|

市場調查報告書

商品編碼

2063723

德國大型廢棄物收集服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Germany Bulky Waste Collection Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

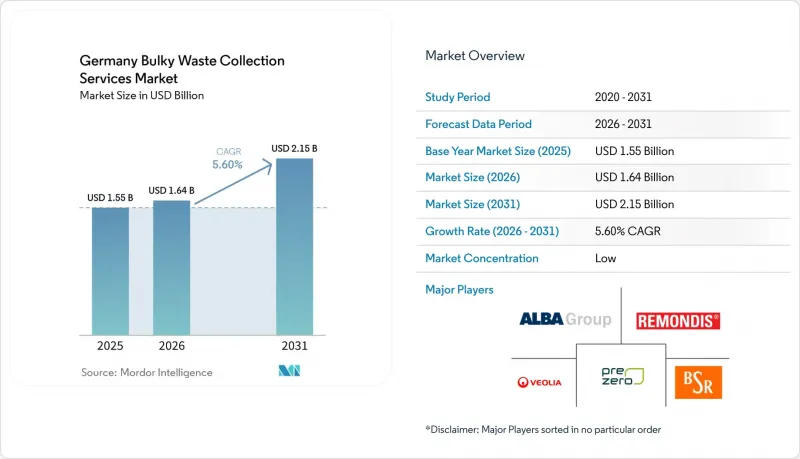

根據 Mordor Intelligence 預測,德國重型廢棄物收集服務市場規模將從 2025 年的 15.5 億美元成長到 2026 年的 16.4 億美元,到 2031 年將達到 21.5 億美元,2026 年至 2031 年的複合年成長率為 5.60%。

本報告按收集模式(路邊收集、按需收集、混合收集、B2B合約收集及其他)、來源(住宅、商業、工業、市政及其他)和廢棄物類型(家具及室內裝飾、金屬及廢料、白色家電、建築及拆除廢棄物及其他)進行細分。市場預測以價值(美元)和數量(噸)表示。

德國大型廢棄物收集服務市場的趨勢與洞察

循環經濟法強制要求對大量廢棄物進行分類收集

德國的《循環經濟法》規定,公共廢棄物管理機構必須提供分類散裝廢棄物收集服務,以便對廢棄物進行組件級再利用和回收。該規定明確了競標中的營運預期,並增強了對預分類和記錄保存投資的合理性。歐盟廢棄物法規規定,到2025年,紡織品強制分類的範圍將進一步擴大,這進一步鞏固了源頭分類流程,並將其與市政收集點的散裝廢棄物物流聯繫起來。明確的合規路徑和處罰措施降低了市政營運商和投資於再利用和回收基礎設施的私人承包商的規劃風險。公共報告要求和聯邦監管提高了德國散裝廢棄物收集服務市場的透明度,有助於市政服務水準與廢棄物減量目標保持一致。聯邦和歐盟層級的監管協調支持了路線設計、收集點容量和再利用夥伴關係關係等方面的穩定成長計畫。

透過市政應用程式和線上入口網站實現大規模廢棄物預約的數位化。

市政應用程式和P2P(P2P) 合作正在改變預約流程,居民可以透過這些方式選擇收集時段、確認交接並接收接受通知。柏林與 Tiptapp 的合作實現了付費的按需收集服務,建立了包含廢棄物認證的完整處理流程。與固定的季度收集週期相比,這大大縮短了回應時間。漢堡的「Stadtreinigung」應用程式簡化了收集日曆、位置導航和廢棄物類型指南的訪問,減少了客服中心的積壓,提高了調度準確性。帶有時間戳記的預約資訊和地址級資料會流入市政系統,有助於最佳化路線以滿足每日需求。數位化管道也減少了非法路邊傾倒垃圾的動機,因為錯過的預約可以比等待下一個固定區域收集日期更快地重新預約。因此,德國的大型廢棄物收集服務市場正穩步向動態容量規劃轉型,而那些能夠即時調度車輛和可靠數據管治的營運商則更具優勢。

降低面臨成本壓力的城市大規模廢棄物收集的頻率。

德國公共事業協會 (IG BAU) 設定的 2025 年和 2026 年薪資成長標準推高了工會成員企業的營運成本,迫使各市政當局重新審視其服務模式。一些小規模的市政當局正在透過減少定期大件垃圾收集的頻率,並將需求轉移到付費的按需服務來應對這項挑戰。減少定期收集會增加每次收集日需要處理的垃圾量,加劇工人的工作壓力,並增加垃圾臨時溢出和居民不滿的風險。此外,預算限制也延緩了中型市政當局數位化試點計畫的實施,限制了基於物聯網的路線最佳化技術的推廣。因此,德國的大件垃圾收集服務市場出現了服務頻率不一致的情況,財政狀況較好的都市區比農村地區進展更快。

細分市場分析

預計到2025年,按需收集模式將佔據德國重型廢棄物收集服務市場67.21%的佔有率,並將在2031年之前保持最快的成長速度,複合年成長率(CAGR)將達到5.93%,這主要得益於數位化預約在各大城市的普及。居民可以透過與市政當局的合作,例如柏林與Tiptapp的合作,短期預約服務。在該合作項目中,GPS驗證的收據檢驗廢棄物已妥善收集。德國重型廢棄物收集服務市場向這種模式轉變的驅動力在於,路線規劃器可以根據社區優先安排預約,並減少每次收集的行駛距離。市政當局正在將按需收集與微型收集工具相結合,例如在人口密集的城市地區使用電動貨運自行車,以及處理無需整車負載容量的小批量垃圾。在中等規模的城市,結合社區收集日和靈活路線的混合策略正在推廣,這些城市正在部署垃圾箱感測器,以便按需觸發服務。

儘管路邊垃圾收集日曆系統在農村和數位化程度較低的地區仍然普遍存在,但隨著智慧型手機的普及和市政應用程式降低了預約門檻,其市場佔有率正在下降。基於合約的B2B框架也支援按需收集系統,因為物業管理公司和商業設施需要優先收集時間和確認資訊。德國的重型廢棄物收集服務市場正受惠於按需資料流,這些資料流能夠持續改善人員配置和營運規劃。從2025年開始,與床墊相關的生產者延伸責任(EPR)補償將為能夠提供高品質分類材料的模式提供財務穩定性。總而言之,按需收集服務是德國最大、成長最快的廢棄物收集服務形式。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 循環經濟法規定對大件垃圾進行單獨收集。

- 透過市政應用程式和線上入口網站實現大件垃圾收集預約的數位化。

- 柏林、慕尼黑和漢堡的都市區密度增加

- 從2025年起,EPR(生產者責任延伸制度)將擴展至床墊和襯墊傢俱領域。

- 老建築的翻新熱潮帶動了對收藏品的需求。

- 德國雙制系統(DSD)標準正在提高回收效率。

- 市場限制因素

- 減少面臨財政困難的城市的大件垃圾收集頻率。

- 與非法傾倒垃圾和黑市廢棄物處理經營者競爭。

- 東德各州司機短缺

- 根據IG BAU的集體談判協議,人事費用很高。

- 價值供應鏈分析

- 收款計劃系統

- 路徑最佳化方法

- 分銷和物流框架

- 監理情勢

- 技術展望

- 波特五力模型

- 人工智慧驅動的生成式廢棄物收集對服務供應商收入成長的影響

第5章 市場規模與成長預測

- 透過恢復模式

- 路邊

- 一經請求

- 混合

- 基於合約的B2B

- 其他

- 來源

- 住宅

- 商業

- 產業

- 市政當局/政府

- 其他用途(宗教場所、臨時災難避難所、電影和電視拍攝場地)

- 廢棄物類型

- 家具和室內裝飾

- 金屬和廢料

- 白色家電/家用電器

- 建設與拆除

- 其他(活動相關廢棄物、醫療/設施相關廢棄物)

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Remondis SE & Co. KG

- PreZero Stiftung & Co. KG

- ALBA Group

- Veolia Environnement SA

- Berliner Stadtreinigung(BSR)

- HCS A/S

- Gemidan

- SUEZ SA

- Stadtreinigung Hamburg

- AWM Munchen(Abfallwirtschaftsbetrieb Munchen)

- Entsorgungsgesellschaft Westmunsterland(EGW)

- FES Frankfurter Entsorgungs and Service GmbH

- Redooo GmbH

- Eggersmann GmbH

- Weg Werk

- Mucvibes

- Aflex

- S&D Recycler

- WeGreen

- Stadtwerke Offenbach

第7章 市場機會與未來展望

According to Mordor Intelligence, the germany bulky waste collection services market size is expected to grow from USD 1.55 billion in 2025 to USD 1.64 billion in 2026 and is forecast to reach USD 2.15 billion by 2031 at 5.60% CAGR over 2026-2031.

This report is Segmented by Collection Model (Curbside, On-Demand, Hybrid, Contracted B2B, and Others), by Source (Residential, Commercial, Industrial, Municipal, and Others), and by Waste Type (Furniture & Upholstery, Metal & Scrap Items, White Goods/Appliances, Construction & Demolition, and Others). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Tons).

Germany Bulky Waste Collection Services Market Trends and Insights

Circular Economy Act Mandating Separate Bulky Waste Collection

Germany's Kreislaufwirtschaftsgesetz requires public waste authorities to provide separate bulky waste collection that enables preparation for reuse and component-level recycling. This mandate clarifies operational expectations for tenders and strengthens the case for investments in pre-sorting and documentation. The 2025 expansion of separate collection obligations for textiles under EU waste rules further normalizes source-separated flows that interact with bulky waste logistics at municipal depots. Clear compliance pathways and sanctioning tools reduce planning risk for municipal operators and private contractors that invest in reuse and recycling infrastructure. Public reporting requirements and federal oversight increase transparency across the Germany bulky waste collection services market, helping align municipal service levels with diversion goals. The regulatory alignment across federal and EU levels supports stable growth planning for route design, depot capacity, and reuse partnerships.

Digitalization of Sperrmull Booking Through Municipal Apps and Online Portals

Municipal apps and peer-to-peer integrations are reshaping booking behavior by letting residents choose collection slots, verify handovers, and receive confirmations. Berlin's cooperation with Tiptapp enables paid on-demand pickups that close the loop with disposal proof, which shortens response times compared with fixed quarterly rounds. Hamburg's Stadtreinigung app streamlines access to collection calendars, site navigation, and guidance on waste types, reducing call-center backlogs and improving scheduling accuracy. Timestamped bookings and address-level data flow into municipal systems and support route optimization that matches daily demand clusters. Digital channels also reduce incentives for curbside dumping because missed bookings can be rescheduled more quickly than waiting for the next fixed neighborhood day. The net effect is a steady migration in the Germany bulky waste collection services market toward dynamic capacity planning that favors operators with real-time dispatch and data governance credibility.

Sperrmull Collection Frequency Reductions in Cost-Pressured Municipalities

Wage increases set by IG BAU for 2025 and 2026 have raised operating costs for unionized operators, putting pressure on municipalities to adjust service models. Some smaller jurisdictions respond by reducing calendar-based bulky-waste rounds and shifting demand toward paid on-demand slots. When scheduled pick-ups are cut back, event-day volumes rise, straining crew capacity and risking interim overflow and resident dissatisfaction. Budget constraints also delay digital pilots in mid-sized municipalities, limiting the diffusion of IoT-enabled route optimization. The net effect is a patchwork of service frequency across the Germany bulky waste collection services market, with better-resourced cities moving faster than rural districts.

Other drivers and restraints analyzed in the detailed report include:

- Growing Urban Population Density in Berlin, Munich, and Hamburg

- EPR Expansion for Mattresses and Upholstered Furniture from 2025

- Illegal Dumping Competition from Schwarzentsorgung

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

On-demand collection model led with a 67.21% of the Germany bulky waste collection services market share in 2025 and is projected to record the fastest growth at a 5.93% CAGR through 2031 as digital booking becomes the default in large cities. Residents can request service within short windows through municipal integrations, such as Berlin's cooperation with Tiptapp, which verifies proper drop-off with GPS-verified receipts. The Germany bulky waste collection services market has shifted toward this format because route planners can prioritize bookings by neighborhood clusters and reduce miles per pickup. Municipalities are pairing on-demand pickup with micro-collection assets such as e-cargobikes for dense cores and small loads that do not require a full truck. Hybrid strategies that mix neighborhood-day events and flexible routes are expanding in mid-sized cities that deploy container sensors to trigger demand-based service.

The curbside calendar model remains in rural and lower-digitized areas, yet it is losing share as smartphone adoption and municipal apps reduce booking friction. Contracted B2B frameworks also support on-demand logic because property managers and commercial estates require prioritized windows and confirmations. The Germany bulky waste collection services market benefits from on-demand data streams that enable continuous improvements in crew assignment and trip planning. EPR-related reimbursements for mattresses starting in 2025 add financial stability to models that can deliver high-quality segregated items. Taken together, these elements make on-demand both the largest and fastest-growing format in the Germany bulky waste collection services market.

List of Companies Covered in this Report:

- Remondis SE & Co. KG

- PreZero Stiftung & Co. KG

- ALBA Group

- Veolia Environnement SA

- Berliner Stadtreinigung (BSR)

- HCS A/S

- Gemidan

- SUEZ S.A.

- Stadtreinigung Hamburg

- AWM Munchen (Abfallwirtschaftsbetrieb Munchen)

- Entsorgungsgesellschaft Westmunsterland (EGW)

- FES Frankfurter Entsorgungs and Service GmbH

- Redooo GmbH

- Eggersmann GmbH

- Weg Werk

- Mucvibes

- Aflex

- S&D Recycler

- WeGreen

- Stadtwerke Offenbach

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Circular Economy Act Mandating Separate Bulky Waste Collection

- 4.2.2 Digitalization of Sperrmull Booking Through Municipal Apps and Online Portals

- 4.2.3 Growing Urban Population Density in Berlin, Munich, and Hamburg

- 4.2.4 EPR Expansion for Mattresses and Upholstered Furniture from 2025

- 4.2.5 Renovation Boom in Altbau Buildings Driving Collection Demand

- 4.2.6 Dual System Deutschland (DSD) Standards Pushing Collection Efficiency

- 4.3 Market Restraints

- 4.3.1 Sperrmull Collection Frequency Reductions in Cost-Pressured Municipalities

- 4.3.2 Illegal Dumping Competition from Schwarzentsorgung

- 4.3.3 Driver Shortages in Eastern German States

- 4.3.4 High Labor Costs Under IG BAU Collective Agreements

- 4.4 Value / Supply-Chain Analysis

- 4.4.1 Collection scheduling systems

- 4.4.2 Route optimization methods

- 4.4.3 Dispatch and logistics framework

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

- 4.8 Impact of GenAI-Powered Waste Collection on Service Providers' Revenue Growth

5 Market Size & Growth Forecasts

- 5.1 By Collection Model

- 5.1.1 Curbside

- 5.1.2 On-Demand

- 5.1.3 Hybrid

- 5.1.4 Contracted B2B

- 5.1.5 Others

- 5.2 By Source

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.2.3 Industrial

- 5.2.4 Municipal/Government

- 5.2.5 Others (Religious Institutions, Temporary Disaster Relief Camps, Film/TV Production Sets)

- 5.3 By Waste Type

- 5.3.1 Furniture & Upholstery

- 5.3.2 Metal & Scrap Items

- 5.3.3 White Goods/Appliances

- 5.3.4 Construction & Demolition

- 5.3.5 Others (Event-specific Waste, Biomedical/Institutional)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)}

- 6.4.1 Remondis SE & Co. KG

- 6.4.2 PreZero Stiftung & Co. KG

- 6.4.3 ALBA Group

- 6.4.4 Veolia Environnement SA

- 6.4.5 Berliner Stadtreinigung (BSR)

- 6.4.6 HCS A/S

- 6.4.7 Gemidan

- 6.4.8 SUEZ S.A.

- 6.4.9 Stadtreinigung Hamburg

- 6.4.10 AWM Munchen (Abfallwirtschaftsbetrieb Munchen)

- 6.4.11 Entsorgungsgesellschaft Westmunsterland (EGW)

- 6.4.12 FES Frankfurter Entsorgungs and Service GmbH

- 6.4.13 Redooo GmbH

- 6.4.14 Eggersmann GmbH

- 6.4.15 Weg Werk

- 6.4.16 Mucvibes

- 6.4.17 Aflex

- 6.4.18 S&D Recycler

- 6.4.19 WeGreen

- 6.4.20 Stadtwerke Offenbach

7 Market Opportunities & Future Outlook

- 7.1 Smart Cities & IoT Integration

- 7.2 Producer Responsibility Expansion

分散式回收系統市場預測至2034年-按系統類型、材料、處理能力、經營模式、技術、最終用戶和地區分類的全球分析

分散式回收系統市場預測至2034年-按系統類型、材料、處理能力、經營模式、技術、最終用戶和地區分類的全球分析 大型廢棄物收集服務:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)日本大型垃圾收集服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)歐洲大型廢棄物收集服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

大型廢棄物收集服務:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)日本大型垃圾收集服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)歐洲大型廢棄物收集服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 智慧廢棄物收集技術市場:按技術、組件、廢棄物類型和最終用戶分類-2026-2032年全球市場預測自動化垃圾收集系統市場:按組件、系統類型、最終用戶和垃圾類型分類-2026-2032年全球市場預測氣動廢棄物收集系統市場:按系統類型、組件、廢棄物類型、安裝方式、應用和銷售管道,全球預測,2026-2032年

智慧廢棄物收集技術市場:按技術、組件、廢棄物類型和最終用戶分類-2026-2032年全球市場預測自動化垃圾收集系統市場:按組件、系統類型、最終用戶和垃圾類型分類-2026-2032年全球市場預測氣動廢棄物收集系統市場:按系統類型、組件、廢棄物類型、安裝方式、應用和銷售管道,全球預測,2026-2032年 自動化廢棄物收集系統市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、營運方式、應用、地區和競爭格局分類,2021-2031年

自動化廢棄物收集系統市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、營運方式、應用、地區和競爭格局分類,2021-2031年 2026-2030年全球自動化廢棄物收集系統市場2032 年自動廢棄物分類和回收系統市場預測:按組件、廢棄物分類類型、技術、最終用戶和地區進行的全球分析

2026-2030年全球自動化廢棄物收集系統市場2032 年自動廢棄物分類和回收系統市場預測:按組件、廢棄物分類類型、技術、最終用戶和地區進行的全球分析