|

市場調查報告書

商品編碼

2072625

日本的測試、檢定和認證 (TIC):市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031)Japan Testing, Inspection, And Certification (TIC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

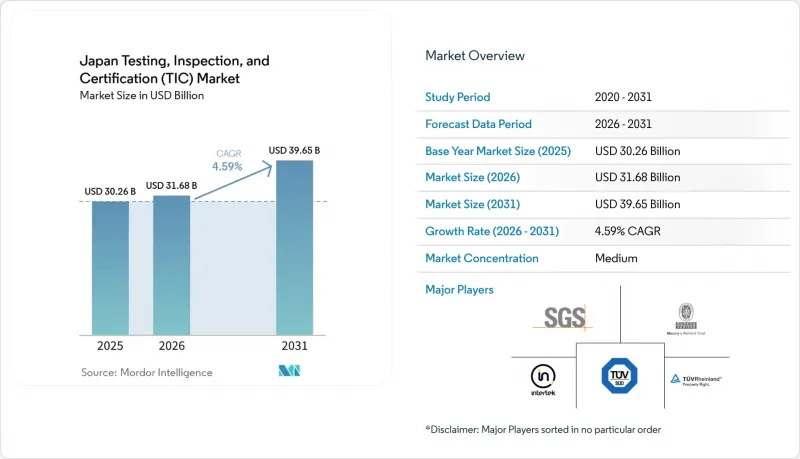

根據 Mordor Intelligence 預測,日本測試、檢驗和認證 (TIC) 市場規模預計將從 2025 年的 302.6 億美元成長到 2026 年的 316.8 億美元,到 2031 年將達到 396.5 億美元,2026 年至 2031 年的複合年成長率為 4.5%。

本報告按服務類型(測試、檢驗、認證)、採購方式(內部和外包)、行業(消費品和零售、資訊通訊技術和電信、汽車和交通運輸以及其他)以及服務交付方式(現場、異地測試設施、遠端/數位化)進行分類。市場預測以美元計價。

日本測試、檢驗和認證 (TIC) 市場的趨勢和洞察

汽車、生命科學和環境領域的監管正變得越來越嚴格。

根據聯合國第155號條例,新車必須通過網路安全審計;再生醫學的贊助商必須提交24個月的真實世界證據;公共產業則面臨PFAS(全氟烷基和多氟烷基物質)微量排放的監管限制。這些相互重疊的監管要求擴大了合規範圍,縮短了核准時間,促使企業將更多預算分配給成熟的檢測實驗室。市場領導者正利用其ISO 17025和ISO 17065認證來獲取多年期契約,進一步鞏固了認證機構在日本檢測、檢驗和認證(TIC)市場的主導地位。

電動車和先進交通工具的安全要求

2025年至2027年間,所有鋰離子電池模組必須具備5分鐘熱失控抑制能力,ADAS演算法必須通過ISO 23792和ISO 34502場景測試,車輛控制器則需要進行滲透測試。汽車製造商正將檢驗支出從內燃機系統轉向高壓、高數據速率平台,這推動了對耐濫用檢查室和造價300萬至500萬美元的800伏消音室的需求成長。因此,日本整體測試、檢驗和認證(TIC)市場對電池、雷達和網路安全的專業訂單激增。日本在汽車製造和下一代行動旅遊技術領域的強大地位,進一步加速了對先進測試基礎設施的投資。電動車和軟體定義汽車產量的不斷成長,推動了對專業認證服務的需求,從而支撐了TIC市場的持續成長。

資本密集先進實驗設施及熟練人員短缺

建造消音室和GMP潔淨室需要500萬至1500萬美元的資本支出,這對新進業者構成了巨大的准入門檻,也給中型檢測實驗室帶來了壓力,因為此類投資需要大量資金和長期規劃。儘管預計到2030年將出現500名工程師的缺口,但各公司仍在加速推動自動化,以應對人才短缺並提高營運效率。然而,實施自動化技術的高成本以及對現有員工進行大規模再培訓的需求,阻礙了這些工作的快速擴展。此外,由於資源有限且需求不斷成長,產能限制也延長了測試、檢驗和認證(TIC)流程所需的時間。由於各公司難以有效率地滿足市場需求,這些延誤正在對日本測試、檢驗和認證(TIC)市場的整體成長潛力產生負面影響。

細分市場分析

預計到2025年,測試業務將佔銷售額的58.23%,主要得益於破壞性測試(電池濫用測試)、生物等效性測試和微生物檢測等高價值訂單的成長。同時,認證業務預計將超越測試業務,以5.26%的複合年成長率成長,這主要得益於對氫能站、離岸風力發電機和符合快速核准條件的醫療設備等第三方認證標誌的需求。日本測試、資訊和認證(TIC)市場正經歷顯著成長,這主要得益於可再生能源和醫療技術領域的進步。此外,監管標準與國際標準的日益趨同以及跨境產品產品核可的增加也進一步推動了這一發展,從而提升了全球認可的認證機構的重要性。

隨著自願性生態標章和貸款機構實質審查要求的盡職調查報告日益普及,定期監測審核的重要性也隨之提升,檢測實驗室正將重心轉向基於ISO 19870標準的氫能和可再生能源認證。儘管這項轉變將逐步改變收費格局,但預計到2031年,檢測業務仍將是日本檢測、檢驗和認證(TIC)市場中規模最大的細分領域。日本的國家氫能戰略進一步推動了對氫氣生產、儲存和可再生能源基礎設施項目認證的需求。同時,跨境能源交易要求的不斷提高以及脫碳報告框架的日益嚴格,也迫使TIC服務提供者拓展其在整個氫能價值鏈中的檢驗。

從採購方式來看,到2025年,外包將佔日本測試、檢驗和認證(TIC)市場佔有率的62.27%,預計到2031年,該模式將以5.15%的最高複合年成長率成長。這主要是由於每個汽車消音室的投資額高達400萬至600萬美元,以及長循環電池測試儀的相關成本高達200萬美元。對外部服務的日益依賴表明,日本TIC市場對具成本效益解決方案的需求不斷成長。日益複雜的合規要求和不斷升級的檢驗基礎設施的需求進一步加劇了這一趨勢,使得大多數製造商自行擴建在經濟上效率低下。

隨著混合模式的日益普及,企業越來越需要進行遠端檢測試點專案並投入大量資金,這促使他們將專案實施外包給第三方。因此,預計未來幾年日本檢測、檢驗和認證 (TIC) 市場的外包比例將進一步擴大。這一趨勢表明,企業越來越依賴專業的第三方服務提供者來滿足行業不斷變化的需求。此外,人工智慧驅動的檢測和基於雲端的合規平台等數位化保障模式的日益普及也推動了這一轉變,這些模式既能減少對現場工作的依賴,又能提高審核頻率和可追溯性。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 汽車、生命科學和環境領域的監管更加嚴格。

- 工業 4.0 的日益複雜化正在推動對數位化資訊通訊技術的需求。

- 電動車和先進出行技術(電池、ADAS、網路安全)的安全要求

- 延長基礎設施和可再生能源專案的壽命

- 新興氫能和氨價值鏈的認證需求

- 高速磁浮列車和鐵路電氣化將加快架空線路巡檢速度。

- 市場限制因素

- 缺乏資本密集型先進實驗室和熟練人員

- 因國內標準與國際標準不一致而產生的調整成本

- 遠端和基於雲端的資訊通訊技術中數據主權面臨的障礙

- 低附加價值製造業的減少抑制了例行檢查的數量。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 市場宏觀經濟趨勢的評估

第5章 市場規模與成長預測

- 按服務類型

- 測試

- 檢查

- 認證

- 透過採購方式

- 內部實施

- 外包

- 按行業

- 消費品和零售

- 資訊通訊技術/通訊

- 汽車和交通運輸

- 航太/國防

- 石油、天然氣和石化產品

- 能源與公共產業

- 工業製造和機械

- 化學/材料

- 建築和基礎設施

- 生命科學與醫療保健

- 食品/農業/飲料

- 其他

- 按服務交付方式

- 現場

- 異地/檢查室

- 遠端/數位

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- SGS Japan Inc.

- Bureau Veritas Japan Co., Ltd.

- Intertek Testing Services Japan KK

- TUV SUD Japan Ltd.

- TUV Rheinland Japan Ltd.

- UL Solutions Japan Inc.

- Japan Quality Assurance Organization(JQA)

- Nippon Kaiji Kyokai(ClassNK)

- Japan Electrical Safety and Environment Technology Laboratories(JET)

- Kaken Test Center

- ALS Japan Co., Ltd.

- Eurofins Scientific Japan KK

- Mistras Group Japan

- Applus+Japan KK

- Element Materials Technology Japan

- DEKRA Certification Japan KK

- NIPPON Kaiji Kyokai Classification Society

- Japan Testing Laboratory Co., Ltd.

- NTT Advanced Technology Corp.(Compliance Test Services)

- Sanwa Kokusai Test Center

- Japan Food Research Laboratories

- Environmental Control Center Co., Ltd.

- TechnoSuruga Laboratory Co., Ltd.

- Japan Inspection Association

- Chiyoda Kenko Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the japan testing, inspection, and certification (TIC) market size is expected to increase from USD 30.26 billion in 2025 to USD 31.68 billion in 2026 and reach USD 39.65 billion by 2031, growing at a CAGR of 4.59% over 2026-2031.

This report is Segmented by Service Type (Testing, Inspection, and Certification), Sourcing Type (In-House and Outsourced), Industry Vertical (Consumer Goods and Retail, ICT and Telecom, Automotive and Transportation, and More), Mode of Service Delivery (On-Site, Off-Site Laboratory, and Remote / Digital). The Market Forecasts are Provided in Terms of Value (USD).

Japan Testing, Inspection, And Certification (TIC) Market Trends and Insights

Rising Regulatory Stringency Across Automotive, Life Sciences and Environment

New vehicle models must clear UN No. 155 cybersecurity audits, regenerative-medicine sponsors have to submit 24-month real-world evidence, and utilities face ultra-trace PFAS limits. These overlapping mandates expand compliance scopes and shorten approval windows, so companies allocate larger budgets to established laboratories. Market leaders capitalize on their ISO 17025 and ISO 17065 track records to secure multi-year contracts, reinforcing the Japan testing, inspection, and certification market dominance of accredited providers. Market leaders capitalize on their ISO 17025 and ISO 17065 track records to secure multi-year contracts, reinforcing the Japan testing, inspection, and certification market dominance of accredited providers.

EV and Advanced Mobility Safety Requirements

From 2025-2027, every lithium-ion module must demonstrate five-minute thermal-runaway containment, ADAS algorithms must pass ISO 23792 and ISO 34502 scenarios, and vehicle controllers require penetration tests. Automakers redirect validation spend from combustion systems to high-voltage, high-data-rate platforms, raising demand for USD 3-5 million abuse chambers and 800-volt anechoic cells. The result is a rapid surge in specialized battery, radar, and cybersecurity orders across the Japan testing, inspection, and certification market. Japan's strong position in automotive manufacturing and next-generation mobility technologies further accelerates investments in advanced testing infrastructure. Growing production of electric and software-defined vehicles is increasing demand for specialized certification services, supporting sustained expansion of the TIC market.

Capital-Intensive Advanced Labs and Skilled-Staff Shortages

Capital outlays ranging from USD 5-15 million for anechoic chambers and GMP cleanrooms pose significant barriers for new entrants and exert pressure on mid-tier laboratories, as these investments require substantial financial resources and long-term planning. Despite a projected gap of 500 engineers by 2030, firms are hastening their automation efforts to address workforce shortages and improve operational efficiency. However, the high costs associated with integrating automation technologies and the extensive retraining required for existing staff are hindering a swift ramp-up of these initiatives. Additionally, capacity constraints, driven by limited resources and increasing demand, are extending turnaround times for testing, inspection, and certification processes. These delays are negatively impacting the overall growth potential of Japan's testing, inspection, and certification market, as companies struggle to meet market demands efficiently.

Other drivers and restraints analyzed in the detailed report include:

- Industry 4.0 Complexity Boosting Demand for Digital TIC

- Infrastructure Life-Extension and Renewable-Energy Projects

- Fragmented Domestic and International Standard Alignment Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, testing accounted for 58.23% of the revenue, driven by high-value orders in destructive battery abuse, bioequivalence trials, and microbiology assays. Meanwhile, certification is poised to surpass testing, boasting a projected 5.26% CAGR, fueled by the demand for third-party marks in hydrogen stations, offshore wind turbines, and expedited medical devices. The Japan TIC Market is witnessing significant growth due to advancements in renewable energy and medical technology sectors. This evolution is further supported by stricter regulatory convergence with international standards and increasing cross-border product approvals, which amplify the importance of globally recognized certification bodies.

Voluntary eco-labels and lender-mandated due-diligence reports elevate recurring surveillance audits, so laboratories pivot to ISO 19870 hydrogen and renewable-energy certificates. This transition will gradually redistribute fees, yet the Japan testing, inspection, and certification market size for testing remains the largest absolute pool through 2031. Japan's national hydrogen strategy is further accelerating certification demand for hydrogen production, storage, and renewable infrastructure projects. In parallel, increasing cross-border energy trade requirements and stricter decarbonization reporting frameworks are pushing TIC providers to expand specialized verification capabilities across the hydrogen value chain.

By sourcing type, outsourced engagements held 62.27% of the Japan testing, inspection, and certification market share in 2025, while the same model registers the highest projected 5.15% CAGR to 2031. This was largely due to the USD 4-6 million investment in each automotive anechoic chamber and the USD 2 million cost associated with long-cycle battery testers. The increasing reliance on outsourced services highlights the growing demand for cost-effective solutions in the Japan TIC market. This trend is further reinforced by rising complexity in compliance requirements and the need for continuous upgrades in testing infrastructure, which makes in-house expansion less economically efficient for most manufacturers.

As hybrid models gain traction, enterprises, faced with new remote-inspection pilots and significant capital requirements, increasingly turn to third parties for project execution. As a result, the portion of Japan's testing, inspection, and certification (TIC) market that is outsourced is set to expand further in the coming years. This trend highlights the growing reliance on specialized third-party providers to meet evolving industry demands. This shift is also supported by the rising adoption of digital assurance models, where AI-enabled inspections and cloud-based compliance platforms reduce on-site dependency while improving audit frequency and traceability.

Complete Report Scope:

- By Service Type

- Testing

- Inspection

- Certification

- By Sourcing Type

- In-house

- Outsourced

- By Industry Vertical

- Consumer Goods and Retail

- ICT and Telecom

- Automotive and Transportation

- Aerospace and Defense

- Oil, Gas and Petrochemicals

- Energy and Utilities

- Industrial Manufacturing and Machinery

- Chemicals and Materials

- Construction and Infrastructure

- Life Sciences and Healthcare

- Food, Agriculture and Beverage

- Others Industry Verticals

- By Mode of Service Delivery

- On-site

- Off-site / Laboratory

- Remote / Digital

List of Companies Covered in this Report:

- SGS Japan Inc.

- Bureau Veritas Japan Co., Ltd.

- Intertek Testing Services Japan K.K.

- TUV SUD Japan Ltd.

- TUV Rheinland Japan Ltd.

- UL Solutions Japan Inc.

- Japan Quality Assurance Organization (JQA)

- Nippon Kaiji Kyokai (ClassNK)

- Japan Electrical Safety and Environment Technology Laboratories (JET)

- Kaken Test Center

- ALS Japan Co., Ltd.

- Eurofins Scientific Japan K.K.

- Mistras Group Japan

- Applus+ Japan K.K.

- Element Materials Technology Japan

- DEKRA Certification Japan K.K.

- NIPPON Kaiji Kyokai Classification Society

- Japan Testing Laboratory Co., Ltd.

- NTT Advanced Technology Corp. (Compliance Test Services)

- Sanwa Kokusai Test Center

- Japan Food Research Laboratories

- Environmental Control Center Co., Ltd.

- TechnoSuruga Laboratory Co., Ltd.

- Japan Inspection Association

- Chiyoda Kenko Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Regulatory Stringency Across Automotive, Life Sciences and Environment

- 4.2.2 Industry 4.0 complexity boosting demand for digital TIC

- 4.2.3 EV and Advanced Mobility Safety Requirements (Battery, ADAS, Cybersecurity)

- 4.2.4 Infrastructure Life-Extension and Renewable-Energy Projects

- 4.2.5 Certification Needs in Emerging Hydrogen and Ammonia Value Chains

- 4.2.6 High-Speed Maglev and Rail Electrification Driving Catenary Inspections

- 4.3 Market Restraints

- 4.3.1 Capital-Intensive Advanced Labs and Skilled-Staff Shortages

- 4.3.2 Fragmented Domestic / International Standard Alignment Costs

- 4.3.3 Data-Sovereignty Hurdles for Remote and Cloud-Based TIC

- 4.3.4 Shrinking Low-Value Manufacturing Segments Curbing Routine Testing Volumes

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Testing

- 5.1.2 Inspection

- 5.1.3 Certification

- 5.2 By Sourcing Type

- 5.2.1 In-house

- 5.2.2 Outsourced

- 5.3 By Industry Vertical

- 5.3.1 Consumer Goods and Retail

- 5.3.2 ICT and Telecom

- 5.3.3 Automotive and Transportation

- 5.3.4 Aerospace and Defense

- 5.3.5 Oil, Gas and Petrochemicals

- 5.3.6 Energy and Utilities

- 5.3.7 Industrial Manufacturing and Machinery

- 5.3.8 Chemicals and Materials

- 5.3.9 Construction and Infrastructure

- 5.3.10 Life Sciences and Healthcare

- 5.3.11 Food, Agriculture and Beverage

- 5.3.12 Others Industry Verticals

- 5.4 By Mode of Service Delivery

- 5.4.1 On-site

- 5.4.2 Off-site / Laboratory

- 5.4.3 Remote / Digital

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 SGS Japan Inc.

- 6.4.2 Bureau Veritas Japan Co., Ltd.

- 6.4.3 Intertek Testing Services Japan K.K.

- 6.4.4 TUV SUD Japan Ltd.

- 6.4.5 TUV Rheinland Japan Ltd.

- 6.4.6 UL Solutions Japan Inc.

- 6.4.7 Japan Quality Assurance Organization (JQA)

- 6.4.8 Nippon Kaiji Kyokai (ClassNK)

- 6.4.9 Japan Electrical Safety and Environment Technology Laboratories (JET)

- 6.4.10 Kaken Test Center

- 6.4.11 ALS Japan Co., Ltd.

- 6.4.12 Eurofins Scientific Japan K.K.

- 6.4.13 Mistras Group Japan

- 6.4.14 Applus+ Japan K.K.

- 6.4.15 Element Materials Technology Japan

- 6.4.16 DEKRA Certification Japan K.K.

- 6.4.17 NIPPON Kaiji Kyokai Classification Society

- 6.4.18 Japan Testing Laboratory Co., Ltd.

- 6.4.19 NTT Advanced Technology Corp. (Compliance Test Services)

- 6.4.20 Sanwa Kokusai Test Center

- 6.4.21 Japan Food Research Laboratories

- 6.4.22 Environmental Control Center Co., Ltd.

- 6.4.23 TechnoSuruga Laboratory Co., Ltd.

- 6.4.24 Japan Inspection Association

- 6.4.25 Chiyoda Kenko Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

2026-2030年全球測驗、檢驗和認證市場

2026-2030年全球測驗、檢驗和認證市場 測試、檢驗和認證市場:2026-2032年全球市場預測(按服務類型、採購方式、技術、合規要求、應用、組織規模和最終用戶行業分類)證書測試市場:2026-2032年全球市場預測(依測試服務、階段、產業、部署類型、最終用戶和組織規模分類)

測試、檢驗和認證市場:2026-2032年全球市場預測(按服務類型、採購方式、技術、合規要求、應用、組織規模和最終用戶行業分類)證書測試市場:2026-2032年全球市場預測(依測試服務、階段、產業、部署類型、最終用戶和組織規模分類) 印度測試、檢驗和認證 (TIC) 市場:市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031)法國的測試、檢定和認證 (TIC):市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031)

印度測試、檢驗和認證 (TIC) 市場:市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031)法國的測試、檢定和認證 (TIC):市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031) 2026-2030年全球人工智慧測試與檢驗市場

2026-2030年全球人工智慧測試與檢驗市場 2026 年至 2035 年測試、檢驗和認證服務市場的商業機會、成長要素、產業趨勢和預測。

2026 年至 2035 年測試、檢驗和認證服務市場的商業機會、成長要素、產業趨勢和預測。 測試、檢驗和認證市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、流程、部署模式、最終用戶和解決方案分類

測試、檢驗和認證市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、流程、部署模式、最終用戶和解決方案分類 服飾、鞋類和皮革製品 (AFL) 的檢測、檢驗和認證 (TIC) 市場:按服務類型、行業和地區分類測試、檢驗和認證 (TIC) 市場:按類型、行業和地區分類

服飾、鞋類和皮革製品 (AFL) 的檢測、檢驗和認證 (TIC) 市場:按服務類型、行業和地區分類測試、檢驗和認證 (TIC) 市場:按類型、行業和地區分類