|

市場調查報告書

商品編碼

2062065

加工中心:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Machining Centers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

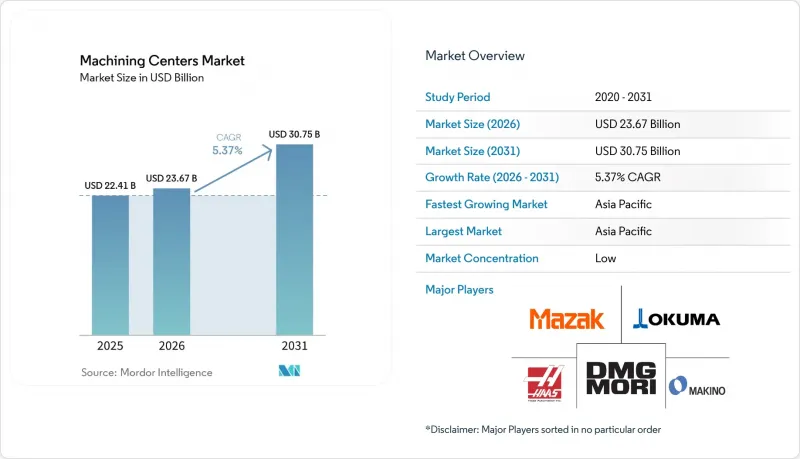

根據 Mordor Intelligence 預測,加工中心市場規模將從 2025 年的 224.1 億美元和 2026 年的 236.7 億美元成長到 2031 年的 307.5 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 5.37%。

本報告按工具機類型(例如,水平加工中心)、軸配置(例如,三軸)、主軸方向(例如,水平、垂直)、結構類型(例如,立柱式、龍門式)、終端用戶行業(例如,汽車、能源)和地區(例如,北美、歐洲)進行分類。市場預測以美元計價。

全球加工中心市場趨勢與洞察

擴大航太零件製造能力

航太計畫正進行多年產能投資,以推動對水平軸和五軸加工平台的需求。普惠公司已投資2億美元,用於擴建位於喬治亞州哥倫布喬治亞的工廠,計劃在2028年將壓縮機和渦輪盤的產量提高30%。這將直接影響齒輪傳動渦輪扇引擎(GTF)和F135引擎的生產速度,並推動對能夠加工鈦和鎳的五軸和大型水平加工生產線的需求。卡曼航太與防務公司計劃在鹽湖城新建一個自動化加工中心,預計於2026年第四季運作,屆時發射系統產量將翻兩番,固體火箭引擎噴嘴產量將翻倍。這將需要高通量金屬加工與自動化檢測相結合。Honeywell公司在堪薩斯州奧拉薩的擴建項目,將增強其在國內的航空電子設備和印刷基板組件製造能力,從而提升整個飛行系統價值鏈的本地精密製造水準。此次產能擴張需要多軸加工單元、自動化托盤和穩定的溫度控管,以在高進給速度和轉速下保持精度,這些都是北美和歐洲航太叢集的優先事項。這些投資的影響期為2-4年,與試運行、製程檢驗和量產準備工作相關,這將滿足加工中心市場的短期需求。

醫療設備製造中的精度要求

2026 年品管系統法規提高了醫療設備製造商的可追溯性和製程控制標準,增加了對亞微米級加工和進程內測量的需求。這些法規符合 ISO 原則,並修訂了 21 CFR 的多項條款,強化了依賴穩定加工製程的品質系統和文件。產能的提升也支持了這一趨勢,新的無塵室和受監管的生產環境正在建設中,以滿足醫療應用領域精密零件和組件的生產需求。對溫度補償、探測循環和數位雙胞胎檢驗的投資正在普及,以減少廢品,並透過一致且檢驗的加工結果確保通過審核。此因素在美國 FDA 的管轄範圍內最為顯著,並延伸至適用 CE 標誌的歐洲,同時也影響為跨國 OEM 提供服務的印度和東協地區的契約製造工廠。這種影響的 2-4 年時間與認證週期和設備前置作業時間相吻合,確保醫療產業的持續發展能夠支撐加工中心市場。

熟練的CNC操作員和程式設計人員短缺

對機械師和數控程式設計人員日益成長的需求正嚴重限制生產規模,限制工廠快速推出。業內人士估計,到2030年,隨著退休人數的增加,美國將面臨嚴重的勞動力短缺,而短期培訓週期不足以充分滿足多軸編程、設置和檢測所需的技能。熟練高級CAM技術需要數年時間,這與季度交付週期不符,並反覆造成自動化程序的瓶頸。大型製造商通常與高校合作並提供更高的薪資,這吸引了小規模代工製造商的人才,加劇了招募競爭。因此,昂貴的多軸設備的運轉率正在下降,而當團隊無法跨班次完成編程和設定工作時,流程整合的實施也會被延緩。這種限制在北美和歐洲最為嚴重,隨著自動化專案提高基本技能需求,這個問題正在蔓延到亞太地區,而這正是目前加工中心市場的瓶頸所在。

細分市場分析

截至2025年,立式加工中心佔據了加工中心市場47.68%的佔有率,但預計到2031年,通用加工中心和五軸加工中心將以6.12%的複合年成長率成長。立式加工中心憑藉其便捷的刀具更換、排放和符合人體工學的設計,在汽車行業的大批量生產和小規模加工車間中佔據主導地位。近期推出的垂直五軸加工中心具有更高的主軸轉速、更強的剛性和更全面的技術週期,從而擴展了單一平台上可加工的零件範圍。水平加工中心仍然是第二大市場佔有率,由於其適用於托盤式自動化和重型切削,因此在動力傳動系統、航太結構件和大型矩形零件的加工中備受青睞。集車削和銑削於一體的多功能工具機透過縮短設定週期、提高幾何精度和將加工流程整合到一台工具機的工作流程中,幫助工廠應對人手不足。

在多品種、小批量生產專案中,具備探針和刀具監控功能的五軸立式加工中心能夠實現零件系列的快速切換和污染控制,而與軟性生產系統整合的水平加工中心則可確保可預測的生產效率。 OEM 設計的變化,例如日益複雜的輪廓、更薄的壁厚以及更多一體成型零件,正在推動加工中心市場中通用工具機和五軸機床的成長。隨著數位雙胞胎檢驗和機上測量技術的進步,產品初始核准週期得以加快,而新型冷卻液管理系統則提高了刀具壽命和表面光潔度,預計未來還將有更多益處。在這樣的市場環境下,擁有更全面的自動化產品組合、針對不同材料範圍客製化的主軸選項以及可部署在其所有加工中心設備上的軟體套件的供應商將更具優勢。

區域分析

預計到2025年,亞太地區將佔全球消費量的54.69%,並在強勁的工業擴張和製造業進步的推動下,以7.12%的複合年成長率成長至2031年。中國持續擴大進出口,預計2025年上半年超越德國,佔全球工具機出口的19%。這反映了國內產能的不斷成長以及對高度精密系統的需求。進口主要主導日本、德國和台灣地區,凸顯了對先進水平工具機和五軸加工中心的持續依賴。同時,中國新建工廠正在擴大中高階產品的產能,進一步鞏固了該地區的製造業基礎。

印度正透過生產連結獎勵計畫計劃 (PLI) 和資本財項目等政策支持來鞏固其市場地位,這些計劃正在擴大精密製造的潛在市場。 「PLI Auto」計畫和已獲批准的資本財項目支援能力建設、卓越中心和測試基礎設施。這些政策支持,加上對技能發展的重視,正使印度得以進軍高附加價值零件和組裝。加之中國,這些趨勢正使亞太地區成為加工中心市場的主要成長引擎。

2025年,北美地區展現出強勁的成長勢頭,主要得益於航太、國防和汽車產業回歸美國。美國製造業技術訂單創歷史新高,顯示產能緊張,短期需求不斷成長。以德國和義大利為首的歐洲,繼續受益於其先進的工業基礎和永續發展主導的資本投資週期,產業結構調整也增強了原始設備製造商(OEM)的能力。中東和非洲地區正透過多元化和能源投資逐步擴張,但仍高度依賴工具機進口。總體而言,亞太地區是成長的基礎,而北美和歐洲則為高附加價值行業和受監管行業提供了穩定的需求。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 擴大航太零件製造能力

- 醫療設備製造中的精度要求

- 汽車動力系統的生產

- 新興市場模具產業的成長

- 對老舊工具機的更換需求

- OEM廠商外包契約製造

- 市場限制因素

- 對於小規模合約製造企業而言,資本投資的門檻相對較高。

- 熟練的CNC操作員和程式設計人員短缺

- 日本和德國製造商的前置作業時間很長。

- 經濟不確定性導致資本財。

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 產業吸引力—五力分析

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

- 向「機器即服務」融資模式轉型

- 汽車業對臥式加工中心的需求日益成長。

第5章 市場規模與成長預測

- 按機器類型

- 臥式加工中心(HMC)

- 立式加工中心(VMC)

- 通用/五軸加工中心

- 多工中心(MTM)

- 其他(龍門/橋式加工中心、車銑複合機床)

- 按軸配置

- 3軸

- 四軸

- 5個或更多軸

- 通過主軸的方位

- 水平的

- 垂直的

- 多軸

- 依結構類型

- 列類型

- 龍門式

- 移動桌類型

- 按最終用戶行業分類

- 車

- 航太/國防

- 能源(石油和天然氣、可再生能源)

- 醫療器材

- 模具製造

- 其他行業(一般製造業、合約製造業、電子產品等)

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 秘魯

- 其他南美國家

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 比荷盧經濟聯盟(比利時、荷蘭、盧森堡)

- 北歐國家(丹麥、芬蘭、冰島、挪威、瑞典)

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 東協(印尼、泰國、菲律賓、馬來西亞、越南)

- 其他亞太國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 科威特

- 土耳其

- 埃及

- 南非

- 奈及利亞

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- DMG MORI

- Yamazaki Mazak

- Okuma Corporation

- Haas Automation

- Makino Milling Machine

- Doosan Machine Tools

- GF Machining Solutions

- Hyundai WIA

- Hurco Companies

- Fives Group

- Hardinge Inc.

- Chiron Group

- Brother Industries

- Jingdiao Group

- JTEKT(Toyoda)

- Spinner Maschinenbau

- Kitamura Machinery

- Emco Group

- Sodick Co.

第7章 市場機會與未來展望

According to Mordor Intelligence, the machining centers market size is projected to expand from USD 22.41 billion in 2025 and USD 23.67 billion in 2026 to USD 30.75 billion by 2031, registering a CAGR of 5.37% between 2026 to 2031.

This report is Segmented by Machine Type (Horizontal Machining Centers, and More), by Axis Configuration (3-Axis, and More), by Spindle Orientation (Horizontal, Vertical, and More), by Structure Type (Column-Type, Gantry-Type, and More), by End-User Industry (Automotive, Energy, and More), and by Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Machining Centers Market Trends and Insights

Aerospace Component Manufacturing Capacity Expansion

Aerospace programs are moving ahead with multi-year capacity investments that lift demand for horizontal and 5-axis machining platforms. Pratt & Whitney committed USD 200 million to its Columbus, Georgia operations to increase compressor and turbine disk output by 30% by 2028, which ties directly to Geared Turbofan and F135 engine build rates and favors 5-axis and heavy-duty horizontal lines with titanium and nickel capability. Karman Space & Defense is quadrupling launch system production and doubling solid rocket motor nozzle output through a new automated machining hub in Salt Lake City that targets Q4 2026 readiness, which will require high-throughput metallic machining integrated with automated inspection. Honeywell's expansion in Olathe, Kansas, is building domestic electronics manufacturing depth for avionics and printed circuit board assemblies, reinforcing localized precision manufacturing across the flight systems value chain. Ramping such capacity requires multi-axis cells, pallet automation, and consistent thermal management to stabilize tolerance at higher feeds and speeds, which is a priority across North American and European aerospace clusters. These investments set up a 2 to 4 year impact window that aligns with commissioning, process validation, and rate readiness, which in turn underpins near term demand in the machining centers market.

Medical Device Manufacturing Precision Requirements

The 2026 Quality Management System Regulation raises the bar on traceability and process control for medical device manufacturers, which elevates the need for sub-micron machining and in-process gauging. The regulation aligns with ISO principles and updates scores of sections across 21 CFR, which solidifies quality systems and documentation that depend on stable machining processes. Capacity additions support the trend, with new cleanrooms and compliant production environments being installed to serve precision parts and assemblies for medical use cases. Investments in thermal compensation, probing cycles, and digital twin validation are spreading to reduce scrap and to pass audits with consistent, verifiable machining outcomes. This driver is strongest in the United States under FDA jurisdiction and extends to Europe under CE marking, with a growing effect in India and ASEAN contract manufacturing hubs that serve multinational OEMs. The 2 4-year impact timeline matches certification cycles and equipment lead times, which keeps the medical pipeline supportive for the machining centers market.

Skilled CNC Operator and Programmer Shortage

Open positions for machinists and CNC programmers continue to weigh on throughput, which limits how fast plants can ramp complex work. Industry sources estimate a significant gap through 2030 in the United States as retirements keep pace with demand, while short training cycles cannot fully cover the skills needed for multi-axis programming, setup, and inspection. Time to proficiency is measured in years for advanced CAM roles, which does not align with quarterly delivery cycles and creates recurring bottlenecks in light-out programs. Larger manufacturers often partner with technical colleges and offer higher wages, which can draw talent away from small job shops and intensify hiring friction. The net effect is idle time on expensive multi-axis assets and slower adoption of process consolidation when teams cannot support programming and setup across shifts. This restraint is most acute in North America and Europe and is spreading in APAC as automation projects raise the baseline skill requirements, which keeps this a near-term drag for the machining centers market.

Other drivers and restraints analyzed in the detailed report include:

- Electric Vehicle Powertrain Component Production

- Mold and Die Industry Growth in Emerging Markets

- Economic Uncertainty Delaying Capital Equipment Purchases

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Vertical machining centers held 47.68% of the machining centers market share in 2025, while universal and 5-axis machines are projected to expand at a 6.12% CAGR through 2031. Vertical configurations dominate high-volume work for automotive and job shop environments because tooling access, chip evacuation, and ergonomics support fast changeovers. Recent vertical 5-axis introductions also push higher spindle speeds, better rigidity, and more comprehensive technology cycles, which widens the set of parts that can be consolidated on a single platform. Horizontal machining centers remain the second largest category and are preferred for palletized automation and heavy cutting, which favors their use in powertrain, aerospace structural parts, and larger prismatic components. Multi-tasking centers that integrate turning and milling reduce setups, improve geometric integrity, and help plants cope with labor constraints by compressing process routes into single machine workflows.

In higher mix and lower volume programs, 5-axis verticals with probing and tool monitoring enable quick part family changeovers and contamination control, while horizontals tied to flexible manufacturing systems secure predictable throughput. OEM design changes that increase contour complexity, thin walls, and integrated features are a catalyst for universal and 5-axis upsizing within the machining centers market. Further gains are likely as digital twin validation and on-machine measurement accelerate first article approval cycles, and as new coolant management systems enhance tool life and surface finish. This mix favors suppliers with deeper automation portfolios, spindle options matched to material families, and software suites that can be deployed across fleets in the machining centers market.

Geography Analysis

Asia Pacific accounted for 54.69% of global consumption in 2025 and is projected to grow at a 7.12% CAGR through 2031, driven by strong industrial expansion and manufacturing depth. China continues to scale both imports and exports, surpassing Germany with a 19% share of global machine tool exports in H1 2025, reflecting rising domestic capabilities alongside demand for high-precision systems. Imports remain led by Japan, Germany, and Taiwan, highlighting continued reliance on advanced horizontals and 5-axis machines. At the same time, new plants in China are expanding mid- to high-end production capacity, reinforcing the region's manufacturing base.

India is strengthening its position through policy support such as Production Linked Incentive schemes and capital goods programs, which are expanding the addressable market for precision manufacturing. The PLI Auto scheme and sanctioned capital goods projects are supporting capability building, centers of excellence, and testing infrastructure. This policy push, combined with a focus on skill development, is enabling India to move into higher-value components and assemblies. Together with China, these trends position Asia Pacific as the primary growth engine for the machining centers market.

North America gained strong momentum in 2025, supported by aerospace, defense, and automotive reshoring, with record U.S. manufacturing technology orders signaling tight capacity and near-term demand. Europe, led by Germany and Italy, continues to benefit from a sophisticated industrial base and sustainability-driven capex cycles, while consolidation enhances OEM capabilities. The Middle East and Africa are gradually expanding through diversification and energy investments, though reliance on imported machine tools remains high. Overall, Asia Pacific anchors growth, while North America and Europe provide stable demand across high-value and regulated sectors.

- DMG MORI

- Yamazaki Mazak

- Okuma Corporation

- Haas Automation

- Makino Milling Machine

- Doosan Machine Tools

- GF Machining Solutions

- Hyundai WIA

- Hurco Companies

- Fives Group

- Hardinge Inc.

- Chiron Group

- Brother Industries

- Jingdiao Group

- JTEKT (Toyoda)

- Spinner Maschinenbau

- Kitamura Machinery

- Emco Group

- Sodick Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aerospace Component Manufacturing Capacity Expansion

- 4.2.2 Medical Device Manufacturing Precision Requirements

- 4.2.3 Electric Vehicle Powertrain Component Production

- 4.2.4 Mold and Die Industry Growth in Emerging Markets

- 4.2.5 Replacement Demand for Aging Machine Tool Fleets

- 4.2.6 Contract Manufacturing Outsourcing by OEMs

- 4.3 Market Restraints

- 4.3.1 High Capital Investment Barriers for Small Job Shops

- 4.3.2 Skilled CNC Operator and Programmer Shortage

- 4.3.3 Long Lead Times from Japanese and German Manufacturers

- 4.3.4 Economic Uncertainty Delaying Capital Equipment Purchases

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Shift Toward Machine-as-a-Service Financing Models

- 4.9 Growing Preference for Horizontal Machining Centers in Automotive

5 Market Size & Growth Forecasts (Value, In USD Billion)

- 5.1 By Machine Type

- 5.1.1 Horizontal Machining Centres (HMC)

- 5.1.2 Vertical Machining Centres (VMC)

- 5.1.3 Universal / 5-Axis Machining Centres

- 5.1.4 Multi-Tasking Machining Centers (MTM)

- 5.1.5 Others (Gantry / Bridge-Type Centres, Turn-Mill Centers)

- 5.2 By Axis Configuration

- 5.2.1 3-Axis

- 5.2.2 4-Axis

- 5.2.3 5-Axis & Above

- 5.3 By Spindle Orientation

- 5.3.1 Horizontal

- 5.3.2 Vertical

- 5.3.3 Multi-spindle

- 5.4 By Structure Type

- 5.4.1 Column-Type

- 5.4.2 Gantry-Type

- 5.4.3 Moving-Table

- 5.5 By End-User Industry

- 5.5.1 Automotive

- 5.5.2 Aerospace & Defense

- 5.5.3 Energy (Oil-Gas, Renewables)

- 5.5.4 Medical Devices

- 5.5.5 Mold and Die Manufacturing

- 5.5.6 Others (General Manfacturing, Job Shops, Electronics, etc.)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Peru

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.6.3.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.6.3.8 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 Australia

- 5.6.4.5 South Korea

- 5.6.4.6 ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam)

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Qatar

- 5.6.5.4 Kuwait

- 5.6.5.5 Turkey

- 5.6.5.6 Egypt

- 5.6.5.7 South Africa

- 5.6.5.8 Nigeria

- 5.6.5.9 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 DMG MORI

- 6.4.2 Yamazaki Mazak

- 6.4.3 Okuma Corporation

- 6.4.4 Haas Automation

- 6.4.5 Makino Milling Machine

- 6.4.6 Doosan Machine Tools

- 6.4.7 GF Machining Solutions

- 6.4.8 Hyundai WIA

- 6.4.9 Hurco Companies

- 6.4.10 Fives Group

- 6.4.11 Hardinge Inc.

- 6.4.12 Chiron Group

- 6.4.13 Brother Industries

- 6.4.14 Jingdiao Group

- 6.4.15 JTEKT (Toyoda)

- 6.4.16 Spinner Maschinenbau

- 6.4.17 Kitamura Machinery

- 6.4.18 Emco Group

- 6.4.19 Sodick Co.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

結構木螺絲全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)

結構木螺絲全球市場規模、佔有率、趨勢和成長分析報告(2026-2034) 全球木結構螺絲市場報告:2021-2032年歷史表現及預測

全球木結構螺絲市場報告:2021-2032年歷史表現及預測 結構木螺絲市場規模、佔有率和成長分析:按類型、材質、驅動系統、應用、通路和地區分類-2026-2033年產業預測

結構木螺絲市場規模、佔有率和成長分析:按類型、材質、驅動系統、應用、通路和地區分類-2026-2033年產業預測 銑床主軸市場機會、成長要素、產業趨勢分析及2026-2035年預測。

銑床主軸市場機會、成長要素、產業趨勢分析及2026-2035年預測。 歐洲加工中心:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)亞太地區加工中心:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)德國加工中心:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

歐洲加工中心:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)亞太地區加工中心:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)德國加工中心:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 2026年全球木結構螺絲市場報告

2026年全球木結構螺絲市場報告 加工中心市場:按類型、軸數、控制方式、應用和銷售管道分類-2026-2032年全球市場預測

加工中心市場:按類型、軸數、控制方式、應用和銷售管道分類-2026-2032年全球市場預測 車削中心,縱型加工中心,水平加工中心的全球市場(2025年)- 終端用戶,競爭企業:分析與預測

車削中心,縱型加工中心,水平加工中心的全球市場(2025年)- 終端用戶,競爭企業:分析與預測