|

市場調查報告書

商品編碼

2063351

法國的測試、檢定和認證 (TIC):市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031)France Testing, Inspection, And Certification (TIC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

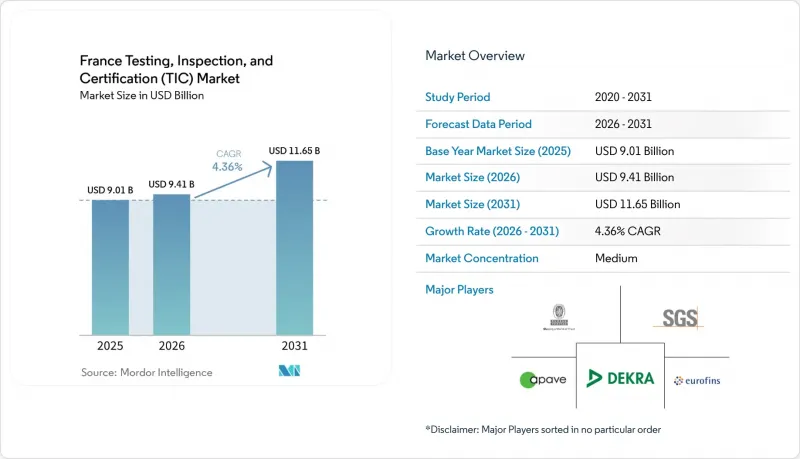

據 Mordor Intelligence 稱,法國測試、檢驗和認證 (TIC) 市場規模預計將從 2025 年的 90.1 億美元成長到 2026 年的 94.1 億美元,到 2031 年達到 116.5 億美元,2026 年至 2031 年的複合年成長率為 4.36%。

本報告按服務類型(測試、檢驗、認證)、採購方式(內部和外包)、行業(消費品和零售、資訊通訊技術和電信、能源和公共產業、化學品和材料、其他)以及服務交付方式(現場、異地/檢查室、其他)進行分類。市場預測以美元計價。

法國檢測、檢驗和認證 (TIC) 市場的趨勢和見解。

歐盟和法國正在迅速增加其監管合規義務。

2024年10月生效的《網路與資訊安全指令2》強制要求超過1萬家法國機構定期進行網路安全審計,違規者將面臨基於全球營業額的處罰。 《網路韌性法》自2026年9月起擴大了連網產品的第三方CE認證範圍,並為測試實驗室提供兩年的準備期。國家協調機制,例如ANSSI的ReCyF框架,正在規範審計清單並對測試實驗室進行認證。 《企業永續發展報告指令》的相應規定要求大型企業在2026年前提供有限保證,並在2028年前提供合理保證,從而促進涵蓋產品安全、網路安全和ESG(環境、社會和治理)檢驗的綜合審計合約的實施。這些法規共同幫助提供多領域項目的供應商維持高且永續的收入來源。

興建氫電池超級工廠的相關需求

Verkor公司位於敦克爾克、耗資15億歐元(17.3億美元)的電池工廠將於2025年12月投產,該項目清晰地展現了電極質量、電解純度和熱失控測試等相關實驗室工作的持續開展。 Lhyfe公司於2025年5月獲得的RFNBO認證表明,第三方認證如何能夠幫助企業獲得多年生產補貼。歐盟委員會於2026年3月制定的綠色氫能計畫預計將涉及多個200兆瓦電解槽的安裝,每個電解槽都需要進行符合ISO 17025標準的分析,以確保氫氣純度、壓力容器完整性和併網安全性。隨著歐盟技術標準的日益嚴格,電池和氫能設施都需要定期重新認證,這將確保對合格評定服務的持續需求。

合格實驗室和熟練審核員短缺

COFRAC於2024年12月修訂了LAB REF 08標準,將認證週期延長至最長24個月,同時,氫氣純度、電池安全和網路安全滲透測試的需求激增。儘管勞動力供應每年僅成長3%,但需求卻以5-6%的速度成長。 Dekra計劃在法國招募1,000名檢驗員,凸顯了人才短缺的現況。此外,諸如2026年啟動的生物樣本庫認證等新項目,進一步加重了監測團隊的負擔。由於大學在ESG保障和物聯網安全方面的課程設置仍然不足,服務提供者不得不從其他公司挖人,或者投資於耗時多年的學徒制項目,這反而會減緩能力建設的步伐。

細分市場分析

2025年,法國檢測、檢驗和認證(TIC)市場主要由檢測領域驅動,佔銷售額的58.94%,這得益於製藥和食品安全等實驗室密集型行業的支撐。然而,預計認證領域的複合年成長率(CAGR)將達到5.12%,成為成長最快的領域。這是因為《網路安全韌性法案》(Cyber Resilience Act)、NIS2法規和《企業永續性發展報告指令》(Corporate Sustainability Reporting Directive)都要求進行第三方認證,而企業內部實驗室無法提供此類認證。因此,預計到2031年,法國TIC市場中認證領域的規模將穩定成長。能夠將上市前測試和上市後監測整合到單一審計服務包中的供應商正在獲得多年期契約,這表明法規正在將認證從成本中心轉變為收入來源。

在高頻抽樣和破壞性測試必不可少的領域,檢測服務仍然至關重要,儘管其成長速度有所放緩。檢測服務透過支援能源、電梯和建築業的資產維護計劃,填補了中間環節的空白。在法國TIC市場,整合這三項服務的混合解決方案市場佔有率不斷成長,這有助於該行業的長期穩定發展。

預計到2025年,外包合約將佔市場佔有率的64.31%,複合年成長率(CAGR)為4.93%,是該細分市場中成長率最高的。法國檢測、檢驗和認證委員會(COFRAC)收緊範圍管理規則,增加了企業內部維持ISO 17025認證的固定成本,導致即使是大型製造商也開始將定期審核外包。因此,隨著大型認證企業將合規相關費用分攤到數百家客戶身上,法國檢測、檢驗和認證(TIC)市場的外部供應商規模逐年擴大。

企業內部團隊仍僅限於高度專利技術和機密性的任務,例如航太領域的故障分析和藥物配方研究。然而,即使是這些公司也開始將定期法定審計外包,以降低人事費用。第五代專用網路實現了遠端檢驗,削弱了現場檢查員曾經擁有的優勢。預計在預測期內,法國技術資訊通訊技術(TIC)市場中企業內部服務的佔有率將逐步下降。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 歐盟和法國正在迅速增加其監管合規義務。

- 大型企業將資訊通訊技術職能外包

- 對永續性/ESG檢驗的需求

- 數位設備的激增和網路安全測試

- 氫電池超級工廠的建造需求

- 引入利用5G技術的遠端和數位化檢測

- 市場限制因素

- 合格檢測實驗室和熟練審核員短缺

- 中小企業高額TIC費用的價格彈性

- 環境法規的區域差異(ZFE-m 等)

- 策略性產業保護主義導致核准延誤

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 對與市場相關的宏觀經濟趨勢進行評估

第5章 市場規模與成長預測

- 按服務類型

- 測試

- 檢查

- 認證

- 透過採購方式

- 內部

- 外包

- 按行業

- 消費品和零售

- 資訊通訊技術/通訊

- 汽車和運輸業

- 航太/國防

- 石油、天然氣、石油化學產品

- 能源與公共產業

- 工業製造和機械

- 化學/材料

- 建設基礎設施

- 生命科學與醫療保健

- 食品/農業/飲料

- 其他行業領域

- 按服務交付方式

- 現場

- 異地/檢查室

- 遠端/數位

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Bureau Veritas SA

- SGS France SAS

- Apave SA

- Dekra SE France

- Eurofins Scientific SE

- Intertek France SAS

- SOCOTEC SA

- TUV SUD France SAS

- TUV Rheinland France SARL

- TUV Nord France SAS

- ALS France SARL

- Element Materials Technology France

- Kiwa France SAS

- Applus+France SAS

- DNV France SAS

- Lloyd's Register Emea Branch France

- UL Solutions France SARL

- BSI Group France SAS

- Control Union France

- Cotecna Inspection France

- AFNOR Certification

第7章 市場機會與未來展望

According to Mordor Intelligence, the france testing, inspection, and certification (TIC) market size is expected to increase from USD 9.01 billion in 2025 to USD 9.41 billion in 2026 and reach USD 11.65 billion by 2031, growing at a CAGR of 4.36% over 2026-2031.

This report is Segmented by Service Type (Testing, Inspection, and Certification), Sourcing Type (In-House and Outsourced), Industry Vertical (Consumer Goods and Retail, ICT and Telecom, Energy and Utilities, Chemicals and Materials, and More ), and Mode of Service Delivery (On-Site, Off-Site Laboratory, and More). The Market Forecasts are Provided in Terms of Value (USD).

France Testing, Inspection, And Certification (TIC) Market Trends and Insights

Mandatory EU And French Regulatory Compliance Surge

The Network and Information Security Directive 2, which took effect in October 2024, obliges more than 10,000 French organizations to commission periodic cybersecurity audits, with fines tied to global turnover for non-compliance. The Cyber Resilience Act extends third-party CE-mark assessments to connected products from September 2026, creating a two-year capacity-build window for laboratories. National alignment efforts, such as ANSSI's ReCyF framework, have standardized audit checklists, accelerating accreditation of inspection bodies. Parallel obligations under the Corporate Sustainability Reporting Directive require limited assurance for large firms by 2026 and reasonable assurance by 2028, driving integrated audit contracts that bundle product safety, cybersecurity, and ESG verification. Together, these rules sustain high recurring revenue for providers able to deliver multidisciplinary programs.

Hydrogen and Battery Gigafactory Build-Out Needs

Verkor's EUR 1.5 billion (USD 1.73 billion) Dunkirk battery plant, inaugurated in December 2025, illustrates the recurring laboratory workload attached to electrode quality, electrolyte purity, and thermal-runaway testing. Lhyfe's RFNBO certification in May 2025 shows how third-party attestations unlock multi-year production subsidies. The European Commission's March 2026 green-hydrogen scheme foresees several 200 megawatt electrolyzers, each demanding ISO 17025-accredited analyses of hydrogen purity, pressure-vessel integrity, and grid-connection safety. Both battery and hydrogen facilities require periodic re-certification as EU technical standards tighten, guaranteeing a durable pipeline for conformity services.

Shortage of Accredited Labs and Skilled Auditors

COFRAC's December 2024 LAB REF 08 revision lengthened accreditation cycles to as much as 24 months, coinciding with surging demand for hydrogen purity, battery safety, and cybersecurity penetration tests. Labor supply grows only 3% annually, versus 5-6% demand growth. Dekra's plan to recruit 1,000 inspectors in France highlights the talent gap, while new programs such as the 2026 biobank accreditation stretch surveillance teams thinner. Universities have yet to scale curricula in ESG assurance or IoT security, forcing providers to poach staff or fund multi-year apprenticeships that delay capacity relief.

Other drivers and restraints analyzed in the detailed report include:

- Sustainability and ESG Verification Demand

- Digital-Device Proliferation and Cybersecurity Testing

- SME Price-Sensitivity to Premium TIC Fees

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Testing dominated the France testing, inspection, and certification market with 58.94% revenue in 2025, anchored by laboratory-intensive fields such as pharmaceuticals and food safety. Certification, however, is poised for the strongest 5.12% CAGR because the Cyber Resilience Act, NIS2, and the Corporate Sustainability Reporting Directive all stipulate third-party attestations that in-house labs cannot deliver. The France TIC market size for certification is therefore set to expand steadily through 2031. Providers able to combine pre-market tests with post-market surveillance inside a single audit package are winning multi-year contracts, evidencing how regulation converts certification from a cost center into a revenue enabler.

Testing remains indispensable where high-frequency sampling or destructive assays are mandatory, yet its growth is steadier. Inspection services fill the middle ground by supporting asset-integrity programs in energy, elevators and construction. The emerging France TIC market share for hybrid solutions that blend all three services underpins the sector's long-run stability.

Outsourced contracts held 64.31% share in 2025 and are forecast to climb at a 4.93% CAGR, the fastest in this segmentation. Tightened COFRAC scope-management rules have raised the fixed cost of maintaining in-house ISO 17025 accreditation, prompting even large manufacturers to shift routine audits outside. The France testing, inspection, and certification (TIC) market size captured by external providers therefore widens each year as accredited majors spread compliance overhead across hundreds of clients.

In-house teams persist only for proprietary or classified work, such as aerospace failure analysis or pharmaceutical formulation studies. Yet even these actors outsource periodic legal audits to reduce payroll costs. Private five-generation networks enable remote verification, shrinking the advantage once held by resident inspectors. Over the forecast horizon, the France TIC market share of in-house services is expected to erode incrementally.

List of Companies Covered in this Report:

- Bureau Veritas SA

- SGS France SAS

- Apave SA

- Dekra SE France

- Eurofins Scientific SE

- Intertek France SAS

- SOCOTEC SA

- TUV SUD France SAS

- TUV Rheinland France SARL

- TUV Nord France SAS

- ALS France SARL

- Element Materials Technology France

- Kiwa France SAS

- Applus + France SAS

- DNV France SAS

- Lloyd's Register Emea Branch France

- UL Solutions France SARL

- BSI Group France SAS

- Control Union France

- Cotecna Inspection France

- AFNOR Certification

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mandatory EU and French Regulatory Compliance Surge

- 4.2.2 Outsourcing of TIC Functions by Large Enterprises

- 4.2.3 Sustainability/ESG Verification Demand

- 4.2.4 Digital-Device Proliferation and Cybersecurity Testing

- 4.2.5 Hydrogen and Battery Gigafactory Build-Out Needs

- 4.2.6 5G-Enabled Remote/Digital Inspections Adoption

- 4.3 Market Restraints

- 4.3.1 Shortage of Accredited Labs and Skilled Auditors

- 4.3.2 SME Price-Sensitivity to Premium TIC Fees

- 4.3.3 Patch-work local environmental rules (ZFE-m etc.)

- 4.3.4 Strategic Sector Protectionism Delaying Approvals

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Testing

- 5.1.2 Inspection

- 5.1.3 Certification

- 5.2 By Sourcing Type

- 5.2.1 In-house

- 5.2.2 Outsourced

- 5.3 By Industry Vertical

- 5.3.1 Consumer Goods and Retail

- 5.3.2 ICT and Telecom

- 5.3.3 Automotive and Transportation

- 5.3.4 Aerospace and Defense

- 5.3.5 Oil, Gas and Petrochemicals

- 5.3.6 Energy and Utilities

- 5.3.7 Industrial Manufacturing and Machinery

- 5.3.8 Chemicals and Materials

- 5.3.9 Construction and Infrastructure

- 5.3.10 Life Sciences and Healthcare

- 5.3.11 Food, Agriculture and Beverage

- 5.3.12 Others Industry Verticals

- 5.4 By Mode of Service Delivery

- 5.4.1 On-site

- 5.4.2 Off-site / Laboratory

- 5.4.3 Remote / Digital

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Bureau Veritas SA

- 6.4.2 SGS France SAS

- 6.4.3 Apave SA

- 6.4.4 Dekra SE France

- 6.4.5 Eurofins Scientific SE

- 6.4.6 Intertek France SAS

- 6.4.7 SOCOTEC SA

- 6.4.8 TUV SUD France SAS

- 6.4.9 TUV Rheinland France SARL

- 6.4.10 TUV Nord France SAS

- 6.4.11 ALS France SARL

- 6.4.12 Element Materials Technology France

- 6.4.13 Kiwa France SAS

- 6.4.14 Applus + France SAS

- 6.4.15 DNV France SAS

- 6.4.16 Lloyd's Register Emea Branch France

- 6.4.17 UL Solutions France SARL

- 6.4.18 BSI Group France SAS

- 6.4.19 Control Union France

- 6.4.20 Cotecna Inspection France

- 6.4.21 AFNOR Certification

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

測試、檢驗和認證市場:2026-2032年全球市場預測(按服務類型、採購方式、技術、合規要求、應用、組織規模和最終用戶行業分類)證書測試市場:2026-2032年全球市場預測(依測試服務、階段、產業、部署類型、最終用戶和組織規模分類)

測試、檢驗和認證市場:2026-2032年全球市場預測(按服務類型、採購方式、技術、合規要求、應用、組織規模和最終用戶行業分類)證書測試市場:2026-2032年全球市場預測(依測試服務、階段、產業、部署類型、最終用戶和組織規模分類) 印度測試、檢驗和認證 (TIC) 市場:市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031)

印度測試、檢驗和認證 (TIC) 市場:市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031) 2026-2030年全球人工智慧測試與檢驗市場

2026-2030年全球人工智慧測試與檢驗市場 2026 年至 2035 年測試、檢驗和認證服務市場的商業機會、成長要素、產業趨勢和預測。

2026 年至 2035 年測試、檢驗和認證服務市場的商業機會、成長要素、產業趨勢和預測。 測試、檢驗和認證市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、流程、部署模式、最終用戶和解決方案分類

測試、檢驗和認證市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、流程、部署模式、最終用戶和解決方案分類 服飾、鞋類和皮革製品 (AFL) 的檢測、檢驗和認證 (TIC) 市場:按服務類型、行業和地區分類測試、檢驗和認證 (TIC) 市場:按類型、行業和地區分類

服飾、鞋類和皮革製品 (AFL) 的檢測、檢驗和認證 (TIC) 市場:按服務類型、行業和地區分類測試、檢驗和認證 (TIC) 市場:按類型、行業和地區分類 測試、檢查和認證市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區的洞察,2026-2034年的預測

測試、檢查和認證市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區的洞察,2026-2034年的預測 自主測試與檢驗系統市場預測至2034年:按組件、測試類型、組織規模、部署模式、最終用戶和地區分類的全球分析

自主測試與檢驗系統市場預測至2034年:按組件、測試類型、組織規模、部署模式、最終用戶和地區分類的全球分析