|

市場調查報告書

商品編碼

2063724

日本大型垃圾收集服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Japan Bulky Waste Collection Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

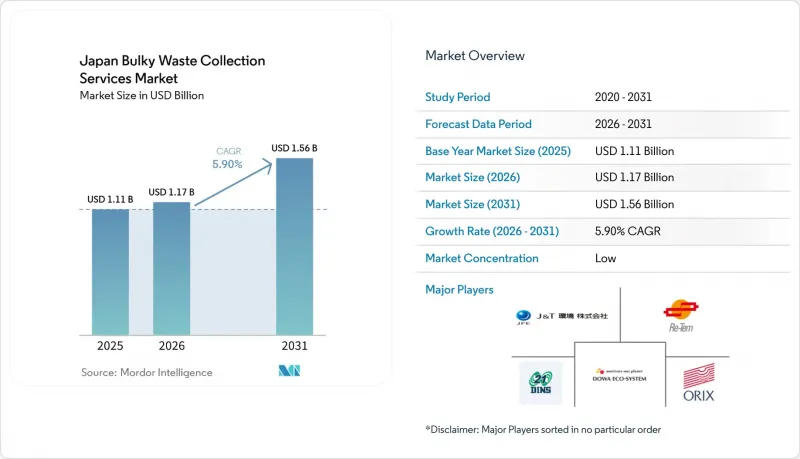

根據 Mordor Intelligence 預測,日本大型廢棄物收集服務市場規模將從 2025 年的 11.1 億美元成長到 2026 年的 11.7 億美元,到 2031 年將達到 15.6 億美元,2026 年至 2031 年的複合年成長率為 5.90%。

本報告按收集模式(路邊收集、按需收集、混合收集、B2B合約收集及其他)、來源(住宅、商業、工業、市政及其他)和廢棄物類型(家具和軟墊、金屬和廢料、白色家電、建築和拆除廢棄物及其他)進行細分。市場預測以價值(美元)和數量(噸)表示。

日本大型廢棄物收集服務市場的趨勢與洞察

掩埋能力有限及土地短缺

在日本,掩埋場的短缺正在影響大型廢棄物收集服務的定價和服務模式。根據第五個基本計畫的政策,日本的循環經濟目標包括在2030年減少最終處置量,這增加了盡可能將大件廢棄物從最終處置轉移到回收途徑的必要性。即使是東京高效的焚化廠網路也會產生灰燼,佔用有限的垃圾掩埋空間,因此,為了減少運往處理設施的垃圾量,對垃圾進行預處理和資源回收的壓力越來越大。由於大件垃圾金屬含量高、含有有害成分,且體積龐大,不符合標準的收集和焚燒流程,因此其處理面臨特殊的挑戰。為此,日本依賴遍佈全國的583個大件垃圾破碎處理設施,日處理能力達2,0401噸。透過上游工程轉售和回收創造價值的企業,在緩解處置限制的同時,提高了單位盈利,在掩埋掩埋費和運輸成本不斷上漲的背景下,成為一項具有競爭力的優勢。從中長期來看,資源回收政策的持續協調可能會有利於那些整合收集、預處理和監管合規的企業。

政府政策旨在促進3R社會和循環經濟。

日本已將循環經濟定位為國家戰略,設定了2030年實現排放產出回收率的明確目標,以及80兆日圓(約5,100億美元)的循環市場目標。這些目標將影響地方政府的規劃和採購政策,尤其是在日本大規模廢棄物收集服務市場中,與收集和分類能力相關的方面。 「循環經濟轉型加速方案」旨在加強生產與回收之間的聯繫,支持廢棄太陽能電池板的回收利用,並擴大再生材料的供應,從而推動上游對可追溯和分揀的垃圾的需求,以便將其供應給合適的處理生產線。對於服務供應商,這創造了提供逆向物流和收集預分類服務的機會,有助於地方政府實現資源生產力目標,並幫助生產者履行其生命週期責任。據行業組織稱,自2000年以來,最終處置的工業廢棄物數量已顯著下降,而進一步減少表明,有必要收集難以處理的廢棄物,並在可以通過認證體系進行大範圍處理的地區最佳化跨縣物流。隨著這些政策的成熟,能夠證明其碳捕獲記錄和碳強度的私人公司將有機會贏得公共合約和企業客戶,這與經合組織揭露規則的發展相一致。

廢棄物管理和處置高成本

在日本的大件垃圾收集服務市場,營運成本仍然是一大限制因素,收集、運輸、中間處理和處置的預算都給市政財政帶來了壓力。國家統計數據顯示,一般廢棄物管理服務每年都會產生巨額支出,由於設施建設和土地相關費用高昂,都市區的人均成本更高。在燃料、人事費用和設施升級等持續壓力下,預計2024年工業廢棄物價格將上漲10%至20%,並預計2025年將進一步上漲。這將透過車輛和處理設施的共用間接影響大件垃圾營運商。城市層面的數據證實了價格和成本的上漲;例如,伊丹市在過去幾個財政年度的大件垃圾收入和每噸處理成本均呈上升趨勢。營運商可以透過利用減少收集頻率和提高容器容量利用率的技術來緩解這些壓力。例如,智慧壓縮容器有助於減少收集頻率並最佳化路線。從長遠來看,在同一設施中進行預分類和加工並回收高附加價值材料的整合模式,可以透過提高資產利用率和增加材料收入來抵消不斷上漲的成本。

細分市場分析

預計到2025年,按需收集服務將佔日本大件垃圾收集服務市場佔有率的43.21%,並在2031年之前以6.21%的複合年成長率成長。這反映了老齡化家庭的需求以及該模式對不規則垃圾收集模式的適用性。此模式的優點在於能夠根據實際收集需求調整車輛調度,從而在需要縮小居住空間或清理舊宅時減少車輛等待時間,並提高客戶滿意度。按需收集模式也支援路邊預分類和按物品處理,從而提高下游回收流程的效率,並有利於致力於實現循環經濟目標的市政當局。在日本大件垃圾收集服務市場,將按需收集的垃圾送到專門的破碎和分類設施的營運商佔據主導地位,而這項服務是透過遍布全國的專業設施網路提供的。這些協同優勢凸顯了為何按需服務比常規的挨家挨戶收集服務成長得更快,因為在一些城市,由於家庭數量的減少,收集路線的密度正在下降。

儘管路邊收集模式在郊區仍然很受歡迎,因為那裡的每週收集模式較為固定,但由於人口結構變化導致每條路線上的住戶數量減少,這種模式的利潤率面臨壓力。結合定時收集和按需柔軟性的混合模式可以滿足郊區和農村地區的需求,因為這些地區的需求在預測期內會波動。基於合約的B2B收集服務為辦公室和零售商提供更穩定的收集量和更長的資產更新週期。此外,企業對廢棄物收集和排放的報告需求也使這類服務受益,這促使企業傾向於選擇能夠記錄結果的綜合服務提供者。在日本,隨著逆向廢棄物需求的加深、路線規劃平台的效率提升以及市政合約更加注重循環經濟成果,預計按需服務的市場規模將比路邊收集服務成長更快。未來,服務提供者的差異化將取決於數位化預約、物品級分類以及與回收商的合作,以回收資源價值並降低掩埋風險。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 掩埋能力有限及土地短缺

- 政府政策旨在促進3R社會和循環經濟。

- 生產者延伸責任法

- 人口老化導致服務需求增加

- 高度都市化且人口稠密的居住

- 嚴格的廢棄物處理法規和強制性收費

- 市場限制因素

- 廢棄物管理和處置高成本

- 廢棄物回收業嚴重人手不足

- 外國居住者面臨的語言障礙

- 複雜多元的地方政府法規

- 價值供應鏈分析

- 收款計劃系統

- 路徑最佳化方法

- 分銷和物流框架

- 監理情勢

- 技術展望

- 波特五力模型

- 人工智慧驅動的生成式廢棄物收集對服務供應商收入成長的影響

第5章 市場規模與成長預測

- 透過恢復模式

- 路邊

- 一經請求

- 混合

- 基於合約的B2B

- 其他

- 來源

- 住宅

- 商業

- 產業

- 市政當局/政府

- 其他用途(宗教場所、臨時災難避難所、電影和電視拍攝場地)

- 廢棄物類型

- 家具和室內裝飾

- 金屬和廢料

- 白色家電/家用電器

- 建設與拆除

- 其他(活動相關廢棄物、醫療/設施相關廢棄物)

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Daiei Kankyo Holdings Co., Ltd.

- ORIX Environmental Resources Management Corporation(OERM)

- J&T Recycling Corporation

- DOWA ECO-SYSTEM Co., Ltd.

- Re-Tem Corporation

- Santou Unyu Co., Ltd.

- SMART RELOCATE INC.

- Veolia Environnement SA

- SUEZ SA

- Ze Okinawa Bulk Trash

- Clean Harbors, Inc.

- Remondis SE & Co. KG

- J&T Recycling Corporation

- TokyoMove

- SHIRAI GROUP

- Recology Inc

- ALBA Group

- PreZero

- Renewi plc

- Ecosystem Japan Co., Ltd

第7章 市場機會與未來展望

According to Mordor Intelligence, the japan bulky waste collection services market size is expected to grow from USD 1.11 billion in 2025 to USD 1.17 billion in 2026 and is forecast to reach USD 1.56 billion by 2031 at 5.90% CAGR over 2026-2031.

This report is Segmented by Collection Model (Curbside, On-Demand, Hybrid, Contracted B2B, and Others), by Source (Residential, Commercial, Industrial, Municipal, and Others), and by Waste Type (Furniture & Upholstery, Metal & Scrap Items, White Goods/Appliances, Construction & Demolition, and Others). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Tons).

Japan Bulky Waste Collection Services Market Trends and Insights

Limited Landfill Capacity and Land Scarcity

In Japan, the scarcity of landfills shapes the pricing and service design of bulky waste collection services. National circular economy targets include reducing final disposal volumes toward 2030 in line with the Fifth Basic Plan's direction, heightening the need to divert bulky items away from final disposal and into recycling streams where feasible. Tokyo's network of high-efficiency incineration plants still produces ash that competes for limited landfill space, which puts pressure on pre-treatment and material recovery to reduce what reaches controlled sites. Bulky waste presents a particular challenge due to its metal content, hazardous components, and dimensions that do not fit standard collection and combustion workflows, which is why Japan relies on a national network of 583 dedicated bulky waste crushing facilities with a daily capacity of 20,401 tons. Providers that capture resale or recycling value upstream ease disposal constraints while strengthening unit economics, making it a competitive differentiator as landfill gate fees and transport burdens rise. Over the medium term, continued policy alignment on resource circulation is likely to favor integrated operators that combine collection, pre-processing, and router-compliant recyclers.

Government Policies Promoting a 3R Society and Circular Economy

Japan has elevated the circular economy to a national strategy, with explicit 2030 targets for input and output recycling rates and a JPY 80 trillion (USD 0.51 trillion) circular market objective, which will shape local government plans and procurement for collection and sorting capacity in the Japan bulky waste collection services market. The Circular Economy Transition Acceleration Package directs closer collaboration between manufacturing and recycling, supports end-of-life solar panel recycling, and expands the supply of recycled materials, driving upstream demand for traceable, segmented collections that can feed compliant processing lines. For service providers, this creates opportunities to offer reverse logistics and pre-sorting at pickup, which helps municipalities meet resource productivity objectives and helps producers comply with lifecycle responsibilities. Industry groups have reported sizable reductions in final disposal of industrial waste since 2000, suggesting that further gains require capturing difficult streams and optimizing cross-prefectural logistics where certification allows wider-area processing. As these policies mature, private operators that can document recovery performance and carbon intensity are positioned to win public contracts and corporate accounts under evolving OECD disclosure rules.

High Cost of Waste Management and Treatment

Operating costs remain a major constraint as collection, transport, intermediate processing, and disposal budgets strain municipal finances in the Japan bulky waste collection services market. National figures show significant annual spending on general waste operations, with urban cores incurring much higher per capita costs due to advanced facility construction and land-related expenses. Industrial waste disposal prices rose 10-20% in 2024 amid persistent fuel, labor, and facility renewal pressures, with further increases projected into 2025, which indirectly affect bulky waste operators through shared fleets and processing hubs. City-level data confirms fee and cost escalation, as seen in Itami City's trend of higher bulky waste revenues and per-ton processing costs across recent fiscal years. Operators can mitigate pressure by using technology that reduces collection frequency and increases bin capacity utilization, as demonstrated by smart compression bins that lower pickups and support route optimization. Over time, integrated models that co-locate pre-sorting with treatment and capture higher-value materials can offset cost inflation by improving asset utilization and increasing materials revenue.

Other drivers and restraints analyzed in the detailed report include:

- Extended Producer Responsibility (EPR) Laws

- Aging Population Creating Service Demand

- Severe Labor Shortages in Waste Collection

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

On-demand collection commanded 43.21% of the Japan bulky waste collection services market share in 2025 and is projected to grow at a 6.21% CAGR through 2031, reflecting alignment with aging household needs and episodic generation patterns. This model's advantage is its ability to match vehicle dispatch with actual pickup requests, reducing idle time and improving customer satisfaction when downsizing or estate clearance is required . The on-demand format also supports curbside pre-sorting and item-level handling, making downstream recycling more efficient and benefiting municipalities working toward circular-economy targets. The Japan bulky waste collection services market favors providers that route on-demand pickups into facilities designed for crushing and segregation, a capability available across a nationwide base of specialized facilities. These combined advantages underscore why on-demand is growing faster than scheduled curbside services, where route density has declined with falling household counts in some municipalities.

Curbside models still serve suburban contexts where weekly patterns remain predictable, yet they face margin pressure as demographics reduce household concentrations per route. Hybrid approaches that pair scheduled pickups with on-call flexibility can bridge the needs of suburban and rural areas, where demand fluctuates during the forecast period. Contracted B2B collection provides steadier volumes with longer asset replacement cycles for offices and retail, and it benefits from corporate reporting needs around waste recovery and emissions, which shifts vendor selection toward integrated providers that can document outcomes. The Japan bulky waste collection services market size for on-demand services is likely to expand faster than curbside services as reverse logistics requirements deepen, routing platforms improve productivity, and municipal contracts emphasize circular outcomes. Over time, operator differentiation will depend on digital booking, item-level classification, and partnerships with recyclers to capture materials value and reduce landfill exposure.

List of Companies Covered in this Report:

- Daiei Kankyo Holdings Co., Ltd.

- ORIX Environmental Resources Management Corporation (OERM)

- J&T Recycling Corporation

- DOWA ECO-SYSTEM Co., Ltd.

- Re-Tem Corporation

- Santou Unyu Co., Ltd.

- SMART RELOCATE INC.

- Veolia Environnement S.A.

- SUEZ S.A.

- Ze Okinawa Bulk Trash

- Clean Harbors, Inc.

- Remondis SE & Co. KG

- J&T Recycling Corporation

- TokyoMove

- SHIRAI GROUP

- Recology Inc

- ALBA Group

- PreZero

- Renewi plc

- Ecosystem Japan Co., Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Limited Landfill Capacity and Land Scarcity

- 4.2.2 Government Policies Promoting 3R Society and Circular Economy

- 4.2.3 Extended Producer Responsibility (EPR) Laws

- 4.2.4 Aging Population Creating Service Demand

- 4.2.5 High Urbanization and Dense Living Conditions

- 4.2.6 Strict Waste Disposal Regulations and Mandatory Fees

- 4.3 Market Restraints

- 4.3.1 High Cost of Waste Management and Treatment

- 4.3.2 Severe Labor Shortages in Waste Collection

- 4.3.3 Language Barriers for Foreign Residents

- 4.3.4 Complex and Varying Municipal Regulations

- 4.4 Value / Supply-Chain Analysis

- 4.4.1 Collection scheduling systems

- 4.4.2 Route optimization methods

- 4.4.3 Dispatch and logistics framework

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

- 4.8 Impact of GenAI-Powered Waste Collection on Service Providers' Revenue Growth

5 Market Size & Growth Forecasts

- 5.1 By Collection Model

- 5.1.1 Curbside

- 5.1.2 On-Demand

- 5.1.3 Hybrid

- 5.1.4 Contracted B2B

- 5.1.5 Others

- 5.2 By Source

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.2.3 Industrial

- 5.2.4 Municipal/Government

- 5.2.5 Others (Religious Institutions, Temporary Disaster Relief Camps, Film/TV Production Sets)

- 5.3 By Waste Type

- 5.3.1 Furniture & Upholstery

- 5.3.2 Metal & Scrap Items

- 5.3.3 White Goods/Appliances

- 5.3.4 Construction & Demolition

- 5.3.5 Others (Event-specific Waste, Biomedical/Institutional)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)}

- 6.4.1 Daiei Kankyo Holdings Co., Ltd.

- 6.4.2 ORIX Environmental Resources Management Corporation (OERM)

- 6.4.3 J&T Recycling Corporation

- 6.4.4 DOWA ECO-SYSTEM Co., Ltd.

- 6.4.5 Re-Tem Corporation

- 6.4.6 Santou Unyu Co., Ltd.

- 6.4.7 SMART RELOCATE INC.

- 6.4.8 Veolia Environnement S.A.

- 6.4.9 SUEZ S.A.

- 6.4.10 Ze Okinawa Bulk Trash

- 6.4.11 Clean Harbors, Inc.

- 6.4.12 Remondis SE & Co. KG

- 6.4.13 J&T Recycling Corporation

- 6.4.14 TokyoMove

- 6.4.15 SHIRAI GROUP

- 6.4.16 Recology Inc

- 6.4.17 ALBA Group

- 6.4.18 PreZero

- 6.4.19 Renewi plc

- 6.4.20 Ecosystem Japan Co., Ltd

7 Market Opportunities & Future Outlook

- 7.1 Smart Cities & IoT Integration

- 7.2 Producer Responsibility Expansion

分散式回收系統市場預測至2034年-按系統類型、材料、處理能力、經營模式、技術、最終用戶和地區分類的全球分析

分散式回收系統市場預測至2034年-按系統類型、材料、處理能力、經營模式、技術、最終用戶和地區分類的全球分析 大型廢棄物收集服務:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)德國大型廢棄物收集服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲大型廢棄物收集服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

大型廢棄物收集服務:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)德國大型廢棄物收集服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲大型廢棄物收集服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 智慧廢棄物收集技術市場:按技術、組件、廢棄物類型和最終用戶分類-2026-2032年全球市場預測自動化垃圾收集系統市場:按組件、系統類型、最終用戶和垃圾類型分類-2026-2032年全球市場預測氣動廢棄物收集系統市場:按系統類型、組件、廢棄物類型、安裝方式、應用和銷售管道,全球預測,2026-2032年

智慧廢棄物收集技術市場:按技術、組件、廢棄物類型和最終用戶分類-2026-2032年全球市場預測自動化垃圾收集系統市場:按組件、系統類型、最終用戶和垃圾類型分類-2026-2032年全球市場預測氣動廢棄物收集系統市場:按系統類型、組件、廢棄物類型、安裝方式、應用和銷售管道,全球預測,2026-2032年 自動化廢棄物收集系統市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、營運方式、應用、地區和競爭格局分類,2021-2031年

自動化廢棄物收集系統市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、營運方式、應用、地區和競爭格局分類,2021-2031年 2026-2030年全球自動化廢棄物收集系統市場2032 年自動廢棄物分類和回收系統市場預測:按組件、廢棄物分類類型、技術、最終用戶和地區進行的全球分析

2026-2030年全球自動化廢棄物收集系統市場2032 年自動廢棄物分類和回收系統市場預測:按組件、廢棄物分類類型、技術、最終用戶和地區進行的全球分析