|

市場調查報告書

商品編碼

2063640

亞太地區加工中心:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Asia-Pacific Machining Centers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

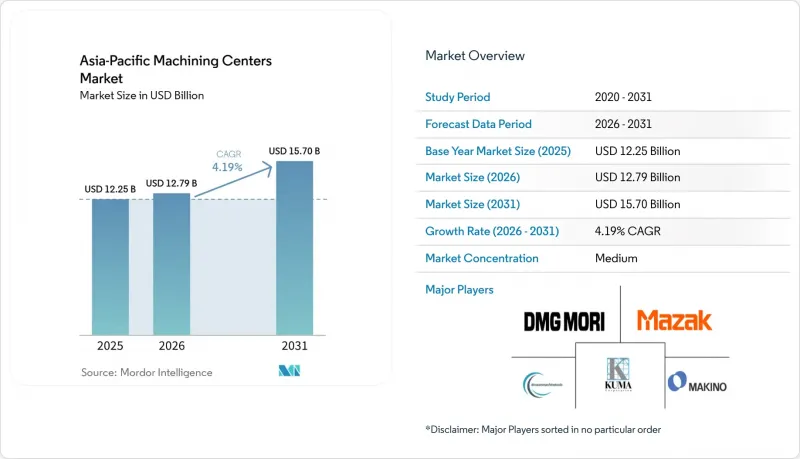

據 Mordor Intelligence 稱,亞太地區加工中心市場在 2025 年的價值為 122.5 億美元,預計到 2031 年將達到 157 億美元,而 2026 年為 127.9 億美元,預測期(2026-2031 年)的複合成長率為 4.19%。

本報告按工具機類型(例如,水平加工中心)、軸配置(3軸、4軸、5軸或更多軸)、主軸方向(水平、其他)、結構類型(立柱式、龍門式、行動工作台式)、最終用戶行業(汽車、其他)和國家/地區(中國、其他)進行細分。市場預測以美元計價。

亞太地區加工中心市場的趨勢與洞察

亞太地區電子製造業的復甦正加速精密加工的需求。

隨著電子組裝和印刷基板製造商業務多元化,新生產線的建立推動了對精密銑削和車削設備的需求,這些設備用於製造關鍵的模具、夾具和沖模。在越南,三星的六大製造地以及北部省份強大的蘋果供應商群聚構成了一個重要的電子製造中心,共同推動了緊湊型立式加工中心當前和未來的訂單成長。同時,在印度,作為不斷擴展的高科技供應鏈的一部分,位於清奈的一家投資3000萬美元的鋁製機殼製造廠(目標月產量為120萬件)凸顯了對高柔軟性加工單元日益成長的需求。在更南方的泰國,投資促進委員會已批准到2025年在電子和消費電子領域投資總計89.1億美元。這項投資熱潮將高度依賴高速主軸平台來適應先進的連接器加工工具。總體而言,採購趨勢正從傳統的大規模生產轉向多品種、小批量生產,這將進一步加速區域加工中心市場的發展。由於獲得 ISO 9001 品質認證是進入這些盈利的高科技供應鏈的必要條件,即使是中型機械製造商也被迫升級其過時的設備。

從內燃機 (ICE) 到電動車 (EV) 的轉變正在推動汽車產業採用多軸動力傳動系統。

從內燃機到電池動力的轉變,使得許多傳統零件的需求減少,同時也催生了新的精密加工需求,例如馬達外殼、電池托盤和減速齒輪等零件需要進行五軸連動加工。 Uno Minda公司正在其位於浦那的工廠投資5,100萬美元,引進專門用於鋁製電池托盤的五軸加工單元,預計將於2026年開始投入生產。日本經濟產業省對先進五軸控制器的出口限制凸顯了這項技術的戰略價值。隨著電動車銷售的成長,亞太地區的加工中心市場也從中受益,供應商紛紛升級其三軸生產線,例如增加旋轉工作台或購買完整的多軸平台。此外,汽車行業為減輕電池的巨大重量而採用的大型鋁製結構件,也加速了對具有大加工範圍和高扭矩的多軸加工中心的需求。這種結構性轉變確保了一級供應商持續的資本投資,以確保盈利的長期電動車平台合約。

高額的初始資本支出(CAPEX)和較長的投資回收期限制了新的資本投資。

中檔五軸加工中心的售價可高達80萬美元,五年總擁有成本(包括安裝和刀具費用)通常超過120萬美元。越南和泰國的中小型企業淨利率低於8%,如果沒有政府聯合融資,很難獲得銀行貸款。目前,工具機製造商正在推廣模組化設計,讓買家先購買三軸機架,之後再添加旋轉工作台,將資本支出分攤到幾年內。在印度和印度尼西亞,租賃和基於主軸運作的收費模式正在興起,降低了准入門檻,但也增加了對供應商運轉率保證的依賴。在資金籌措環境改善之前,這些限制將對亞太地區的加工中心市場構成負擔,尤其是對二級供應商而言。

細分市場分析

2025年,立式加工中心將佔據亞太地區加工中心市場佔有率的38%。這是因為它們在加工常見的矩形零件(例如引擎缸體和模架)方面,每主軸小時成本最低。來自中國、印度和泰國經銷商的支持使得維護成本保持在較低水平,從而使代工製造商能夠快速提高產能。越南和馬來西亞的消費性電子產品訂單商也傾向於選擇垂直加工中心,因為它們安裝空間有限,並且能夠利用重力排放切屑,從而保持鋁製外殼的表面光潔度。此外,泰國47個電子產品專案也進一步推動了亞太地區加工中心市場的發展,其中許多專案都指定使用高速立式加工中心單元進行連接器加工。

亞太地區多功能加工中心市場預計將在2026年至2031年間以6.20%的複合年成長率成長,主要驅動力是買家為節省占地面積而將銑削和車削工序整合到加工中心中。 DMG Mori的NTX系列、ACCUWAY的銑削車削生產線以及通泰的三刀塔平台,使航太和醫療器材工廠能夠在一次裝夾中完成複雜零件的加工,從而減少高達40%的在製品。這些工具機需要操作人員精通兩種G程式碼,而東協地區此類人才稀缺,因此製造商紛紛提供模擬軟體和遠端支援服務包以加速市場推廣。汽車零件供應商對集粗加工、精加工和探針測量於一體的多功能加工中心的需求不斷成長,也進一步推動了市場成長。

三軸加工系統能夠在確保大多數鋼鋁零件加工精度的前提下,簡化編程,預計到2025年將佔據亞太地區加工中心市場46%的佔有率。汽車和消費電子產業的二級供應商依靠這些設備,在操作人員培訓需求極低的情況下,也能按時完成訂單。此外,中國和印度的翻新商以新機60%的價格供應二手三軸設備,進一步擴大了其市場覆蓋範圍。

五軸平台預計到2031年將以6.80%的複合年成長率成長,這反映了市場對渦輪葉片、航太支架和電動汽車馬達外殼等需要同時進行輪廓加工的零件的需求。湯本馬達(Yumoto Denki)的32托盤自動化單元目前已實現五軸機床18小時無人值守運作,這表明透過先進的設定可以提高生產效率。日本對精度低於3微米的設備實施出口限制,促使企業加強本地採購,並將技術支援和培訓集中在日本、韓國和台灣地區。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電子製造業回歸亞太地區,加速了精密加工的需求。

- 動力傳動系統從內燃機 (ICE) 向電動車 (EV) 的轉變正在推動汽車產業採用多軸加工技術。

- 中國、日本和韓國對智慧工廠的激勵措施正在促進對CNC自動化領域的投資。

- 亞太地區的航太創業公司對先進精密加工技術的需求日益成長。

- 中國和新加坡的「暗工廠」擴張正在推動自動化加工中心的普及。

- 印度鈦植入製造的擴張增加了對高精度加工的需求。

- 市場限制因素

- 高昂的初始投資成本和較長的投資回收期阻礙了新的資本投資。

- 東協地區技術純熟勞工短缺,阻礙了加工中心的運轉率。

- 半導體設備投資的波動會擾亂工具機。

- 在日本,市場成長正在放緩,因為人們更傾向於維修現有設備而不是購買新機器。

- 價值/供應鏈分析

- 監理情勢

- 技術展望

- 產業吸引力—五力分析

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 按機器類型

- 臥式加工中心(HMC)

- 立式加工中心(VMC)

- 通用/五軸加工中心

- 多功能加工中心(MTM)

- 其他(龍門/橋式加工中心、車銑複合機床)

- 按軸配置

- 3軸

- 四軸

- 5個或更多軸

- 通過主軸的方位

- 橫版

- 垂直的

- 多軸

- 依結構類型

- 列類型

- 龍門式

- 移動桌類型

- 按最終用戶行業分類

- 車

- 航太/國防

- 能源(石油和天然氣、可再生能源)

- 醫療器材

- 模具製造

- 其他行業(一般製造業、合約製造業、電子產品等)

- 國家

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 其他亞太國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Yamazaki Mazak Corporation

- DMG Mori Co., Ltd.

- Okuma Corporation

- Makino Milling Machine Co., Ltd.

- Doosan Machine Tools Co., Ltd.

- Hyundai WIA Corporation

- Haas Automation, Inc.

- JTEKT Corporation

- Fanuc Corporation

- Fair Friend Group

- Hurco Companies, Inc.

- MHI Machine Tool Co., Ltd.

- Chongqing Machine Tool Co., Ltd.

- Guangdong Taikan NC Machine Co., Ltd.

- Dalian Machine Tool Group

- Brother Industries, Ltd.

- Kiwa Japan Co., Ltd.

- Hwacheon Machine Tools Co., Ltd.

- Ace Micromatic Group

- Shanghai THREEGUN Machine Tool Co., Ltd.

- Shenyang Machine Tool Co., Ltd.

- Nidec Machine Tool Corporation

- Sodick Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the asia-Pacific machining centers market size was valued at USD 12.25 billion in 2025 and is estimated to grow from USD 12.79 billion in 2026 to reach USD 15.70 billion by 2031, at a CAGR of 4.19% during the forecast period (2026-2031).

This report is Segmented by Machine Type (Horizontal Machining Centers, and More), by Axis Configuration (3-Axis, 4-Axis, 5-Axis & Above), by Spindle Orientation (Horizontal, and More), by Structure Type (Column-Type, Gantry-Type, and Moving-Table), by End-User Industry (Automotive, and More), and by Country (China, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Machining Centers Market Trends and Insights

Electronics Manufacturing Reshoring in Asia-Pacific Accelerates Precision Machining Demand

As electronics assemblers and printed circuit board manufacturers diversify their geographic footprints, the establishment of new production lines is driving the need for precision milling and turning equipment to produce essential molds, jigs, and dies. In Vietnam, Samsung's six major manufacturing complexes and the robust Apple supplier corridors in the northern provinces have established a dominant electronics manufacturing hub, collectively boosting current and forward-looking orders for compact vertical machining centers. Meanwhile, India's expanding tech supply chain saw the addition of a USD 30 million aluminum-housing facility in Chennai, designed to produce 1.2 million units per month, underscoring the growing need for flexible machining cells. Further south, Thailand's Board of Investment approved a total of USD 8.91 billion in electronics and electrical appliance investments for 2025. This surge will heavily depend on high-speed spindle platforms for advanced connector tooling. Overall, procurement trends are shifting away from traditional mass production toward high-mix, small-batch capabilities, further accelerating the regional machining centers market. Because mandatory ISO 9001 quality audits are required to enter these lucrative tech supply chains, even mid-tier machine shops are being compelled to upgrade their legacy equipment.

Internal Combustion Engine (ICE)-to-Electric Vehicle (EV) Powertrain Shift Drives Multi-Axis Machining Adoption Across Automotive Sector

Shifting from internal-combustion engines to battery power removes many legacy parts yet introduces new precision needs for motor housings, battery trays, and reduction gears that call for simultaneous five-axis cutting. Uno Minda invested USD 51 million in its Pune plant to install 5-axis cells dedicated to aluminum battery trays, with production slated for 2026. Japan's trade ministry's export controls on advanced five-axis controllers underscore the technology's strategic value. As EV volumes rise, the Asia-Pacific machining centers market benefits as suppliers either upgrade three-axis lines with rotary tables or buy full multi-axis platforms. Furthermore, the automotive push to offset the massive weight of batteries with large-scale aluminum structural castings is accelerating demand for large-envelope, high-torque multi-axis centers. This structural shift ensures sustained capital expenditure from Tier 1 suppliers eager to secure lucrative, long-term EV platform contracts.

High Upfront Capital Expenditure (CAPEX) and Long Payback Periods Limit New Equipment Investments

A mid-range five-axis machining center can cost up to USD 800,000, while total ownership over five years often exceeds USD 1.2 million, including installation and tooling. Small firms in Vietnam and Thailand run on net margins below 8% and struggle to secure bank financing without state co-investment. Machine builders now push modular designs so buyers can start with a three-axis frame and bolt on rotary tables later, spreading cash outlay across several years. Leasing and pay-per-spindle-hour models are emerging in India and Indonesia, lowering barriers yet creating dependence on vendor uptime guarantees. Until financing terms ease, this restraint will weigh on the Asia-Pacific machining centers market, especially among tier-2 suppliers.

Other drivers and restraints analyzed in the detailed report include:

- Smart Factory Incentives in China Japan and South Korea Boost Computer Numerical Control (CNC) Automation Investments

- Dark Factory Expansion in China and Singapore Drives Automated Machining Center Deployment

- Skilled Labor Shortages Across ASEAN Hinder Machining Center Utilization

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Vertical machining centers accounted for 38% of the Asia-Pacific machining centers market share in 2025 because they cut common prismatic parts such as engine blocks and mold bases at the lowest cost per spindle hour. Widespread dealer support across China, India, and Thailand keeps maintenance costs low and lets job shops add capacity quickly. Orders from consumer-electronics suppliers in Vietnam and Malaysia also favor vertical formats that fit tight floor plans and evacuate chips by gravity, preserving surface finish on aluminum housings. The Asia-Pacific machining centers market gains additional pull from Thailand's 47 electronics projects, many of which specify high-speed VMC cells for connector tooling.

The Asia-Pacific machining centers market size for multi-tasking machining centers is projected to expand at a 6.20% CAGR between 2026 and 2031 as buyers consolidate milling and turning to save floor space. DMG Mori's NTX series, ACCUWAY turn-mill lines, and Tongtai's three-turret platform enable aerospace and medical shops to finish complex parts in a single setup, reducing work-in-process by up to 40%. These machines demand operators fluent in both G-code families, which is scarce across ASEAN, so builders bundle simulation software and remote support to speed adoption. As automotive suppliers retool for electric-vehicle battery trays, they increasingly specify multi-tasking capability to combine roughing, finishing, and probing on the same platform, reinforcing the growth trajectory.

Three-axis systems held 46% of the Asia-Pacific machining centers market share in 2025 because they achieve tolerances acceptable for most steel and aluminum parts while keeping programming simple. Tier-2 automotive and appliance vendors rely on these machines to meet short delivery windows with minimal operator training. Chinese and Indian refurbishers also supply used three-axis units at 60% of new-machine prices, further extending their footprint.

Five-axis platforms are advancing at a 6.80% CAGR through 2031, reflecting demand for turbine blades, aerospace brackets, and electric-vehicle motor housings that require simultaneous contouring. Yumoto Denki's 32-pallet automated cell now runs five-axis machines 18 hours unattended, proving the productivity boost achievable with advanced setups. Export controls on sub-3-micron accuracy units from Japan reinforce regional sourcing, concentrating technical support and training in Japan, South Korea, and Taiwan.

List of Companies Covered in this Report:

- Yamazaki Mazak Corporation

- DMG Mori Co., Ltd.

- Okuma Corporation

- Makino Milling Machine Co., Ltd.

- Doosan Machine Tools Co., Ltd.

- Hyundai WIA Corporation

- Haas Automation, Inc.

- JTEKT Corporation

- Fanuc Corporation

- Fair Friend Group

- Hurco Companies, Inc.

- MHI Machine Tool Co., Ltd.

- Chongqing Machine Tool Co., Ltd.

- Guangdong Taikan NC Machine Co., Ltd.

- Dalian Machine Tool Group

- Brother Industries, Ltd.

- Kiwa Japan Co., Ltd.

- Hwacheon Machine Tools Co., Ltd.

- Ace Micromatic Group

- Shanghai THREEGUN Machine Tool Co., Ltd.

- Shenyang Machine Tool Co., Ltd.

- Nidec Machine Tool Corporation

- Sodick Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Electronics manufacturing reshoring in Asia-Pacific accelerates precision machining demand

- 4.2.2 ICE-to-EV powertrain shift drives multi-axis machining adoption across automotive sector

- 4.2.3 Smart factory incentives in China, Japan, and South Korea boost CNC automation investments

- 4.2.4 Asia-Pacific space start-ups increase demand for advanced precision machining capabilities

- 4.2.5 Dark factory expansion in China and Singapore drives automated machining center deployment

- 4.2.6 Titanium implant manufacturing growth in India raises need for high-precision machining

- 4.3 Market Restraints

- 4.3.1 High upfront CAPEX and long payback periods limit new equipment investments

- 4.3.2 Skilled labor shortages across ASEAN hinder machining center utilization

- 4.3.3 Semiconductor capex volatility disrupts machining equipment demand cycles

- 4.3.4 Retrofit preference over new machine purchases in Japan slows market growth

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Machine Type

- 5.1.1 Horizontal Machining Centers (HMC)

- 5.1.2 Vertical Machining Centers (VMC)

- 5.1.3 Universal/5-Axis Machining Centers

- 5.1.4 Multi-Tasking Machining Centers (MTM)

- 5.1.5 Others (Gantry/Bridge-Type Centers, Turn-Mill Centers)

- 5.2 By Axis Configuration

- 5.2.1 3-Axis

- 5.2.2 4-Axis

- 5.2.3 5-Axis & Above

- 5.3 By Spindle Orientation

- 5.3.1 Horizontal

- 5.3.2 Vertical

- 5.3.3 Multi-spindle

- 5.4 By Structure Type

- 5.4.1 Column-Type

- 5.4.2 Gantry-Type

- 5.4.3 Moving-Table

- 5.5 By End-User Industry

- 5.5.1 Automotive

- 5.5.2 Aerospace & Defense

- 5.5.3 Energy (Oil-Gas, Renewables)

- 5.5.4 Medical Devices

- 5.5.5 Mold and Die Manufacturing

- 5.5.6 Others (General Manufacturing, Job Shops, Electronics, etc.)

- 5.6 By Country

- 5.6.1 China

- 5.6.2 Japan

- 5.6.3 India

- 5.6.4 Australia

- 5.6.5 South Korea

- 5.6.6 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Yamazaki Mazak Corporation

- 6.4.2 DMG Mori Co., Ltd.

- 6.4.3 Okuma Corporation

- 6.4.4 Makino Milling Machine Co., Ltd.

- 6.4.5 Doosan Machine Tools Co., Ltd.

- 6.4.6 Hyundai WIA Corporation

- 6.4.7 Haas Automation, Inc.

- 6.4.8 JTEKT Corporation

- 6.4.9 Fanuc Corporation

- 6.4.10 Fair Friend Group

- 6.4.11 Hurco Companies, Inc.

- 6.4.12 MHI Machine Tool Co., Ltd.

- 6.4.13 Chongqing Machine Tool Co., Ltd.

- 6.4.14 Guangdong Taikan NC Machine Co., Ltd.

- 6.4.15 Dalian Machine Tool Group

- 6.4.16 Brother Industries, Ltd.

- 6.4.17 Kiwa Japan Co., Ltd.

- 6.4.18 Hwacheon Machine Tools Co., Ltd.

- 6.4.19 Ace Micromatic Group

- 6.4.20 Shanghai THREEGUN Machine Tool Co., Ltd.

- 6.4.21 Shenyang Machine Tool Co., Ltd.

- 6.4.22 Nidec Machine Tool Corporation

- 6.4.23 Sodick Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

結構木螺絲全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)

結構木螺絲全球市場規模、佔有率、趨勢和成長分析報告(2026-2034) 全球木結構螺絲市場報告:2021-2032年歷史表現及預測

全球木結構螺絲市場報告:2021-2032年歷史表現及預測 結構木螺絲市場規模、佔有率和成長分析:按類型、材質、驅動系統、應用、通路和地區分類-2026-2033年產業預測

結構木螺絲市場規模、佔有率和成長分析:按類型、材質、驅動系統、應用、通路和地區分類-2026-2033年產業預測 銑床主軸市場機會、成長要素、產業趨勢分析及2026-2035年預測。

銑床主軸市場機會、成長要素、產業趨勢分析及2026-2035年預測。 歐洲加工中心:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)德國加工中心:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)加工中心:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

歐洲加工中心:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)德國加工中心:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)加工中心:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026年全球木結構螺絲市場報告

2026年全球木結構螺絲市場報告 加工中心市場:按類型、軸數、控制方式、應用和銷售管道分類-2026-2032年全球市場預測

加工中心市場:按類型、軸數、控制方式、應用和銷售管道分類-2026-2032年全球市場預測 車削中心,縱型加工中心,水平加工中心的全球市場(2025年)- 終端用戶,競爭企業:分析與預測

車削中心,縱型加工中心,水平加工中心的全球市場(2025年)- 終端用戶,競爭企業:分析與預測