|

市場調查報告書

商品編碼

2063826

飼料添加劑諾西肽預混合料:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031)Feed Additive Nosiheptide Premix - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

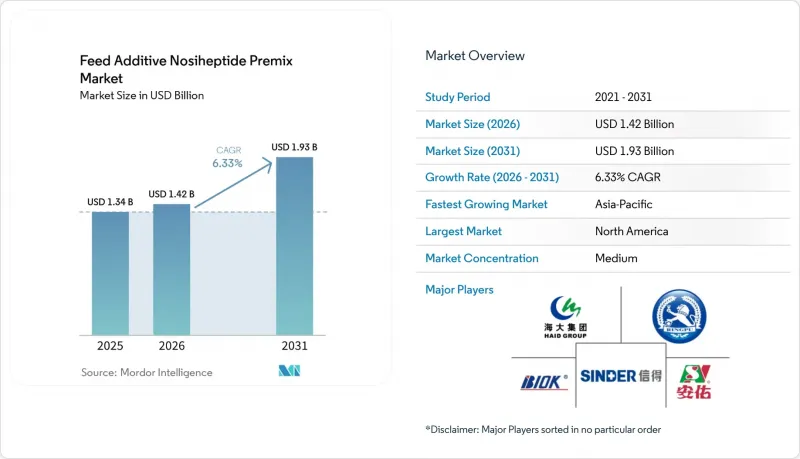

根據 Mordor Intelligence 預測,諾西肽預混合料飼料添加劑的市場規模預計將從 2025 年的 13.4 億美元成長到 2026 年的 14.2 億美元,到 2031 年將達到 19.3 億美元。

預計 2026 年至 2031 年的年複合成長率(CAGR)為 6.33%。

本報告按畜牧業(家禽、豬、反芻動物、水產養殖及其他)、配方類型(傳統預混合料和有機/非基因預混合料)、原料(合成諾西肽和生物發酵諾西肽)以及地區(北美、南美、歐洲、亞太地區以及中東和非洲)進行細分。市場預測以美元計價。

全球飼料添加劑諾西肽預混合料市場趨勢及洞察

促進抗生素替代品監管

美國嚴格的抗生素合理使用法規正在推動替代品的普及,例如飼料添加劑諾西肽預混合料。 2024年,美國食品藥物管理局(FDA)透過產業指南(GFI)263及相關合理使用舉措,加強了應對抗生素抗藥性的力度。這些措施要求將對動物具有重要醫療價值的抗生素置於獸醫監管之下,並促進其在畜牧業中的合理使用。因此,飼料生產商正在加速向非重要醫療價值的替代品(例如諾西肽)過渡,以在遵守不斷變化的抗生素抗藥性法規的同時,保持飼料轉換率和生產力。

亞太地區雞肉出口擴張

亞洲家禽出口的成長推動了對特種飼料添加劑(包括諾西肽預混合料)的需求。根據荷蘭合作銀行發布的《全球家禽季刊(2025)》,2024年第四季全球加工家禽貿易量量達約40萬噸,較去年同期成長15%。這一成長主要得益於包括泰國和中國在內的亞洲生產商的大量出口。隨著出口的擴大,生產商被迫採用符合嚴格殘留物和可追溯性標準的飼料解決方案,這促使諾西肽的使用量增加,以確保在維持生產效率的同時符合相關法規。

歐盟嚴格的殘留物檢測體系

歐盟嚴格的殘留物檢測法規增加了飼料添加劑生產商的合規成本。歐盟委員會第2024/1229號條例規定了非目標飼料中24種抗菌物質的最大可接受交叉污染限值。該法規要求使用高靈敏度的分析方法進行檢測。達到嚴格的閾值需要高解析度層析法等先進技術,這增加了檢測的複雜性和營運成本。小規模預混合料生產商,尤其是那些沒有專用生產線或認證實驗室的生產商,在滿足這些要求方面面臨巨大的挑戰。這種情況限制了它們進入市場,而有利於擁有完善品管系統的大規模垂直整合企業。

細分市場分析

至2025年,家禽業將佔飼料添加劑諾西肽預混合料市場54%的最大佔有率。這一主導地位主要得益於集約化肉雞生產系統和強勁的出口需求。較短的生產週期使得飼料配方能夠快速調整,從而促進了商業化生產中添加劑使用量的增加。出口市場需要低殘留飼料解決方案以滿足嚴格的進口標準,這進一步鞏固了家禽業的主導地位。豬業將佔據第二大市場佔有率,這主要得益於對腸道健康管理的需求;而水產養殖業由於生物安全和疾病預防措施的加強,其應用也在逐步增加。

預計2026年至2031年間,家禽市場將以7.8%的複合年成長率(CAGR)達到最高成長速度。這一成長主要得益於全球家禽消費量的成長和集約化養殖系統的擴張。消費者對無抗生素肉類生產的日益偏好,推動了非醫療用途飼料添加劑的應用,以確保生產性能和飼料轉換率。家禽養殖戶受惠於生產週期的縮短,因此能夠快速採用新的飼料技術。這種適應性,加上強勁的出口需求和監管合規性,使家禽成為市場中成長最快的細分領域。

區域分析

到2025年,北美將佔飼料添加劑諾西肽預混合料市場36%的最大佔有率。這一主導地位歸功於嚴格的法規結構和無抗生素畜牧系統的廣泛應用。美國食品藥物管理局(FDA)強制要求對具有重要醫療價值的抗菌藥物進行獸醫監管,加速了向非重要醫療替代品的轉變。此外,該地區垂直整合的家禽生產商正在利用先進的飼料管理系統並迅速推出新的配方,從而確保商業性畜牧養殖對諾西肽等專用飼料添加劑的穩定需求。

亞太地區預計將在2026年至2031年間以7.9%的複合年成長率實現最高成長,這主要得益於畜牧業生產的擴張和出口導向供應鏈的蓬勃發展。肉類消費量的成長和農業系統的集約化正在推動提高飼料生產效率的添加劑的應用。區域生產商正投資於飼料生產基礎設施和現代化生產方法,以供應國內和國際市場。中國、泰國和越南等國正在加強其在全球禽肉出口中的地位,這推動了對符合嚴格殘留物和品質標準的特殊添加劑的需求。

歐洲市場雖然成熟,但其價值導向日益增強,這得益於嚴格的法規結構和對認證畜牧系統日益成長的需求。關於抗菌劑使用和殘留限量的嚴格政策,促使生產商轉向使用非醫療必需的飼料添加劑。畜牧養殖戶正在採用先進的可追溯系統和認證飼料原料,以滿足監管機構和零售商的要求。這種轉變增加了營運複雜性和生產成本,尤其對小規模生產商而言更是如此。另一方面,對無抗生素和有機畜牧產品的強勁需求支撐了高價,使供應商能夠抵消合規成本,並在全部區域保持盈利。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 監管部門為推廣抗生素替代品所做的努力

- 亞太地區雞肉出口成長

- 「不含抗生素」標籤導致高價商品的出現。

- 擴大精準發酵生產規模

- 飼料廠引進自動預混合料稱重技術

- 增加對窄譜抗生素的創業融資

- 市場限制因素

- 歐盟嚴格的殘留物檢測體系

- 中國諾西肽原料藥供應波動

- 它在反芻動物飼料的應用還很落後。

- 桿菌肽與酪胺酸預混合料之間的競爭

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 畜牧業

- 家禽

- 豬

- 反芻動物

- 水產養殖

- 其他牲畜

- 依配方類型

- 傳統預混合料

- 有機/非基因改造預混合料

- 按原料

- 合成諾西肽

- 生物發酵諾西肽

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 其他北美國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Zhejiang Shenghua Biok Biology Co., Ltd.

- Tianjin Ringpu Bio-Pharmacy Co., Ltd.

- Anyou Biotechnology Group Co., Ltd.

- Guangdong Haid Group Co., Ltd.

- Shandong Shengli Bioengineering Co., Ltd.

- Zhejiang Esigma Animal Health Co., Ltd.

- Shandong Sinder Technology Co., Ltd.

- Hainan Zhongxin Chemical Co., Ltd.

- Anyou Biotechnology Group Co., Ltd.

- Fengchen Group Co., Ltd.

- Anhui Wanbei Pharmaceutical Co., Ltd.

- Zhejiang University Sunny Nutrition Technology Co., Ltd.

- Chattha Group

第7章 市場機會與未來展望

According to Mordor Intelligence, the feed additive nosiheptide premix market size is projected to grow from USD 1.34 billion in 2025 to USD 1.42 billion in 2026, reaching USD 1.93 billion by 2031, with a CAGR of 6.33% over 2026-2031.

This report is Segmented by Livestock (Poultry, Swine, Ruminants, Aquaculture, and Other Livestocks), by Formulation Type (Conventional Premix and Organic/Non-GMO Premix), by Source (Synthetic Nosiheptide and Bio-Fermented Nosiheptide), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Feed Additive Nosiheptide Premix Market Trends and Insights

Regulatory Push for Antibiotic Replacement

Stringent antimicrobial stewardship regulations in the United States are driving the adoption of alternatives such as nosiheptide premixes in animal feed. In 2024, the United States Food and Drug Administration (FDA) strengthened its antimicrobial resistance strategy through Guidance for Industry (GFI) 263 and related stewardship initiatives. These measures mandate that medically important antimicrobial drugs for animals remain under veterinary oversight and promote their judicious use in livestock production . As a result, feed manufacturers and producers are increasingly turning to non-medically important alternatives, such as nosiheptide, to sustain feed efficiency and productivity while complying with evolving antimicrobial resistance policies.

Growth of Poultry Meat Exports from Asia-Pacific

Increasing poultry meat exports from Asia are driving demand for specialized feed additives, including nosiheptide premixes. According to the Rabobank Global Poultry Quarterly (2025), global processed chicken trade reached approximately 400,000 metric tons in Q4 2024, marking a 15% year-on-year growth . This growth was supported by significant export contributions from Asian producers such as Thailand and China. The expansion in exports is prompting producers to adopt feed solutions that comply with strict residue and traceability standards, leading to greater use of nosiheptide to ensure compliance while maintaining productivity and efficiency.

Stringent Residue-Testing Regimes in the European Union

Stringent residue-testing regulations in the European Union are driving up compliance costs for feed additive manufacturers. Commission Regulation (EU) 2024/1229 sets maximum cross-contamination limits for 24 antimicrobial substances in non-target feed . This regulation requires the use of highly sensitive analytical methods for detection. The strict thresholds necessitate advanced technologies, such as high-resolution chromatography, which increase testing complexity and operational expenses. Smaller premix manufacturers, particularly those lacking dedicated production lines or accredited laboratories, face significant challenges in meeting these requirements. This situation limits their market participation and benefits larger, vertically integrated companies with established quality-control systems.

Other drivers and restraints analyzed in the detailed report include:

- Emergence of Antibiotic-Free Labeling Premiums

- Scale-Up of Precision-Fermentation Manufacturing

- Volatility of Nosiheptide API Supply from China

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Poultry accounted for the largest 54% share of the feed additive nosiheptide premix market in 2025. This dominance was driven by intensive broiler production systems and strong export-oriented demand. Short production cycles enable quicker adjustments to feed formulations, leading to greater additive utilization in commercial operations. Export markets demand low-residue feed solutions to comply with stringent import standards, further solidifying poultry's leading position. Swine represents a secondary segment, supported by gut health management needs, while aquaculture adoption is gradually increasing due to stricter biosecurity and disease-prevention measures.

The poultry segment market size is projected to grow at the fastest CAGR of 7.8% from 2026 to 2031. This growth is attributed to increasing global poultry consumption and the expansion of intensive farming systems. The growing preference for antibiotic-free meat production is driving the adoption of non-medically important feed additives that ensure performance and feed efficiency. Poultry producers benefit from shorter production cycles, enabling faster integration of new feed technologies. This adaptability, combined with strong export demand and regulatory compliance, positions poultry as the fastest-growing segment in the market.

Geography Analysis

North America is accounted for the largest 36% of the feed additive nosiheptide premix market share in 2025. This dominance is attributed to strict regulatory frameworks and the widespread adoption of antibiotic-free livestock production systems. The United States Food and Drug Administration mandates veterinary oversight for medically important antimicrobials, driving the transition toward non-medically important alternatives. Additionally, vertically integrated poultry producers in the region leverage advanced feed management systems and quickly adopt new formulations, thereby ensuring steady demand for specialized feed additives such as nosiheptide in commercial livestock production.

The Asia-Pacific region is projected to register the fastest CAGR of 7.9% from 2026 to 2031, driven by the growth of livestock production and export-oriented supply chains. Rising meat consumption and the intensification of farming systems are promoting the adoption of performance-enhancing feed additives. Regional producers are investing in feed manufacturing infrastructure and modern production practices to serve both domestic and international markets. Countries like China, Thailand, and Vietnam are enhancing their roles in global poultry exports, which is driving the demand for specialized additives that comply with stringent residue and quality standards.

Europe represents a mature but value-driven market, supported by stringent regulatory frameworks and increasing demand for certified livestock production systems. Strict policies on antimicrobial usage and residue compliance are encouraging producers to shift toward non-medically important feed additives. Livestock producers are adopting advanced traceability systems and certified feed inputs to meet regulatory and retailer requirements. This transition increases operational complexity and production costs, particularly for smaller manufacturers. At the same time, strong demand for antibiotic-free and organic animal products supports premium pricing, enabling suppliers to offset compliance costs while maintaining profitability across the region.

- Zhejiang Shenghua Biok Biology Co., Ltd.

- Tianjin Ringpu Bio-Pharmacy Co., Ltd.

- Anyou Biotechnology Group Co., Ltd.

- Guangdong Haid Group Co., Ltd.

- Shandong Shengli Bioengineering Co., Ltd.

- Zhejiang Esigma Animal Health Co., Ltd.

- Shandong Sinder Technology Co., Ltd.

- Hainan Zhongxin Chemical Co., Ltd.

- Anyou Biotechnology Group Co., Ltd.

- Fengchen Group Co., Ltd.

- Anhui Wanbei Pharmaceutical Co., Ltd.

- Zhejiang University Sunny Nutrition Technology Co., Ltd.

- Chattha Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory push for antibiotic replacement

- 4.2.2 Growth of poultry meat exports from Asia-Pacific

- 4.2.3 Emergence of antibiotic-free labeling premiums

- 4.2.4 Scale-up of precision-fermentation manufacturing

- 4.2.5 Integration of premix dosing automation at feed mills

- 4.2.6 Rising venture funding for narrow-spectrum antimicrobials

- 4.3 Market Restraints

- 4.3.1 Stringent residue-testing regimes in the European Union

- 4.3.2 Volatility of nosiheptide API supply from China

- 4.3.3 Slower adoption in ruminant rations

- 4.3.4 Price competition from bacitracin and tylosin premixes

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Livestock

- 5.1.1 Poultry

- 5.1.2 Swine

- 5.1.3 Ruminants

- 5.1.4 Aquaculture

- 5.1.5 Other Livestock

- 5.2 By Formulation Type

- 5.2.1 Conventional Premix

- 5.2.2 Organic/Non-GMO Premix

- 5.3 By Source

- 5.3.1 Synthetic Nosiheptide

- 5.3.2 Bio-fermented Nosiheptide

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 France

- 5.4.3.3 United Kingdom

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 India

- 5.4.4.3 Japan

- 5.4.4.4 South Korea

- 5.4.4.5 Australia

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Egypt

- 5.4.6.3 Rest of Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global-Level Overview, Market-Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Zhejiang Shenghua Biok Biology Co., Ltd.

- 6.4.2 Tianjin Ringpu Bio-Pharmacy Co., Ltd.

- 6.4.3 Anyou Biotechnology Group Co., Ltd.

- 6.4.4 Guangdong Haid Group Co., Ltd.

- 6.4.5 Shandong Shengli Bioengineering Co., Ltd.

- 6.4.6 Zhejiang Esigma Animal Health Co., Ltd.

- 6.4.7 Shandong Sinder Technology Co., Ltd.

- 6.4.8 Hainan Zhongxin Chemical Co., Ltd.

- 6.4.9 Anyou Biotechnology Group Co., Ltd.

- 6.4.10 Fengchen Group Co., Ltd.

- 6.4.11 Anhui Wanbei Pharmaceutical Co., Ltd.

- 6.4.12 Zhejiang University Sunny Nutrition Technology Co., Ltd.

- 6.4.13 Chattha Group

7 Market Opportunities and Future Outlook

特種飼料添加劑市場:2026-2032年全球市場預測(依產品種類、目標動物種類、成分、劑型、最終用戶及通路分類)飼料添加劑市場:按類型、劑型、畜種、成分、功能、最終用戶和分銷管道分類-2026-2032年全球市場預測

特種飼料添加劑市場:2026-2032年全球市場預測(依產品種類、目標動物種類、成分、劑型、最終用戶及通路分類)飼料添加劑市場:按類型、劑型、畜種、成分、功能、最終用戶和分銷管道分類-2026-2032年全球市場預測 全球特種飼料添加劑市場

全球特種飼料添加劑市場 印度飼料添加劑:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)飼料用甲硫胺酸添加劑:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

印度飼料添加劑:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)飼料用甲硫胺酸添加劑:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 全球飼料添加劑市場:按類型、功能、最終用戶、動物種類、來源、形態和地區分類-預測至2031年

全球飼料添加劑市場:按類型、功能、最終用戶、動物種類、來源、形態和地區分類-預測至2031年 飼料添加劑市場規模、佔有率和成長分析(按類型、畜種、成分、形態、功能和地區分類)—產業預測(2026-2033 年)

飼料添加劑市場規模、佔有率和成長分析(按類型、畜種、成分、形態、功能和地區分類)—產業預測(2026-2033 年) 特種飼料添加劑市場(按類型、動物、產地、形態、功能、製造技術和地區分類)-預測至2030年

特種飼料添加劑市場(按類型、動物、產地、形態、功能、製造技術和地區分類)-預測至2030年 飼料添加劑市場-全球產業規模、佔有率、趨勢、機會及預測(按成分類型、牲畜、形態、地區和競爭情況細分,2020-2030 年)

飼料添加劑市場-全球產業規模、佔有率、趨勢、機會及預測(按成分類型、牲畜、形態、地區和競爭情況細分,2020-2030 年) 中國飼料添加劑市場:依產品種類、牲畜、來源、形式、最終用戶、地區、機會、預測,2017-2031年

中國飼料添加劑市場:依產品種類、牲畜、來源、形式、最終用戶、地區、機會、預測,2017-2031年