|

市場調查報告書

商品編碼

2063722

大型廢棄物收集服務:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Bulky Waste Collection Service - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

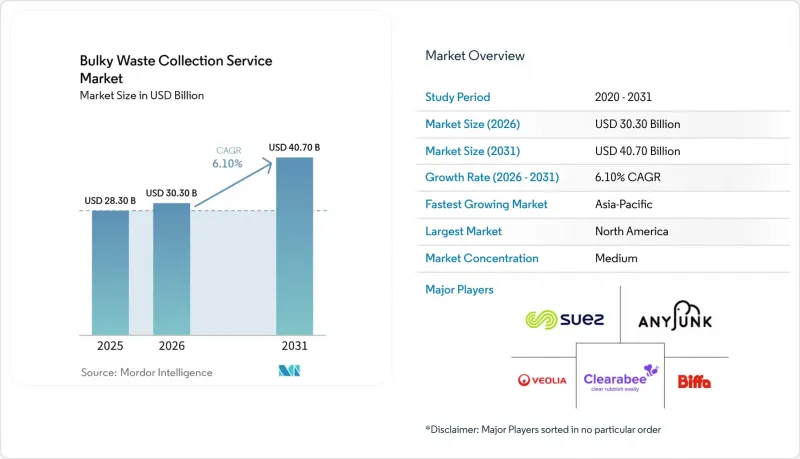

根據 Mordor Intelligence 預測,大型廢棄物收集服務的市場規模預計將從 2025 年的 283 億美元成長到 2026 年的 303 億美元,然後從 2026 年到 2031 年以 6.10% 的複合年成長率成長,到 2031 年達到 407 億美元。

本報告廢棄物類型(家具及室內裝潢、金屬及廢料等)、來源(住宅、商業等)、收集模式(上門收集、按需收集等)和地區(北美、歐洲、亞太、南美、中東和非洲)進行細分。市場預測以價值(十億美元)和數量(噸)為單位呈現。

全球大型廢棄物收集服務市場趨勢及洞察

都市化進程和一般廢棄物產生量的增加。

快速的都市化過程導致大件廢棄物(包括家具、家電和維修垃圾)的產生量持續成長。預計全球垃圾總量將從2023年的21億噸增至2050年的38億噸,這將進一步加劇本已缺乏足夠傳輸能力和專門處理大件垃圾能力的城市系統的壓力。在低收入地區,未收集和管理不善的廢棄物仍然是正規垃圾收集系統面臨的結構性障礙,隨著財政能力的提升、捐助項目和基礎設施資金籌措的推進,服務差距正在逐步縮小,而這些差距的擴大將形成長期的潛在需求。英國地方政府的數據顯示,2024年至2025年間,英國將收集2,520萬噸廢棄物,這顯示垃圾處理量將保持穩定,凸顯了針對無法容器化的大件廢棄物制定專門解決方案的重要性。隨著都市化的推進,大件廢棄物收集服務市場受益於多戶住宅可預測的更新週期和維修,這使得城市中心的需求更加集中。此外,大眾對安全且便利的垃圾收集服務的需求日益成長,也推動了這個市場的發展,並引導用戶選擇合法公司。

政府對廢棄物管理有嚴格的規定

關鍵司法管轄區更嚴格的政策正在加強可追溯性和資源回收義務,從而促進了經認證的收集和分揀能力的採用。在歐盟,修訂後的《廢棄物框架指令》將於2025年10月16日生效,要求成員國在30個月內建立紡織品和鞋類生產者延伸責任制(EPR)。這將引入新的資金籌措和營運管道,以擴大難以處理的散裝廢棄物的正規收集範圍。在英國,打擊廢棄物犯罪的資金增加,無人機監控和自動車牌識別等工具的使用範圍也在擴大,以遏制那些透過降價進行競爭的不法經營者。該系統重點關注分類收集、環保定價和出口裝運前分揀等方面的法規,正朝著檢驗的回收率方向發展,這有利於那些擁有可審計的數位化記錄和健全品管的經營者。在印度,建築和拆除廢棄物的修訂要求已立法生效。全國範圍內的廢棄物追蹤系統正在逐步實施,這標誌著從自願參與轉向強制執行,並擴大了對專業大宗廢棄物收集和記錄保存服務的需求。大宗廢棄物收集服務市場正透過以合規為導向的競標和夥伴關係來應對這一變化,從而提升處理受監管廢物流的能力。

非法傾銷的氾濫以及與非正規部門的競爭

非法傾倒垃圾持續侵占合法經營者的資源,並加重地方政府的清理負擔。在英格蘭,2024年至2025年間記錄在案的非法傾倒垃圾案件高達126萬起,其中相當一部分發生在主要道路上。公部門大規模廢棄物的成本也不斷攀升,這直接削弱了合法服務模式的經濟可行性。儘管執法機構已阻止非法出口並查封了大量無證設施,但案件數量仍然遠高於調查能力,表明執法能力存在持續缺口,助長了非法活動。廢棄物犯罪也是宏觀經濟的拖累,據估計每年造成英國數億英鎊的損失。這阻礙了對合法網路的投資,並降低了那些非法垃圾處理方式較為廉價的地區的合法垃圾收集率。由於執法力度不足,大型廢棄物收集服務市場面臨更高的客戶獲取成本,因為家庭和小型企業在選擇合法或非法途徑時,需要權衡便利性和感知風險。隨著數位化廢棄物追蹤和有針對性的執法力度不斷加大,資料外洩的風險或許會降低,但短期波動仍然會使規劃和利用變得複雜。因此,高風險地區的營運商必須與地方當局密切合作,並使其宣傳、收費系統和服務交付週期與當地執法部門的步伐保持一致。

細分市場分析

2025年,路邊收集服務佔大件垃圾收集市場佔有率的49.21%。這主要得益於與市政當局簽訂的長期契約,從而維持了可預測的常規路線。另一方面,按需服務預計將以6.71%的複合年成長率快速成長至2031年,這得益於基於應用程式的預約、物聯網驅動的路線最佳化以及電動汽車車隊的普及,這些因素降低了邊際收整合本並提高了服務可用性。 Republic Services在2025年和2026年對電動收集車輛、可再生天然氣項目和聚合物加工的投資表明,整合到下游流程中可以抵消收集運營的波動,並增強市政競標中的服務提案競爭力。 Suez的WasteConnect和AutoDiag的實施表明,互聯容器、即時品質監控和流量分析可以提高路線密度並減少污染物,這對快速反應的運作至關重要。這些大件廢棄物的成分差異很大。因此,大規模廢棄物收集服務市場正在向混合模式靠攏,將基本路線的效率與當天或第二天處理垃圾的靈活處理能力結合。

公共垃圾收集中心的政策也支持這種混合模式。在艾克斯-馬賽-普羅旺斯大區,為了規範服務並改善評估,公共垃圾收集中心的使用規則和每日接收量限制在2025年進行了修訂。這有助於實現資源回收目標,並減輕尖峰時段路邊垃圾收集系統的壓力。在德國,諸如奧伯哈弗爾為居民提供的免費大件廢棄物投放服務等項目,是對傳統路邊垃圾收集的補充,有助於防止在未經許可的路線上非法傾倒垃圾。身分驗證和居住證明檢查也堵住了先前允許承包商非法傾倒垃圾的漏洞。地方服務的更新,例如每次收集的垃圾量限制和分類規則,使現場操作與處理需求相匹配,中轉站的處理能力也不斷提高。當預約系統和公共垃圾收集中心的規則得到有效溝通時,錯過收集的情況就會減少,客戶體驗會得到改善,送來的廢棄物品質也會更加穩定,從而使大件廢棄物收集服務市場受益。在法規允許的範圍內,引入與預訂時段和離峰時段獎勵掛鉤的價格訊號,可以進一步平滑需求,從而提高航線生產力和資產利用效率。

區域分析

2025年,北美市場佔據主導地位,佔大型廢棄物收集服務市場佔有率的35.70%。這得益於家具的穩定週轉以及多個州對床墊和家具回收津貼的生產者延伸責任制(EPR)措施的成熟。 2025年和2026年報告顯示,企業在可再生天然氣、聚合物和電氣化領域的投資表明,企業持續專注於價值回收,以補充常規和按需大件廢棄物收集服務。隨著市政當局收緊品質標準並將數位化報告引入路邊垃圾收集項目,整合下游資產的營運商可以在合規性和經濟效益方面脫穎而出。加拿大和墨西哥的大件廢棄物收集服務市場也面臨制度化趨勢,但由於執法能力不平衡,非正規活動仍是一個不利因素。在該地區,路線密度和人力資源供應仍然是獲得多年合約的關鍵因素,尤其是在存在季節性大件廢棄物高峰的大都會圈。

歐洲的政策協調正在重塑垃圾收集的經濟模式和實施機制。 2025年10月,歐盟修訂後的《廢棄物框架指令》生效,強制要求紡織品和鞋類實施生產者延伸責任制(EPR)。該指令還強調了危險物質的單獨收集,並設定了減少食物廢棄物的目標。這些變更擴大了公共專案管理的材料範圍,並提高了對可追溯路線管理和分類的需求。法國的公共收集點網路已成為一個成熟的機制典範,在該機制中,公民和承包商引導大宗廢棄物通過正規路線,這反映了掩埋法規和專案設計對使用者行為的影響。英國地方政府關於廢棄物收集和非法傾倒的數據凸顯了法規對於保護合規企業和維持資源回收目標進展的重要性。隨著跨境廢棄物運輸法規數位追蹤技術的進步以及成員國對紡織品生產者延伸責任制(EPR)的實施,企業正面臨新的物流要求,這些要求有利於那些擁有強大系統整合能力的公司。因此,歐洲重型廢棄物收集服務市場正在整合路線規劃、公共中心門禁和預約系統,以確保分類和收集設施的順利交接和可靠的處理能力。

亞太地區預計將成為成長最快的地區,到2031年複合年成長率將達到6.52%。印度的全國性數位化廢棄物追蹤計畫以及近期對建築和拆除廢棄物相關法規的修訂表明,垃圾處理正朝著正規化收集和可追溯性方向發展,從而將更多大件廢棄物納入規範的收集管道。隨著該地區主要城市擴大路邊收集和預約模式,政策制定者正優先考慮品質和安全標準,這將需要部署更多訓練有素的工作人員和現代化車輛。在東南亞和非洲部分地區,尤其是在大件廢棄物,加強執法和提高公眾意識對於減少垃圾流向非正規管道和提高服務普及率至關重要。撒哈拉以南非洲的學術研究表明,家庭垃圾分類法規的遵守取決於清晰的宣傳和持續的執法,這兩點都直接影響著大件廢棄物進入正規收集管道。隨著各國政府實施綜合系統並加強監管,大件廢棄物收集服務市場將受益於正規參與度的提高和更穩定的處理流程。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 都市化與一般廢棄物產生量之間的關係

- 政府對廢棄物管理有嚴格的規定

- 消費者環保意識日益增強

- 建築和拆除活動增加

- 智慧城市計畫和數位基礎設施發展

- 電子商務的擴張和家具更換趨勢

- 市場限制因素

- 缺乏標準化的廢棄物分類方法

- 農村和發展中地區意識水平低

- 熟練勞動力和專用設備短缺

- 非正規部門非法傾銷和競爭的氾濫

- 價值供應鏈分析

- 收款計劃系統

- 路徑最佳化方法

- 分銷和物流框架

- 監理情勢

- 技術展望

- 波特五力模型

- 人工智慧驅動的生成式廢棄物收集對服務供應商收入成長的影響

第5章 市場規模及成長預測(價值:美元,數量:噸)

- 按集合模型

- 路邊

- 一經請求

- 混合

- B2B合約

- 其他

- 來源

- 住宅

- 商業的

- 產業

- 市政當局/政府

- 其他用途(宗教場所、臨時災難避難所、電影和電視拍攝場地)

- 廢棄物類型

- 家具和室內裝飾

- 金屬和廢料

- 白色家電/家用電器

- 建設與拆除

- 其他(活動相關廢棄物、醫療/設施相關廢棄物)

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 東南亞(新加坡、馬來西亞、泰國、印尼、越南、菲律賓)

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 南非

- 奈及利亞

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- Partnership Model Benchmarking

- 策略趨勢

- 市佔率分析

- 公司簡介

- Waste Management, Inc.

- Republic Services, Inc.

- Veolia Environnement SA

- SUEZ SA

- Biffa plc

- Clean Harbors, Inc.

- Stericycle, Inc.

- Remondis SE & Co. KG

- Casella Waste Systems, Inc.

- GFL Environmental Inc.

- Waste Connections, Inc.

- Rumpke Waste & Recycling

- Recology Inc

- ALBA Group

- Van Gansewinkel

- PreZero

- Junk King

- LoadUp Technologies

- Renewi plc

- EnviroServ Holdings

第7章 市場機會與未來展望

According to Mordor Intelligence, the bulky waste collection service market size is expected to grow from USD 28.30 billion in 2025 to USD 30.30 billion in 2026 and is forecast to reach USD 40.70 billion by 2031 at 6.10% CAGR over 2026-2031.

This report is Segmented by Waste Type (Furniture & Upholstery, Metal & Scrap Items, and More), by Source (Residential, Commercial, and More), by Collection Model (Curbside, On-Demand, and More), and by Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD Billion) and Volume (Tons).

Global Bulky Waste Collection Service Market Trends and Insights

Rising Urbanization and Municipal Solid Waste Generation

Rapid urban concentration continues to elevate bulky streams such as furniture, appliances, and renovation debris. Global waste volumes are projected to increase from 2.1 billion tonnes in 2023 to 3.8 billion tonnes by 2050, intensifying pressure on city systems that are already short of transfer capacity and specialized handling for oversized items. In lower-income settings, uncollected and mismanaged waste remains a structural barrier to formal capture, creating a long pipeline of latent demand as fiscal capacity, donor programs, and infrastructure financing close service gaps over time. Local authority data in England showed 25.2 million tonnes of waste collected in 2024-2025, indicating steady volumes that underscore the importance of dedicated solutions for oversized fractions that cannot be containerized. As urbanization advances, the bulky waste collection service market benefits from predictable replacement cycles and renovation activity in multi-family housing, which concentrates demand into municipal cores. The bulky waste collection service market also benefits from rising public expectations for safe, convenient removal, which steers users toward formal providers

Stringent Government Regulations on Waste Management

Policy tightening across leading jurisdictions is increasing traceability and diversion obligations, which drives the adoption of certified collection and sorting capabilities. In the European Union, the revised Waste Framework Directive entered into force on October 16, 2025, and requires Member States to establish Extended Producer Responsibility for textiles and footwear within 30 months, introducing new funding and operational flows to expand formal collection of the difficult, bulky fraction. England has increased funding for waste crime enforcement and is scaling tools such as drone surveillance and automatic number plate recognition to deter illegal operators that undercut compliant service. Regulatory emphasis on separate collection, eco-modulated fees, and pre-shipment sorting for exports is moving the system toward verifiable recovery rates, favoring operators with audit-ready digital records and robust quality control. India has codified updated construction and demolition requirements. It is rolling out national waste tracking, signaling a transition from voluntary practices to mandatory performance that expands demand for specialized bulky pick-ups and documented processing. The bulky waste collection service market is responding through compliance-led bids and partnerships that build capacity for regulated streams.

Prevalence of Illegal Dumping and Informal Sector Competition

Illegal disposal continues to divert material away from formal providers and imposes cleanup costs on local authorities. England recorded 1.26 million fly-tipping incidents in 2024-2025, with a significant share occurring on highways, and a measured public-sector spend to clear larger loads, which directly erodes the economics of compliant service models. Enforcement agencies have disrupted illegal exports and identified numerous unlicensed sites, but case volumes remain high relative to investigative capacity, indicating a persistent gap that sustains shadow activity. Waste crime is also a macroeconomic drag, with estimated multi-hundred-million-pound annual costs in the United Kingdom, which undermine investment in compliant networks and lower formal capture rates where cheap, illegal options persist. The bulky waste collection service market faces higher customer acquisition costs when enforcement is inconsistent, as households and small businesses weigh convenience and perceived risk when choosing between formal and informal channels. As digital waste tracking and targeted enforcement scale, leakage risks can recede, but near-term variability still complicates planning and utilization. Operator strategies in exposed geographies, therefore, depend on close coordination with municipalities to align communications, fee structures, and service windows with local enforcement rhythms.

Other drivers and restraints analyzed in the detailed report include:

- Smart City Initiatives and Digital Infrastructure Development

- Increase in Construction and Demolition Activities

- Shortage of Trained Workforce and Specialized Equipment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Curbside service accounted for 49.21% of the bulky waste collection market share in 2025, as long-standing municipal agreements maintained predictable, scheduled routes. On-demand formats are projected to grow faster, at a 6.71% CAGR through 2031, as app-based scheduling, IoT-enabled route optimization, and electrified fleets lower marginal pickup costs and improve service windows. Republic Services' 2025 and 2026 investments in electric collection vehicles, renewable natural gas projects, and polymer processing demonstrate how downstream integration can offset collection volatility and enhance service proposals in municipal tenders. SUEZ's WasteConnect and AutoDiag deployments demonstrate how connected containers, live quality monitoring, and flow analytics can increase route density and reduce contamination, which is critical for ad hoc operations. These bulky pickups vary widely in composition. The bulky waste collection service market is thus converging on hybrid operations that blend base-route efficiency with flexible capacity for same-day or next-day requests.

Public center policies reinforce this hybridization. The Aix-Marseille-Provence area revised access rules and daily limits for public drop-off centers in 2025 to standardize services and enhance valuation, thereby advancing diversion goals and reducing strain on curbside systems during seasonal peaks. In Germany, projects like Oberhavel's free bulky waste delivery window for residents complement traditional curbside pickups and help divert volumes from unauthorized channels, while identity checks and residency proof close loopholes that previously allowed professional dumping. Local service updates, including per-collection volume caps and separate placement rules, continue to align field operations with processing needs and improve throughput at transfer sites. The bulky waste collection service market benefits when appointment systems and public center rules are well communicated, as they reduce missed collections, enhance the customer experience, and stabilize inbound quality. Price signals tied to appointment slots and off-peak incentives can further smooth demand, where regulations allow, thereby improving route productivity and asset utilization.

Geography Analysis

North America led with 35.70% of the bulky waste collection service market share in 2025, supported by steady furniture turnover and maturing Extended Producer Responsibility measures that subsidized mattress and furniture collection in several states. Reported company investments into renewable natural gas, polymers, and electrification in 2025 and 2026 indicate continued emphasis on value recovery that complements scheduled and on-demand bulky pickups. As municipalities tighten quality expectations and add digital reporting to curbside programs, operators with integrated downstream assets can differentiate on both compliance and economics. The bulky waste collection service market in Canada and Mexico is also navigating formalization trends, though informal activity remains a headwind due to uneven enforcement capacity. In this region, route density and workforce availability remain the decisive factors in securing multi-year contracts, particularly in large metropolitan areas with seasonal, bulky peaks.

Europe's policy harmonization is reshaping collection economics and execution. In October 2025, the EU's updated Waste Framework Directive came into effect, mandating Extended Producer Responsibility for textiles and footwear. The directive also emphasized the separate collection of hazardous materials and set targets for reducing food waste. These changes broadened the scope of materials managed under official programs, heightening the demand for traceable routing and sorting. France's public drop-off network serves as a mature template for how citizens and contractors route bulky items into formal channels, reflecting the impact of landfill restrictions and program design on user behavior. England's data on local authority-collected waste and fly-tipping underscores the importance of enforcement to protect compliant operators and maintain progress toward diversion goals. As digital tracking advances in cross-border waste shipment rules and Member States operationalize textile EPR schemes, operators see new logistics requirements that favor those with strong systems integration. The bulky waste collection service market in Europe is, therefore, aligning route planning with public center access controls and appointment systems to ensure smooth handoffs and reliable throughput at sorting and recovery sites.

Asia-Pacific is projected to be the fastest-growing region at a 6.52% CAGR through 2031. India's national digital waste-tracking program and recent updates to construction and demolition rules signal a shift toward formalized recovery and traceability, bringing more bulky loads into regulated channels. As major cities in the region scale curbside and appointment models for oversized items, policymakers are prioritizing quality and safety standards, which require better-trained crews and modernized fleets. In Southeast Asia and parts of Africa, improving enforcement and public education will be a prerequisite for reducing leakage into informal channels and increasing service penetration, especially for bulky waste. Academic work in Sub-Saharan Africa highlights that regulatory compliance with household segregation depends on clear communication and consistent enforcement, both of which directly affect routing bulky fractions toward formal collection. As governments roll out integrated systems and step up oversight, the bulky waste collection service market will benefit from broader formal participation and more stable processing flows.

- Waste Management, Inc.

- Republic Services, Inc.

- Veolia Environnement S.A.

- SUEZ S.A.

- Biffa plc

- Clean Harbors, Inc.

- Stericycle, Inc.

- Remondis SE & Co. KG

- Casella Waste Systems, Inc.

- GFL Environmental Inc.

- Waste Connections, Inc.

- Rumpke Waste & Recycling

- Recology Inc

- ALBA Group

- Van Gansewinkel

- PreZero

- Junk King

- LoadUp Technologies

- Renewi plc

- EnviroServ Holdings

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Urbanization and Municipal Solid Waste Generation

- 4.2.2 Stringent Government Regulations on Waste Management

- 4.2.3 Growing Environmental Consciousness Among Consumers

- 4.2.4 Increase in Construction and Demolition Activities

- 4.2.5 Smart City Initiatives and Digital Infrastructure Development

- 4.2.6 Expansion of E-Commerce and Furniture Replacement Trends

- 4.3 Market Restraints

- 4.3.1 Lack of Standardized Waste Segregation Practices

- 4.3.2 Limited Awareness in Rural and Developing Regions

- 4.3.3 Shortage of Trained Workforce and Specialized Equipment

- 4.3.4 Prevalence of Illegal Dumping and Informal Sector Competition

- 4.4 Value / Supply-Chain Analysis

- 4.4.1 Collection scheduling systems

- 4.4.2 Route optimization methods

- 4.4.3 Dispatch and logistics framework

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

- 4.8 Impact of GenAI-Powered Waste Collection on Service Providers' Revenue Growth

5 Market Size & Growth Forecasts (Value in USD & Volume in Tons)

- 5.1 By Collection Model

- 5.1.1 Curbside

- 5.1.2 On-Demand

- 5.1.3 Hybrid

- 5.1.4 Contracted B2B

- 5.1.5 Others

- 5.2 By Source

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.2.3 Industrial

- 5.2.4 Municipal/Government

- 5.2.5 Others (Religious Institutions, Temporary Disaster Relief Camps, Film/TV Production Sets)

- 5.3 By Waste Type

- 5.3.1 Furniture & Upholstery

- 5.3.2 Metal & Scrap Items

- 5.3.3 White Goods/Appliances

- 5.3.4 Construction & Demolition

- 5.3.5 Others (Event-specific Waste, Biomedical/Institutional)

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.4.3.7 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Turkey

- 5.4.5.4 South Africa

- 5.4.5.5 Nigeria

- 5.4.5.6 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Partnership Model Benchmarking

- 6.3 Strategic Moves

- 6.4 Market Share Analysis

- 6.5 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)}

- 6.5.1 Waste Management, Inc.

- 6.5.2 Republic Services, Inc.

- 6.5.3 Veolia Environnement S.A.

- 6.5.4 SUEZ S.A.

- 6.5.5 Biffa plc

- 6.5.6 Clean Harbors, Inc.

- 6.5.7 Stericycle, Inc.

- 6.5.8 Remondis SE & Co. KG

- 6.5.9 Casella Waste Systems, Inc.

- 6.5.10 GFL Environmental Inc.

- 6.5.11 Waste Connections, Inc.

- 6.5.12 Rumpke Waste & Recycling

- 6.5.13 Recology Inc

- 6.5.14 ALBA Group

- 6.5.15 Van Gansewinkel

- 6.5.16 PreZero

- 6.5.17 Junk King

- 6.5.18 LoadUp Technologies

- 6.5.19 Renewi plc

- 6.5.20 EnviroServ Holdings

7 Market Opportunities & Future Outlook

- 7.1 Smart Cities & IoT Integration

- 7.2 Producer Responsibility Expansion

- 7.3 Key Investment Strategies

分散式回收系統市場預測至2034年-按系統類型、材料、處理能力、經營模式、技術、最終用戶和地區分類的全球分析

分散式回收系統市場預測至2034年-按系統類型、材料、處理能力、經營模式、技術、最終用戶和地區分類的全球分析 德國大型廢棄物收集服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)日本大型垃圾收集服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)歐洲大型廢棄物收集服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

德國大型廢棄物收集服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)日本大型垃圾收集服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)歐洲大型廢棄物收集服務:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 智慧廢棄物收集技術市場:按技術、組件、廢棄物類型和最終用戶分類-2026-2032年全球市場預測自動化垃圾收集系統市場:按組件、系統類型、最終用戶和垃圾類型分類-2026-2032年全球市場預測氣動廢棄物收集系統市場:按系統類型、組件、廢棄物類型、安裝方式、應用和銷售管道,全球預測,2026-2032年

智慧廢棄物收集技術市場:按技術、組件、廢棄物類型和最終用戶分類-2026-2032年全球市場預測自動化垃圾收集系統市場:按組件、系統類型、最終用戶和垃圾類型分類-2026-2032年全球市場預測氣動廢棄物收集系統市場:按系統類型、組件、廢棄物類型、安裝方式、應用和銷售管道,全球預測,2026-2032年 自動化廢棄物收集系統市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、營運方式、應用、地區和競爭格局分類,2021-2031年

自動化廢棄物收集系統市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、營運方式、應用、地區和競爭格局分類,2021-2031年 2026-2030年全球自動化廢棄物收集系統市場2032 年自動廢棄物分類和回收系統市場預測:按組件、廢棄物分類類型、技術、最終用戶和地區進行的全球分析

2026-2030年全球自動化廢棄物收集系統市場2032 年自動廢棄物分類和回收系統市場預測:按組件、廢棄物分類類型、技術、最終用戶和地區進行的全球分析