|

市場調查報告書

商品編碼

2038375

2026 年至 2035 年測試、檢驗和認證服務市場的商業機會、成長要素、產業趨勢和預測。Testing, Inspection and Certification (TIC) Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

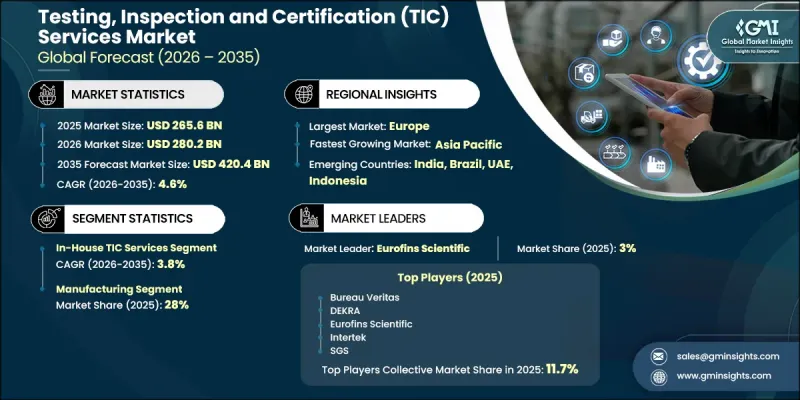

2025 年全球測試、檢驗和認證 (TIC) 服務市值為 2,656 億美元,預計到 2035 年將以 4.6% 的複合年成長率成長至 4,204 億美元。

全球對產品安全、合規性和品質保證的日益重視,是推動該市場成長的主要動力,尤其是在製造業、能源、運輸和消費品等關鍵產業。測試、檢驗和檢驗流程的需求也與日俱增。各行業監管的日益複雜和合規標準的日益嚴格,促使企業更加依賴第三方 TIC 服務提供者進行公正的評估和文件編制。此外,不斷提高的永續性要求和環境法規也推動了測試和認證需求的成長。風險緩解、營運透明度和產品可靠性的日益重要性進一步刺激了市場需求。持續的工業化、技術進步和跨境貿易活動的拓展,共同推動了 TIC 服務產業的長期成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 2656億美元 |

| 預測金額 | 4204億美元 |

| 複合年成長率 | 4.6% |

到2025年,測試服務業將佔據51%的市場。該行業在製造業、醫療產業和消費品行業中應用廣泛,因為在這些行業中,準確的產品檢驗和合規性確認至關重要。監管機構會對測試流程進行例行監控和檢驗,以確保其在各種應用中的準確性、一致性和符合相關標準。

預計2026年至2035年間,企業內部檢測、合規和認證(TIC)服務市場將以3.8%的複合年成長率成長。許多企業正優先發展內部TIC能力,以加強對品質保證流程的控制、提升資料保密性並縮短前置作業時間。投資內部檢測基礎設施的企業通常會將資源投入先進的實驗室、專用設備和熟練的技術人員。在製藥、航太和汽車製造等法規結構,企業不斷擴展其內部合規能力,以滿足不斷變化的安全和品質標準。

預計到2025年,美國測試、檢驗和認證(TIC)服務市場規模將達到651億美元。製造業是推動這項強勁需求的主要力量,因為TIC服務對於確保產品可靠性、合規性和營運效率至關重要。電子、汽車和機械等行業高度依賴認證和檢驗流程來滿足國內和國際標準。政府法律規範的不斷加強也持續推高合規要求,從而支撐了美國各地對TIC服務的持續需求。

目錄

第1章:調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率分析

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 加強對產品安全和品質法規的嚴格執行

- 新興國家的工業化進程和製造業產出成長

- 消費者對認證和永續產品的意識和需求日益增強

- 引入數位化和遠端檢測技術(人工智慧、物聯網、區塊鏈)

- 產業潛在風險與挑戰

- 複雜的測試環境會帶來高昂的營運和服務成本。

- 各地區認證標準存在差異

- 市場機遇

- 拓展TIC服務在可再生能源、電動車和綠色科技領域的應用。

- 網路安全和數位系統認證的需求日益成長

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 美國職業安全與健康管理局 (OSHA) 國家認可實驗室 (NRTL) 計畫要求

- 美國國家標準與技術研究院 (NIST) 和美國國家標準協會 (ANSI) 制定的實驗室認證和計量標準

- EPA 和 FDA 對環境和生命科學測試的監管合規框架

- CPSC 安全標準和 FCC 電磁相容性 (EMC) 法規

- 獲得加拿大標準委員會 (SCC) 和加拿大衛生署產品安全法規的認證

- 歐洲

- 歐盟關於認證和市場監管的第765/2008號條例

- CE標誌指令(機械、低電壓、電磁相容性和醫療設備)

- 歐盟企業永續發展報告指令(CSRD)與強制性ESG檢驗

- REACH 和 RoHS 對化學物質和有害物質的監管

- 歐洲認可(EA)跨境實驗室有效性多邊協議

- 亞太地區

- 中國強制產品認證(CCC)和CNAS實驗室認可條例

- 日本工業標準(JIS)和PSE標誌顯示電氣設備的安全性。

- 印度的BIS(印度標準局)和NABL認證框架

- 東協化妝品、電子設備和藥品管理體制的統一化

- 澳洲及紐西蘭聯合標準及安全認證標準(AS/NZS)

- 拉丁美洲

- 巴西國家計量、品質和技術研究院 (Inmetro) 認證規則

- 墨西哥NOM(Normas Oficiales Mexicanas)和EMA認證標準

- IRAM 安全認證和 OAA 實驗室在阿根廷的認可。

- 南方共同市場工業產品與消費品區域標準化協定

- 中東和非洲

- GCC標準化組織(GSO)和G-Mark認證要求

- 沙烏地阿拉伯的SASO和SABER平台合格評定法規

- 阿拉伯聯合大公國工業和先進技術部 (MoIAT) 產品安全計劃

- 南非的 SANAS 認證和 SABS 技術品質標準

- 非洲標準化組織(ARSO)制定的洲內貿易框架

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析

- 按玩家類型分類的定價策略

- 專利分析(基於初步研究)

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- GenAI 各細分市場的應用案例與部署藍圖

- 風險、限制和監管考量

- 永續性和環境方面

- 碳足跡評估

- 融入循環經濟

- 電子廢棄物管理要求

- 綠色製造舉措

- 預測假設和情境分析(基於初步研究)

- 基本案例-驅動複合年成長率的關鍵宏觀經濟與產業變量

- 樂觀情境-宏觀經濟與產業的順風

- 悲觀情景-宏觀經濟放緩或產業逆風

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲(MEA)

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場估計與預測:依服務業分類,2022-2035年

- 測試服務

- 電磁相容性測試

- 電氣安全和性能測試

- 機械和材料測試

- 其他

- 檢查服務

- 裝運前檢驗和合約檢驗

- 工業設施和設備的檢查

- 建築和基礎設施檢查

- 其他

- 身份驗證服務

- 產品認證

- 管理系統認證

- 人才認證

- 其他

- 校對服務

- 測量儀器的校準

- 測量和測量標準

- 其他

- 其他

第6章 市場估計與預測:依採購方式分類,2022-2035年

- 內部TIC服務

- 內部測試和品管實驗室

- 內部檢驗和認證部門

- 企業研發和合規性測試中心

- 其他

- 外包TIC服務

- 獨立第三方TIC提供者

- 合約檢測實驗室

- 外部檢驗和認證機構

- 其他

第7章 市場估計與預測:依最終用途分類,2022-2035年

- 製造業

- 工業機械和設備的測試

- 品管和工廠審核

- 供應鍊和零件檢驗

- 能源與公共產業

- 可再生能源系統測試

- 智慧電網和電池認證

- 核能發電廠安全檢查

- 評估油氣資產健康狀況

- 食品/飲料

- 食品安全和衛生檢測

- 包裝和標籤合規性

- 供應鏈可追溯性和原產地檢驗

- 有機和永續發展認證

- 車

- 電動汽車測試和認證

- 自動駕駛車輛的驗證

- 聯網汽車的網路安全測試

- 車輛檢驗和型式認可

- 化學品

- 化學成分和純度測試

- 危險物質認證

- 環境和監管合規性審計

- 建築和基礎設施

- 建築材料測試

- 結構完整性檢查

- 綠建築與永續發展認證

- 醫療保健和生命科學

- 生物相容性和滅菌測試

- 藥物驗證和臨床試驗

- 醫療設備和軟體的驗證

- 航太/國防

- 飛機零件認證

- 國防系統和軍事標準測試

- 航太系統認證

- 消費品

- 電氣產品安全測試

- 玩具、紡織品和化妝品的認證

- 消費者保護和品質保證

- 其他

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲(MEA)

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- 世界公司

- Bureau Veritas

- DEKRA

- DNV

- Eurofins Scientific

- Intertek

- SGS

- TUV Rheinland

- TUV SUD

- 該地區的領先企業

- APAVE

- BSI

- Centre Testing International

- CCIC

- CSA

- Lloyd's Register

- SOCOTEC

- UL Solutions

- 新興企業和專業公司

- ALS

- Applus+Services

- Element Materials Technology Group

- Kiwa

- NSF International

- QIMA

- RINA

The Global Testing, Inspection and Certification (TIC) Services Market was valued at USD 265.6 billion in 2025 and is estimated to grow at a CAGR of 4.6% to reach USD 420.4 billion by 2035.

The market growth is strongly supported by rising global emphasis on product safety, regulatory compliance, and quality assurance across key industries such as manufacturing, energy, transportation, and consumer goods. TIC services play a critical role in ensuring that products meet domestic and international regulatory requirements before entering global supply chains. Increasing globalization of trade has further strengthened the need for standardized certification and independent verification processes. Growing regulatory complexity and tightening compliance norms across industries are pushing organizations to rely more on third-party TIC providers for unbiased assessment and documentation. In addition, expanding sustainability requirements and environmental regulations are contributing to higher testing and certification volumes. The rising importance of risk mitigation, operational transparency, and product reliability is further reinforcing demand. Continuous industrialization, technological advancement, and expansion of cross-border trade activities are collectively sustaining long-term growth momentum across the TIC services industry.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $265.6 Billion |

| Forecast Value | $420.4 Billion |

| CAGR | 4.6% |

The testing services segment accounted for 51% share in 2025. This segment remains widely used across manufacturing, healthcare, and consumer goods industries, where accurate product validation and compliance verification are essential. Testing processes are routinely monitored and validated by regulatory bodies to ensure accuracy, consistency, and adherence to required standards across various applications.

The in-house TIC services segment is expected to grow at a CAGR of 3.8% from 2026 to 2035. Many organizations prefer internal TIC capabilities to maintain greater control over quality assurance processes, improve data confidentiality, and reduce turnaround time. Companies investing in in-house testing infrastructure typically allocate resources toward advanced laboratories, specialized equipment, and skilled technical personnel. Industries operating under strict regulatory frameworks, including pharmaceuticals, aerospace, and automotive manufacturing, continue to expand internal compliance capabilities to meet evolving safety and quality standards.

U.S. Testing, Inspection and Certification (TIC) Services Market generated USD 65.1 billion in 2025. Strong demand is driven by the manufacturing sector, where TIC services are essential for ensuring product reliability, regulatory compliance, and operational efficiency. Industries such as electronics, automotive, and machinery rely heavily on certification and inspection processes to meet domestic and international standards. Regulatory oversight by government bodies continues to reinforce compliance requirements, supporting sustained demand for TIC services across the country.

Major players operating in the Global Testing, Inspection and Certification (TIC) Services Industry include Bureau Veritas, SGS, Intertek, TUV SUD, TUV Rheinland, DNV, Eurofins Scientific, UL Solutions, Applus+, and DEKRA. Companies in the Global Testing, Inspection And Certification (TIC) Services are focusing on expanding their global service networks to strengthen client accessibility and operational reach. Strategic investments in digital inspection technologies, automation, and data analytics are enhancing efficiency and accuracy in service delivery. Firms are also increasing laboratory capacity and upgrading testing infrastructure to meet rising demand across industries. Mergers and acquisitions are being actively pursued to broaden service portfolios and strengthen geographic presence. Additionally, organizations are prioritizing industry-specific certification expertise to cater to complex regulatory requirements.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.4 Research trail & confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Service

- 2.2.3 Sourcing

- 2.2.4 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing enforcement of stringent product safety and quality regulations

- 3.2.1.2 Rising industrialization and manufacturing output in emerging economies

- 3.2.1.3 Increased consumer awareness and demand for certified, sustainable products

- 3.2.1.4 Adoption of digital and remote inspection technologies (AI, IoT, blockchain)

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High operational and service costs for complex testing environments

- 3.2.2.2 Variability in certification standards across regions

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of TIC services in renewable energy, EVs, and green technologies

- 3.2.3.2 Growing demand for cybersecurity and digital system certification

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S. OSHA Nationally Recognized Testing Laboratory (NRTL) program requirements

- 3.4.1.2 NIST and ANSI laboratory accreditation and metrology standards

- 3.4.1.3 EPA and FDA regulatory compliance frameworks for environmental and life sciences testing

- 3.4.1.4 CPSC safety standards and FCC electromagnetic compatibility (EMC) regulations

- 3.4.1.5 Canada Standards Council (SCC) accreditation and Health Canada product safety rules

- 3.4.2 Europe

- 3.4.2.1 EU Regulation (EC) No 765/2008 for accreditation and market surveillance

- 3.4.2.2 CE Marking directives (Machinery, Low Voltage, EMC, and Medical Devices)

- 3.4.2.3 EU Corporate Sustainability Reporting Directive (CSRD) and ESG verification mandates

- 3.4.2.4 REACH and RoHS chemical substances and hazardous material restrictions

- 3.4.2.5 EA (European Accreditation) multilateral agreements for cross-border laboratory validity

- 3.4.3 Asia Pacific

- 3.4.3.1 China Compulsory Certification (CCC) and CNAS laboratory accreditation rules

- 3.4.3.2 Japan Industrial Standards (JIS) and PSE mark for electrical appliance safety

- 3.4.3.3 India BIS (Bureau of Indian Standards) and NABL accreditation frameworks

- 3.4.3.4 ASEAN harmonized regulatory regimes for cosmetics, electronics, and pharmaceuticals

- 3.4.3.5 Australia and New Zealand (AS/NZS) joint standards and safety certification codes

- 3.4.4 Latin America

- 3.4.4.1 Brazil Inmetro (National Institute of Metrology, Quality and Technology) certification rules

- 3.4.4.2 Mexico NOM (Normas Oficiales Mexicanas) and EMA accreditation standards

- 3.4.4.3 Argentina IRAM safety certification and OAA laboratory accreditation

- 3.4.4.4 Mercosur regional standardization agreements for industrial and consumer goods

- 3.4.5 Middle East & Africa

- 3.4.5.1 GCC Standardization Organization (GSO) and G-Mark certification requirements

- 3.4.5.2 Saudi Arabia SASO and SABER platform conformity assessment regulations

- 3.4.5.3 UAE MoIAT (Ministry of Industry and Advanced Technology) product safety schemes

- 3.4.5.4 South Africa SANAS accreditation and SABS technical quality standards

- 3.4.5.5 African Organization for Standardisation (ARSO) intra-continental trade frameworks

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 Pestel analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Pricing Analysis (Driven by primary research)

- 3.8.1 Historical Price Trend Analysis

- 3.8.2 Pricing Strategy by Player Type

- 3.9 Patent analysis (Driven by primary research)

- 3.10 Impact of AI and Generative AI on the Market

- 3.10.1 AI Driven Disruption of Existing Business Models

- 3.10.2 GenAI Use Cases and Adoption Roadmap by Segment

- 3.10.3 Risks Limitations and Regulatory Considerations

- 3.11 Sustainability & environmental aspects

- 3.11.1 Carbon Footprint Assessment

- 3.11.2 Circular Economy Integration

- 3.11.3 E-Waste Management Requirements

- 3.11.4 Green Manufacturing Initiatives

- 3.12 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.12.1 Base Case- Key Macro & Industry Variables Driving CAGR

- 3.12.2 Optimistic Scenarios- Favorable macro and industry tailwinds

- 3.12.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Service, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 Testing Services

- 5.2.1 Electromagnetic compatibility testing

- 5.2.2 Electrical safety and performance testing

- 5.2.3 Mechanical and materials testing

- 5.2.4 Others

- 5.3 Inspection Services

- 5.3.1 Pre-shipment and consignment inspection

- 5.3.2 Industrial site and equipment inspection

- 5.3.3 Construction and infrastructure inspection

- 5.3.4 Others

- 5.4 Certification Services

- 5.4.1 Product certification

- 5.4.2 Management system certification

- 5.4.3 Personnel certification

- 5.4.4 Others

- 5.5 Calibration Services

- 5.5.1 Instrument calibration

- 5.5.2 Metrology and measurement standards

- 5.5.3 Others

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Sourcing, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 In-House TIC Services

- 6.2.1 Internal testing and quality control laboratories

- 6.2.2 Captive inspection and certification departments

- 6.2.3 Corporate R&D and compliance testing centers

- 6.2.4 Others

- 6.3 Outsourced TIC Services

- 6.3.1 Independent third-party TIC providers

- 6.3.2 Contract-based testing laboratories

- 6.3.3 External inspection and certification bodies

- 6.3.4 Others

Chapter 7 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 Manufacturing

- 7.2.1 Industrial machinery and equipment testing

- 7.2.2 Quality control and factory audits

- 7.2.3 Supply chain and component verification

- 7.3 Energy and Utilities

- 7.3.1 Renewable energy system testing

- 7.3.2 Smart grid and battery certification

- 7.3.3 Nuclear plant safety inspection

- 7.3.4 Oil and gas asset integrity assessments

- 7.4 Food and Beverages

- 7.4.1 Food safety and hygiene testing

- 7.4.2 Packaging and labeling compliance

- 7.4.3 Supply chain traceability and origin verification

- 7.4.4 Organic and sustainability certifications

- 7.5 Automotive

- 7.5.1 Electric vehicle testing and certification

- 7.5.2 Autonomous vehicle validation

- 7.5.3 Connected car cybersecurity testing

- 7.5.4 Vehicle inspection and homologation

- 7.6 Chemicals

- 7.6.1 Chemical composition and purity testing

- 7.6.2 Hazardous material certification

- 7.6.3 Environmental and regulatory compliance audits

- 7.7 Construction and Infrastructure

- 7.7.1 Building materials testing

- 7.7.2 Structural integrity inspections

- 7.7.3 Green building and sustainability certification

- 7.8 Healthcare and Life Sciences

- 7.8.1 Biocompatibility and sterilization testing

- 7.8.2 Pharmaceutical and clinical trial validation

- 7.8.3 Medical device and software validation

- 7.9 Aerospace and Defense

- 7.9.1 Aviation component certification

- 7.9.2 Defense system and military standards testing

- 7.9.3 Space system qualification

- 7.10 Consumer Products

- 7.10.1 Electrical appliance safety testing

- 7.10.2 Toy, textile, and cosmetic certification

- 7.10.3 Consumer protection and quality assurance

- 7.11 Others

Chapter 8 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 US

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Nordics

- 8.3.7 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Southeast Asia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Players

- 9.1.1 Bureau Veritas

- 9.1.2 DEKRA

- 9.1.3 DNV

- 9.1.4 Eurofins Scientific

- 9.1.5 Intertek

- 9.1.6 SGS

- 9.1.7 TUV Rheinland

- 9.1.8 TUV SUD

- 9.2 Regional Champions

- 9.2.1 APAVE

- 9.2.2 BSI

- 9.2.3 Centre Testing International

- 9.2.4 CCIC

- 9.2.5 CSA

- 9.2.6 Lloyd's Register

- 9.2.7 SOCOTEC

- 9.2.8 UL Solutions

- 9.3 Emerging Players & Specialists

- 9.3.1 ALS

- 9.3.2 Applus+ Services

- 9.3.3 Element Materials Technology Group

- 9.3.4 Kiwa

- 9.3.5 NSF International

- 9.3.6 QIMA

- 9.3.7 RINA

2026-2030年全球人工智慧測試與檢驗市場

2026-2030年全球人工智慧測試與檢驗市場 測試、檢驗和認證市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、流程、部署模式、最終用戶和解決方案分類

測試、檢驗和認證市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、流程、部署模式、最終用戶和解決方案分類 測試、檢查和認證市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區的洞察,2026-2034年的預測

測試、檢查和認證市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區的洞察,2026-2034年的預測 自主測試與檢驗系統市場預測至2034年:按組件、測試類型、組織規模、部署模式、最終用戶和地區分類的全球分析

自主測試與檢驗系統市場預測至2034年:按組件、測試類型、組織規模、部署模式、最終用戶和地區分類的全球分析 2026年全球測試、檢驗和認證市場報告

2026年全球測試、檢驗和認證市場報告 全球測試、檢驗和認證 (TIC) 市場:按服務類型、來源和應用分類 - 預測(至 2031 年)

全球測試、檢驗和認證 (TIC) 市場:按服務類型、來源和應用分類 - 預測(至 2031 年) 測試與試運行市場報告:按服務類型、試運行類型、採購方式、最終用戶行業和地區分類(2026-2034 年)

測試與試運行市場報告:按服務類型、試運行類型、採購方式、最終用戶行業和地區分類(2026-2034 年) 熱交換器檢測服務市場規模、佔有率和成長分析:按檢測技術、應用和地區分類-2026-2033年產業預測2026年全球醫療設備測試、檢驗及認證市場報告

熱交換器檢測服務市場規模、佔有率和成長分析:按檢測技術、應用和地區分類-2026-2033年產業預測2026年全球醫療設備測試、檢驗及認證市場報告 全球測試、檢驗和認證 (TIC) 市場:按服務類型、解決方案類型、應用、最終用戶和地區分類 - 市場規模、行業趨勢、機會分析和預測 (2026–2035)

全球測試、檢驗和認證 (TIC) 市場:按服務類型、解決方案類型、應用、最終用戶和地區分類 - 市場規模、行業趨勢、機會分析和預測 (2026–2035)