|

市場調查報告書

商品編碼

2063627

醫療設備用熱可塑性橡膠:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年)Thermoplastic Elastomers In Medical Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

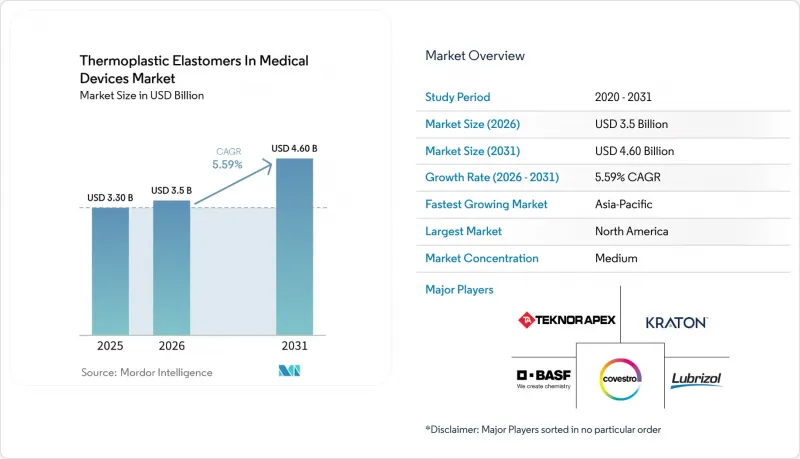

據 Mordor Intelligence 稱,2025 年醫療設備用熱可塑性橡膠市值為 33 億美元,預計到 2031 年將從 2026 年的 35 億美元成長至 46 億美元,預測期(2026-2031 年)複合年成長率為 5.59%。

本報告材料類型(熱可塑性橡膠- 苯乙烯基/苯乙烯-乙烯-丁烯-苯乙烯 (TPE-S/SEBS) 等)、應用(導管、管材等)、加工技術(擠出成型、射出成型成型、吹塑成型成型、薄膜成型等)和地區(北美、歐洲等)進行細分。市場預測以美元計價。

全球醫療設備用熱可塑性橡膠(TPE)市場趨勢及洞察

在敏感應用中聚氯乙烯/鄰苯二甲酸酯的遷移

歐盟法規2023/2482將鄰苯二甲酸二(2-乙基己基)酯(DEHP)列為關注物質,並設定了含有DEHP的醫療設備的最終申請截止日期為2029年1月1日。這為原始設備製造商(OEM)提供了36個月的過渡期,以鼓勵其過渡到替代材料,例如SEBS和熱塑性聚氨酯(TPU),這些替代材料可以解決塑化劑滲出的問題。 2024年發布的指南強制要求對每日每公斤體重釋放超過10微克塑化劑的醫療設備進行風險效益分析,這實際上使傳統的PVC產品線無法使用。北美製造商正在與歐洲製造商協調時間表,以保持全球一致性,並推動醫療設備熱可塑性橡膠體領域向無鄰苯二甲酸酯材料的集體過渡。

微創導管治療的擴展

在導管檢查室中,需要具有優異抗彎強度和易於插入性的導管軸的心血管、神經血管和泌尿器官系統系統手術範圍正在不斷擴大。聚醚嵌段醯胺(PEBA)化合物,例如Pebax Rnew,與尼龍12相比,可將推進力降低50%,從而最大限度地減少血管損傷並縮短手術時間。彎曲疲勞測試表明,PEBA導管軸在90度彎曲下可承受10,000次循環,使用壽命幾乎是傳統聚氨酯導管的三倍。這推動了在可實現當日出院的環境中,PEBA導管的應用日益廣泛。 FDA 510(k)核准流程允許製造商使用現有主文件更新導管設計,將核准時間縮短一半,並加速熱可塑性橡膠在醫療設備的進一步應用。

E&L檢驗和滅菌引起的物理性質變化

ISO 10993-18:2020 要求進行詳細的化學成分分析測試,每個 E&L 專案的成本約為 30 萬美元,耗時九個月。 50 kGy 的伽馬射線滅菌會使未改質 PEBA 的拉伸強度降低 25%,因此配製商必須添加抗氧化劑,而這又會引入新的萃取物。環氧乙烷滅菌會導致殘留氯丙烷,根據 ISO 10993-7:2024 標準,每件器械中氯丙烷的含量必須低於 4 µg。這些科學和監管方面的挑戰延長了醫療設備用熱可塑性橡膠的研發週期,並阻礙了其短期成長。

細分市場分析

2025年,苯乙烯基嵌段共聚物佔據了醫療設備熱可塑性橡膠市場43.18%的佔有率,這主要得益於其經濟高效的透明度和高達50 kGy的伽馬射線輻照穩定性。受神經血管和周邊血管導管對超薄、抗扭轉壁的需求不斷成長的推動,PEBA預計將在2031年之前以7.12%的年成長率成長。阿科瑪的生物基產品Pebax Rnew 30R53含有30%的蓖麻油,邵氏D硬度達到53,符合歐盟綠色交易的採購規定。 TPU在2025年佔銷售額的22%,是輸液器導管的首選材料,能夠承受泵浦驅動應用中長達7天的磨損。 TPE-E 和 TPC 適用於最高 121°C 的高壓釜,但由於酯鍵的存在,它們的 γ 射線輻照穩定性有限。 TPV 和 TPO 由於其不透明度和高萃取物含量,市場佔有率不足 8%。

區域分析

2025年,北美在醫療設備用熱可塑性橡膠市場銷售額中佔36.33%。明尼蘇達州、麻薩諸塞州和加州等關鍵產業叢集支撐了這一市場主導地位,Medtronic、雅培和波士頓科學等行業領導者正在這些地區FDA的監管下拓展其新型導管和穿戴式產品線。同時,歐洲市場銷售額穩定在28%,其地位得以維持,這得益於醫療設備法規(MDR)更為嚴格的文件要求,有利於能夠提供全面安全合規(E&L)文件的成熟材料供應商。亞太地區目前佔市場佔有率的26%,預計將成為市場成長的主要驅動力,到2031年,其年均成長率預計將達到7.63%。

該地區的成長主要受三大因素驅動。首先,隨著中國和印度大力推行在地採購,Technoapex 和 DCM Shriram 於 2026 年成立的合資企業 Polytech 計畫精簡營運流程。在區域內進行食材和生產將使前置作業時間縮短六週。其次,隨著持續血糖監測的保險覆蓋範圍擴大,惠及數百萬患者,感測器製造商在本地組裝也日益成長。最後,日本和韓國的 OEM 製造商正專注於高純度產品,符合 ISO 10993-18 標準的供應商可獲得 10-15% 的價格溢價。

相較之下,拉丁美洲和中東及非洲市場合計僅佔醫療設備用熱可塑性橡膠市場銷售額的8%。高額進口關稅和有限的普及率阻礙了對先進雙色射出成型成型機的投資。此外,雖然傳統PVC作為短期消耗品仍可接受,但值得注意的是,大型跨國公司可能會將過剩產能從西方國家轉移到這些地區。如果歐洲和北美對鄰苯二甲酸二辛酯(DEHP)的銷售實施限制,這種轉移就可能發生。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 在敏感應用中聚氯乙烯和鄰苯二甲酸酯的遷移

- 微創導管治療的擴展

- 穿戴式裝置和居家照護設備的擴展

- 歐盟醫療器材法規 (EU MDR) 對原始設備製造商 (OEM) 造成的變更管理負擔有利於穩定的供應商。

- 透過包覆成型(與PP/PA黏合)實現零件整合

- 伽瑪射線穩定的透明TPE可製成不含PVC的輸液管/導管。

- 市場限制因素

- E&L;驗證和滅菌引起的物理性質變化

- PVC和矽膠在大規模生產應用的成本溢價

- OEM廠商基於MDR的材料變更管理導致進度延誤。

- 醫用樹脂供應鏈中的薄弱環節,以及滅菌過程中的瓶頸。

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 五力分析

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 產業競爭

第5章 市場規模與成長預測

- 依材料類型

- 熱可塑性橡膠- 苯乙烯基/苯乙烯-乙烯-丁烯-苯乙烯(TPE-S/SEBS)

- 熱塑性聚氨酯(TPU)

- 熱可塑性橡膠- 醯胺/聚醚嵌段醯胺 (TPE-A/PEBA)

- 熱可塑性橡膠- 聚酯/熱塑性共聚酯 (TPE-E/TPC)

- 熱塑性硫化橡膠(TPV)

- 熱塑性聚烯(TPO)

- 透過使用

- 導管和管子

- 注射器和活塞

- 塞子和密封件

- 連接器和機殼

- 穿戴式裝置和皮膚接觸介面

- 透過加工技術

- 擠壓

- 射出成型

- 吹塑成型和薄膜

- 包覆成型與雙組分注塑

- 添加劑/其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 其他亞太國家

- 中東和非洲

- GCC

- 南非

- 其他中東和非洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 市佔率分析

- 公司簡介

- Actega DS GmbH

- Arkema SA

- Avient Corporation

- BASF SE

- Celanese Corporation

- Compagnie de Saint-Gobain SA

- Covestro AG

- Duke Extrusion

- Dynasol Group

- Elastron Kimya AS

- HEXPOL AB

- KRAIBURG TPE GmbH & Co. KG

- Kraton Corporation

- Kuraray Co., Ltd.

- Lubrizol Corporation

- Mitsubishi Chemical Corporation

- Nordson MEDICAL

- RTP Company

- Tekni-Plex, Inc.

- Teknor Apex Company

- TSRC Corporation

- Zeus Company Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the thermoplastic elastomers in medical devices market size was valued at USD 3.30 billion in 2025 and is estimated to grow from USD 3.5 billion in 2026 to reach USD 4.60 billion by 2031, at a CAGR of 5.59% during the forecast period (2026-2031).

This report is Segmented by Material Type (Thermoplastic Elastomer - Styrenic / Styrene-Ethylene-Butylene-Styrene (TPE-S/SEBS), and More), Application (Catheters & Tubing, and More), Processing Technology (Extrusion, Injection Molding, Blow Molding & Film, and More), and Geography (North America, Europe, and More). Market Forecasts are Provided in Value (USD).

Global Thermoplastic Elastomers In Medical Devices Market Trends and Insights

Shift Away from PVC/Phthalates in Sensitive Uses

European Regulation 2023/2482 identifies DEHP as a substance of concern, setting a final application deadline of January 1, 2029, for medical devices containing DEHP. This provides OEMs with a 36-month window to reformulate, prompting a shift toward SEBS and thermoplastic polyurethane (TPU) alternatives that eliminate plasticizer leaching concerns. Guidance issued in 2024 requires a benefit-risk analysis for devices releasing more than 10 µg/kg body weight/day of plasticizer, effectively disqualifying traditional PVC lines. North American manufacturers are aligning their timelines with European counterparts to maintain global consistency, driving a collective shift in the thermoplastic elastomers in the medical devices market toward phthalate-free materials.

Growth in Minimally Invasive, Catheter-Based Therapies

Catheter laboratories are expanding their range of cardiovascular, neurovascular, and urological procedures, which rely on kink-resistant, pushable shafts. Polyether block amide (PEBA) compounds, such as Pebax Rnew, reduce advancement force by 50% compared to nylon 12, minimizing vessel trauma and shortening procedure times. Flexural-fatigue testing demonstrates that PEBA shafts endure 10,000 cycles at 90-degree bends, nearly tripling the lifespan of conventional polyurethane catheters, supporting broader adoption in same-day discharge environments. FDA 510(k) pathways enable manufacturers to update catheter designs using existing master files, reducing approval times by half and driving further penetration in the thermoplastic elastomers in medical devices market.

E &L Validation and Sterilization-Induced Property Shifts

ISO 10993-18:2020 requires detailed chemical-profile testing, with each E&L program costing approximately USD 300,000 and taking nine months to complete. Gamma sterilization at 50 kGy can decrease the tensile strength of unmodified PEBA by 25%, prompting compounders to include antioxidant packages, which subsequently introduce new extractables. Ethylene-oxide sterilization leaves residual ethylene chlorohydrin, which must remain below 4 µg/device under ISO 10993-7:2024 limits. These scientific and regulatory challenges extend development timelines, restraining near-term growth of the thermoplastic elastomers in the medical devices market.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Wearable and Home-Care Devices

- OEM Change-Control Burden Under EU MDR Favors Stable Suppliers

- Cost Premium vs PVC and Silicone in Volume Applications

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, styrenic block copolymers accounted for 43.18% of the thermoplastic elastomers in medical devices market size due to their cost-effective transparency and 50 kGy gamma stability. PEBA is expected to grow at an annual rate of 7.12% through 2031, driven by the increasing demand for neurovascular and peripheral-vascular catheters requiring ultra-thin, kink-resistant walls. Arkema's bio-based Pebax Rnew 30R53, with 30% castor-oil content, achieves Shore D 53 hardness, aligning with EU Green Deal procurement rules. TPU held 22% of revenue in 2025, preferred for infusion-set tubing designed to withstand pump-driven abrasion for seven days of wearable use. TPE-E and TPC are suitable for autoclave applications up to 121 °C, although their ester linkages limit gamma stability. TPV and TPO remain below 8%, constrained by opacity and higher extractables.

Geography Analysis

In 2025, North America accounted for 36.33% of the revenue in the thermoplastic elastomers for medical devices market. This dominance is supported by key clusters in Minnesota, Massachusetts, and California, where industry leaders such as Medtronic, Abbott, and Boston Scientific are scaling new catheter and wearable lines under FDA scrutiny. Meanwhile, Europe, contributing a steady 28% to the market revenue, maintains its position due to stricter MDR documentation, which benefits established material suppliers capable of providing comprehensive E&L dossiers. Asia-Pacific, currently holding 26% of the market, is expected to drive growth, with an expansion rate of 7.63% projected through 2031.

The region's growth is driven by three key factors. Firstly, with China and India promoting local sourcing, Teknor Apex's 2026 joint venture, PolyTek, with DCM Shriram, is set to streamline operations. Their in-region compounding reduces lead times by six weeks. Secondly, as reimbursement for continuous-glucose monitoring expands, millions more lives are covered, encouraging sensor manufacturers to localize assembly. Lastly, Japanese and South Korean OEMs are focusing on high-purity grades; suppliers meeting ISO 10993-18 standards can secure price premiums of 10-15%.

In contrast, Latin America and the combined regions of the Middle East & Africa account for a mere 8% of the thermoplastic elastomers in medical devices market revenue. High import duties and a limited installed base discourage investments in advanced two-shot injection presses. Additionally, while legacy PVC remains acceptable for short-term consumables, it is notable that major multinationals might redirect surplus capacity from the West to these regions. This shift could occur once DEHP sales face restrictions in Europe and North America.

- Actega DS GmbH

- Arkema S.A.

- Avient Corporation

- BASF

- Celanese Corporation

- Compagnie de Saint-Gobain S.A.

- Covestro

- Duke Extrusion

- Dynasol Group

- Elastron Kimya A.S.

- HEXPOL AB

- KRAIBURG TPE GmbH & Co. KG

- Kraton

- Kuraray Co., Ltd.

- Lubrizol

- Mitsubishi Chemical

- Nordson MEDICAL

- RTP Company

- Tekni-Plex, Inc.

- Teknor Apex Company

- TSRC Corporation

- Zeus Company Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift Away from PVC/Phthalates in Sensitive Uses

- 4.2.2 Growth in Minimally Invasive, Catheter-Based Therapies

- 4.2.3 Expansion of Wearable and Home-Care Devices

- 4.2.4 OEM Change-Control Burden Under EU MDR Favors Stable Suppliers

- 4.2.5 Overmolding-Driven Part Consolidation (Bonding To PP/PA)

- 4.2.6 Gamma-Stable Transparent Tpes Enabling PVC-Free IV/Tubing

- 4.3 Market Restraints

- 4.3.1 E&L Validation and Sterilization-Induced Property Shifts

- 4.3.2 Cost Premium Vs PVC and Silicone in Volume Applications

- 4.3.3 OEM Material Change-Control Under MDR Extends Timelines

- 4.3.4 Supply-Chain Fragility for Medical-Grade Resins, Sterilization Bottlenecks

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter;s Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Material Type

- 5.1.1 Thermoplastic Elastomer - Styrenic / Styrene-Ethylene-Butylene-Styrene (TPE-S/SEBS)

- 5.1.2 Thermoplastic Polyurethane (TPU)

- 5.1.3 Thermoplastic Elastomer - Amide / Polyether Block Amide (TPE-A/PEBA)

- 5.1.4 Thermoplastic Elastomer - Polyester / Thermoplastic Copolyester (TPE-E/TPC)

- 5.1.5 Thermoplastic Vulcanizate (TPV)

- 5.1.6 Thermoplastic Polyolefin (TPO)

- 5.2 By Application

- 5.2.1 Catheters & Tubing

- 5.2.2 Syringes & Plungers

- 5.2.3 Stoppers & Seals

- 5.2.4 Connectors & Device Housings

- 5.2.5 Wearables & Skin-Contact Interfaces

- 5.3 By Processing Technology

- 5.3.1 Extrusion

- 5.3.2 Injection Molding

- 5.3.3 Blow Molding & Film

- 5.3.4 Overmolding & 2K

- 5.3.5 Additive / Other

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Actega DS GmbH

- 6.3.2 Arkema S.A.

- 6.3.3 Avient Corporation

- 6.3.4 BASF SE

- 6.3.5 Celanese Corporation

- 6.3.6 Compagnie de Saint-Gobain S.A.

- 6.3.7 Covestro AG

- 6.3.8 Duke Extrusion

- 6.3.9 Dynasol Group

- 6.3.10 Elastron Kimya A.S.

- 6.3.11 HEXPOL AB

- 6.3.12 KRAIBURG TPE GmbH & Co. KG

- 6.3.13 Kraton Corporation

- 6.3.14 Kuraray Co., Ltd.

- 6.3.15 Lubrizol Corporation

- 6.3.16 Mitsubishi Chemical Corporation

- 6.3.17 Nordson MEDICAL

- 6.3.18 RTP Company

- 6.3.19 Tekni-Plex, Inc.

- 6.3.20 Teknor Apex Company

- 6.3.21 TSRC Corporation

- 6.3.22 Zeus Company Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment

熱可塑性橡膠市場-2026-2032年全球市場預測

熱可塑性橡膠市場-2026-2032年全球市場預測 2026年全球醫療設備熱可塑性橡膠市場報告

2026年全球醫療設備熱可塑性橡膠市場報告 熱可塑性橡膠(TPE):市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031)中東和非洲熱可塑性橡膠(TPE)市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

熱可塑性橡膠(TPE):市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031)中東和非洲熱可塑性橡膠(TPE)市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 熱可塑性橡膠市場:依類型、應用、終端用戶產業及地區分類

熱可塑性橡膠市場:依類型、應用、終端用戶產業及地區分類 全球熱可塑性橡膠市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球熱塑性聚醯胺彈性體市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球熱可塑性橡膠市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球熱塑性聚醯胺彈性體市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 全球熱可塑性橡膠市場:市場規模、佔有率和趨勢分析(按應用、材料和地區分類),細分市場預測(2026-2033 年)

全球熱可塑性橡膠市場:市場規模、佔有率和趨勢分析(按應用、材料和地區分類),細分市場預測(2026-2033 年) 醫療設備熱可塑性橡膠市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)2026年全球熱可塑性橡膠市場報告

醫療設備熱可塑性橡膠市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)2026年全球熱可塑性橡膠市場報告