|

市場調查報告書

商品編碼

1936525

醫療設備熱可塑性橡膠市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)Thermoplastic Elastomers in Medical Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

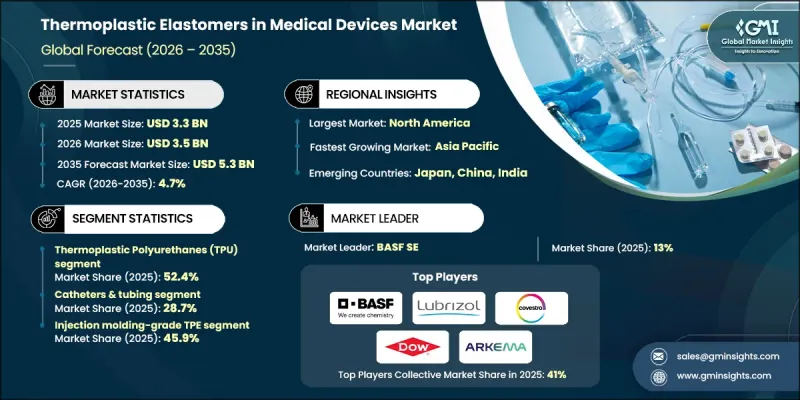

全球醫療設備用熱可塑性橡膠市場預計到 2025 年將達到 33 億美元,到 2035 年將達到 53 億美元,年複合成長率為 4.7%。

熱可塑性橡膠(TPE) 已從小眾材料穩步發展成為現代醫療製造中不可或缺的組成部分。其彈性、生物相容性和高效加工性能的結合,滿足了人們對耐用、對患者友好的醫療技術日益成長的需求。醫療機構越來越關注能夠提升病患舒適度並提供穩定性能的解決方案,這使得 TPE 成為下一代醫療設備開發的首選材料。在嚴格的安全標準和環境法規的推動下,永續性和負責任的材料管理已成為醫用 TPE 領域的核心挑戰。向低生態影響、高耐滅菌性的可再生材料的轉變,正持續加速其應用。持續的技術創新提高了配方安全性、機械穩定性、耐化學性和整體使用壽命,從而解決了傳統彈性體長期存在的許多問題。持續的臨床和環境測試體現了該行業致力於推進材料科學發展並支持更安全醫療結果的承諾。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始金額 | 33億美元 |

| 預測金額 | 53億美元 |

| 複合年成長率 | 4.7% |

預計到2025年,熱塑性聚氨酯(TPU)將佔據52.4%的市場佔有率,並在2035年之前以5%的複合年成長率成長。 TPU因其優異的柔軟性和強度平衡性,仍是應用最廣泛的醫用級熱可塑性橡膠(TPE),能夠在不影響結構完整性的前提下精確控制其柔軟度。這些特性滿足了複雜的醫療工程需求,並在各種醫療應用中提供穩定的性能。

預計到2025年,導管和管材市場佔有率將達到28.7%,並在2026年至2035年間以5.5%的複合年成長率成長。這一市場主導地位主要得益於材料的特性,這些特性使其在較長的使用週期內仍能保持生物相容性、柔軟性和無菌性。熱塑性彈性體(TPE)確保了從常規醫療程序到先進治療系統的可靠性能,進一步鞏固了其在該領域的重要性。

預計到2025年,北美醫療設備熱可塑性橡膠市佔率將達到35%。該地區受益於成熟的醫療保健基礎設施、嚴格的監管以及醫療設備製造商的高度集中。對聚合物研究的持續投入以及以合規為導向的創新,正透過提升安全標準、增強器材功能和改善病患體驗,鞏固該地區的領先地位。

目錄

第1章調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 從聚氯乙烯過渡到不含鄰苯二甲酸酯的替代品

- 對不含乳膠的醫療產品的需求不斷成長

- 老化與慢性病盛行率

- 產業潛在風險與挑戰

- 原料成本上漲和通用PVC

- 與熱固性樹脂相比,耐熱性有限

- 市場機遇

- 永續的生物基TPE配方

- 抗菌和感染預防材料

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 透過TPE化學結構

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利狀態

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續努力

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 考慮到碳足跡

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依TPE成分分類,2022-2035年

- 熱塑性聚氨酯(TPU)

- 聚醚基TPU

- 聚酯基TPU

- 苯乙烯基嵌段共聚物(TPE-S/SEBS)

- SEBS(氫化苯乙烯)

- SBS 和其他苯乙烯類化合物

- 熱塑性硫化橡膠(TPV)

- PP/EPDM動態硫化橡膠

- 熱塑性共聚酯彈性體(COPE/TPC-ET)

- 聚醚二醇/PBT嵌段共聚物

- 熱塑性聚醯胺彈性體(PEBA/TPE-A)

- 熱塑性烯烴彈性體(TPE-O/TPO)

第6章 按應用領域分類的市場估算與預測,2022-2035年

- 導尿管

- 靜脈導管

- 泌尿系統

- 心血管導管和球囊導管

- 單腔和多腔醫用導管

- 藥物輸送/輸液管

- 醫療設備和器械

- 用於治療磨牙症的牙科牙套

- 蠕動泵管

- 尿道導管手把和組件

- 呼吸防護面罩貼紙

- 一次性醫療用品

- 咽拭子刷

- 檢查手套(非乳膠)

- 一次性口罩和衣物

- 醫用薄膜、包裝袋和包裝材料

- 輸液袋和生理食鹽水水袋

- 生物製藥儲存袋

- 經腸營養及腸外營養袋

- 腹膜透析袋

- 醫用耳塞和墊圈

- 點滴瓶蓋及密封裝置

- 注射器墊圈和柱塞頭

- 管瓶瓶塞和隔膜

- 外科手術及診斷器械

- 手術器械的握柄和手柄

- 診斷設備機殼

- 醫用鞋

- 植入式醫療設備及其組件

- 外科用網片(聚合物)

- 聚合物假體零件

- 彈性體植入塊

第7章 依加工方式分類的市場估算與預測,2022-2035年

- 射出成型級TPE

- 擠出級TPE

- 吹塑成型級TPE

- 包覆成型/共注塑級TPE

第8章 2022-2035年各地區市場估算與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第9章:公司簡介

- BASF SE

- Lubrizol Corporation

- Covestro AG

- Dow Chemical

- Arkema

- Teknor Apex

- Kraiburg TPE

- Hexpol/Elastron

- Kuraray

- RTP Company

- Evonik

- Kraton

- DSM Biomedical

- Trinseo

- Mitsubishi Chemical

The Global Thermoplastic Elastomers in Medical Devices Market was valued at USD 3.3 billion in 2025 and is estimated to grow at a CAGR of 4.7% to reach USD 5.3 billion by 2035.

Thermoplastic elastomers have steadily evolved from niche materials into indispensable components within modern medical manufacturing. Their combination of elasticity, biocompatibility, and efficient processing supports the growing demand for durable, patient-friendly medical technologies. Healthcare providers increasingly prioritize solutions that deliver consistent performance while improving patient comfort, positioning TPEs as a preferred material class for next-generation device development. Sustainability and responsible material management have become central to the medical TPE landscape, driven by strict safety standards and environmental regulations. The shift toward recyclable materials with lower ecological impact and high sterilization resistance continues to accelerate adoption. Ongoing innovation addresses long-standing concerns related to conventional elastomers by improving formulation safety, mechanical stability, chemical resistance, and overall lifespan. Continuous clinical and environmental testing reflects the industry's commitment to advancing material science while supporting safer healthcare outcomes.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.3 Billion |

| Forecast Value | $5.3 Billion |

| CAGR | 4.7% |

Thermoplastic Polyurethanes accounted for 52.4% share in 2025 and are forecast to grow at a CAGR of 5% through 2035. TPU remains the most widely adopted medical-grade TPE due to its balance of flexibility and strength, which allows precise control over softness without compromising structural reliability. These attributes support complex medical engineering requirements and contribute to consistent performance across a wide range of medical applications.

The catheters and tubing segment held a 28.7% share in 2025 and is anticipated to grow at a CAGR of 5.5% during 2026-2035. This dominance is supported by the material's ability to maintain biocompatibility, flexibility, and sterility throughout extended use cycles. TPEs ensure reliable performance across both routine medical procedures and advanced therapeutic systems, reinforcing their importance within this segment.

North America Thermoplastic Elastomers in Medical Devices Market held a 35% share in 2025. The region benefits from a mature healthcare infrastructure, rigorous regulatory oversight, and a strong concentration of medical device manufacturers. Continued investment in polymer research and compliance-focused innovation strengthens regional leadership by enhancing safety standards, device functionality, and patient experience.

Key companies operating in the Global Thermoplastic Elastomers in Medical Devices Market include Lubrizol Corporation, BASF SE, Covestro AG, Arkema, Dow Chemical, Kuraray, Kraiburg TPE, Teknor Apex, Hexpol/Elastron, RTP Company, Kraton, Evonik, Mitsubishi Chemical, Trinseo, and DSM Biomedical. Companies operating in the Thermoplastic Elastomers in Medical Devices Market focus on material innovation, regulatory alignment, and long-term partnerships to strengthen their competitive position. Manufacturers invest heavily in research to improve formulation safety, mechanical performance, and sterilization compatibility while meeting evolving compliance requirements. Strategic collaborations with medical device producers allow early integration of customized materials into product design cycles. Firms also prioritize sustainability initiatives by developing recyclable and low-impact elastomer solutions. Capacity expansion, geographic diversification, and portfolio optimization further support market penetration, while consistent quality assurance and clinical validation help build trust with healthcare providers and regulatory bodies.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 TPE Chemistry

- 2.2.3 Application

- 2.2.4 Processing Method

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Shift from PVC to phthalate-free alternatives

- 3.2.1.2 Growing demand for latex-free medical products

- 3.2.1.3 Aging population & chronic disease prevalence

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Higher material cost vs. Commodity PVC

- 3.2.2.2 Limited high-temperature resistance vs. Thermosets

- 3.2.3 Market opportunities

- 3.2.3.1 Sustainable & bio-based TPE formulations

- 3.2.3.2 Antimicrobial & infection-prevention materials

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By TPE Chemistry

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By TPE Chemistry, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Thermoplastic Polyurethanes (TPU)

- 5.2.1 Polyether-Based TPU

- 5.2.2 Polyester-Based TPU

- 5.3 Styrenic Block Copolymers (TPE-S/SEBS)

- 5.3.1 SEBS (Hydrogenated Styrenic)

- 5.3.2 SBS & Other Styrenic Variants

- 5.4 Thermoplastic Vulcanizates (TPV)

- 5.4.1 PP/EPDM Dynamic Vulcanizates

- 5.5 Thermoplastic Copolyester Elastomers (COPE/TPC-ET)

- 5.5.1 Polyether Glycol/PBT Block Copolymers

- 5.6 Thermoplastic Polyamide Elastomers (PEBA/TPE-A)

- 5.7 Thermoplastic Olefin Elastomers (TPE-O/TPO)

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Catheters & tubing

- 6.2.1 Intravenous (iv) catheters

- 6.2.2 Urological catheters

- 6.2.3 Cardiovascular catheters & balloon catheters

- 6.2.4 Single & multi-lumen medical tubing

- 6.2.5 Drug delivery & infusion tubing

- 6.3 Medical equipment & devices

- 6.3.1 Dental guards for bruxism disease

- 6.3.2 Peristaltic pump tubes

- 6.3.3 Urine catheter grips & components

- 6.3.4 Respiratory face masks & seals

- 6.4 Disposable medical goods

- 6.4.1 Throat swab brushes

- 6.4.2 Examination gloves (non-latex)

- 6.4.3 Disposable masks & garments

- 6.5 Medical films, bags & packaging

- 6.5.1 Iv & saline bags

- 6.5.2 Biopharmaceutical storage bags

- 6.5.3 Enteral & parenteral nutrition bags

- 6.5.4 Peritoneal & dialysis bags

- 6.6 Medical tips & gaskets

- 6.6.1 Infusion bottle caps & closures

- 6.6.2 Syringe gaskets & plunger tips

- 6.6.3 Vial stoppers & septa

- 6.7 Surgical & diagnostic instruments

- 6.7.1 Surgical instrument grips & handles

- 6.7.2 Diagnostic equipment housings

- 6.8 Medical footwear

- 6.9 Implantable devices & components

- 6.9.1 Surgical meshes (polymeric)

- 6.9.2 Polymeric prostheses components

- 6.9.3 Elastomeric implant blocks

Chapter 7 Market Estimates and Forecast, By Processing Method, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Injection Molding-Grade TPE

- 7.3 Extrusion-Grade TPE

- 7.4 Blow Molding-Grade TPE

- 7.5 Overmolding & Co-Injection Grade TPE

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 BASF SE

- 9.2 Lubrizol Corporation

- 9.3 Covestro AG

- 9.4 Dow Chemical

- 9.5 Arkema

- 9.6 Teknor Apex

- 9.7 Kraiburg TPE

- 9.8 Hexpol/Elastron

- 9.9 Kuraray

- 9.10 RTP Company

- 9.11 Evonik

- 9.12 Kraton

- 9.13 DSM Biomedical

- 9.14 Trinseo

- 9.15 Mitsubishi Chemical

熱可塑性橡膠市場-2026-2032年全球市場預測

熱可塑性橡膠市場-2026-2032年全球市場預測 2026年全球醫療設備熱可塑性橡膠市場報告

2026年全球醫療設備熱可塑性橡膠市場報告 熱可塑性橡膠(TPE):市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031)中東和非洲熱可塑性橡膠(TPE)市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)醫療設備用熱可塑性橡膠:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年)

熱可塑性橡膠(TPE):市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031)中東和非洲熱可塑性橡膠(TPE)市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)醫療設備用熱可塑性橡膠:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年) 熱可塑性橡膠市場:依類型、應用、終端用戶產業及地區分類

熱可塑性橡膠市場:依類型、應用、終端用戶產業及地區分類 全球熱可塑性橡膠市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球熱塑性聚醯胺彈性體市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球熱可塑性橡膠市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球熱塑性聚醯胺彈性體市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 全球熱可塑性橡膠市場:市場規模、佔有率和趨勢分析(按應用、材料和地區分類),細分市場預測(2026-2033 年)2026年全球熱可塑性橡膠市場報告

全球熱可塑性橡膠市場:市場規模、佔有率和趨勢分析(按應用、材料和地區分類),細分市場預測(2026-2033 年)2026年全球熱可塑性橡膠市場報告