|

市場調查報告書

商品編碼

2063457

南美洲報關代理:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)South America Customs Brokerage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

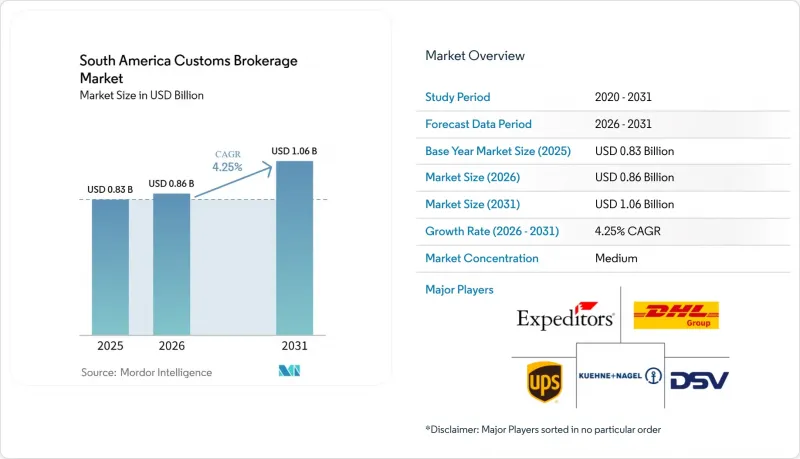

據 Mordor Intelligence 稱,2025 年南美洲報關代理市場價值為 8.2683 億美元,預計到 2031 年將達到 10.6225 億美元,而 2026 年為 8.626 億美元,預測期(2026-2031 年)的複合年成長率為 4.25%。

儘管關稅表每季度有所調整,但由於電子商務、區域性單一窗口計劃以及汽車和電子產品製造商的近岸外包等因素推動了小包裹流量的成長,貨運量依然保持強勁。本報告按運輸方式(海運、空運及其他)、仲介類型(純報關行和貨運代理)、進口商規模(大型企業、中型企業及其他)、數位化應用情況(傳統方式和基於API的方式)、最終用戶(零售和電子商務、汽車及其他)以及國家/地區(巴西、哥倫比亞及其他)進行細分。市場預測以美元計價。

南美洲報關代理市場的趨勢與洞察

跨境電子商務的快速成長

在巴西、阿根廷和智利,低價值小包裹已佔海關申報總量的四分之一以上,迫使報關行以更低的收費處理更多交易。巴西的「Remessa Conforme」(合格申報)計畫登記了67%的進口小包裹,並要求預付關稅,從而加快了海關業務向Mercado Libre等平台的轉移。哥倫比亞5000美元的簡化申報限額也產生了類似的效果,促進了中小企業的進口。阿根廷的SUCA入口網站在上線第一年就處理了320萬個小包裹,鼓勵報關行採用自動化流程,而不是手動輸入資料。隨著海關流程的加快和更多企業開始直接出口,南美洲報關代理市場的潛在規模正在擴大。

促進南方共同市場與太平洋聯盟之間的貿易便利化

2025年簽署的AEO互認協議涵蓋哥倫比亞的570家公司,並消除了五個經濟區內重複的合規審計。巴西和阿根廷將於2026年運作AFC PLUS系統,為綠色通道貨物設定12小時的目標通關時間,並建立可預測的停留時間。智利將與墨西哥、秘魯和哥倫比亞整合原產地證書交換,而秘魯的VUCE指令要求在2026年12月前實現部際間的全面協調。隨著海關風險的降低,出口商將擴大區域內貿易,因此流程的協調統一將促進南美洲報關代理市場的擴張。

複雜且經常變動的關稅體系

阿根廷在兩年內對其通用對外關稅(CET)例外條款進行了14次調整,迫使報關行每天都要查閱官方公報。巴西的雙重增值稅制度將持續到2033年,這意味著申報時需要同時計算新舊兩種制度下的課稅。哥倫比亞計劃在2026年以行政罰款取代刑事處罰,預計將增加審計次數。頻繁的規則變更正在透過增加成本和阻礙小規模企業進入市場,減緩南美報關代理市場的成長。

細分市場分析

預計到2025年,海運將佔南美清關市場佔有率的47.33%,而空運快遞和普通貨物的複合年成長率預計到2031年將達到5.46%。小包裹運輸正推動運輸方式的轉變,這主要歸因於50美元的「合格包裹」(Remessa Conforme)限額以及疫苗運輸需要2至8攝氏度的溫度控制。國際航空運輸協會(IATA)的「ONE Record」系統預計到2025年將達到22%,屆時報關行將能夠根據航空公司的資料饋送自動填寫申報單。

儘管海運和航線對於糧食、化學品和汽車散件組裝套件(KD套件)的運輸仍然至關重要,但進口商擴大選擇簽訂包含運輸、保險和清關的綜合合約。在跨安第斯走廊,公路和鐵路運輸使用TIR單證,允許貨物抵達後再繳納關稅,這為熟悉陸路邊境檢查規定的報關行創造了利基服務。隨著數位化申報系統的日趨成熟,與空運快遞相關的南美報關代理市場預計將持續擴張。

貨運代理和第三方物流整合業者佔據南美報關仲介市場60.67%的佔有率。這主要是由於企業托運人傾向於單一聯繫點。桑托斯和布宜諾斯艾利斯的港口報關服務縮短了門到門的運輸週期,並推廣了「供應商管理式報關」合約。然而,純粹的報關行預計將以4.88%的複合年成長率成長,其業務涵蓋審計合規、退稅收取以及根據南方共同市場機動車法規提供的商品分類諮詢。

儘管與海關檢查員建立傳統關係對黃道貨物仍然至關重要,但利用應用程式介面(API)的新興參與企業正透過聘用前公務員和整合即時海關資料庫來獲得競爭優勢。因此,南美洲報關代理市場分為兩類:注重規模的服務包和高技能諮詢合約。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 跨境電子商務的蓬勃發展

- 南方共同市場和太平洋聯盟的貿易便利化

- 數位化清關平台(單一窗口,區塊鏈)

- 將供應鏈近岸外包至南美洲

- 亞馬遜自由貿易區的出現

- 在海關文件中揭露碳足跡

- 市場限制因素

- 複雜且經常變化的收費系統

- 高昂的物流成本和港口堵塞

- 各國數位簽章法律存在不一致之處

- 持證仲介人員高齡化

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 地緣政治事件的影響

- 波特五力模型

第5章 市場規模與成長預測

- 透過運輸方式

- 海上運輸

- 空運(快遞和普通貨物)

- 跨境陸路運輸(卡車和鐵路)

- 仲介類型

- 純粹的報關行

- 貨運代理/第三方物流綜合仲介

- 按進口商規模

- 大公司

- 中端市場

- 小規模/小型貨運商

- 透過數位化實施

- 傳統仲介

- 數位化優先/基於 API 的仲介

- 產業最終用途

- 零售與電子商務

- 汽車和電動車

- 電子和半導體

- 製藥和生命科學

- 航太/國防

- 化學產品和工業產品

- 其他

- 國家

- 巴西

- 阿根廷

- 智利

- 哥倫比亞

- 秘魯

- 其他南美國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- DHL Global Forwarding

- DSV

- Kuehne+Nagel

- CEVA Logistics(CMA CGM)

- Maersk Customs Services

- UPS Supply Chain Solutions

- Expeditors International

- FedEx Logistics

- Hellmann Worldwide Logistics

- GEODIS

- Rhenus Logistics

- Noatum Logistics

- Yusen Logistics

- TIBA Group

- Grupo RAS

- Allink Transportes

- Aduana Brokerage Services(ABS Group)

- Agunsa

- Ultramar

- FS Agencia de Aduanas

第7章 市場機會與未來展望

According to Mordor Intelligence, the south america customs brokerage market size was valued at USD 826.83 million in 2025 and estimated to grow from USD 862.6 million in 2026 to reach USD 1062.25 million by 2031, at a CAGR of 4.25% during the forecast period (2026-2031).

Growing e-commerce parcel flows, regional single-window programs, and near-shoring by automotive and electronics manufacturers keep volumes resilient even as tariff schedules change each quarter. This report is Segmented by Mode of Transport (Ocean, Air, and More), by Broker Type (Pure Customs Broker, Freight Forwarder), by Importer Size (Large Enterprises, Mid-Market, and More), by Digital Adoption (Traditional, API-Based), by End-User (Retail and E-Commerce, Automotive and More), and by Country (Brazil, Colombia, and More ). The Market Forecasts are Provided in Terms of Value (USD).

South America Customs Brokerage Market Trends and Insights

Cross-Border E-Commerce Boom

Low-value parcels already form more than one-quarter of customs declarations in Brazil, Argentina, and Chile, pushing brokers to process higher transaction counts for lower fees. Brazil's Remessa Conforme program enrolls 67% of inbound parcels and collects duties upfront, shifting brokerage work upstream to platforms like Mercado Libre. Colombia's USD 5,000 simplified-declaration ceiling achieves a similar effect and accelerates SME imports. Argentina's SUCA portal handled 3.2 million parcels in its first year, encouraging brokers to automate rather than re-key data. Accelerated clearance cycles enlarge the addressable South America customs brokerage market as more merchants begin exporting directly.

Mercosur & Pacific Alliance Trade Facilitation

The AEO-reciprocity pact signed in 2025 covers 570 Colombian companies and removes duplicate compliance audits across five economies. Brazil and Argentina activated the AFC PLUS system in 2026, imposing 12-hour targets for green-channel cargo and creating predictable dwell times. Chile integrated certificate-of-origin exchanges with Mexico, Peru, and Colombia, while Peru's VUCE mandates full inter-agency linkage by December 2026. Harmonized processes enlarge the South America customs brokerage market because exporters expand intra-regional trade when clearance risk falls.

Complex & Frequently Changing Tariff Schema

Argentina adjusted Common External Tariff exceptions 14 times in two years, forcing brokers to monitor gazettes daily. Brazil's dual-VAT rollout runs to 2033, so declarations must calculate legacy and new levies in parallel. Colombia will replace criminal sanctions with administrative fines in 2026, increasing audit volume. Frequent rule changes add cost and slow the South America customs brokerage market growth by deterring smaller entrants.

Other drivers and restraints analyzed in the detailed report include:

- Digital Customs-Clearance Platforms (Single Window, Blockchain)

- Near-Shoring of Supply Chains into South America

- High Logistics Costs & Port Congestion

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Air express and general cargo will post a 5.46% CAGR through 2031, even though ocean freight controlled 47.33% of the South America customs brokerage market share in 2025. Small parcels propel the modal shift under the USD 50 Remessa Conforme ceiling and by vaccine consignments that demand 2-to-8 °C chains of custody. IATA's ONE Record adoption hit 22% in 2025, allowing brokers to auto-populate declarations from airline data feeds.

Ocean and sea lanes remain vital for grains, chemicals, and automotive knockdown kits, yet importers increasingly negotiate all-in contracts that bundle freight, insurance, and clearance. Truck and rail flows on trans-Andean corridors use TIR carnets that suspend duties until arrival, a service niche for brokers fluent in land-border inspection rules. As digital-first filing systems mature, the South America customs brokerage market size tied to air express should keep widening.

Freight forwarders and 3PL-integrated operators captured 60.67% of the South America customs brokerage market share because enterprise shippers value a single liability point. On-dock brokerage suites in Santos and Buenos Aires shorten door-to-door cycles and encourage "vendor-managed clearance" contracts. However, pure customs brokers are forecast to grow at 4.88% CAGR by offering audit defense, drawback recovery, and classification advice under Mercosur automotive rules.

Traditional relationship capital with inspectors still matters for yellow-channel cargo, but API-driven entrants now match that advantage by hiring ex-officials and overlaying real-time tariff databases. The South America customs brokerage market, therefore, splits between scale-based service bundles and high-skill advisory retainers.

List of Companies Covered in this Report:

- DHL Global Forwarding

- DSV

- Kuehne + Nagel

- CEVA Logistics (CMA CGM)

- Maersk Customs Services

- UPS Supply Chain Solutions

- Expeditors International

- FedEx Logistics

- Hellmann Worldwide Logistics

- GEODIS

- Rhenus Logistics

- Noatum Logistics

- Yusen Logistics

- TIBA Group

- Grupo RAS

- Allink Transportes

- Aduana Brokerage Services (ABS Group)

- Agunsa

- Ultramar

- FS Agencia de Aduanas

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cross-Border E-Commerce Boom

- 4.2.2 Mercosur & Pacific Alliance Trade Facilitation

- 4.2.3 Digital Customs-Clearance Platforms (Single Window, Blockchain)

- 4.2.4 Near-Shoring of Supply Chains into South America

- 4.2.5 Emergence of Amazonian Free-Trade Zones

- 4.2.6 Carbon-Footprint Disclosure in Customs Paperwork

- 4.3 Market Restraints

- 4.3.1 Complex & Frequently Changing Tariff Schema

- 4.3.2 High Logistics Costs & Port Congestion

- 4.3.3 Patchy Digital-Signature Laws Across Countries

- 4.3.4 Ageing Certified-Broker Talent Pool

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Geo-Political Events

- 4.8 Porter's Five Forces

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Mode of Transport (Value)

- 5.1.1 Ocean / Sea

- 5.1.2 Air (Express and General Cargo)

- 5.1.3 Cross-Border Land (Truck and Rail)

- 5.2 By Broker Type

- 5.2.1 Pure Customs Broker

- 5.2.2 Freight Forwarder / 3PL-Integrated Brokers

- 5.3 By Importer Size

- 5.3.1 Large Enterprisess

- 5.3.2 Mid-Market

- 5.3.3 SMEs / Micro-shippers

- 5.4 By Digital Adoption

- 5.4.1 Traditional Brokerages

- 5.4.2 Digital-first / API-based Brokerages

- 5.5 By End-Use Industry

- 5.5.1 Retail and E-commerce

- 5.5.2 Automotive and EV

- 5.5.3 Electronics and Semiconductors

- 5.5.4 Pharmaceuticals and Life Sciences

- 5.5.5 Aerospace and Defense

- 5.5.6 Chemicals and Industrial Goods

- 5.5.7 Others

- 5.6 By Country

- 5.6.1 Brazil

- 5.6.2 Argentina

- 5.6.3 Chile

- 5.6.4 Colombia

- 5.6.5 Peru

- 5.6.6 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 DHL Global Forwarding

- 6.4.2 DSV

- 6.4.3 Kuehne + Nagel

- 6.4.4 CEVA Logistics (CMA CGM)

- 6.4.5 Maersk Customs Services

- 6.4.6 UPS Supply Chain Solutions

- 6.4.7 Expeditors International

- 6.4.8 FedEx Logistics

- 6.4.9 Hellmann Worldwide Logistics

- 6.4.10 GEODIS

- 6.4.11 Rhenus Logistics

- 6.4.12 Noatum Logistics

- 6.4.13 Yusen Logistics

- 6.4.14 TIBA Group

- 6.4.15 Grupo RAS

- 6.4.16 Allink Transportes

- 6.4.17 Aduana Brokerage Services (ABS Group)

- 6.4.18 Agunsa

- 6.4.19 Ultramar

- 6.4.20 FS Agencia de Aduanas

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment