|

市場調查報告書

商品編碼

2061524

印度飼料添加劑:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)India Feed Additives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

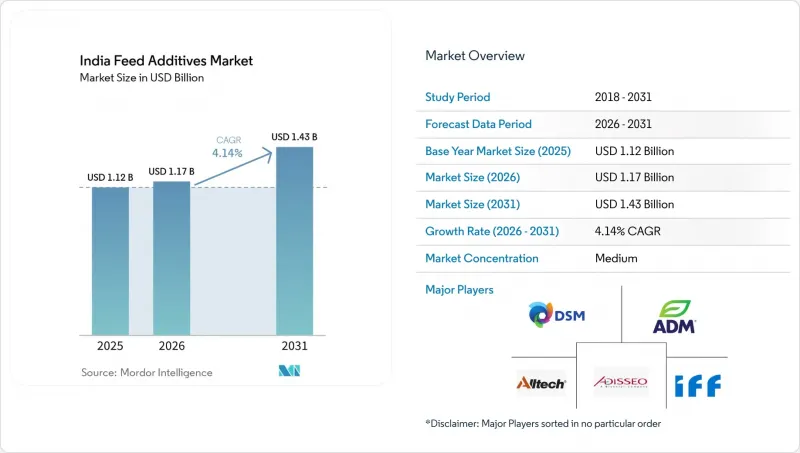

據 Mordor Intelligence 稱,印度飼料添加劑市場預計到 2026 年價值 11.7 億美元,高於 2025 年的 11.2 億美元,預計到 2031 年將達到 14.3 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 4.14%。

本報告按添加劑(酸味劑、胺基酸、抗生素、抗氧化劑、粘合劑、酵素、調味劑/甜味劑、礦物質、黴菌毒素解毒劑、植物性成分、色素、益生元、益生菌、維生素、酵母)和目標動物(水產養殖、家禽、反芻動物、豬和其他動物)進行細分。市場預測以價值(美元)和數量(噸)表示。

印度飼料添加劑市場的趨勢與洞察

家禽產量增加

2024年,商業肉雞和蛋雞養殖場生產了超過450萬噸雞肉和1,400億枚雞蛋。一體化程度超過80%,並建立了以酵素、胺基酸和有機酸為基礎的統一營養方案。領先的一體化企業將績效獎金與飼料轉換率掛鉤,促使營養學家積極採用已被證實能帶來可衡量結果的解決方案。標準化的養殖設施和自動化餵食系統實現了對耐熱植物來源原料和新一代植酸酶比例的精確控制。早期採用者報告稱,透過將植酸酶和益生菌結合使用,飼料轉換率提高了4%,這進一步鞏固了對優質功能性添加劑的需求。這些努力正在推動印度飼料添加劑市場的長期成長趨勢。

禁用抗生素生長促效劑

2024年,印度食品安全標準局(FSSAI)禁止使用粘菌素、氯黴素和硝基呋喃。這些生長促進劑的禁用促使綜合家禽養殖戶轉向益生菌、益生元、酵素和植物性添加劑,這些產品能夠在不產生抗菌殘留的情況下保護腸道環境。隨著綜合家禽養殖戶重新設計飼料飼料以符合更新後的殘留基準值,2025年益生菌的銷量年增了23%。飼料配製商也用有機酸取代飼料中的抗生素,這些有機酸可以降低腸道pH值並抑制致病菌。國際供應商抓住這項轉變帶來的機遇,推出了耐熱芽孢桿菌孢子,這些孢子能夠承受高達90°C的製粒溫度。隨著禁令範圍擴大到更多化合物,天然來源的性能增強劑在印度飼料添加劑市場的受歡迎程度可能會越來越高。

原物料價格波動

2025年初,由於玉米用於生產乙醇,其價格上漲至每公擔2425印度盧比(每噸293美元),而大豆粕則維持在每噸52,000印度盧比(每噸630美元)。由於飼料佔家禽生產成本的65%,價格的急劇上漲立即擠壓了利潤空間。為因應這一局面,飼料生產商儲備了60天的庫存,並調整了配方,添加了能夠分解非澱粉多醣的酶,從而將玉米的比例降低了3%至5個百分點。然而,由於外匯波動和運費上漲,價格仍存在不確定性。小規模酪農養殖戶和養豬戶率先削減了添加劑預算,導致印度飼料添加劑市場整體銷售量暫時下滑。

細分市場分析

截至2025年,胺基酸在印度飼料添加劑市場佔19.05%的佔有率。抗氧化劑雖然規模較小,但成長速度最快,年複合成長率達4.65%,這主要是由於原料價格波動導致飼料儲存期延長,增加了氧化風險。預計到2031年,抗氧化劑的年複合成長率也將達到3.74%,因為飼料生產商會不斷調整蛋白質含量以提高利潤率。 2025年,抗氧化劑在印度飼料添加劑市場規模中佔比達2.134億美元,並受益於生產連結獎勵計畫計劃(PLI),該計劃旨在促進國內離胺酸和甲硫胺酸產能的擴張。本地發酵降低了運輸成本,並減輕了來自中國的供應風險,使一體化企業能夠以穩定的價格簽訂合約。色氨酸的使用量自2023年以來加倍,這反映出其在旨在減輕蛋雞壓力的專用飼料飼料中的應用。酵素製劑產品系列持續多元化,新增了針對高纖維、區域性飼料客製化的木聚醣酶和蛋白酶。益生菌和植物萃取物的應用因低溫運輸供應情況而異,但耐熱芽孢桿菌孢子和薑黃精油的市場成長高於平均值。 BIS品質標準正將小規模混合商擠出市場,導致市場集中在DSM-Firmenich和Trouw Nutrition等擁有ISO認證預混合料生產線的知名品牌。

所有畜禽品種對維生素和礦物質預混合料的需求保持穩定。玉米運輸過程中發生的黃麴毒素污染事件提高了酪農養殖合作社的防範意識,導致對黴菌毒素解毒劑的需求增加。酵母細胞壁成分作為免疫調節劑,正被引入家禽幼畜飼料中,作為抗生素的替代品。總體而言,這些趨勢支持飼料添加劑供應商穩步成長,這些供應商提供經科學驗證的產品和強大的本地分銷網路,進一步增強了印度飼料添加劑市場的收入成長動能。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

- 調查方法

第2章:本報告的內容

第3章:執行摘要和主要發現

第4章:主要產業趨勢

- 飼養的動物數量

- 家禽

- 反芻動物

- 豬

- 飼料生產

- 水產養殖

- 家禽

- 反芻動物

- 豬

- 法律規範

- 印度

- 價值鍊和通路分析

- 市場促進因素

- 工業化家禽生產的成長正在推動飼料添加劑的使用。

- 禁止使用抗生素類生長促進劑將導致對添加劑配方進行審查。

- 支持水產養殖的措施正在提振對特殊添加劑的需求。

- 擴建綜合飼料廠將提高分銷效率。

- 透過生產關聯激勵計劃降低國內氨基酸成本

- 精準畜牧養殖實現微劑量給藥

- 市場限制因素

- 原物料價格波動推高了生產成本。

- 法規核准流程變得越來越漫長和複雜。

- 低溫運輸缺陷正在降低益生菌的存活率。

- 在後院飼養本地家禽會阻礙食品添加劑的廣泛使用。

第5章 市場規模與成長預測

- 添加劑

- 酸味劑

- 按添加劑類型

- 富馬酸

- 乳酸

- 丙酸

- 其他酸味劑

- 按添加劑類型

- 胺基酸

- 按添加劑類型

- 離胺酸

- 甲硫胺酸

- 蘇胺酸

- 色氨酸

- 其他胺基酸

- 按添加劑類型

- 抗生素

- 按添加劑類型

- 巴氏桿菌

- 青黴素

- 四環黴素

- 泰樂菌素

- 其他抗生素

- 按添加劑類型

- 抗氧化劑

- 按添加劑類型

- 丁基Hydroxyanisole(BHA)

- 二丁基羥基甲苯(BHT)

- 檸檬酸

- 乙氧喹

- 沒食子酸丙酯

- 生育酚

- 其他抗氧化劑

- 按添加劑類型

- 活頁夾

- 按添加劑類型

- 天然黏合劑

- 合成黏合劑

- 按添加劑類型

- 酵素

- 按添加劑類型

- 碳水化合物消化酶

- 植酸酶

- 其他酵素

- 按添加劑類型

- 調味劑和甜味劑

- 按添加劑類型

- 香味

- 甜味劑

- 按添加劑類型

- 礦物

- 按添加劑類型

- 主要礦物

- 微量元素

- 按添加劑類型

- 黴菌毒素解毒劑

- 按添加劑類型

- 粘合劑

- 生物轉化劑

- 按添加劑類型

- 植物源

- 按添加劑類型

- 精油

- 香草和香辛料

- 其他植物性添加劑

- 按添加劑類型

- 顏料

- 按添加劑類型

- 類胡蘿蔔素

- 薑黃素和螺旋藻

- 按添加劑類型

- 益生元

- 添加劑

- 果寡糖

- 半乳寡糖

- 菊糖

- 乳果糖

- 甘露聚醣

- 木寡糖

- 其他益生元

- 添加劑

- 益生菌

- 按添加劑類型

- 雙歧桿菌

- 腸球菌

- 乳酸菌

- 片球菌

- 鏈球菌

- 其他益生菌

- 按添加劑類型

- 維他命

- 按添加劑類型

- 維生素A

- 維生素B

- 維生素C

- 維生素E

- 其他維生素

- 按添加劑類型

- 東方

- 按添加劑類型

- 新鮮酵母

- 硒酵母

- 用過的酵母

- 托魯拉乾酵母

- 乳清酵母

- 酵母衍生成分

- 按添加劑類型

- 酸味劑

- 動物

- 水產養殖

- 按目標動物

- 魚

- 蝦

- 其他養殖物種

- 按目標動物

- 家禽

- 依動物類型

- 肉雞

- 產蛋母雞

- 其他家禽

- 依動物類型

- 反芻動物

- 依動物類型

- 牛

- 牛

- 其他反芻動物

- 依動物類型

- 豬

- 其他動物

- 水產養殖

第6章 競爭情勢

- 關鍵策略趨勢

- 市佔率分析

- 企業狀況

- 公司簡介

- Adisseo

- Archer Daniel Midland Co.

- BASF SE

- Alltech, Inc.

- Cargill Inc.

- DSM Nutritional Products AG

- Solvay SA

- IFF(Danisco Animal Nutrition)

- Kerry Group Plc

- SHV(Nutreco NV)

- Evonik Industries AG

- Elanco Animal Health Inc.

- Novus International, Inc.

第7章:執行長面臨的關鍵策略問題

According to Mordor Intelligence, india feed additives market size in 2026 is estimated at USD 1.17 billion, growing from 2025 value of USD 1.12 billion with 2031 projections showing USD 1.43 billion, growing at 4.14% CAGR over 2026-2031.

This report is Segmented by Additive (Acidifiers, Amino Acids, Antibiotics, Antioxidants, Binders, Enzymes, Flavors and Sweeteners, Minerals, Mycotoxin Detoxifiers, Phytogenics, Pigments, Prebiotics, Probiotics, Vitamins, and Yeast), Animal (Aquaculture, Poultry, Ruminant, Swine, and Other Animals). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

India Feed Additives Market Trends and Insights

Rising Industrial Poultry Production

Commercial broiler and layer farms produced more than 4.5 million tons of chicken meat and over 140 billion eggs in 2024. Integration levels crossed 80%, creating uniform nutritional protocols that rely on enzymes, amino acids, and organic acids. Major integrators linked performance bonuses to feed conversion ratios, so nutritionists aggressively adopt solutions demonstrated to deliver a measurable return. Standardized housing and automated feeders enable precise inclusion rates for heat-stable phytogenics and next-generation phytases. Early adopters report a 4% improvement in feed efficiency when phytase is combined with probiotics, further entrenching demand for premium functional additives. These practices reinforce the long-term expansion path of the India feed additives market.

Ban on Antibiotic Growth Promoters

The Food Safety and Standards Authority of India banned colistin, chloramphenicol, and nitrofurans in 2024. Eliminating these growth promoters pushed integrators toward probiotics, prebiotics, enzymes, and phytogenics that safeguard gut health without antimicrobial residues. Probiotic sales rose 23% year over year in 2025 as poultry integrators reformulated rations to comply with updated maximum-residue thresholds. Feed compounders also replaced in-feed antibiotics with organic acids that lower gut pH and suppress pathogens. International suppliers capitalized on this inflection by launching heat-stable Bacillus spores engineered to survive pelleting temperatures up to 90 °C. As the ban expands to cover additional molecules, the India feed additives market will increasingly favor natural performance enhancers.

Raw-Material Price Volatility

Maize prices climbed to INR 2,425 per quintal (USD 293 per metric ton) in early 2025 due to ethanol diversion, while soybean meal hovered at INR 52,000 per ton (USD 630 per metric ton). Feed accounts for 65% of poultry production cost, so any spike immediately erodes margins. Feed mills responded by stockpiling 60-day inventory and reformulating with enzymes that unlock non-starch polysaccharides, reducing corn inclusion by 3-5 percentage points. However, currency swings and freight charges still feed uncertainty into pricing. Small dairy and swine farms cut additive budgets first, temporarily damping overall volumes in the India feed additives market.

Other drivers and restraints analyzed in the detailed report include:

- Growing Aquaculture Output and Export Incentives

- Expansion of Integrated Feed Mills

- Cold-Chain Gaps Restraining Probiotic Viability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Amino acids retained a 19.05% share of the India feed additives market in 2025, while antioxidants, though smaller, are growing fastest at a 4.65% CAGR because volatile ingredient prices lengthen feed storage cycles and raise rancidity risk. are forecast to rise at a 3.74% CAGR through 2031 as feed formulators fine-tune protein levels for margin relief. The category commanded USD 213.4 million of the India feed additives market size in 2025 and benefits from the Production Linked Incentive scheme that encourages domestic lysine and methionine capacity. Local fermentation reduces freight premiums and mitigates Chinese supply risk, allowing integrators to lock in contracts at steady prices. Tryptophan usage doubled since 2023, reflecting adoption in specialty layer rations aimed at stress reduction. Enzyme portfolios continue to diversify with xylanases and proteases tailored to high-fiber regional diets. Probiotics and phytogenics see variable uptake depending on cold chain access, but heat-stable Bacillus spores and turmeric-derived essential oils post above-market growth. BIS quality mandates are pushing out sub-scale blenders and consolidating share toward established brands, including DSM-Firmenich and Trouw Nutrition, which both operate ISO-certified premix lines.

Demand for vitamin and mineral premixes remains stable across livestock species. Mycotoxin detoxifiers are gaining traction after aflatoxin outbreaks in maize shipments heightened awareness in dairy cooperatives. Yeast cell-wall derivatives used as immune modulators are entering poultry starter diets as antibiotic replacements. Collectively, these trends underpin steady gains for additive suppliers that offer scientifically validated products and robust local distribution, reinforcing revenue momentum in the India feed additives market.

List of Companies Covered in this Report:

- Adisseo

- Archer Daniel Midland Co.

- BASF SE

- Alltech, Inc.

- Cargill Inc.

- DSM Nutritional Products AG

- Solvay S.A.

- IFF(Danisco Animal Nutrition)

- Kerry Group Plc

- SHV (Nutreco NV)

- Evonik Industries AG

- Elanco Animal Health Inc.

- Novus International, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY & KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Animal Headcount

- 4.1.1 Poultry

- 4.1.2 Ruminants

- 4.1.3 Swine

- 4.2 Feed Production

- 4.2.1 Aquaculture

- 4.2.2 Poultry

- 4.2.3 Ruminants

- 4.2.4 Swine

- 4.3 Regulatory Framework

- 4.3.1 India

- 4.4 Value Chain & Distribution Channel Analysis

- 4.5 Market Drivers

- 4.5.1 Rising Industrial Poultry Production Drives Feed Additive Uptake

- 4.5.2 Antibiotic Growth-Promoter Ban Reshapes Additive Mix

- 4.5.3 Aquaculture Incentives Spur Specialty Additives

- 4.5.4 Integrated Feed Mill Expansion Boosts Distribution Efficiency

- 4.5.5 PLI scheme lowering domestic amino-acid costs

- 4.5.6 Precision livestock farming enabling micro-dosing

- 4.6 Market Restraints

- 4.6.1 Volatile Raw-Material Prices Inflate Production Costs

- 4.6.2 Lengthy and Complex Regulatory Approvals

- 4.6.3 Cold-chain gaps Restraining probiotic viability

- 4.6.4 Backyard desi poultry limiting additive uptake

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Additive

- 5.1.1 Acidifiers

- 5.1.1.1 By Sub Additive

- 5.1.1.1.1 Fumaric Acid

- 5.1.1.1.2 Lactic Acid

- 5.1.1.1.3 Propionic Acid

- 5.1.1.1.4 Other Acidifiers

- 5.1.1.1 By Sub Additive

- 5.1.2 Amino Acids

- 5.1.2.1 By Sub Additive

- 5.1.2.1.1 Lysine

- 5.1.2.1.2 Methionine

- 5.1.2.1.3 Threonine

- 5.1.2.1.4 Tryptophan

- 5.1.2.1.5 Other Amino Acids

- 5.1.2.1 By Sub Additive

- 5.1.3 Antibiotics

- 5.1.3.1 By Sub Additive

- 5.1.3.1.1 Bacitracin

- 5.1.3.1.2 Penicillins

- 5.1.3.1.3 Tetracyclines

- 5.1.3.1.4 Tylosin

- 5.1.3.1.5 Other Antibiotics

- 5.1.3.1 By Sub Additive

- 5.1.4 Antioxidants

- 5.1.4.1 By Sub Additive

- 5.1.4.1.1 Butylated Hydroxyanisole (BHA)

- 5.1.4.1.2 Butylated Hydroxytoluene (BHT)

- 5.1.4.1.3 Citric Acid

- 5.1.4.1.4 Ethoxyquin

- 5.1.4.1.5 Propyl Gallate

- 5.1.4.1.6 Tocopherols

- 5.1.4.1.7 Other Antioxidants

- 5.1.4.1 By Sub Additive

- 5.1.5 Binders

- 5.1.5.1 By Sub Additive

- 5.1.5.1.1 Natural Binders

- 5.1.5.1.2 Synthetic Binders

- 5.1.5.1 By Sub Additive

- 5.1.6 Enzymes

- 5.1.6.1 By Sub Additive

- 5.1.6.1.1 Carbohydrases

- 5.1.6.1.2 Phytases

- 5.1.6.1.3 Other Enzymes

- 5.1.6.1 By Sub Additive

- 5.1.7 Flavors & Sweeteners

- 5.1.7.1 By Sub Additive

- 5.1.7.1.1 Flavors

- 5.1.7.1.2 Sweeteners

- 5.1.7.1 By Sub Additive

- 5.1.8 Minerals

- 5.1.8.1 By Sub Additive

- 5.1.8.1.1 Macrominerals

- 5.1.8.1.2 Microminerals

- 5.1.8.1 By Sub Additive

- 5.1.9 Mycotoxin Detoxifiers

- 5.1.9.1 By Sub Additive

- 5.1.9.1.1 Binders

- 5.1.9.1.2 Biotransformers

- 5.1.9.1 By Sub Additive

- 5.1.10 Phytogenics

- 5.1.10.1 By Sub Additive

- 5.1.10.1.1 Essential Oil

- 5.1.10.1.2 Herbs & Spices

- 5.1.10.1.3 Other Phytogenics

- 5.1.10.1 By Sub Additive

- 5.1.11 Pigments

- 5.1.11.1 By Sub Additive

- 5.1.11.1.1 Carotenoids

- 5.1.11.1.2 Curcumin & Spirulina

- 5.1.11.1 By Sub Additive

- 5.1.12 Prebiotics

- 5.1.12.1 By Sub Additive

- 5.1.12.1.1 Fructo Oligosaccharides

- 5.1.12.1.2 Galacto Oligosaccharides

- 5.1.12.1.3 Inulin

- 5.1.12.1.4 Lactulose

- 5.1.12.1.5 Mannan Oligosaccharides

- 5.1.12.1.6 Xylo Oligosaccharides

- 5.1.12.1.7 Other Prebiotics

- 5.1.12.1 By Sub Additive

- 5.1.13 Probiotics

- 5.1.13.1 By Sub Additive

- 5.1.13.1.1 Bifidobacteria

- 5.1.13.1.2 Enterococcus

- 5.1.13.1.3 Lactobacilli

- 5.1.13.1.4 Pediococcus

- 5.1.13.1.5 Streptococcus

- 5.1.13.1.6 Other Probiotics

- 5.1.13.1 By Sub Additive

- 5.1.14 Vitamins

- 5.1.14.1 By Sub Additive

- 5.1.14.1.1 Vitamin A

- 5.1.14.1.2 Vitamin B

- 5.1.14.1.3 Vitamin C

- 5.1.14.1.4 Vitamin E

- 5.1.14.1.5 Other Vitamins

- 5.1.14.1 By Sub Additive

- 5.1.15 Yeast

- 5.1.15.1 By Sub Additive

- 5.1.15.1.1 Live Yeast

- 5.1.15.1.2 Selenium Yeast

- 5.1.15.1.3 Spent Yeast

- 5.1.15.1.4 Torula Dried Yeast

- 5.1.15.1.5 Whey Yeast

- 5.1.15.1.6 Yeast Derivatives

- 5.1.15.1 By Sub Additive

- 5.1.1 Acidifiers

- 5.2 By Animal

- 5.2.1 Aquaculture

- 5.2.1.1 By Sub Animal

- 5.2.1.1.1 Fish

- 5.2.1.1.2 Shrimp

- 5.2.1.1.3 Other Aquaculture Species

- 5.2.1.1 By Sub Animal

- 5.2.2 Poultry

- 5.2.2.1 By Sub Animal

- 5.2.2.1.1 Broiler

- 5.2.2.1.2 Layer

- 5.2.2.1.3 Other Poultry Birds

- 5.2.2.1 By Sub Animal

- 5.2.3 Ruminants

- 5.2.3.1 By Sub Animal

- 5.2.3.1.1 Beef Cattle

- 5.2.3.1.2 Dairy Cattle

- 5.2.3.1.3 Other Ruminants

- 5.2.3.1 By Sub Animal

- 5.2.4 Swine

- 5.2.5 Other Animals

- 5.2.1 Aquaculture

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments)

- 6.4.1 Adisseo

- 6.4.2 Archer Daniel Midland Co.

- 6.4.3 BASF SE

- 6.4.4 Alltech, Inc.

- 6.4.5 Cargill Inc.

- 6.4.6 DSM Nutritional Products AG

- 6.4.7 Solvay S.A.

- 6.4.8 IFF(Danisco Animal Nutrition)

- 6.4.9 Kerry Group Plc

- 6.4.10 SHV (Nutreco NV)

- 6.4.11 Evonik Industries AG

- 6.4.12 Elanco Animal Health Inc.

- 6.4.13 Novus International, Inc.

7 KEY STRATEGIC QUESTIONS FOR FEED ADDITIVE CEOS

全球特種飼料添加劑市場

全球特種飼料添加劑市場 飼料用甲硫胺酸添加劑:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

飼料用甲硫胺酸添加劑:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 全球飼料添加劑市場:按類型、功能、最終用戶、動物種類、來源、形態和地區分類-預測至2031年

全球飼料添加劑市場:按類型、功能、最終用戶、動物種類、來源、形態和地區分類-預測至2031年 飼料添加劑市場規模、佔有率和成長分析(按類型、畜種、成分、形態、功能和地區分類)—產業預測(2026-2033 年)

飼料添加劑市場規模、佔有率和成長分析(按類型、畜種、成分、形態、功能和地區分類)—產業預測(2026-2033 年) 特種飼料添加劑市場(按類型、動物、產地、形態、功能、製造技術和地區分類)-預測至2030年

特種飼料添加劑市場(按類型、動物、產地、形態、功能、製造技術和地區分類)-預測至2030年 飼料添加劑市場-全球產業規模、佔有率、趨勢、機會及預測(按成分類型、牲畜、形態、地區和競爭情況細分,2020-2030 年)

飼料添加劑市場-全球產業規模、佔有率、趨勢、機會及預測(按成分類型、牲畜、形態、地區和競爭情況細分,2020-2030 年) 中國飼料添加劑市場:依產品種類、牲畜、來源、形式、最終用戶、地區、機會、預測,2017-2031年日本飼料添加劑市場評估:依產品類型、牲畜、原料、格式、最終用戶和地區劃分的機會和預測(2018-2032)全球飼料添加劑市場評估:依產品類型、牲畜、原料、形式、最終用戶、地區、機會、預測(2017-2031)印度飼料添加劑市場評估:依產品類型、牲畜、原料、形式、最終用戶、地區、機會、預測(2018 財年-2032 財年)

中國飼料添加劑市場:依產品種類、牲畜、來源、形式、最終用戶、地區、機會、預測,2017-2031年日本飼料添加劑市場評估:依產品類型、牲畜、原料、格式、最終用戶和地區劃分的機會和預測(2018-2032)全球飼料添加劑市場評估:依產品類型、牲畜、原料、形式、最終用戶、地區、機會、預測(2017-2031)印度飼料添加劑市場評估:依產品類型、牲畜、原料、形式、最終用戶、地區、機會、預測(2018 財年-2032 財年)