|

市場調查報告書

商品編碼

2061574

中東和非洲熱可塑性橡膠(TPE)市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Middle-East And Africa Thermoplastic Elastomer (TPE) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

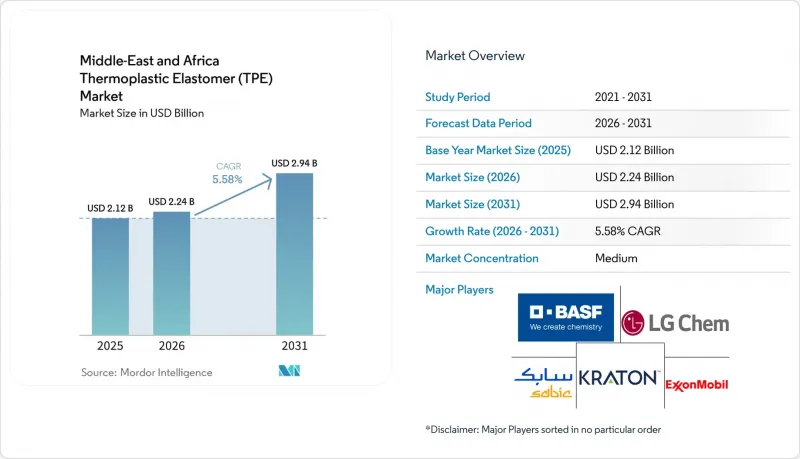

根據 Mordor Intelligence 預測,中東和非洲熱可塑性橡膠市場規模將從 2025 年的 21.2 億美元成長到 2026 年的 22.4 億美元,到 2031 年將達到 29.4 億美元,2026 年至 2031 年的複合年成長率為 5.58%。

本報告按產品類型(苯乙烯嵌段共聚物 (TPE-S)、熱塑性烯烴 (TPE-O) 等)、應用領域(汽車和交通運輸、建築和施工等)以及地區(沙烏地阿拉伯、南非以及其他中東和非洲國家)對產業進行細分。市場規模和預測均以美元計價。

中東和非洲熱可塑性橡膠(TPE)市場趨勢與洞察

對輕型汽車的需求

摩洛哥和南非的汽車製造商正在用烯烴基熱塑性彈性體(TPE)取代三元乙丙橡膠(EPDM)熱固性樹脂,用於汽車保險桿飾板、玻璃密封條和進氣管道,以減輕重量並延長電動車(EV)的續航里程。 Stellantis公司投資30億蘭特(約1.65億美元)在科加(Koega)建設的工廠計劃年產5萬件產品,在地採購率達到35%,這將直接刺激中東和非洲地區對用於內飾軟觸感材料、車門密封條和NVH(噪音、振動和聲振粗糙度)部件的熱可塑性橡膠的需求。預計到2025年,摩洛哥的汽車產量將超過100萬輛,這將推動該地區對聚丙烯基混合材料的需求。從 2026 年 3 月起,南非將對新能源汽車 (NEV) 相關設施實行 150% 的稅額扣抵,屆時 TPU 線束護套將更具成本競爭力,在耐磨性和煙霧密度方面超越 PVC(聚氯乙烯)。

醫療設備領域推行PVC替代的監管舉措

海灣國家的監管機構正逐步遵守歐盟REACH(化學品註冊、評估、授權和限制)法規,該法規將鄰苯二甲酸二(2-乙基己基)酯(DEHP)增塑聚氯乙烯(PVC)列為「高度關注物質」。 2025年12月的一項調查顯示,沙烏地阿拉伯不含DEHP產品的滲透率僅30%左右,凸顯了醫用TPU和SEBS(苯乙烯-乙烯-丁烯-苯乙烯)管材市場巨大的成長潛力。如果沙烏地阿拉伯食品藥物管理局(FDA)將採購不含DEHP的產品納入醫院認證標準,中東和非洲地區耐水解TPU熱可塑性橡膠的市場規模可望在三年內翻倍。阿拉伯聯合大公國和埃及的採購改革同樣重要,因為即使在兒童腫瘤病房,成本驅動的採購觀念仍然傾向於價格較低的PVC。

石油原料價格波動劇烈

2026年2月,沿岸地區丙烯現貨平均價格為1美元/公斤。然而,如果布蘭特原油價格上漲10美元/桶,丙烯價格將上漲0.10美元/公斤,這可能會使沒有指數掛鉤合約的轉化商的利潤率下降400至600個基點。像沙烏地基礎工業公司(SABIC)這樣的大型綜合企業自然可以透過上游業務裂解價差貨幣化來對沖風險,而獨立化合物生產商則被迫依賴填料稀釋或長期採購合約,這兩種方法都會降低柔軟性。

細分市場分析

2025年,熱塑性烯烴(TPO)在中東和非洲熱可塑性橡膠市場佔有25.59%的佔有率,這主要得益於市場對前擋板、門飾條和鞋底的需求,這些產品兼具成本優勢和輕量化特性。此外,該地區的聚丙烯供應也為該細分市場提供了助力,即使乙烯合約價格走軟,也能維持毛利率。彈性體合金在預測期(2026-2031年)內將以5.86%的複合年成長率加速成長,其壓縮永久變形性能已接近熱固性三元乙丙橡膠(EPDM),且只需一次注塑成型即可固化,從而縮短引擎艙射出成型件的生產週期。在熱塑性聚氨酯(TPU)等特殊產品領域,BASF計畫於2026年運作的阻燃生產線將得到應用;同時,在DL Chemical的管理下,苯乙烯基嵌段共聚物也在不斷拓展。

在120 度C以上表現出優異性能的共聚酯和聚醯胺共混物,其特點是持續創新、價格高且產量有限。科思創被阿布達比國家石油公司(ADNOC)收購後獲得的注資將用於沿岸地區的聚醚多元醇生產線,從而增強其下游熱塑性聚氨酯(TPU)業務的韌性。儘管中東和非洲的熱可塑性橡膠市場仍以烯烴基樹脂為主,但隨著醫療設備和電動車結構設計對模量範圍要求的不斷提高,特種樹脂的應用將逐步增加。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場促進因素

- 對輕型汽車的需求

- 推動制定法規,以取代醫療設備中的聚氯乙烯(PVC)材料。

- 該地區鞋類製造地的擴張

- GCC的整合裂解裝置可生產客製化的烯烴基TPE等級產品。

- 採用3D列印技術製造用於石油和天然氣產業零件物流的TPU材料

- 市場限制因素

- 石油原料價格波動劇烈

- 熱固性橡膠在高溫環境下的競爭

- 本地TPU複合材料和加工領域技術純熟勞工短缺。

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 依產品類型

- 苯乙烯基嵌段共聚物(TPE-S)

- 熱塑性烯烴(TPE-O)

- 彈性體合金(TPE-V 或 TPV)

- 熱塑性聚氨酯(TPU)

- 熱塑性共聚酯

- 熱塑性聚醯胺

- 透過使用

- 汽車和運輸業

- 建築/施工

- 鞋類

- 電氣和電子設備

- 醫學領域

- 電器產品

- HVAC

- 黏合劑、密封劑和塗料

- 其他用途

- 按地區

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- Arkema

- BASF SE

- Covestro AG

- DSM

- DuPont

- Evonik Industries AG

- Exxon Mobil Corporation

- Huntsman International LLC

- LANXESS

- LCY GROUP

- LG Chem

- Mitsubishi Chemical Corporation

- SABIC

- Sumitomo Chemicals Co. Ltd

- Kraton Corporation

第7章 市場機會與未來展望

According to Mordor Intelligence, the middle-East and Africa Thermoplastic Elastomer Market size is expected to grow from USD 2.12 billion in 2025 to USD 2.24 billion in 2026 and is forecast to reach USD 2.94 billion by 2031 at 5.58% CAGR over 2026-2031.

This report Segments the Industry Into Product Type (Styrenic Block Copolymer (TPE-S), Thermoplastic Olefin (TPE-O), and More), Application (Automotive and Transportation, Building and Construction, and More), and Geography (Saudi Arabia, South Africa, and the Rest of the Middle-East and Africa). The Market Size and Forecasts are Provided in Terms of Value (USD).

Middle-East And Africa Thermoplastic Elastomer (TPE) Market Trends and Insights

Automotive Light-Weighting Demand

Vehicle makers in Morocco and South Africa are replacing EPDM (ethylene propylene diene monomer) thermosets with olefinic TPEs in bumper fascia, glazing encapsulation, and air-intake ducts to curb weight and extend electric vehicle (EV) range. Stellantis's R3 billion (USD 165 million) Coega plant targets 50,000 units yearly with 35% local content, directly stimulating the Middle-East and Africa Thermoplastic Elastomer market demand for interior soft-touch skins, door seals, and NVH (noise, vibration, and harshness) components. Morocco's output surpassed 1 million vehicles in 2025, intensifying regional pull for polypropylene-based blends. Tax deductions of 150% for new-energy-vehicle facilities in South Africa from March 2026 sharpen the cost case for TPU wire-harness jackets that outperform PVC (polyvinyl chloride) in abrasion and smoke density.

Regulatory Push Replacing PVC in Medical Devices

Gulf regulators are progressively aligning with European REACH (Registration, Evaluation, Authorisation, and Restriction of Chemicals) listings that classify DEHP (Di(2-ethylhexyl) phthalate)-plasticized PVC as a Substance of Very High Concern. A December 2025 audit placed Saudi Arabia's DEHP-free penetration at roughly 30%, highlighting substantial headroom for medical-grade TPU and SEBS (styrene ethylene butylene styrene) tubing. Once the Saudi FDA (food and drug administration) ties hospital accreditation to DEHP-free sourcing, the Middle-East and Africa thermoplastic elastomer market volume for hydrolysis-resistant TPU could double within three years. Procurement reforms in the UAE and Egypt are likewise critical, as cost-driven purchasing still favors lower-priced PVC even in pediatric oncology units.

Volatile Petro-Feedstock Prices

Spot propylene in February 2026 averaged USD 1.00 per kg in the Gulf, but a USD 10 per-barrel Brent jump can lift propylene by USD 0.10 per kg, stripping 400-600 basis-points of margin from converters lacking index-linked contracts. Integrated majors such as SABIC hedge naturally by monetizing upstream cracks, while standalone compounders must rely on filler dilution or long-term offtake deals, both of which curb flexibility.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Regional Footwear Manufacturing Bases

- GCC Integrated Crackers Enabling Bespoke Olefinic TPE Grades

- Competition from Thermoset Rubber at High-Temperature Service

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Thermoplastic Olefin captured 25.59% of the Middle-East and Africa Thermoplastic Elastomer market share in 2025, fueled by bumper fascia, door trims, and footwear soles that balance cost and light weight. The segment benefits from an in-region polypropylene supply that anchors gross margins even when ethylene contracts soften. Elastomeric Alloy is accelerating at a 5.86% CAGR during the forecast period (2026-2031), nearing thermoset EPDM compression-set performance but curing in one-shot injection cycles, which trims takt times for under-hood seals. Specialty streams such as TPU leverage BASF's 2026 flame-retardant line, while styrenic block copolymers gain scale under DL Chemical's stewardship.

Continuous innovation is evident in copolyester and polyamide blends that thrive above 120°C, commanding premium pricing but serving limited volumes. Covestro's capital injection post-acquisition by ADNOC is earmarked for Gulf-based polyether polyol lines, strengthening downstream TPU resilience. The Middle-East and Africa thermoplastic elastomer market continues to skew toward olefinic grades, yet specialty resin uptake will edge higher as medical-device and EV architectures require tighter modulus windows.

List of Companies Covered in this Report:

- Arkema

- BASF SE

- Covestro AG

- DSM

- DuPont

- Evonik Industries AG

- Exxon Mobil Corporation

- Huntsman International LLC

- LANXESS

- LCY GROUP

- LG Chem

- Mitsubishi Chemical Corporation

- SABIC

- Sumitomo Chemicals Co. Ltd

- Kraton Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Drivers

- 4.1.1 Automotive light-weighting demand

- 4.1.2 Regulatory push replacing PVC in medical devices

- 4.1.3 Expanding regional footwear manufacturing bases

- 4.1.4 GCC integrated crackers enabling bespoke olefinic TPE grades

- 4.1.5 3-D-printing-grade TPU for oil and gas spare-parts logistics

- 4.2 Market Restraints

- 4.2.1 Volatile petro-feedstock prices

- 4.2.2 Competition from thermoset rubber at high-temperature service

- 4.2.3 Skilled-labor gap in local TPU compounding and processing

- 4.3 Value Chain Analysis

- 4.4 Porter's Five Forces

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitutes

- 4.4.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Styrenic Block Copolymer (TPE-S)

- 5.1.2 Thermoplastic Olefin (TPE-O)

- 5.1.3 Elastomeric Alloy (TPE-V or TPV)

- 5.1.4 Thermoplastic Polyurethane (TPU)

- 5.1.5 Thermoplastic Copolyester

- 5.1.6 Thermoplastic Polyamide

- 5.2 By Application

- 5.2.1 Automotive and Transportation

- 5.2.2 Building and Construction

- 5.2.3 Footwear

- 5.2.4 Electricals and Electronics

- 5.2.5 Medical

- 5.2.6 Household Appliances

- 5.2.7 HVAC

- 5.2.8 Adhesive, Sealant and Coating

- 5.2.9 Other Applications

- 5.3 By Geography

- 5.3.1 Saudi Arabia

- 5.3.2 South Africa

- 5.3.3 Rest of Middle-East and Africa

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Arkema

- 6.4.2 BASF SE

- 6.4.3 Covestro AG

- 6.4.4 DSM

- 6.4.5 DuPont

- 6.4.6 Evonik Industries AG

- 6.4.7 Exxon Mobil Corporation

- 6.4.8 Huntsman International LLC

- 6.4.9 LANXESS

- 6.4.10 LCY GROUP

- 6.4.11 LG Chem

- 6.4.12 Mitsubishi Chemical Corporation

- 6.4.13 SABIC

- 6.4.14 Sumitomo Chemicals Co. Ltd

- 6.4.15 Kraton Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

熱可塑性橡膠市場-2026-2032年全球市場預測

熱可塑性橡膠市場-2026-2032年全球市場預測 2026年全球醫療設備熱可塑性橡膠市場報告

2026年全球醫療設備熱可塑性橡膠市場報告 熱可塑性橡膠(TPE):市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031)醫療設備用熱可塑性橡膠:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年)

熱可塑性橡膠(TPE):市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031)醫療設備用熱可塑性橡膠:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年) 熱可塑性橡膠市場:依類型、應用、終端用戶產業及地區分類

熱可塑性橡膠市場:依類型、應用、終端用戶產業及地區分類 全球熱可塑性橡膠市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球熱塑性聚醯胺彈性體市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球熱可塑性橡膠市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球熱塑性聚醯胺彈性體市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 全球熱可塑性橡膠市場:市場規模、佔有率和趨勢分析(按應用、材料和地區分類),細分市場預測(2026-2033 年)

全球熱可塑性橡膠市場:市場規模、佔有率和趨勢分析(按應用、材料和地區分類),細分市場預測(2026-2033 年) 醫療設備熱可塑性橡膠市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)2026年全球熱可塑性橡膠市場報告

醫療設備熱可塑性橡膠市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)2026年全球熱可塑性橡膠市場報告