|

市場調查報告書

商品編碼

2063297

航運和海事資訊通訊技術:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Marine And Shipping TIC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

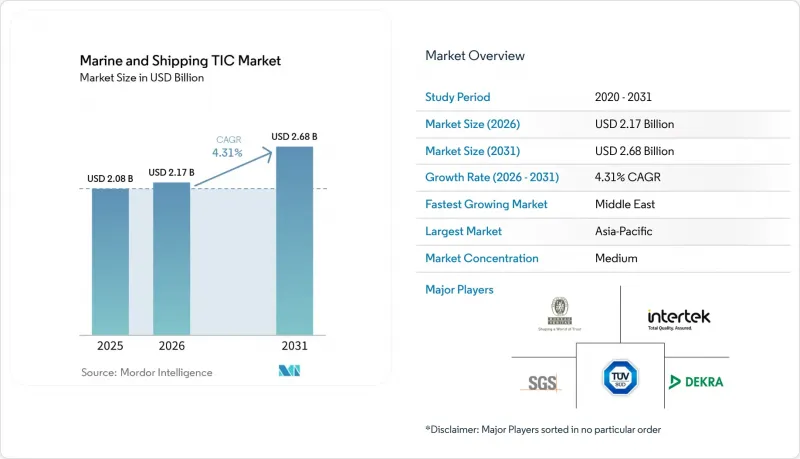

根據 Mordor Intelligence 估計,船舶和航運 TIC 市場規模在 2025 年為 20.8 億美元,到 2026 年成長至 21.7 億美元,到 2031 年成長至 26.8 億美元,2026 年至 2031 年的複合年成長率為 4.31%。

本報告按服務類型(測試、檢驗、認證)、採購類型(內部、外包)、服務交付方式(現場、異地/實驗室、遠端/數位化)以及地區(北美、歐洲、亞太、中東和非洲、南美)進行細分。市場預測以美元計價。

全球造船及航運TIC市場趨勢及洞察

強制性脫碳正在推動替代燃料測試。

國際海事組織(IMO)設定了碳排放強度降低目標,計畫從2026年的11%逐步提高到2030年的21.5%,並要求船東在商業營運前對氨、甲醇和氫動力推進系統進行檢驗。 DNV的歐盟資助的「Ammonia24」計畫已發布安全指南,使得39艘氨燃料船舶的訂單得以推進。這顯示標準化如何加速資本投資。每艘動力來源替代燃料的新船都需要進行試運行試驗、中期檢驗和改裝後檢驗,從而創造了柴油船隊先前所不具備的持續收入來源。勞氏暫存器也順應了這項轉變,於2025年發布了氫燃料電池安裝指南,為船廠提供了關於通風、洩漏檢測和防爆設計的明確指南。隨著基於目標的標準取代了強制性規則,船級社可以自由地為早期採用者提供其昂貴的測試方案。

離岸風力發電設施的加速建設使得船舶保固檢驗變得特別必要。

為了滿足歐洲75吉瓦離岸風力發電裝置容量和380吉瓦的規劃需求,自升式平台、動力定位系統和海底電纜安裝都需要持續的船舶品質保證檢驗。 DNV於2026年2月為Austoed公司4.2吉瓦的Hornsea 3和4專案頒發的合格證書,便是目前起重機載重曲線和天氣窗口建模領域高技術嚴謹性的一個典型例證。法國船級社(Bureau Veritas)和美國船級社(ABS)也在2026年初為重型裝運船隻頒發了類似的認證,加劇了利潤豐厚的檢驗業務的競爭。諸如在50公尺浪高的海況下對葉片進行公差檢驗等新要求,遠遠超出了傳統貨物檢驗的範圍,這有望帶來更高的費用收入。必維集團海事與海洋工程部門報告稱,2023 年收入為 11.6 億歐元(12.4 億美元),其中離岸風力發電收入佔比不斷增加,凸顯了該部門對盈利的重大影響。

新興國家合格船舶檢驗員短缺

東南亞、非洲和南美洲面臨替代燃料系統、數位雙胞胎檢驗和先進無損檢測方面認證檢驗員的嚴重短缺。儘管國際海事研究所 (IIMS) 和勞暫存器船級社海事學院等機構開展了相關項目,但人才培養體系仍然脆弱。中國和韓國佔全球造船訂單的80%以上,但該地區的從業人員難以掌握國際船級社協會 (IACS) 的統一要求,導致核准前置作業時間延長。印度船級社 (IRS) 依賴外國專家進行複雜的檢驗,推高了專案成本。 STCW公約下缺乏關於人工智慧驅動診斷的強制性繼續教育,這意味著技能差距依然存在,尤其是在船舶停留時間長的非洲港口。

細分市場分析

認證領域成長最為迅速,複合年成長率達4.47%,反映出船東需要證明自主航行和替代燃料的安全性。在法定船體厚度檢驗和壓艙水檢驗的支持下,檢驗領域到2025年仍將佔最大佔有率,達到45.23%。隨著數位雙胞胎和軟體檢驗技術的成熟,船舶和航運檢驗認證服務市場的規模預計將穩定成長。日本船級社(ClassNK)的「AUTO-Nav2 (All)」標籤和法國船級社(Bureau Veritas)的「Augmented Surveyor 3D」平台的日益普及表明,即時數據的流動正在模糊檢驗和認證之間的界限。船東擴大將實驗室測試納入綜合檢驗契約,這簡化了行政流程,並將收入轉移到提供綜合服務的供應商身上。

儘管檢測服務的擴張速度緩慢,但燃油品質分析和排放氣體採樣對於合規性仍然至關重要。結合無人機影像和雷射雷達掃描的持續監測訂閱服務正在推動經常性收入的成長,並促進從一次性報告向數據驅動的全生命週期保障的結構性轉變。隨著遠端工具的普及,認證正變得具有戰略意義,因為監管機構和保險公司在接受基於演算法和感測器的證據時,會依賴船級社的認可。

區域分析

預計到2025年,亞太地區將佔全球收入的34.41%,這主要得益於中國在造船領域的領先地位,其訂單量佔全球52.8%,以及韓國28.1%的累積訂單。日本船級社(ClassNK)預計將在船舶數量方面位居榜首,而中國船級社則躋身總噸位前五,這反映了該地區在造船業的活躍地位。日本的「MEGURI2040」計畫於2026年初認證了四艘自主航行船舶,刺激了對新型測試框架的需求。印度船舶登記局(IRS)自2025年1月以來已註冊了115艘船舶,並在沙烏地阿拉伯開設了辦事處,將其在亞太地區的專業知識擴展到周邊市場。韓國船舶登記局 (KR) 預測,2025 年銷售額將達到 2,060 億韓元(1.55 億美元),年增 4%,並計劃在 2026 年進一步實現收入成長,這主要得益於國內造船活動的增加。

預計到2031年,中東地區將以5.61%的複合年成長率成為所有地區中成長最快的地區。沙烏地阿拉伯的港口投資以及阿拉伯聯合大公國(阿拉伯聯合大公國)物流網路的擴張,正吸引那些尋求接近性新建設碼頭和海上能源項目的船級社。此外,日益緊張的地緣政治局勢推高了霍爾木茲海峽的戰爭風險溢價,從而增強了對獨立船體和引擎檢驗的需求,並推動了檢驗業務的成長。印度船級社利雅得分店憑藉其戰略優勢,掌握了這些機會。

由於船隊發展成熟,歐洲和北美地區的成長率低於平均水平,但它們在離岸風力發電、船舶品質保證檢驗和數位雙胞胎認證等高回報細分市場中佔據主導地位。 DNV的布雷默哈芬離岸風電能力中心(擁有100名工程師)和勞氏船級社的休士頓辦事處凸顯了其對先進能力的持續投入。非洲和南美洲由於檢驗員數量和測試基礎設施有限而落後,但遠端檢驗和培訓的夥伴關係正在逐步釋放其潛力。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 強制性脫碳正在加速替代燃料的測試。

- 擴大數位雙胞胎技術在預測性維護檢驗的應用

- 自主船舶的成長增加了對認證的需求。

- 對壓艙水水處理適用性進行更嚴格的測試。

- 隨著離岸風力發電設施的加速發展,船舶保固檢驗將變得不可或缺。

- 船體完整性檢驗的保險費獎勵

- 市場限制因素

- 新興國家合格船舶檢驗員短缺

- 先進非破壞性檢測設備高成本

- 船旗國法規結構的碎片化

- 地緣政治緊張影響跨境檢測機會

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按服務類型

- 測試

- 檢查

- 認證

- 依採購類型

- 內部

- 外包

- 按服務交付方式

- 現場

- 異地/檢查室

- 遠端/數位

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太國家

- 中東

- 以色列

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Bureau Veritas SA

- Intertek Group plc

- SGS SA

- TUV SUD AG

- DEKRA SE

- Lloyd's Register Group Limited

- DNV AS

- American Bureau of Shipping

- Nippon Kaiji Kyokai(ClassNK)

- RINA SpA

- China Classification Society

- Korean Register

- Indian Register of Shipping

- Tasneef(Emirates Classification Society)

- Russian Maritime Register of Shipping

- Polish Register of Shipping

- Hellenic Register of Shipping

- Vietnam Register

- Croatian Register of Shipping

第7章 市場機會與未來展望

According to Mordor Intelligence, the marine and Shipping TIC market size was valued at USD 2.08 billion in 2025 and is estimated to grow from USD 2.17 billion in 2026 to USD 2.68 billion by 2031, at a CAGR of 4.31% from 2026 to 2031.

This report is Segmented by Service Type (Testing, Inspection, and Certification), Sourcing Type (In-House, and Outsourced), Mode of Service Delivery (On-Site, Off-site/Laboratory, and Remote/Digital), and Geography (North America, Europe, Asia-Pacific, Middle East, Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Marine And Shipping TIC Market Trends and Insights

Decarbonization Mandates Driving Alternative Fuel Testing

The International Maritime Organization has set carbon-intensity reduction milestones that escalate from 11% in 2026 to 21.5% by 2030, obligating owners to validate ammonia, methanol, and hydrogen propulsion systems before commercial deployment. DNV's EU-funded Ammonia24 program has already issued safety guidance enabling an orderbook of 39 ammonia-fueled vessels to proceed, demonstrating how standardization accelerates capital commitments. Each alternative-fuel newbuild triggers commissioning tests, mid-term surveys, and retrofit validations, creating recurring revenue streams previously absent from diesel fleets. Lloyd's Register complemented the shift by publishing hydrogen fuel-cell installation guidelines in 2025, giving shipyards clear reference points for ventilation, leak detection, and explosion-proof design. As goal-based standards replace prescriptive rules, classification societies are free to offer proprietary testing packages at premium rates for early adopters.

Accelerated Offshore Wind Installations Necessitating Marine Warranty Surveys

Europe's 75 gigawatt installed offshore wind base and 380 gigawatt pipeline demand requires continuous marine warranty verification for jack-up vessels, dynamic positioning systems, and subsea cable equipment. DNV's compliance certificates for Orsted's 4.2 gigawatt Hornsea 3 and 4 projects, issued in February 2026, exemplify the elevated technical rigor now applied to crane load curves and weather-window modeling. Bureau Veritas and American Bureau of Shipping issued similar approvals to heavy-lift vessels in early 2026, reinforcing a competitive race for high-margin survey work. Novel requirements such as blade-tolerance checks in 50-meter seas extend well beyond conventional cargo inspections, boosting fee potential. Bureau Veritas's Marine and Offshore division reported EUR 1.16 billion (USD 1.24 billion) revenue in 2023, with offshore wind contributing a rising portion, underscoring the segment's material impact on earnings.

Shortage of Qualified Marine Surveyors in Emerging Economies

Southeast Asia, Africa, and South America lack sufficient surveyors certified in alternative-fuel systems, digital twin validation, and advanced non-destructive testing. Training pipelines remain thin despite programs from the International Institute of Marine Surveying and Lloyd's Register Maritime Academy. China and South Korea control more than 80% of global shipbuilding orders, yet regional workforces struggle to master IACS unified requirements, stretching approval lead times. Indian Register of Shipping relies on expatriate experts for complex inspections, raising project costs. Without mandated continuous education on AI-driven diagnostics under the STCW Convention, the skills gap persists, especially in African ports where detention rates stay elevated.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Digital Twin Adoption for Predictive Maintenance Verification

- Growth in Autonomous Shipping Raising Certification Demand

- High Cost of Advanced Non-Destructive Testing Equipment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Certification accounted for the fastest expansion, with a 4.47% CAGR, reflecting owners' need to prove autonomous navigation and alternative-fuel safety. Inspection remained the largest slice at 45.23% in 2025, anchored by statutory hull-thickness and ballast-water checks. The Marine and Shipping TIC market size for certification services is projected to grow steadily as digital twin and software validation mature. The rising uptake of ClassNK's AUTO-Nav2 (All) notation and Bureau Veritas's Augmented Surveyor 3D platform underscores how real-time data flows blur the boundaries between Inspection and certification. Owners increasingly bundle lab tests within integrated survey contracts, compressing administration and tilting revenue toward full-scope providers.

Testing services expand more slowly, yet fuel-quality analysis and emissions sampling remain indispensable for compliance. Continuous monitoring subscriptions tied to drone imagery and LiDAR scans expand recurring revenue, reinforcing the structural shift from one-off reports to data-driven lifecycle assurance. As remote tools proliferate, certification's strategic importance grows because regulators and insurers rely on class approvals to accept algorithmic or sensor-based evidence.

Geography Analysis

Asia-Pacific held 34.41% of 2025 revenue, propelled by China's 52.8% share of global shipbuilding orders and South Korea's 28.1% orderbook leadership. ClassNK rose to first place by vessel count, and China Classification Society climbed into the top five by gross tonnage, evidencing robust regional activity. Japan's MEGURI2040 program certified four autonomous vessels in early 2026, spurring demand for novel testing frameworks. Indian Register of Shipping delivered 115 vessels since January 2025 and opened a Saudi Arabia office, extending Asia-Pacific know-how into adjacent markets. Korean Register's revenue advanced 4% year over year to KRW 206 billion (USD 155 million) in 2025 and targets further gains in 2026, in line with rising domestic construction activity.

The Middle East is forecast to post the fastest regional CAGR at 5.61% through 2031. Saudi Arabia's port investments and the United Arab Emirates' logistics expansion attract classification societies seeking proximity to greenfield terminals and offshore energy projects. Survey demand also heightens when geopolitical flare-ups raise war-risk premiums in the Strait of Hormuz, intensifying calls for independent hull and machinery inspections. Indian Register of Shipping's Riyadh branch illustrates strategic positioning to capture these opportunities.

Europe and North America exhibit below-average growth due to mature fleets, but they dominate high-margin niches such as offshore wind, marine warranty surveys, and digital-twin certifications. DNV's Bremerhaven Offshore Wind Competence Center, with 100 engineers, and Lloyd's Register's Houston office underline continued investment in advanced capabilities. Africa and South America lag due to limited surveyor pools and testing infrastructure, though remote inspection and training partnerships are gradually unlocking latent potential.

- Bureau Veritas SA

- Intertek Group plc

- SGS SA

- TUV SUD AG

- DEKRA SE

- Lloyd's Register Group Limited

- DNV AS

- American Bureau of Shipping

- Nippon Kaiji Kyokai (ClassNK)

- RINA S.p.A.

- China Classification Society

- Korean Register

- Indian Register of Shipping

- Tasneef (Emirates Classification Society)

- Russian Maritime Register of Shipping

- Polish Register of Shipping

- Hellenic Register of Shipping

- Vietnam Register

- Croatian Register of Shipping

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Decarbonization Mandates Driving Alternative Fuel Testing

- 4.2.2 Expanding Digital Twin Adoption for Predictive Maintenance Verification

- 4.2.3 Growth in Autonomous Shipping Raising Certification Demand

- 4.2.4 Stricter Ballast Water Treatment Compliance Testing

- 4.2.5 Accelerated Offshore Wind Installations Necessitating Marine Warranty Surveys

- 4.2.6 Insurance Premium Incentives for Verified Hull Integrity

- 4.3 Market Restraints

- 4.3.1 Shortage of Qualified Marine Surveyors in Emerging Economies

- 4.3.2 High Cost of Advanced Non-Destructive Testing Equipment

- 4.3.3 Fragmented Regulatory Framework Across Flag States

- 4.3.4 Geopolitical Tensions Impacting Cross-Border Inspection Access

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Testing

- 5.1.2 Inspection

- 5.1.3 Certification

- 5.2 By Sourcing Type

- 5.2.1 In-house

- 5.2.2 Outsourced

- 5.3 By Mode of Service Delivery

- 5.3.1 On-site

- 5.3.2 Off-site / Laboratory

- 5.3.3 Remote / Digital

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Middle East

- 5.4.4.1 Israel

- 5.4.4.2 Saudi Arabia

- 5.4.4.3 United Arab Emirates

- 5.4.4.4 Turkey

- 5.4.4.5 Rest of Middle East

- 5.4.5 Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Egypt

- 5.4.5.3 Rest of Africa

- 5.4.6 South America

- 5.4.6.1 Brazil

- 5.4.6.2 Argentina

- 5.4.6.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Bureau Veritas SA

- 6.4.2 Intertek Group plc

- 6.4.3 SGS SA

- 6.4.4 TUV SUD AG

- 6.4.5 DEKRA SE

- 6.4.6 Lloyd's Register Group Limited

- 6.4.7 DNV AS

- 6.4.8 American Bureau of Shipping

- 6.4.9 Nippon Kaiji Kyokai (ClassNK)

- 6.4.10 RINA S.p.A.

- 6.4.11 China Classification Society

- 6.4.12 Korean Register

- 6.4.13 Indian Register of Shipping

- 6.4.14 Tasneef (Emirates Classification Society)

- 6.4.15 Russian Maritime Register of Shipping

- 6.4.16 Polish Register of Shipping

- 6.4.17 Hellenic Register of Shipping

- 6.4.18 Vietnam Register

- 6.4.19 Croatian Register of Shipping

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

裝卸整平機市場規模、佔有率和成長分析:按操作方式、核心材料成分、最終用途產業、分銷管道和地區分類-2026-2033年產業預測

裝卸整平機市場規模、佔有率和成長分析:按操作方式、核心材料成分、最終用途產業、分銷管道和地區分類-2026-2033年產業預測 全球物流市場:市場規模、佔有率、趨勢和成長分析(2026-2034)

全球物流市場:市場規模、佔有率、趨勢和成長分析(2026-2034) 2026年全球智慧物流市場報告

2026年全球智慧物流市場報告 智慧物流自動化市場預測至2034年—全球解決方案、運輸方式、組件、技術、應用、最終用戶和區域分析

智慧物流自動化市場預測至2034年—全球解決方案、運輸方式、組件、技術、應用、最終用戶和區域分析 2026-2030年全球物流市場

2026-2030年全球物流市場 亞太地區政府和教育物流:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)按需物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)政府與教育物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)

亞太地區政府和教育物流:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)按需物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)政府與教育物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年) 全球資料中心物流市場(2026 年)2026年貨櫃存放場即時定位系統(RTLS)全球市場報告

全球資料中心物流市場(2026 年)2026年貨櫃存放場即時定位系統(RTLS)全球市場報告