2034 年—按架構類型、記憶體技術、組件、應用、最終用戶和地區分類的全球分析

記憶體處理單元 (MPU) 市場預測至 2034 年—按架構類型、記憶體技術、組件、應用、最終用戶和地區分類的全球分析 2026年全球軍工和航太應用記憶體和處理器市場報告

2026年全球軍工和航太應用記憶體和處理器市場報告 石墨烯基儲存裝置市場分析及預測(至2035年):類型、產品、技術、組件、應用、材料類型、裝置、最終用戶、功能、安裝模式2026年全球儲存層級記憶體市場報告用於儲存設備的矽晶圓:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

石墨烯基儲存裝置市場分析及預測(至2035年):類型、產品、技術、組件、應用、材料類型、裝置、最終用戶、功能、安裝模式2026年全球儲存層級記憶體市場報告用於儲存設備的矽晶圓:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 數位射頻記憶體市場:依產品類型、容量、應用和最終用戶分類-2026-2032年全球預測

數位射頻記憶體市場:依產品類型、容量、應用和最終用戶分類-2026-2032年全球預測 HBM全球市場預測(2026):AI主導的需求與HBM4生產趨勢

HBM全球市場預測(2026):AI主導的需求與HBM4生產趨勢 數位射頻記憶體市場-全球產業規模、佔有率、趨勢、機會、預測:架構、應用、平台、區域及競爭格局(2021-2031年)

數位射頻記憶體市場-全球產業規模、佔有率、趨勢、機會、預測:架構、應用、平台、區域及競爭格局(2021-2031年) 全球數位射頻識別市場(2026-2030 年)

全球數位射頻識別市場(2026-2030 年)