|

市場調查報告書

商品編碼

2063725

歐洲大型廢棄物收集服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Europe Bulky Waste Collection Service - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

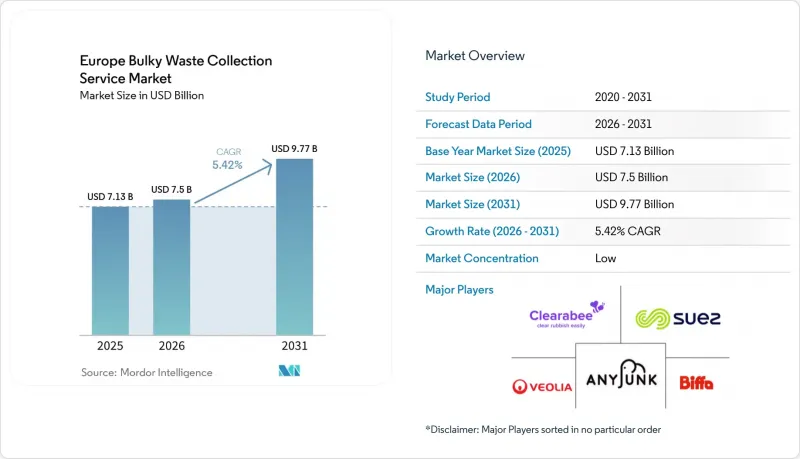

根據 Mordor Intelligence 預測,歐洲重型廢棄物收集服務市場規模將從 2025 年的 71.3 億美元和 2026 年的 75 億美元成長到 2031 年的 97.7 億美元,2026 年至 2031 年的複合年成長率為 5.42%。

本報告按收集模式(上門收集、按需收集、其他)、來源(住宅、商業、其他)、廢棄物類型(家具和軟墊、金屬和廢料、其他)以及地區(英國、德國、法國、義大利、西班牙、俄羅斯和其他歐洲國家)進行細分。市場預測以價值(美元)和數量(噸)表示。

歐洲大型廢棄物收集服務市場趨勢與洞察

住宅和商業領域的維修和整修活動增加

受住宅和商業房地產維修整修活動增加的推動,歐洲重型廢棄物收集服務市場正經歷顯著成長。新冠疫情後,住宅維修支出激增,法國、德國、西班牙和義大利等國的維修授權年增率高達15%至20%,主要得益於遠距辦公的興起和節能維修的需求。住宅裝修每個項目會產生2至5噸重型廢棄物,包括舊固定裝置、地板材料、電器和家具,需要專業的垃圾處理服務。歐盟的節能舉措,例如《建築能源性能指令》(EPBD),以及德國、法國和荷蘭的補貼計劃,進一步提高了裝修率,導致重型廢棄物量增加。受混合辦公模式和辦公室、零售店、酒店和餐廳重新設計的推動,商業維修也加劇了垃圾量的成長,其中包括隔間牆、設備和過時的設備。歐洲35%的建築建於1970年以前,老舊建築需要持續維護,因此對廢棄物收集服務的需求仍然強勁。在監管壓力、人口趨勢以及歐洲建築環境生命週期等因素的推動下,市政當局和私營企業正在擴展按需收集和分類設施等服務,以應對混合散裝廢棄物的管理問題。

歐盟嚴格的廢棄物管理法規與循環經濟政策

歐盟正在實施近年來最全面的廢棄物改革,其中包括一系列重塑整個供應鏈(從生產商到收集商)角色的條款。修訂後的《廢棄物框架指令》將於2025年10月生效,其中包含擴大紡織品生產者責任制以及基於既定時間表的食物廢棄物減量目標等要求,這些都將對上游環節產生壓力,最終影響分揀和收集流程。數位化廢棄物運輸系統將從2026年5月起強制要求對歐盟境內的廢棄物流動進行近乎即時的追蹤,從而加強執法力度,並堵住此前允許透過錯誤分類規避回收義務的漏洞。包裝改革也持續推進,朝著可回收性評估和產業特定要求的方向發展,加速材料重新設計和下游分類。這些變革將對能夠管理整個重型廢棄物流程中資料完整性、認證和分類品質的營運商進行評估。它們還將提高合規標準,並影響歐洲重型廢棄物收集服務市場的競標、定價和技術應用。

非法傾倒和合違規問題

廢棄物犯罪和違規削弱了合法經營者的價格競爭力,並阻礙了環境目標的實現。在英國,當局強調了廢棄物犯罪造成的巨大經濟損失,並實施了一項多年計劃,其中包括為數位化廢棄物追蹤系統提供資金,以及擴大執法力度以遏制非法活動。該計劃涵蓋了數據、監控和許可監管方面的改進,表明執法政策正轉向數據驅動的威懾和早期療育。在全球層面,多邊組織指出,廢棄物走私的規模和複雜性模糊了供應鏈中的責任追究,並為合法收集者增加了額外的合規成本。這些趨勢在執法不力的地區造成了短期價格壓力。從長遠來看,數位追蹤要求和協調一致的跨境措施應能提高基本的合規水平,並使歐洲大型廢棄物收集服務市場中合規的經營者受益。

細分市場分析

預計到2025年,上門收集服務將佔據46.72%的市場佔有率,而按需服務預計將以5.82%的複合年成長率成長至2031年,這主要得益於人口密集城市居民對便利性日益成長的需求。這種差異反映了服務設計的重大轉變,在大都會圈,基於應用程式的預約和快速回應已不再是可選項。結合固定路線和隨叫隨到服務的混合模式正日益普及,因為它們既能保持路線密度,又能靈活應對需求激增。在歐洲大規模市政廢棄物收集服務市場,包括GPS追蹤和動態調度在內的數位化功能正成為市政競標的基本要求。對資料收集和服務交付認證進行標準化的營運商可以提高計費準確性、應對力和客戶滿意度。

路邊垃圾收集的韌性源自於既有路線網路的網路效應,最佳化後的路線能夠隨著規模的擴大降低單位成本。競標規範中擴大納入永續性和報告條款,近期公共合約也表明,為了實現區域氣候目標,垃圾收集正朝著使用電動車、尺寸合適的車輛以及先進的車載系統方向發展。基於應用程式的平台憑藉著精細化的服務和透明的定價競爭,在人口密集地區實現了最永續的成果。市政投放網路和門禁設施可以作為路邊垃圾收集的補充,減輕高峰期的廢棄物壓力。隨著合規性和績效報告的整合,歐洲重型廢棄物收集服務市場的收集模式選擇將需要在成本、應對力和資料完整性之間取得平衡。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 都市化進程和家庭垃圾的增加

- 歐盟嚴格的廢棄物管理法規與循環經濟政策

- 歐洲消費者環保意識日益增強

- 智慧廢棄物管理技術的廣泛應用

- 地方政府擴大廢棄物收集計劃

- 電子商務和包裝廢棄物的成長

- 市場限制因素

- 專用收集設備的高營運成本

- 農村和偏遠地區基礎設施匱乏

- 地方政府面臨的預算限制

- 非法傾倒和合違規問題

- 價值供應鏈分析

- 收款計劃系統

- 路徑最佳化方法

- 分銷和物流框架

- 監理情勢

- 技術展望

- 波特五力模型

- 人工智慧驅動的生成式廢棄物收集對服務供應商收入成長的影響

第5章 市場規模與成長預測,以及

- 透過恢復模式

- 上門收集

- 一經請求

- 混合

- 基於合約的B2B

- 其他

- 來源

- 住宅

- 商業

- 產業

- 市政當局/政府

- 其他用途(宗教場所、臨時災難避難所、電影和電視拍攝場地)

- 廢棄物類型

- 家具和室內裝飾

- 金屬和廢料

- 白色家電/家用電器

- 建設與拆除

- 其他(活動相關廢棄物、醫療/設施廢棄物)

- 國家

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Clearabee

- AnyJunk Limited

- Veolia Environnement SA

- SUEZ SA

- Biffa plc

- FCC Environment(FCC Recycling UK Limited)

- Stericycle, Inc.

- Remondis SE & Co. KG

- Casella Waste Systems, Inc.

- Serco

- Waste Connections, Inc.

- PreZero Service Sud GmbH

- Redooo GmbH

- Eggersmann GmbH

- FES Frankfurter Entsorgungs

- Mucvibes

- Aflex

- S&D Recycler

- WeGreen

- Stadtwerke Offenbach

第7章 市場機會與未來展望

According to Mordor Intelligence, the europe bulky waste collection service market size is projected to expand from USD 7.13 billion in 2025 and USD 7.5 billion in 2026 to USD 9.77 billion by 2031, registering a CAGR of 5.42% between 2026 to 2031.

This report is Segmented by Collection Model (Curbside, On-Demand, and More), Source (Residential, Commercial, and More), by Waste Type (Furniture & Upholstery, Metal & Scrap Items, and More), and by Geography (United Kingdom, Germany, France, Italy, Spain, Russia, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Tons).

Europe Bulky Waste Collection Service Market Trends and Insights

Increasing Renovation and Refurbishment Activities Across Residential and Commercial Sectors

The European bulky waste collection service market is growing significantly, driven by increased renovation and refurbishment activities in residential and commercial properties. Post-COVID-19, home improvement spending has surged, with countries such as France, Germany, Spain, and Italy reporting 15-20% annual growth in renovation permits driven by remote work trends and energy-efficiency upgrades. Residential renovations generate 2-5 tons of bulky waste per project, including old fixtures, flooring, appliances, and furniture, requiring specialized disposal services. EU energy efficiency initiatives, such as the Energy Performance of Buildings Directive (EPBD), and subsidy programs in Germany, France, and the Netherlands have further boosted renovation rates, thereby contributing to increased bulky waste volumes. Commercial refurbishments, driven by hybrid work models and redesigns in offices, retail, hotels, and restaurants, add to this waste, including partition walls, fixtures, and outdated equipment. With 35% of European buildings constructed before 1970, aging properties require ongoing maintenance, sustaining demand for waste collection services. Municipalities and private operators are expanding services such as on-demand pickups and sorting facilities to manage mixed bulky waste, driven by regulatory pressures, demographic trends, and the lifecycle of Europe's built environment.

Stringent European Union Waste Management Regulations and Circular Economy Policies

The European Union is implementing the most comprehensive waste reforms in years, with provisions that reshape roles across the chain from producers to collectors. The revised Waste Framework Directive entered into force in October 2025 and includes requirements such as Extended Producer Responsibility for textiles on a set timetable and targets to reduce food waste, creating upstream pressure that ultimately affects sorting and collection practices. The Digital Waste Shipment System requires near real-time tracking for intra-European Union waste movements from May 2026, enabling better enforcement and closing gaps that previously allowed misclassification to avoid recycling obligations. Packaging reforms continue to advance toward recyclability grading and domain-specific obligations that will accelerate material redesign and downstream separation. These changes reward operators who can manage data integrity, certification, and sorting quality across bulky waste streams. They also set a higher baseline for compliance that will influence bids, pricing, and technology adoption in the Europe bulky waste collection service market.

Illegal Dumping and Non-Compliance Issues

Waste crime and non-compliance erode legitimate operators' pricing and undermine environmental goals. In England, authorities have documented significant financial losses from waste crime and introduced a multi-year plan that funds digital waste tracking and expands enforcement tools to deter illegal activity. The plan includes measures to improve data, surveillance, and permitting oversight, signaling an enforcement shift toward data-driven deterrence and earlier intervention. At the global level, multilateral bodies have highlighted the scale and complexity of waste trafficking, which complicates accountability along the supply chain and imposes additional compliance costs on lawful collectors. These patterns create near-term pricing pressure in regions with persistent enforcement gaps. Over time, digital tracking requirements and coordinated cross-border action can improve baseline compliance, which should benefit aligned operators in the Europe bulky waste collection service market.

Other drivers and restraints analyzed in the detailed report include:

- Rising Adoption of Smart Waste Management Technologies

- Increasing Urbanization and Household Waste Generation

- High Operational Costs of Specialized Collection Equipment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Curbside collection held 46.72% share in 2025, while on-demand services are projected to advance at a 5.82% CAGR through 2031 as convenience expectations rise in dense cities. This divergence reflects a broader shift in service design, where app-based booking and shorter response times are no longer optional in metropolitan areas. Hybrid models that blend fixed routes with on-call capacity are gaining favor because they protect route density while enabling flexible surge response. Digital capabilities, including GPS tracking and dynamic scheduling, are becoming a baseline requirement in large municipal tenders in the Europe bulky waste collection service market. Operators that standardize data capture and proof-of-service improve billing accuracy, audit readiness, and customer satisfaction.

Curbside's resilience stems from network effects in established corridors, where optimized routes lower unit costs at scale. Tender specifications increasingly embed sustainability and reporting clauses, and recent public contracts illustrate the shift toward electric or right-sized vehicles and advanced in-cab systems to meet local climate goals. App-based platforms compete through service granularity and transparent pricing, with the most durable gains in high-density neighborhoods. Municipal drop-off networks and access-controlled sites can complement curbside by relieving pressure during peak disposal periods. As compliance and performance reporting converge, selection of the collection model in the Europe bulky waste collection service market will balance cost, responsiveness, and data integrity.

List of Companies Covered in this Report:

- Clearabee

- AnyJunk Limited

- Veolia Environnement S.A.

- SUEZ S.A.

- Biffa plc

- FCC Environment (FCC Recycling UK Limited)

- Stericycle, Inc.

- Remondis SE & Co. KG

- Casella Waste Systems, Inc.

- Serco

- Waste Connections, Inc.

- PreZero Service Sud GmbH

- Redooo GmbH

- Eggersmann GmbH

- FES Frankfurter Entsorgungs

- Mucvibes

- Aflex

- S&D Recycler

- WeGreen

- Stadtwerke Offenbach

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing urbanization and household waste generation

- 4.2.2 Stringent European Union waste management regulations and circular economy policies

- 4.2.3 Growing environmental awareness among European consumers

- 4.2.4 Rising adoption of smart waste management technologies

- 4.2.5 Expansion of municipal waste collection programs

- 4.2.6 Growth in e-commerce and packaging waste

- 4.3 Market Restraints

- 4.3.1 High operational costs of specialized collection equipment

- 4.3.2 Limited infrastructure in rural and remote areas

- 4.3.3 Budget constraints faced by municipal authorities

- 4.3.4 Illegal dumping and non-compliance issues

- 4.4 Value / Supply-Chain Analysis

- 4.4.1 Collection scheduling systems

- 4.4.2 Route optimization methods

- 4.4.3 Dispatch and logistics framework

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

- 4.8 Impact of GenAI-Powered Waste Collection on Service Providers' Revenue Growth

5 Market Size & Growth Forecasts (Value) and (Volume)

- 5.1 By Collection Model

- 5.1.1 Curbside

- 5.1.2 On-Demand

- 5.1.3 Hybrid

- 5.1.4 Contracted B2B

- 5.1.5 Others

- 5.2 By Source

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.2.3 Industrial

- 5.2.4 Municipal/Government

- 5.2.5 Others (Religious Institutions, Temporary Disaster Relief Camps, Film/TV Production Sets)

- 5.3 By Waste Type

- 5.3.1 Furniture & Upholstery

- 5.3.2 Metal & Scrap Items

- 5.3.3 White Goods/Appliances

- 5.3.4 Construction & Demolition

- 5.3.5 Others (Event-specific Waste, Biomedical/Institutional)

- 5.4 By Country

- 5.4.1 United Kingdom

- 5.4.2 Germany

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Spain

- 5.4.6 Russia

- 5.4.7 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)}

- 6.4.1 Clearabee

- 6.4.2 AnyJunk Limited

- 6.4.3 Veolia Environnement S.A.

- 6.4.4 SUEZ S.A.

- 6.4.5 Biffa plc

- 6.4.6 FCC Environment (FCC Recycling UK Limited)

- 6.4.7 Stericycle, Inc.

- 6.4.8 Remondis SE & Co. KG

- 6.4.9 Casella Waste Systems, Inc.

- 6.4.10 Serco

- 6.4.11 Waste Connections, Inc.

- 6.4.12 PreZero Service Sud GmbH

- 6.4.13 Redooo GmbH

- 6.4.14 Eggersmann GmbH

- 6.4.15 FES Frankfurter Entsorgungs

- 6.4.16 Mucvibes

- 6.4.17 Aflex

- 6.4.18 S&D Recycler

- 6.4.19 WeGreen

- 6.4.20 Stadtwerke Offenbach

7 Market Opportunities & Future Outlook

- 7.1 Smart Cities & IoT Integration

- 7.2 Producer Responsibility Expansion

分散式回收系統市場預測至2034年-按系統類型、材料、處理能力、經營模式、技術、最終用戶和地區分類的全球分析

分散式回收系統市場預測至2034年-按系統類型、材料、處理能力、經營模式、技術、最終用戶和地區分類的全球分析 大型廢棄物收集服務:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)德國大型廢棄物收集服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)日本大型垃圾收集服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

大型廢棄物收集服務:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)德國大型廢棄物收集服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)日本大型垃圾收集服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 智慧廢棄物收集技術市場:按技術、組件、廢棄物類型和最終用戶分類-2026-2032年全球市場預測自動化垃圾收集系統市場:按組件、系統類型、最終用戶和垃圾類型分類-2026-2032年全球市場預測氣動廢棄物收集系統市場:按系統類型、組件、廢棄物類型、安裝方式、應用和銷售管道,全球預測,2026-2032年

智慧廢棄物收集技術市場:按技術、組件、廢棄物類型和最終用戶分類-2026-2032年全球市場預測自動化垃圾收集系統市場:按組件、系統類型、最終用戶和垃圾類型分類-2026-2032年全球市場預測氣動廢棄物收集系統市場:按系統類型、組件、廢棄物類型、安裝方式、應用和銷售管道,全球預測,2026-2032年 自動化廢棄物收集系統市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、營運方式、應用、地區和競爭格局分類,2021-2031年

自動化廢棄物收集系統市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、營運方式、應用、地區和競爭格局分類,2021-2031年 2026-2030年全球自動化廢棄物收集系統市場2032 年自動廢棄物分類和回收系統市場預測:按組件、廢棄物分類類型、技術、最終用戶和地區進行的全球分析

2026-2030年全球自動化廢棄物收集系統市場2032 年自動廢棄物分類和回收系統市場預測:按組件、廢棄物分類類型、技術、最終用戶和地區進行的全球分析